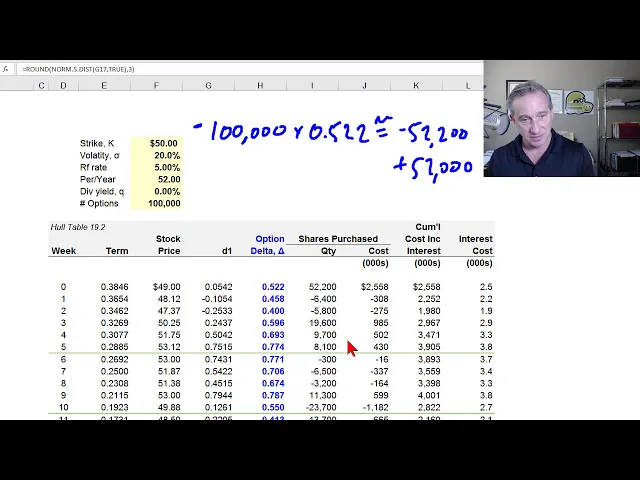

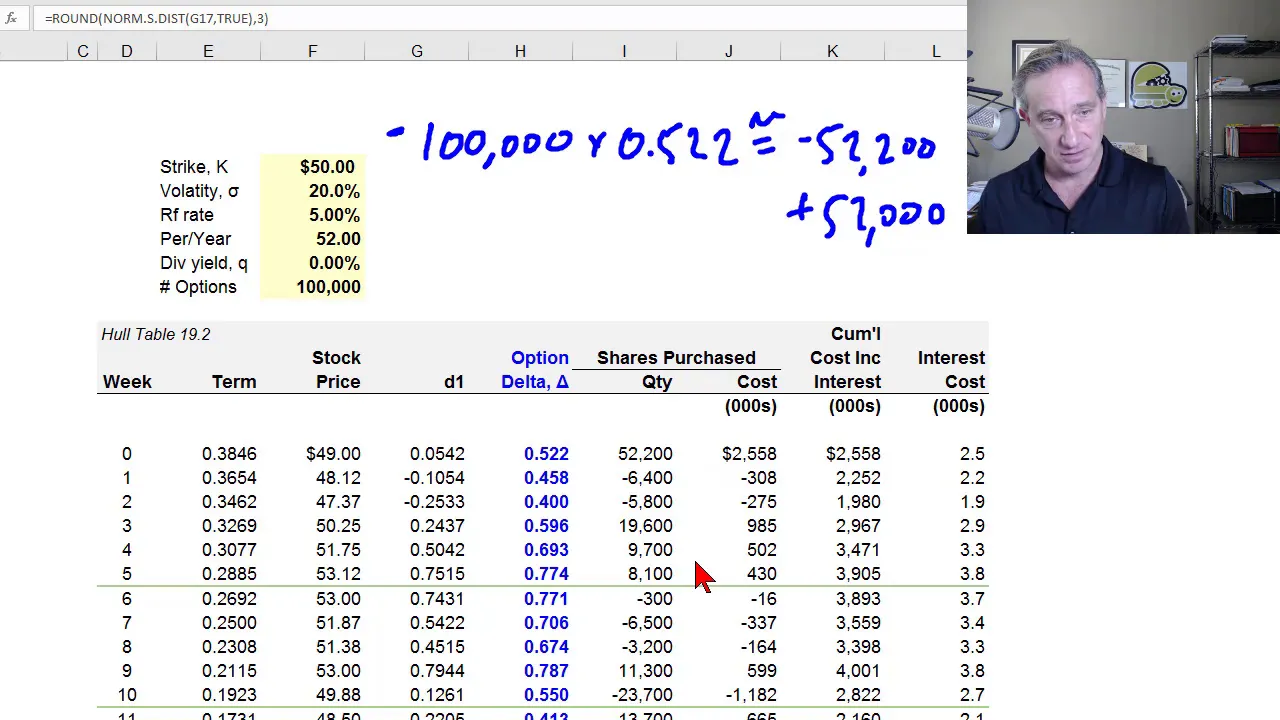

so I'm gonna walk through exactly what happens here with a dynamic Delta hedge using John Hall's example and the situation is that you can imagine you're the market maker and you are writing or selling 100,000 call options let's say to me and that means you are exposed to price risk specifically if the stock price increases you're going to incur a loss on these call options that you've written to me so you hedge that risk out by purchasing shares the only difference is that you're going to rebalance every week that's the Dyne meaning of dynamic as the option Delta changes you're going to rebalance your portfolio to maintain Delta neutrality or neutralised exposure with respect to Delta so I have here a replication of John hulls table 19. 2 in this sheet the next sheet in the workbook is his table 19. 3 so that's with my calculations and my values do match what he displays and so you can see exactly how this dynamic Delta hedge operates and the situation we have here is you can imagine your the market maker and you have written that is to say you have sold 100,000 call options let's say to me is the counterparty you've written or sold call options it's a hundred thousand an option contract is for a hundred options so we can also think of this as writing 1,000 call option contracts but you have price exposure so you want to dynamically Delta hedge in order to do that it's critical that we understand the definition of option Delta I've already covered this in my previous video in this playlist you want to go back to that first make sure you understand Delta but let's quickly just recap the intuition of this and let's just say that you've written only hundred options let's say hundred options call options that you've written where that per option Delta is right here point five to two so I'm just going to say Greek Delta of the call is 0.

5 to two you written 100 call options what does this mean that means you're exposed to a price increase in the stock are you not right I hold the option it's a call option if the stock goes up by a dollar it's gaining in value for me and losing in value for you as the option seller or writer and the point five to two is telling us that if the change in the stock price equals plus one dollar then with a delta of 0. 5 to 2 we're expecting a change in the call value to be minus in this case for you as the writer of 52 cents per option that's how we interpret it point five to two fifty two point two cents per one dollar your the option writer if the stock price goes up by a dollar that is in terms of the option position again for me of about 52 cents and a loss for U of 52 cents right on a mark-to-market basis so if it's a hundred options then you are losing fifty two dollars and 20 cents just like I am gaining fifty two dollars and 20 cents so that's the purpose of the the Greek that is option Delta first partial derivative that's the sensitivity to call value with respect to a change in the stock price not the only risk factor for the option but along with volatility and maturity one of the top three exposures that you have okay so but in John Hall's example here we have written or you let's say you're the market maker have written 100,000 call options with a strike price of $50 we're assuming 20% volatility why would we use that well that would be the price them so I'm gonna pay you it turns out John hull explains that the orc tells us that the black-scholes price would be value of all that would be $240,000 so you would collect the option premium on writing me those options and then you incur the risk that the stock price will go up we have risk-free rate of 5% and we're gonna do a dynamic Delta hedge on a weekly basis that's a choice that we make we're gonna rebalance weekly so I have 52 periods per year and it's going to be on a non dividend paying stock so here's the table that shows the dynamic Delta hedge starting at week zero and what I don't show here going down is we go for 20 weeks because these are call options with a 20-week maturity and so this initial term here is 0. 38 for 6 and that's in years so that's because when when you first write me these 100,000 options the remaining term to maturity or the remaining term is going to be 20 weeks divided by 52 weeks in the year that's point three eight four six years right all the inputs into the black-scholes are really in per annum terms and then they get adjusted in the formula and so this just happens to be here the stock this is the stock price column this simulates stock price right obviously at the time that you write me the options you don't know what's going to happen so this is just one we could think of this is one trial and a simulation that Hall happens to show and 19.

3 is is the different trial the only difference here is in the first trial here these option the options ends up in the money so I'm going to exercise them and the next one they end up out of the money so they're gonna expire worthless for me as the does the holder or long position in these options so I have your d1 this column is not in the actual table so I'm just I'm just showing it here I think I it could be easily collapsed so I'd mix playing the previous video right that's the key input into the option Delta calculation and and there also is an intuition that I discussed in the previous video if you want the intuition but our option Delta here is just a straightforward function of the d1 it's norm s disc right so this is it's really just n of D 1 on a call option that's the standard normal cumulative distribution function meaning that this is a probability function so these have the characteristics of a probability for the call option it's gonna it's gonna the option Delta needs to lie between 0 & 1 and technically just so we're we're comprehensive here for a call option Delta the it's really NFD one hair cutted by E raised to the negative dividend time maturity so that dividend yield does hair cut that in the exponent but for non dividend this value is 1 so oftentimes that's why you just see NFD 1 because we assume a non dividend paying Spock stock ok so you've written the 100,000 options they have a per option Delta of 0. 5 to 2 that's per option also technically called percentage Delta can be confusing because the options are strictly speaking a unitless and now the first step in the dynamic delta hedge because what's the situation well you have written 100,000 options and that's the quantity I'm gonna use a minus sign just to show that you have written them to me and they have a per option Delta of 0. 5 to 2 that equals 50 2200 and I'm going to use a negative because you've written them and that is your position Delta you have a position Delta of negative 50 2200 this quantity times per option Delta has a very straightforward interpretation it means that if the stock price goes up by $1 you expect to lose fifty two thousand two hundred dollars on these written options but I'm going to stress the approximately equals to just to be mindful of the fact that the option Delta is a first partial derivative so it is a linear approximation the larger that move in the stock price the less accurate will they approximation be okay but you want to hedge this exposure to price risk that you have what do you do you purchase shares shares by definition have a delta of 1.

0 right stock price goes up by dollar you gain in the position the share position by a dollar and a one-to-one correspondence the shares have an option have an avid Delta of one so how do you hedge this Delta exposure you simply purchase 52,000 shares that way stock price goes up by $1 that's your loss on the options that you've written but this is your offsetting gain on the stock and it goes the other direction as well stock price goes down by $1 this would be your gain on the option position and this would be our loss on the stock you are neutralized or perfectly hedged with respect to the assumptions for that exposure to the risk factor here of the stock price which is captured by Delta to purchase the 50 2002 in our chairs you incur a cost of 2. 5 million approximately that's just based on purchasing that many shares at this price 50 2. 2 times the price for a cost of 2.

5 million I'm going to be just round and our cumulative cost starts at that value the final column here is the interest cost and what we're gonna do is we're gonna just be charged interest for the purchases on our stock at the five percent but this is weekly so it's the car at the end of the first week it's the two point six five that we needed to fund the purchase multiplied by the five percent but that's per annum so we divide by 50 to get a weekly interest rate why are we doing that because it's correct in finance to always assume a funding cost if we don't have the cash we need to borrow it even if we have the cash there's an opportunity cost to using it for this purpose so it's correct in general to be explicit about the funding cost even if it's an opportunity okay so that's great we are Delta hedged and then we move to the next week and then I really only need to show you one week to show you what we're doing with the dynamic Delta hedge and so what's changing here well the only two things that are changing our time is marching on and that is significant for these options that's the time decay mattered and theta captured in theta but so as these options as the maturity shortens as time goes by the option Delta is changing and in fact as it get as we get to closer to expiration it's going to tend to 1 or 0 depending on whether in or out of the money so that's one change but the more significant one for us here is captured by the simulation this just happens to be at one trial among whatever I'm using John holes numbers but they just could easily be random the stock price is changing so as covered in the previous video right Delta is not constant with respect to the stock price for this call option here to increasing function the stock price so in this first step it happens to be that the stock price drops from forty nine to forty eight point one two the call option Delta is going to drop right so dynamically that's the most important thing that's going on here in the simulation the stock price is changing so the option Delta is changing so our option Delta here because it drops goes down to point four five eight in the second week stock price drops it happens to stop drop option Delta goes down and then in the third week for the first time in the simulation here the stock price goes up and you can see the Delta goes from point four to almost point six an increase in the Delta well we want a net position that's neutralized or hedged perfectly with respect to this Delta so in that first week here we purchased fifty two thousand two in our chairs but our but now we go into the or weeks in the first into the first week beginning the second week I'm not sure how to say that the option Delta the per option Delta here drops to 0. 45 8 we have written or you have written to me 100,000 options but now the option Delta is zero point four or five eight I mean these the negative because you've written them from your perspective and so the position Delta is has drops from fifty two thousand two hundred to negative or 45 thousand eight hundred or drops so to speak from negative fifty two thousand two hundred to negative forty five thousand forty five thousand eight hundred so your position Delta changes now so you don't need to actually own fifty two thousand two hundred shares anymore in a sense your overheads now you can sell some of them you can sell the difference if you sell six thousand four hundred shares from the fifty two thousand two hundred that you owned you will you will have remaining forty five thousand eight hundred shares and you'll be back to perfectly Delta heads toward Delta neutralized back to a situation and where any gain or loss and your option position is offset by a gain or loss in your share position and so that's really that's really all that's happening here with the dynamic Delta hedge now we go to the next week stock price and simulation drops again down to 0. 4 we don't need as many sheriff's we can share we can sell another or you can sell another five thousand eight in our chairs so that I know I can see your share position will be forty thousand so you can look at any one of these now I don't even need to do the math here to see that in this very there's a very dramatic drop here from a price of 53 to forty nine point eight eight and there is a large share sale which will bring us to a held share position of 55,000 shares I can just read that here knowing that this is solved were based on the perfect Delta hedge okay so that's the basic dynamic we get down to the bottom here of John holes as the options of Proust maturity and as mentioned this first sheet says a scenario where the stock price ends up above the strike price that strike price is $50 happens to be that in his scenario here we end up with a stock price of 50 7.

25 remember you've written me the options so they're in the money I'm going to exercise and that option Delta as it approaches an expiration here is tending towards 1. 0 and your cumulative cost for this dynamic Delta hedge is five point two six three million so that sounds fairly high except that I exercise the options are in the money so you're paying me that on that strike price here you're paying me seven point two five million however you own here cumin of Leon the quantity here it doesn't show here but kimly you own a hundred thousand options at the the $50. 00 that you do collect and that's five million so you have five million dollars worth of stock here your cumulative cost was five point two six three million such that your cumulative cost here is two hundred sixty three thousand dollars at the end of the twenty weeks and that matches John holes number okay so I'll go back up keep that in mind at the end of twenty weeks the cumulative cost for you to dynamically Delta hedge this was two hundred and sixty three thousand what we don't show here is when you first wrote me the options you did collect that premium John Holt tells us that you that premium was approximately two hundred forty thousand dollars it's based on pricing those options with a black Scholes model of volatility assumption of twenty percent you collect two hundred twenty four thousand dollar $240,000 then go the 20 weeks dynamically Delta hedging your price risk away so from that perspective really hedging out all your risk at a cost of future value 263,000 so his point there is if you take that the present value they equalize if you think about it that makes some logical sense you it should it if you want to take that premium and then incur that cost to hedge at all the risk of me risk free position there shouldn't be any profit for you the kicker on that there are the assumption there is that this simulation reflects a realized volatility of 20% I haven't checked that I bet it's John Hall I'm sure it's right so this does equal out if the realized volatility equals the implied volatility at the time you priced the options right obviously if this pricing reflects them you must reflect implied volatility it will probably under our overstate the actual real realized volatility and then there will be a profit or loss that's the key assumption there and then so I won't go through the second sheet in this 19.