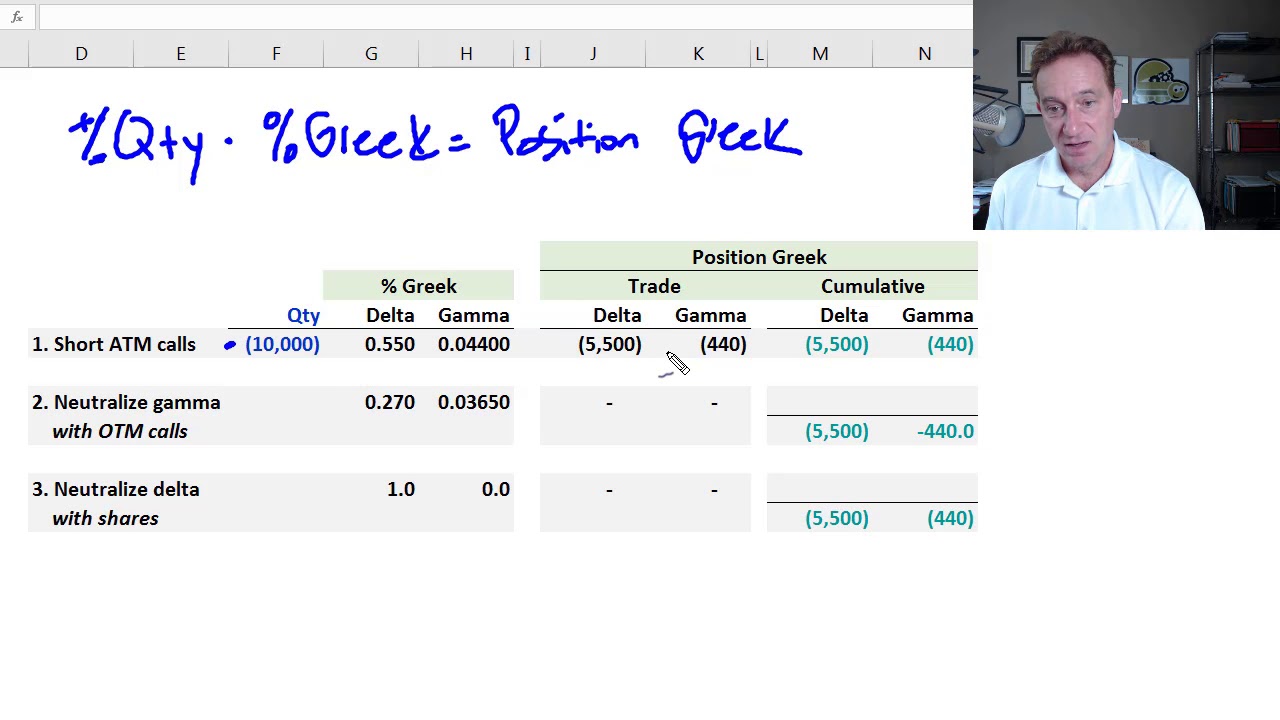

my previous two videos explained option delta then option gamma now I'm going to tie them together to explain and visually interpret what it means to have Delta plus gamma exposure when we are either long or short the call or the put option and I do that I'll use a single simple formula quantity multiplied by percentage Greek equals position Greek so we'll distinguish between percentage Greek and position Greek help us avoid a confusion and understand why percentage gamma is always positive but our position gamma can be negative or is negative if we have a short option

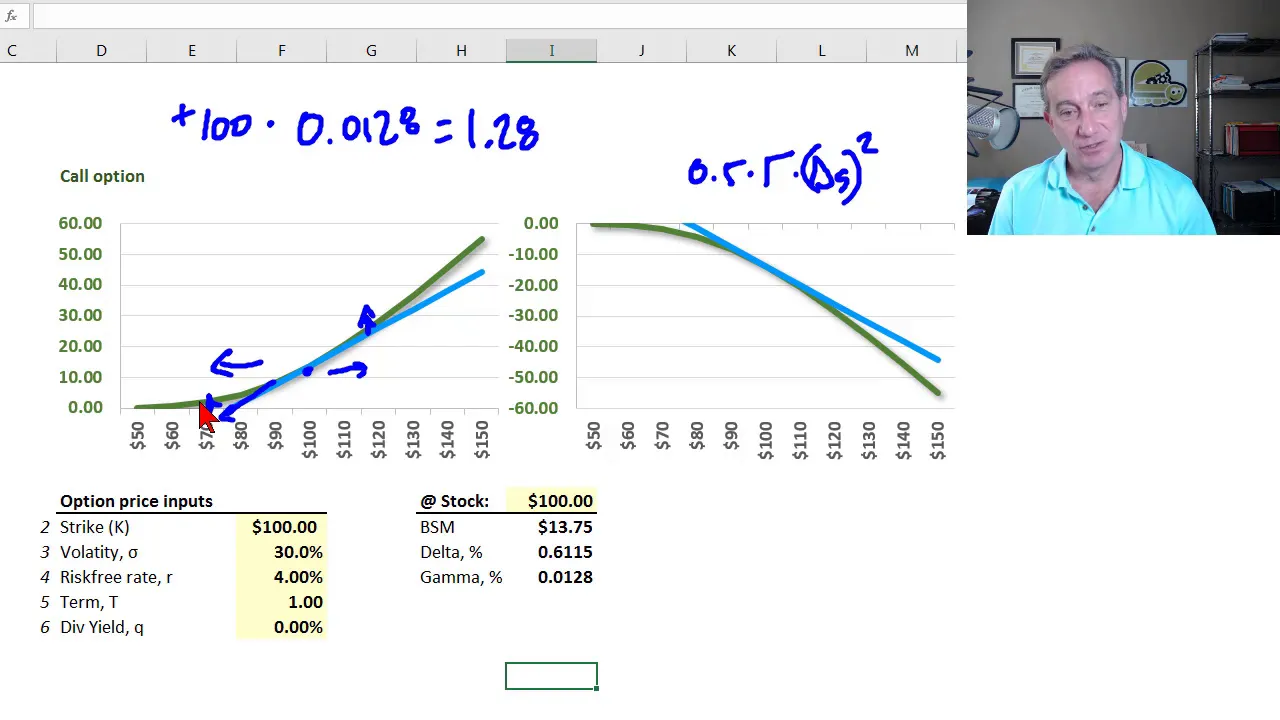

position I'm showing two different graphs but these are just opposite sides of the same single underlying trade so way to think about this is on the left can be U and on the right will be me as your counterparty over here right this sheet is for a call option on the next sheet is for a put option so on the Left we have your person your perspective as a buyer or the one who is a long position in this option and let's say you bought it from me so I sold it or I wrote the

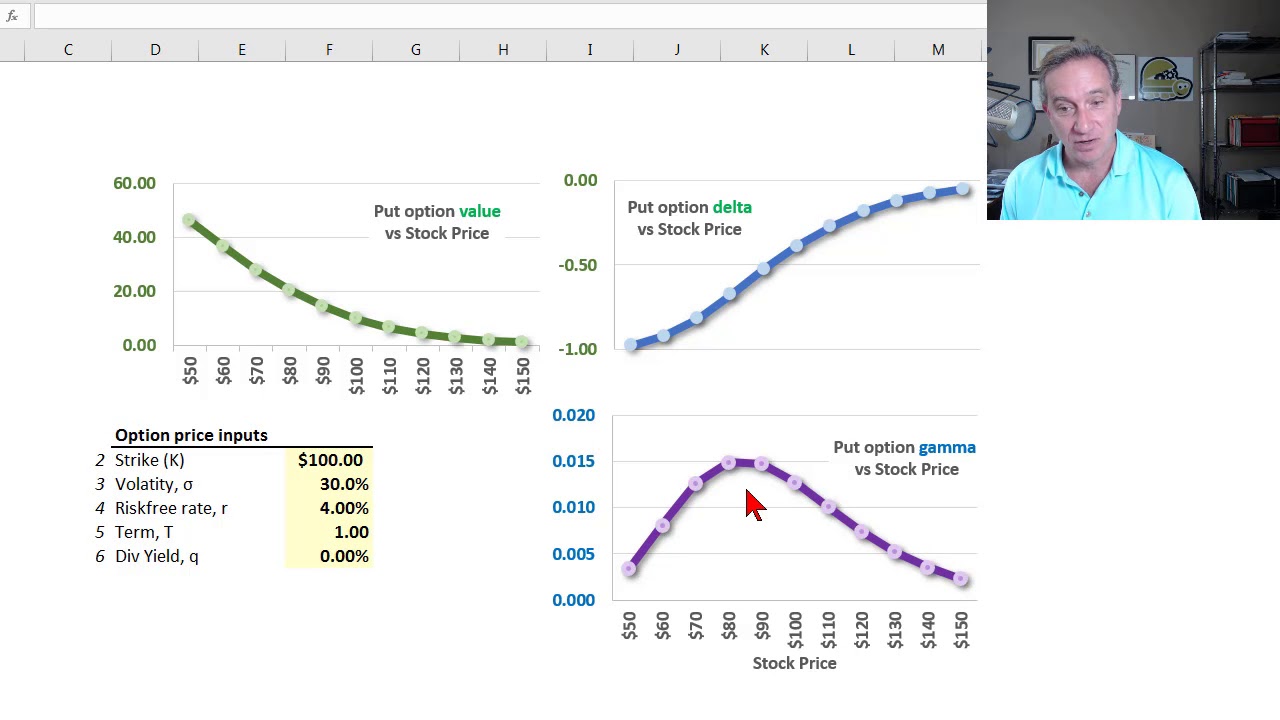

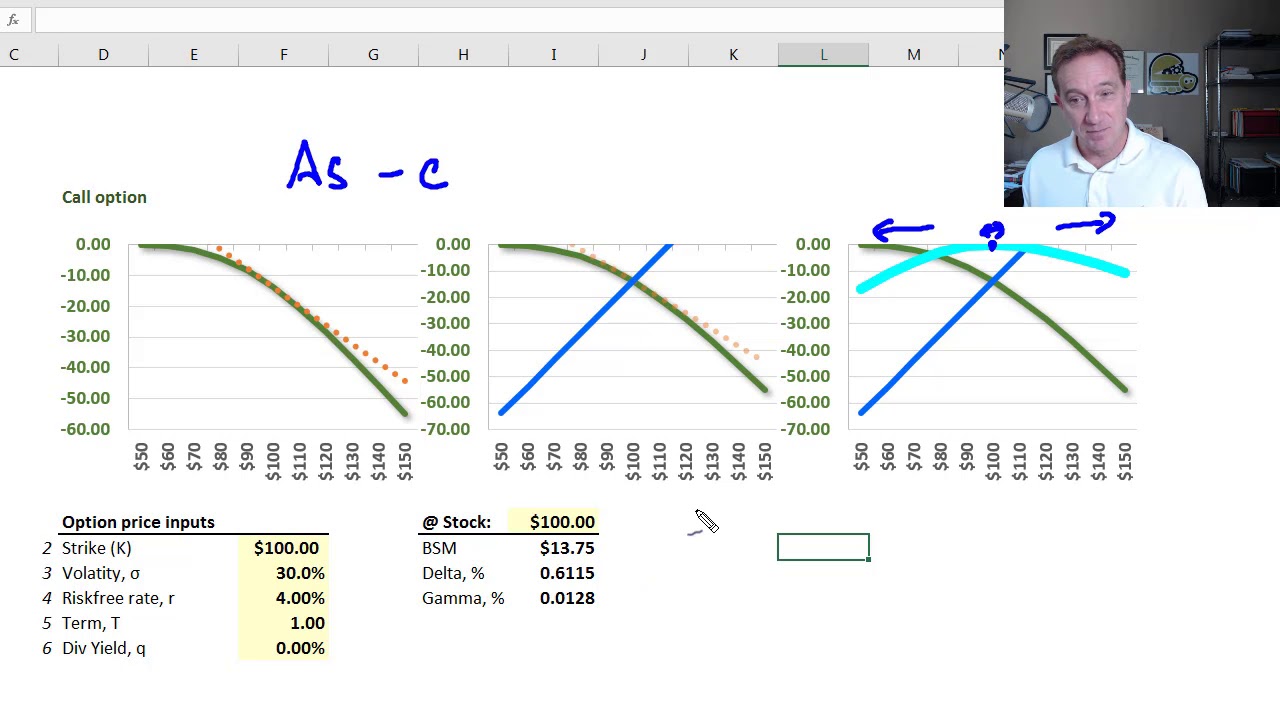

option then this is my perspective as the one who has a short position and the option but they are mirror images of each other on the lower left we have option inputs as usual and I have tied beats together so that if we and in this downloadable worksheet so that if you change the stock price for example my tangent lines those are the ones in blue do shift to their appropriate location so right here I'm showing the tangent line where the point of tangency is the $100 and this is an at the money option so

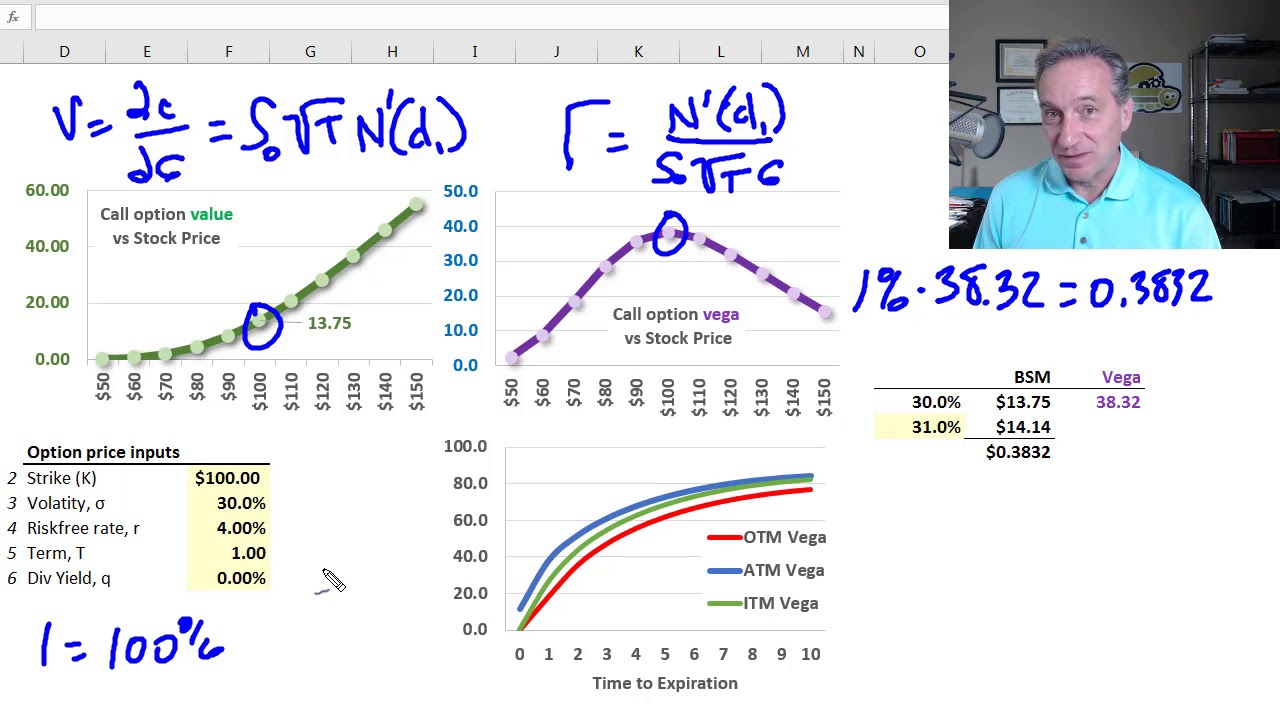

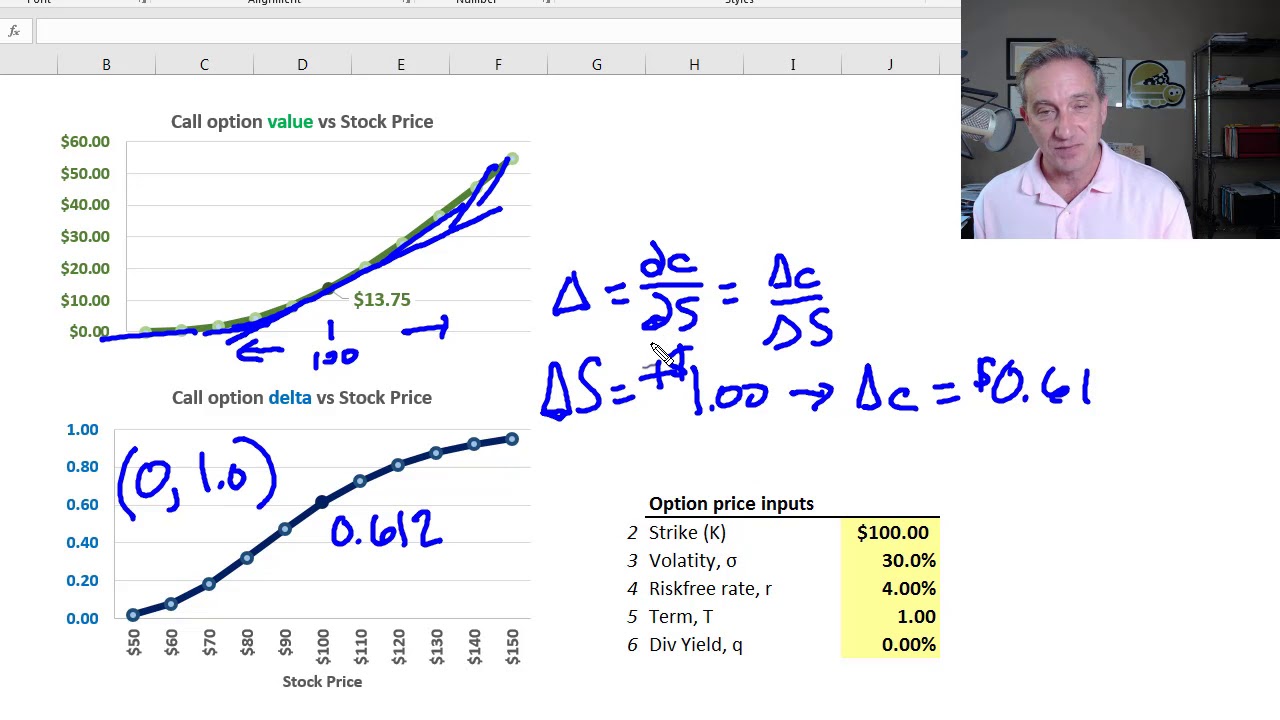

for you on the left long position the call option the black Scholes Merton value of this option according to these assumptions when the stock price is 100 and we're at the money is $13.75 that's the where we hit the y-axis here right we have a graph of on the Y axons call option value as it varies with a change in the stock price on the x-axis and so now tying Deltan gamma together for both of our relative perspectives here's the key formula very simple formula we want to note to recognize the our position exposure our

position Greek so let's look at the position Delta all we need to do is multiply the quantity times the percentage Greek so in this case I'm going to say we're using Delta so I'm saying the percentage Delta right it's just quantity times the percentage Greek in this case quantity x multiplied by the percentage Delta cover Delta to videos back in the playlist and I mentioned that technically we call it percentage Delta but it's a confusing in this case because the Delta percentage Delta is a unitless quantity but we call it a percentage Delta we could

call it a per option Delta as well for a call option of course we do know that it needs to be between 0 and 1 so it's about where we expect and at the money call option quantity multiplied by percentage Greek in this case the percentage Delta is going to give us the position Greek in this case the position Delta that's the important formula that I always try to really really emphasize to avoid the confusions that we're gonna explain shortly we multiply the quantity by the percentage Greek to get the position in Greek so let

me do that for Delta specifically from your perspective as the one who is long the call option and let's just now say that we're dealing with a single contract so we have a quantity that a single contract is for 100 options you've purchased one option contract in this underlying stock what is your position Delta well we take the quantity that's 100 we multiply it by the percentage Delta zero point 6 1 1 5 and we see that your position Delta is 61 point one five and then I'm going to be explicit here about the fact

this is a positive because you purchased or are long and of course this is positive as well it must be and so your position Delta is positive 61 15 how do we interpret that very easily actually well it's characterized by movement along the blue line in this case for a contract of 100 options stock price increases by $1 we get you game your long your position gains by about sixty one dollars very simple now what about my perspective same single rule I use the same single rule throughout all four examples I am short 100 call

options so I'm gonna move any move over here or make sure I make sure I'm focused on my position as the counterparty I am short when I don't call options and so I need to use negative 100 for the quantity negative signifies the fact that I'm sure I multiplied by the percentage Delta 0.6 1 1 5 and so my position Delta is negative 60 1 15 so you see how this distinction between the percentage Greek in this case percentage Delta and the position Greek in this case position Delta is important my interpretation similar I'm your

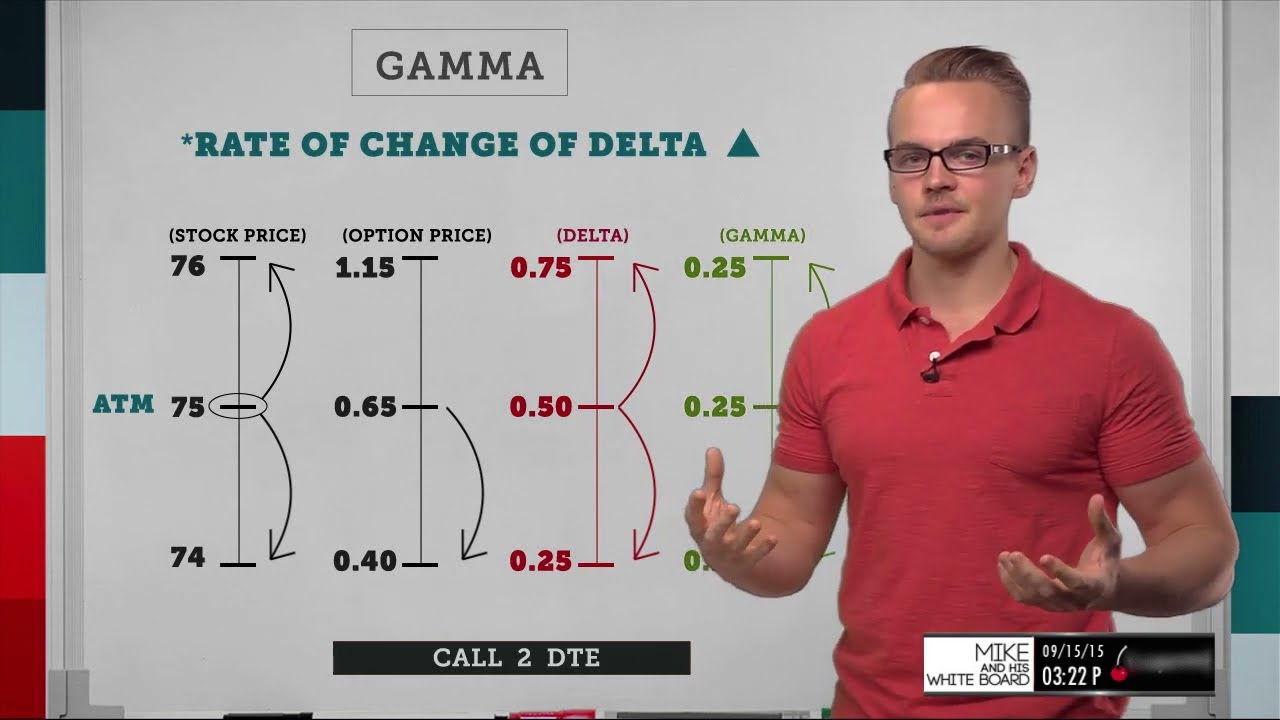

counterparty so from a linear perspective I'm gonna have the mirror mancierge if the stock price goes up a dollar my negative 61 position Delta says I lose 61 dollars I'm short the option ok now what about gamma well we have covered and we can just visually see that using Delta we characterize Delta or we can visualize Delta as moving along the blue line it's not going to address the gaps between the straight line and the reality of the curvature and we so we can call that curvature gamma sum we can also call it can city

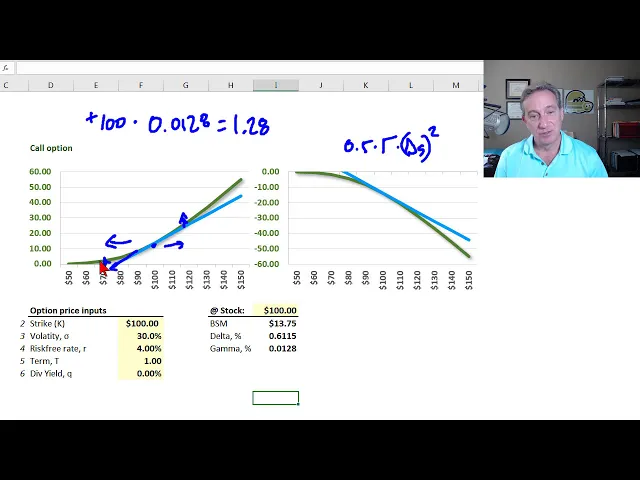

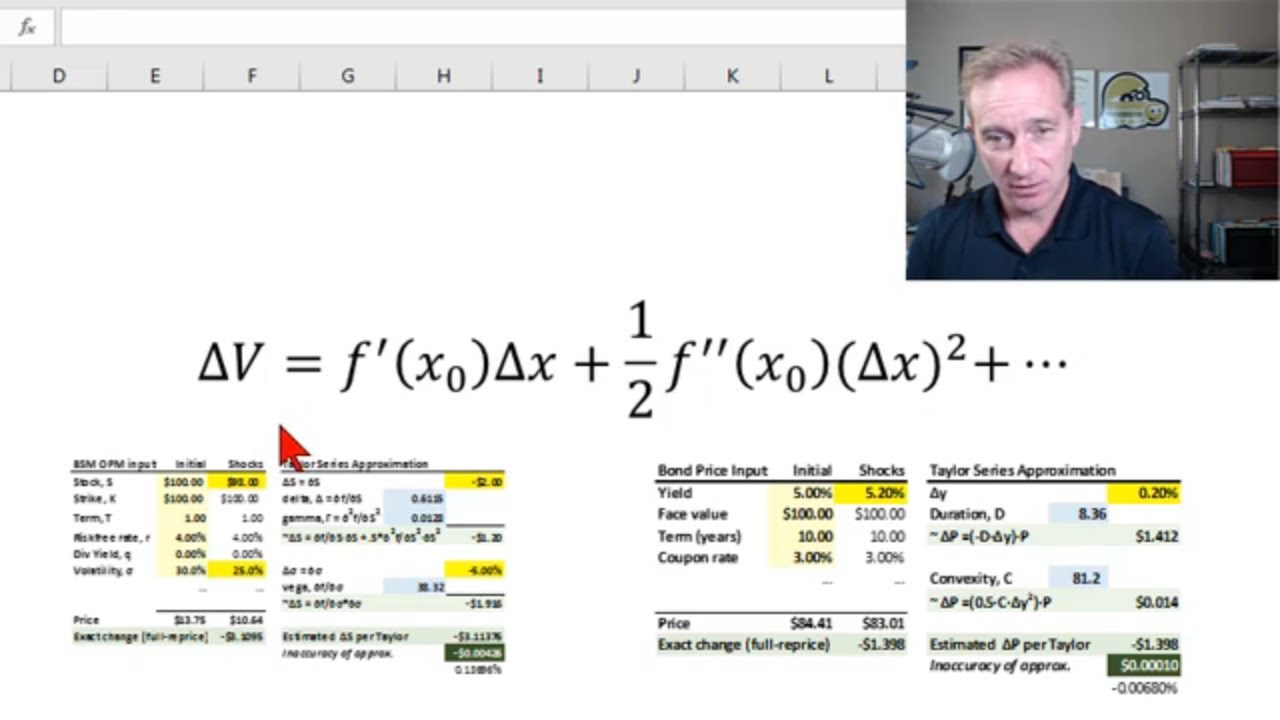

but we call it gamma in the option context and so let's take a look at your position gamma applying the same rule you've purchased 100 options now all be explicit about the quantity the percentage gamma is positive point zero one to eight your position gamma is one point two eight and so I'm not gonna worry about the numerical translation of that position gamma into the actual value Delta here but if you're familiar with the Taylor series it's not too hard really we just take that gamma and further Taylor series where I be multiplied by 1/2

times the gamma I'll use gamma for that multiplied by the change in the risk factor that in that case that's the stock price here and we square it so that this gamma adjustment is always positive okay but not my focus now currently my focus just is just on the directionality the impact can we came back we come back from your perspective and we can see you have positive gamma and visually this is confirmed and it's very interesting it means that you are in a win-win situation positive gamma which is necessary for long the option if

you're long an option you have positive gamma and we can see now why that's true positive quantity times a percentage gamma that is always positive means the position gamma is always positive now we can see why you're in a win-win position stock price increases per the Delta moving up the blue line you are gaining but that gap is also positive that positive position Delta quantifies the fact that when you gain the curvature makes you gain even more you gain an accelerating rate but also very interesting how about when you lose notice you this gap makes

you lose less you are win-win on both sides what about me I've written the option I'm short applying the same exact rule however I I am short 100 options quantity x same gamma point 0 1 2 8 and my position gamma is negative 1 point 2 8 I have negative position gamma and so I am lose-lose right we start at 100 stock price let's say stock price decreases my Delta exposure produces a gain for me after all right I'm short a call option I'm gonna gain directionally here due to the Delta as I move to

the left however the gap works against me so the curvature in the form of negative position gamma means I gain less and then notice over here stock price increase I've written a call option my deltas showing up for me here as a loss that's the biggest factor but the gap works against me when I lose I lose even more I'm lose lose and so for this reason here's the a key characteristic of gamma let's just say at the money here at 100 you Delta hedge or we both Delta hedge your Delta hedge here where you

are you are long you are long 100 options your Delta hedge would be too short be short 61 options I'm sorry 61 shares long hundred options with a position Delta of 61 means you would short 61 shares to be Delta neutral or neutralized or Delta right shares have a delta of 1 so that means your protective against Delta but you'll still have the positive gamma so you would gain on any big jumps in the stock price so positive gamma when your Delta neutralized is to be positively exposed to volatility over here same situation for me

I'm negative 100 options my Delta hedge is to be long 61 shares if I if I write you 100 options then I purchased 61 shares I am hedged with respect to Delta but I will still have my negative position gamma exposure and that means that if there are large jumps in the stock price I lose and so we say short short position gamma is exposure to volatility okay and so then more briefly I'll just take a look at the next sheet and that's for the put option and you'll notice for the put option here the

percentage Delta is negative as we expect we know that it needs to be between negative 1 and 0 and so let's say from your the your perspective you're the one who's purchased one option contract on these puts so your position Delta is quantity plus 100 multiplied by the negative 0.388 5 means your position Delta is negative 38 so 30 25 this round and negative 39 is your position Delta that means is stock price increases by one dollar you can expect to lose by $39 your what about your gamma your negative 100 put options multiplied by

your gamma notice the gamma is the same gamma is going to be the same for the call on the put if the strike and term are identical per put-call parity actually so your negative 100 options at per percentage or per option gamma of point 0 1 2 8 means your position gamma is negative no I'm sorry your positive I meant positive point one to eight just like before your position gamma is positive so that means you've purchased the put stock price decreases you gain on the Delta but the gap works in your favor you gain

even more due to the curvature or gamma when the stock price decreases your long the put so you lose according to Delta when the stock price increases however the curvature the gamma protects you you lose less due to this positive gamma exposure positive position gamma and then finally for me on the right I am I have written one hundred put options with a / / gamma or percentage gamma of 0.001 to 8 and so my position gamma is actually the same as it was before same for the call on the put because they both share

the same percentage gamma so in this case now I've written the put and so I'm going to lose if the stock price decreases but my negative position gamma exposure means I lose even more and then sad for me stock price increases that's what I wanted in terms of Delta I'm in terms of the Delta exposure I'm gaining but I'm gonna be it's gonna be mitigated I'm gonna gain even less due to the curvature and so my negative position gamma exposure is basically a short position on volatility the abrupt jumps themselves are working against me just

like they're working in your favor so I hope we'll hope that's helpful in tying together Delta Gamma and visually providing the intuition for that thank you