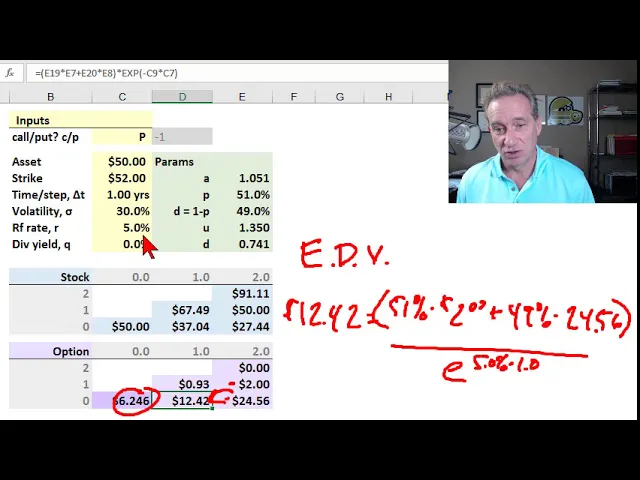

next in my sub series I'll explain the change we make to the model to accommodate the early exercise feature so now the model will handle an american-style option which can be exercised before maturity most of the model doesn't change parameters don't change stock price simulation doesn't change terminal values don't change when we do the backward induction the only thing that changes for an american-style option is that these interim nodes now become a maximum function they are the maximum of the expected discounted value which I'll review again and the intrinsic value and that is to acknowledge that at these interim nodes unlike with the european-style option this american-style option can be exercised here so it's natural to assume that the value here would be the higher of expected discounted value or intrinsic value so you share the same assumptions that we find in John hole's example 13. 10 and the big difference here is we're going to do an american-style option as opposed to a European stell option that capital P here denotes american-style meaning that this option can be exercised prior to maturity and this is one of the use cases for the binomial model that black Scholes Merton afterall is restrictive in its assumptions the classic black Scholes is really designed for a European option when we want to add features like early exercise a la american-style it's just much easier to use the binomial model binomial model is infinitely flexible so for my assumptions at following Hall's example 13:10 asset or stock price at time of purchased so that's really s Sub Zero right $50 the strike is 52 that means as a put style at the time of purchase were in the money we have two dollars of intrinsic value for the put my time step is one year so this is really unrealistic vary the time steps are usually much shorter time step of one year with only two steps unrealistically truncated binomial tree means that we have an american-style option with two years to maturity right one two steps each step is a ridiculously large one year my volatility is 30 percent per annum always per annum input assumptions here and the risk-free rate five percent also per annum in the previous videos I've covered how we calculate the parameters in particular the P is the probability of an up jump and therefore because it's binomial meaning either each node or branch of the tree either goes up or down that means that the down probability is 1 minus the P or in this case 49% and those are solved for us owing to that elegant risk-neutral valuation framework that I described to videos previously also in this example I will use the volatility to inform the calculation of the U and D those are very simple I covered those in the previous video and this is matching U and D to the volatility input so that the standard deviation of this binomial variable implied by the und equals or approximately equals this 30% so those are solved for us very simple we have those parameters and then the two steps right we start today at that stock price following this asset value initially and it either goes up or down for the tree right if if it goes up it goes up by multiplier multiplying the 1. 35 or up by 35% in this case where the volatility is ful fully 30% and that's a one-year difference so that's why that's so large on the other hand the $50.

00 could go down to thirty seven dollars and four cents so we build out the tree only two steps and then we have three terminal values and so that brings us to the backward induction and what we have there is we start with the terminal values and these terminal values are intrinsic values so that with the put option here if the stock jumps up all the way to ninety one dollars and eleven cents with a strike price of 52 well that's deeply out of the money intrinsic value is therefore zero and you'll notice I use a formula here where I take the asset price and subtract the strike price and then multiply that by this toggle value here which will be one for a call negative one for a put that allows me to use the same formula for that switches for a call or a put that's all that is and my intrinsic value you can see here is $24. 50 my terminal value if this dock takes two consecutive down jumps and goes all the way down to 27:44 after that after all that's a put so the intrinsic value here at this node would be the payoff for a European option $24 & 56789:cdefghijstuvwxyzcdefghijstuvwxyz 49% probability that's the down jump multiplied by the 24:56 and so this is the expected value of these two between these two forward nodes really it's the mean or weighted average value weighted by the probabilities but it's one year forward so we discount it continuously by dividing by E raised to the risk-free rate five percent five percent multiplied by one year in this case so divided by the five percent or you can see that's the same as multiplying by e raised to the negative five percent but that then discounts the expected value back to this node and so we call that I'm just going to abbreviate the expected discounted value I like it because it applies fundamental financial building blocks however this then and then we do that again for for this node here and we get the six dollars and about 25 cents however what we've done here is we've treated this like a european-style option which is to say we assumed it will it can only be exercised at maturity so now I'll show you the next page which makes the the single adjustment that treats this now as an american-style put so now I really do comport with halls figure or 13. 10 and this is going to be really straightforward because all of the inputs and parameters are the same and because the up-and-down are the same so is the stock price the simulated stock price tree these values are all unchanged further the terminal values are unchanged as well the only difference here when we switch the american-style put is the treatment here of these all of the interim nodes and so I'll just isolate on the fourteen dollars and 96 cents you may notice my formula makes one adjustment here's the part hopefully can see right up and above here I'm going to just draw here here's the part that's unchanged because that is my expected discounted value same as I did before what we're doing now for each of the nodes each of the interim nodes as we're saying they are equal to the maximum of the expected discounted value that we did before or the intrinsic value that's really the only change to all of the interim nodes not to the final nodes which continue to be just intrinsic value that's the only change required to switch this model to a treat it as an american-style option in this case a put is that we now have this maximum function and hopefully the logic is somewhat intuitive the idea but previously at one year that two-year option could not be exercised now it can be exercised at one year and if the intrinsic value is greater than the expected discounted value rational agent would exercise the option so it should have a higher value so in this case for this $14.

98 and forty-two cents that we calculated previously which is the expected discounted value however here at this node where the stock jumped down to thirty seven dollars and four cents the option is now much further in the money and you can see strike price of fifty two dollars minus thirty seven dollars and four cents is an intrinsic value at that point in time under this simulation of $14. 90 so the that's the value used in the max function that's the change you might notice this note above here at 93 cents does not change after all at this node the intrinsic value would be zero that option be out of the money however this node changes and and it feeds into the calculation of this node which is the price of the option and here at time zero that intrinsic value is only two dollars so that's not what's getting used the expected discounted values getting used however it's informed by a slightly higher value at this node so that it increases to seven dollars and forty three cents which was an increase from what we did before we got about six dollars and twenty five since six for six I'm sorry six dollars 0.