Okay before we head into this week's market outlook an update for the applied level um one part the applied asset management under screeners you'll find the momentum screener up and this was coded in Python the code is also available for you there's two versions one in momentum uh just straight momentum one uh using relative strength with momentum and there will be more screeners uh all utilizing uh Python in Applied analysis uh I'm doing this one uh the use of AI for financial analysis uh and it matters what model you're using the type of prompt that

you give uh I'll show you uh how you can get it done in uh GPT4 in Gemini in Claude and in deepseek uh and I'll show you some interesting uh output where uh the same prompt using the four different models will get you different things uh so it is it is I think worth having more than one model uh to use and Just by changing prompts a little bit uh you can get uh different output so there is some work to do in learning how to ask a model and depending on what model you're asking

learning how to ask it the right question so we'll do financial analysis for a subindustry we'll do a whole industry i started with coal uh because uh Trump has uh reintroduced uh clean beautiful coal or is it beautiful clean coal it's beautiful clean coal that is the Executive order you must uh use the words beautiful and clean before you use the word coal so I started using it and in about 20 minutes of just tweaking the prompt I estimate I was able to save maybe about six hours of work six seven hours of work that

I would normally do to get the content that it delivered to me now it's not perfect uh you do have to go through it and then at every uh Every so often you have to prompt it in specific areas again and then you do have to check some things but it does save a considerable amount of time so we'll actually do a whole video on generating the uh subindustry uh video understanding coal mining by using AI so rather than me uh showing you uh a video on the coal industry I will show you a video

on AI outputting what we need to know about the coal industry that's kind of cool right uh a Competitive analysis uh we can use it uh to generate a very fast competitive analysis of uh the top five companies by let's say revenue by let's say revenue to China by let's say the amount of metric tons mined by market cap however we want we can do a competitive analysis and then we will do a company analysis by feeding it uh a 10K and asking it to summarize it and then feeding it certain parts of the 10K

and asking it very particular particular questions so we'll Do a whole analysis from the subindustry down to the competition down to a company analysis uh and a lot of the work is in the prompt and the prompt is a function of the type of model that you're using how the model is designed so we're going to have to read some technical notes there uh and the perspective from which you're uh asking the question from uh so uh usually takes me 3 weeks to do a really deep dive on a subindustry three to four weeks to

Really get to where I want to be uh I'll uh I'm going to take the three to four weeks and get right into this stuff and then I'm going to show you how you can probably get all of this uh in about uh a couple of hours just by modifying your prompt so taking like 3 weeks and what would normally take me 3 weeks bringing it down to a couple of hours that is called power and you better know that going forward that will uh be in the applied analysis And that will be a series

of videos i don't think I'm going to get that done in one video that will be a series of videos because there's a whole bunch of front-end work that I'm going to have to do uh to explain the type of model and perspective so that we can work with some simple prompts first so I can show you what I mean by that and then we'll go into uh something deeper okay let's uh let's head in we have a lot to get through this week i've uh put a lot in Here the big story from last

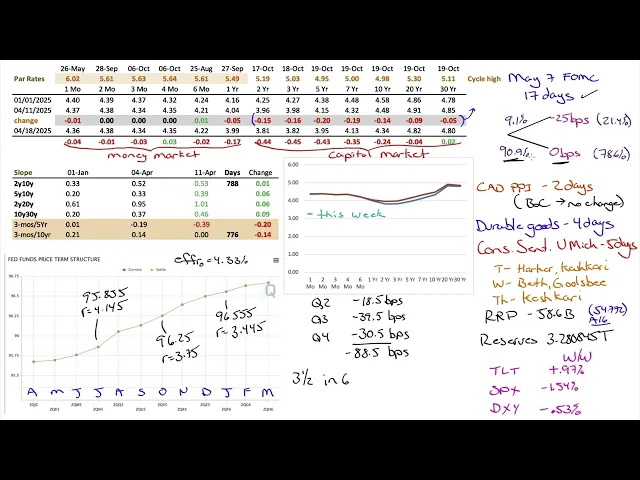

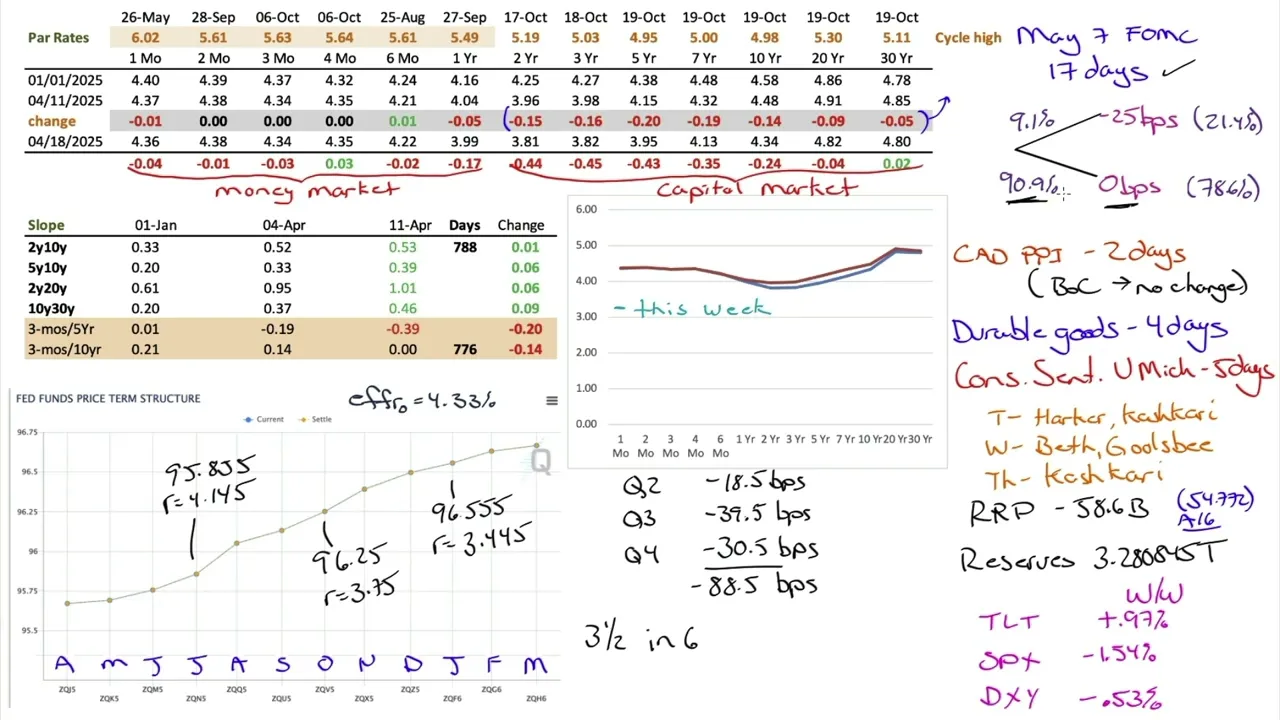

week was Powell versus Trump i'm going to call it round two and if you're scoring this one uh you got to give uh this one to Powell maybe a 10 N round look at the uh yields here from the 2-year to the 30-year all recovered somewhat from the week before had a big move up in yields they've come down a bit but uh have not recovered uh as much as they lost i think this is short-lived i'll lay out my argument in the screens Coming up but I think that yields uh on the long end

of the curve go much higher we have the FOMC uh in 17 days 90 almost 91% on no rate cut and this is primarily based on what Powell said on Friday at the Economic Club of Chicago i will I have a whole screen uh on uh on some of the points that he made in between now and then you have a couple of uh items coming out pce I don't think that's going to give uh much help uh not much more help than what We've seen from CPI already we get the ECI the employment cost

index for Q1 i don't see a lot of help there when I say help I mean help in uh getting Powell to cut rates i don't see much help there q1 GDP uh and um April jobs report we will get that uh you get Q1 GDP at the end of the month and you get uh on two Fridays not this Friday coming up but the next Friday you have a jobs report April 2nd what would help Powell cut is a Negative print on Q1 GDP and a dismal jobs report no jobs created or very few

jobs or even jobs lost that would be permission to cut i personally think he has permission to cut right now if it were me I would be leaning more towards a cut so I I don't agree with the 90.9 but I think the market probably has it right i just don't agree with that i think he does have permission to cut now um let's say Q1 GDP is negative uh everyone's going to be looking at the M Component the imports component and I'll show you in a little while why that might be important if you

remove the imports component the front running ahead of all the uh all the tariffs if you remove that or adjust for that you still have a positive uh Q1 GDP uh without that effect i think I think that will be uh the dominant number to look at as opposed to the uh overall negative number if if we do get a negative print which means the jobs report would have To do all well I'm not going to call it heavy lifting at this point all the really light lifting in other words show nothing to get the

to get the Fed to move i don't think this Fed wants to help this president let's just say that i don't think this Fed wants to help this president and if they do uh cut rates in May it's got to be really clear that they have permission from the data to cut otherwise they're going to look like They're bowing uh to King Trump and they're not going to want to do that we have a flat curve from the 3month uh to the 10-year the money market to capital market curve is now flat again it uh

dropped 14 basis points for uh the week ahead what do we got canadian PPI in two days uh last week Bank of Canada made uh no change so I don't see this as being important but there it is it might affect the currency but uh I don't think by much durable goods for the US in four Days that'll be uh interesting to look at i think once we start getting some of the April data in that has the effect of the tariffs both the real effect for however long some have been in place and the

psychological effect the change in behavior because of it it'll start to be reflected in April data going forward 4 days consumer sentiment University of Michigan 5 days uh was dismal last week does he continue that you have some Fed speak going on this week but I think the Main speaker Powell has spoken i don't know how important this is to look at anymore reverse uh repo uh hit its lowest for this cycle 54 billion August 16th ended the week at 58 billion heading towards zero reserves are down as well but let's keep in mind that

you had uh tax uh tax payments that were due so a lot of money sitting in bank accounts were sitting there ready to pay their taxes uh which means they transferred from their own Personal or business accounts to the Treasury general account so you would see reserves drop uh for tax payments uh same with the reverse repo money coming out of money market funds to make your tax payments uh so the TGA uh increasing uh whereas the reserves in the system would decrease until the TGA starts spending that money and throwing that money back out

into the banking system which then shows up in reserves again let's see if that reverses Out uh TLT had a good week as we pointed out up here uh up.97 spx not so much down 1.54 and I'm going to start adding the DXY in here if your domestic market is the US that's not important to you if you're an international investor investing in the US this is going to become more and more of an issue for you because I do believe we are in a downward movement on the US dollar uh and I think that

continues on week overw week down 0.53 so even though TLT had a positive week 0.97 the long end of the curve US treasuries uh recovering somewhat depending on the currency you're holding whether if it was the Canadian the yen or the euro you actually showed a loss in your own domestic currency and this is how you have to start thinking about it unless you say look I'm going to be in the US for the next 10 years I don't really care about the currency uh there are uh more and more reasons Why you may want

to hedge out the currency for most individual investors the easiest way to hedge out the currency is just to get out of the asset and I think at the margin that is what is going on and as that is going on that puts more downward pressure on the US dollar and more upward pressure on other currencies as uh investors repatriate their dollars so negative.53% if you're uh in Japan uh that one I can clearly I I think I have Clear appreciated by more than what uh TLT did so you actually ended up with a loss

now if you're in US equities you lost 1.4 4 broadly speaking you know you could have been in just the few that went up maybe you you had better allocation but broadly speaking if you're diversified across US equities down 1.5% add to that the loss uh of the US dollar as well you're down even more so from an allocation Perspective from an international allocation perspective the US is looking less attractive and you have to overcome the weight of the US dollar which I think probably has more downside uh to it uh I um spoke with

one person last week who um uh is close to uh decisions allocation decisions for a large pension fund in Canada i can't say much more than that without revealing probably who I'm talking to um they are beginning the process of Underweing US assets and overweing Canadian assets still with a large allocation to the US but an underweing which means at the margin they have to be sellers and at the margin they're buyers of Canadian assets so at the margin they're sellers of US dollars at the margin they're buyers of Canadian dollars uh so that that

uh is going to add and you know at the margin again some more pressure to the US dollar uh effective Federal funds rate of 433 here is our Fed funds futures curve our implied rates uh I've written down here based on where the index value is um pretty much the same week overw week in terms of the rate cuts implied by the Fed funds rate but being pushed further into Q3 and Q4 coming out of Q2 less than uh one one cut uh half a cut let's say because it's being priced out of May three

and a half cuts in six sessions um if you get a recession I Guess it depends on the flavor of the recession and the type of recession and uh how the FOMC feels uh and the rhetoric from Trump uh the worse it gets from Trump the more likely I think he is to force the Fed into a position where they will only act if it's very clear that they should act to avoid uh looking like they're bowing down uh or or acquiescing uh to what one person wants uh all in an effort to maintain Uh

uh the um psychological belief for investors that the Fed is in fact independent so Trump is not helping his cause here he's not helping the cause at all by doing what he's doing because if they do feel that they have some permission to move it will now appear that they're less independent than they used to be which is a bigger problem so it's actually making the problem worse that the best thing Trump can do at this point I think is stop Harassing the Fed but that's not his style following along with capital market yields being

lower real yields also uh are lower as well uh break evens uh kind of flat looking at OAS uh they also contracted as well in line with uh the recovery in nominal yields uh in 2020 uh to about 2022 you had very very low rates and during that period of time uh as far as corporate issuance goes it was Really high um because rates were so low most of the high yield debt and I'll just circle where we have high yield on here most high yield debt tends to be nine years or less the longest

nine years in between three to five years with five five to seven kind of being the preferred tenor let's say five 2022 to 20 2020 to 2022 puts those maturities 2025 to 2027 and a lot of debt was issued during that period of time uh re Uh refinancing that now is refinancing it at much higher rates so that's uh sort of what might be keeping small cap stocks under pressure is just the amount of refinancing that's going to have to be done at these higher rates looking at uh unemployment insurance um for uh continuing claims

uh that is creeping up people staying on unemployment longer uh even though initial claims really aren't aren't Moving that much down 9,000 uh week over week if it's not seasonally adjusted uh you are up about 3,000 but looking at initial claims filed in federal programs uh 542 uh for uh the week ending 508 the week before these are these are not numbers that are suggesting that Doge is making significant inroads at all now if we think well they all got severance we're Really not going to see it for quite some time we may never see

it if if during that period of time that they have severance they're able to line up other jobs they might may bypass the unemployment lineup altogether we may never see it but we're certainly certainly not seeing it at this point in time mortgages 6.83 up 21 uh basis points Thursday over Thursday uh the spread between the US 10-year uh and the 30-year fixed rate 249 basis points last week we had Dr horton announce earnings and it was a miss swing and a miss and much lower guidance uh revenue uh for 2025 they are guiding to

33.3 to 34.8 billion that's down from 36 billion to 37.5 uh so midway through here is uh call it 36.75 midway uh through here is about 34 so almost 10% down on revenues for their guidance their sales 85 to 87,000 homes Uh making up this revenue down from 90 to 92,000 and I'm going to show you some data from realtor.com in a second uh we're getting inventory builds in the US particularly in some of the southern states California Texas Arizona Florida Nevada where DH DR Horton uh has a large presence days on the market are

increasing uh price cuts are increasing and it's March usually going into the spring the spring season you don't get That many price cuts you start getting them um once you get into the summer July August September if they haven't sold in the busy season the spring season now's the time to cut but you're getting uh huge amounts of uh price cuts going in to the spring season okay this is uh weekly housing trends week of April 12th is the last column here this is the week of April 5th this is the week of March 29th

all the numbers in here are Year-over-year so we can see median listing prices year-to- date negative.8% new listings year-to date up 8.1% and if we look at what happened in the last 3 weeks as of the 29th year-over-year was up 31.2 for April 5th year-over-year was 8.6 week of April 12th up 12.8 these are all higher uh than the year-to- date implying that the year-to- date is being pulled upwards uh by the more recent weeks you can really see it with active listings up 27.6% year-over-year uh with uh a lot of the more recent weeks

pulling it higher week ending March 29th active listings up 32% uh 30% for April 5th and 31.2 for April 12th time on the market 5 days slower meaning it's taking 5 days longer on average than it did the year before and you can see that that has slowly been increasing 2 days slower 4 days and then week ending April 12th 4 days longer let us look at uh March uh for the full Month because we do have that that data this is active listing count here we are here uh you can see it moving uh

upwards here uh for March usually uh uh it would increase a little bit into the beginning of the year it tends to fall into the spring season and then increase after that you can see that trend down here uh these years down here the yellow line 2022 the green line is 2021 the pink line 2023 there's 2024 uh and this line here is 2020 there We are these are all pre- pandemic up here 2017 2018 is the orange and 2019 is the red and we are moving up and we'll see how that plays out over

time here it is again march 25th uh or sorry March 20 2025 total listing count uh we can see it's above the post pandemic years but not above the prepandemic years yet this is newly listed homes uh you can't see it right here but it's hidden right in the yellow line here which is 2022 newly listed homes you can see that really Starting to increase it's starting to increase but sort of in line with preandemic uh rates of increase but certainly not post pandemic um where housing inventory is growing the fastest in the West 40%

the South 31 Midwest 17.7 the Northeast 11.3 uh at the metro level all 50 of the largest markets saw inventory rise year-over-year some of the biggest gains San Jose California Las Vegas Nevada Denver Colorado all in the 60% Uh most metros still have fewer homes available than they did pre- pandemic that said 18 markets have now surpassed their 2017 2019 uh inventory levels up from just 15 last month 18 now uh meaning the rest uh of the 50 largest you still have 32 that are lower than pre- pandemic but now we're up to 18 denver

San Antonio and Dallas uh home sellers return boosting new listings in most metro areas inventory Of newly listed homes increased across all four regions led by West uh 14% South 10 Midwest and Northeast uh biggest year-over-year gains in new listings Denver San Jose Richmond we've seen those up above home listings linger slightly longer than last year there is March over here everything below is uh post pandemic the green is 2021 the yellow is 2022 the pink uh is 2023 the brown is 2024 notice that it is above all of Those but still below uh prepandemic

levels uh and then it gives you uh time uh time on market rose in all four regions compared to last year in every region homes are selling faster than they did pre- pandemic compared to the 201719 average we can see uh that they are still moving faster northeast 19 days faster but we've seen uh from above when we looked at the northeast uh it tended to have the lowest level of newer listings uh and up here uh inventory is Growing is growing but growing the slowest 11.3 versus all the others so it would stand to

reason that uh if we are seeing um time on market it would be from the northeast uh sellers are cutting uh more often uh so where are we here there's the right up here the median price uh for March is sitting up here this is in line with 2023 and 2024 uh so median prices have uh have increased quite a bit this is price Price reductions look where it look where it is the percentage uh on price reductions 17.5 above all the other years so it is it's above post pandemic and above preandemic and again

for this time of year look at the trends it's uh usually downwards this has been straight straight up it's usually uh uh odd to see uh that type of price cutting going into the busy season which is the spring buying season that is the busy season up 17.5 above all the Years uh and this is where um the p uh regional metro area price trends year-over-year median list price changes by region midwest and south are both down west is flat only the northeast is up uh so I'll leave that uh the links to uh these

these two in the uh description box below so you can go through it so to sum up from that last uh from the last screen I don't know that I would be too eager to get into US home builders uh at This point probably not for a couple of quarters let's see how this uh how it plays out where the 10year goes from here i got a sneaking suspicion the 10ear goes higher i also have a sneaking suspicion inventory uh probably continues to climb uh which isn't going to help home builders too much let's move

over to S&P s&p uh drifted down last week for the last couple of weeks I've said that I would short every rally i believe the words I used was with Impunity i have been doing that that has been working out well i'm still net long US assets if we split it between equities and treasuries I got a big position uh in duration which you know I've talked about that for quite some time i am looking at pairing that down and I do have a position in US equities which I have been reducing over time as

the market gives me opportunities i sell on green days i no longer buy on red days i used to do that you sell on green Days you buy on red days i see red days i'm not adding to my US positions i'm adding to my Canadian position so I am decreasing my exposure uh to the US um if we look at the four quarter operating earnings the forward uh four quarter 27524 down from 27732 that is a a fairly big drop week overweek i don't recall if I've seen it drop that much usually when it

drops it drops like 45 cents 70 cents something like that uh that is over a $2 drop um in in a week uh also we do have Uh uh a move from international allocators from being overweight US to moving towards being more equal weight or underweight the combination of dropping earnings and a move away from an overweight position is going to drop the multiple so I have two scenarios here uh earnings uh end at 260 with an 18 or uh down to 250 at a 17 the longer this fight goes on with China the more

likely you are to end at about 250 uh in terms of the forward the four Quarter forward operating earnings right uh and um a multiple of 18 versus 17 so 260 at 18 I get the 4680 250 at 17 4250 so within that range I would probably say okay that you probably uh find a good entry point for US equities within that range we're sitting at uh 5280 on the index uh getting down to 4680 uh is another 600 points down a little over 10% down getting down to 4250 uh you got another 400 points

from There so that's about another,000 points off the index where it is almost 20% down from where it is uh and really this is dependent on how long the administration stays on this particular course how long China uh decides that it does not need the US as much as the US says it does uh who's going to make the first move how they're going to engineer uh a victory for both sides because you have to the longer that goes on the more likely you're going to get 250 the more Likely you're going to get a

move not only from uh overweight US equities to uh equal weight but maybe even underweight you could get down to the 17 so I seem to think that somewhere in that range call it 4500 uh seems to be where I would probably say okay well now I don't mind uh being uh having more uh um more assets in the US or more exposure to US assets and that is as long as uh this whole talk about taxing uh uh taxing capital Foreign capital goes away you have uh I guess some conversation about withholding tax uh

for non US residents as high as 50% uh I sent that uh that link in to my uh money manager at JP Morgan saying if this happens I see no reason to be in US assets any longer if you're going to do a 50% withholding that's 50% withholding on your interest payments 50% withholding on the dividend payments and there is Some talk about cancelling the tax treaty between Canada and the US so all the US uh stocks that are held in retirement accounts right now there is no withholding because of that tax treaty if that

goes away suddenly you're facing anywhere from 35 to 50% withholding tax there's going to be a lot of selling of US assets to avoid that you got to stop that conversation from happening now I don't think that's going to happen i think that's a that's Just a wild shot what the last thing you want to do is start chasing away the very capital that gives your market the valuation it does if if if they are going to pursue that uh get rid of that 17 bring it down to 15 maybe even 14 uh on the

multiple because if you don't have international uh uh allocation support for your market it doesn't justify a multiple at that level only justifies that multiple if you think well the market's going to Outperform and if it's going to outperform I want to be in it so obviously outperformance means a higher multiple for every dollar of earnings that's what that means so that that conversation has to go away but uh that caught my eye the moment I saw it is is if you're going to start taxing uh taxing uh the income at that level uh there

is not enough capacity in zero coupon bonds to move from uh zero coupon Bonds uh and the majority of uh investment money is held by boomers who are in or near retirement who are not holding on to zero dividend paying growth stocks they're in income paying value stocks they would flee from that very quickly that has to go away um sitting at 19 times forward earnings 19.18 down from 19 uh.34 the drop in the S&P help lower the multiple along with uh the drop in uh earnings as well implied volatility still elevated but uh Coming

down a bit uh same with TLT elevated but just coming down a bit week over week if we look where our uh last reading was S&P 25.6% at one point we were under 10% within the last year under 10% 25.6 down from 315 and TLT17 down from 24% uh other indexes uh not doing as well as SPX s&p is down 14% off its all-time high which was February uh 19th 2 months ago we're April 20th now 2 Months ago uh down 14% having actually touched a bare market on a closing basis was we were in

a bare market for 12 hours from the close of the market to the open of the market what was that 4 to 4 to 9:30 19 and 1/2 hours we were in a bare market uh and then up uh up we go the very next day uh uh let's uh let's take a 90-day pause on all of this cuz the bond market is getting as Trump said that very technical term yippy the bond market's getting a little yippy uh so Off we go but then uh we're sort of fading away from there iwm JJR small

caps uh the Russell uh versus the S&P uh down 20 23% on the Russell down 24% on uh S&P small caps and Triple Q down almost 18% uh with SPY only being down 14% and I think you probably have more downside on all of these uh if you uh are rerating this multiple they're all uh all going to head down uh so I am Rethinking my positions uh as I said in US equities I uh short the market on any rally uh I mean could you get a big rally uh in the market if if

Trump says "Uh hey listen uh I talked with China things look good here's what we're going to do." You probably get a big rally but let's remember you still have those 10% tariffs across the board and you have reciprocal tariffs coming back in 90 days and you have a boycotting of American products uh and a Potential $90 billion hit to tourism for 2025 based on uh some estimates that I've seen is that the hit to tourism for the US will be around $90 billion i'm going to show you some numbers in a little while showing

you just the the fall off week over week in terms of imports uh to the US and exports from the US uh just the big falloff but with a grain of salt it was a runup ahead of the tariffs so the week after was okay first week of April versus last week of March we would see a big a big change uh but with all of this going on I seem to think uh that uh that uh where we are in terms of earnings where we are in terms of the multiple and therefore the index

level we're still we still haven't reflected um uh I think where we're headed 450 to 480 on spy I think represents uh uh probably uh a market that is more fairly valued and at a multiple that would represent an either equal or Underweing of US assets uh for earnings coming up uh I don't expect them to agree that's that's just too much of a big number if there were like two companies yeah I would expect that they would agree I mean you can't mess mess up that badly but that's uh this is this is where

we are right if you can't get the small stuff right uh how do you how do you expect me to have faith that you're getting the big stuff right i'm going to show you uh that with CNN shortly i'll show you a couple of p I got one really neat picture from Barcelona because that's where I am now was walking down the streets and I said "What is going on over there?" And uh somebody explained it to me i thought "No way." I had to take a picture of it i'll show you what that looks

like and then uh later that evening I'm watching uh CNN on YouTube one clip and I noticed they had written something down i thought "Oh come on you're CNN for God's Sake journalism you can't even get this right." Again you can't get the small stuff right how can I trust the big stuff let's uh go through here and see uh who's reporting this week all right here's our distribution not much on Monday only one we start on uh Tuesday uh so uh Verizon whenever we see Verizon AT&T and T-Mobile are usually not that far behind

uh we have some financials in here uh industrials will become Interesting uh because they're probably tied more globally uh than most so some of the uh guidance here will be uh interesting to see tesla and PTE which is a home builder tesla I am short Tesla only 400 shares but Tesla you can't be short that many shares because it is still still a cult stock but I'm going to stay short through earnings uh they have not done well i could walk away now with a profit a fairly good one but I'm going to stay short

through earnings i Don't see how they make earnings if they do make earnings I am going to cry foul i'll take a lesson from the president and say "Oh they're lying i cry foul i'm being cheated it's being stolen from me." Uh pneumont uh gold prices have been on an absolute tear uh if we anticipate a lower US dollar going forward which I do uh and a desire to be away from uh US assets uh US treasuries we're going to need another alternative Uh as a safe asset where's that going to be at the margin

gold will get some of that so their guidance will be interesting there is AT&T uh T-Mobile is probably just a day or two behind that uh some financials that week and then more industrials uh throughout here boeing will be interesting because uh China has uh singled out Boeing as a company to avoid cancel whatever orders you have return some planes sorry but we don't want your Business anymore uh so let's see what Boeing uh has to say as far as their uh guidance is concerned there's IBM uh in there we don't have too much tech

this week well I shouldn't say too much tech too much of the big names that that that we'd normally pay attention to there's IBM in there next Era in energy first Energy and Next Era next Era uh telling a different story than Duke and they both share Florida duke Energy uh having hit 52- week highs a few times in the First quarter next era nope nowhere even near there uh going in the opposite direction can they pull it out uh can they give us some reason to keep holding on to their stock because it just

has not been performing very well uh let's go to Thursday freeport uh copper prices have been strong gold prices have been strong when we think of their Indonesian operations you think of gold with gold prices this strong that Copper is basically free they're profitable uh just with the gold even before they start selling the copper however you do have talk about uh uh uh u imports uh tariffing copper imports uh into uh into the US and with the US and China in this stupid war that is going to that is going to uh uh weigh

on copper demand uh let's see what happens uh in their uh in their guidance hasn't shown up in pricing uh in pricing yet uh let's see anything else jump out At us southwest Airlines uh Texas Instrument Service Now uh they've been a high rider uh in uh Consumer Staples Pepsi Proctor and Gamble uh let's see anything else I want to Oh Amazon uh Amazon on Thursday after the close and uh we got 16 on Friday before the open t-mobile there's T-Mobile i was wondering where that was uh going to end up uh Intel uh there

we go uh I mean there's a Bunch more here of course but you know not not sort of the headline ones that we look at all right let's get right to the cage match powell versus Trump april 16th Powell uh was uh speaking at the Economic Club of Chicago uh and then was interviewed uh some of the questions uh focused on the effect of trade tell us about the Fed put uh have you seen long rates lately what have you been doing with reserves dollar supply Uh US federal debt so on effective trade this probably

upset Trump quite a bit uh we'll be seeing higher inflation uh and lower employment as a result of this so we will be moving away from our goals uh for the balance of the year that is not what uh that is not the message Trump wanted out there that everything he's doing is going to be lower inflation and more jobs and here's Powell saying no no no it's going to be the other way around uh the tariff Announcements uh that were made April 2nd uh were larger than anticipated uh so the economic impact will likely

be larger as well now these were delayed for 90 days the question is uh are they even going to see the light of day again or can we say well look those those simply just won't happen will he uh declare victory uh in 90 days which uh will be early July sometime come out and say "Well you know all these countries came and they bowed down uh and and uh You know gave me everything I wanted so we're going to let them off the hook we're not going to worry about reciprocal tariffs." I don't know

um big question mark there on what he wants to do or what he's I don't even think he knows what he's going to do until the day that that that he does it fed put uh he laughed and said no there's no Fed put let me explain why markets are functioning as one would Expect the markets are selling off uh you know to paraphrase him he says well duh what do you think is going to happen this is not a reason for us to step in this is not an unorderly market it is doing what

it's doing we're not here to protect the value of assets from normal changes in fundamentals so we're not going to do anything that's not helpful for markets rising long rates again he pointed markets are orderly yeah they're doing what they're doing markets are Orderly they're acting as expected given the uncertainty and he said there may have been some private sector deleveraging uh that caused the initial uh the initial rise in in yields for reserves uh he said they are abundant uh and the debt ceiling was the main cause of the slowdown in runoff uh because

if you hit the debt ceiling then you lose what he says you lose visibility on some of the information that we need to Determine where the level of reserves would be so it just was prudent to slow the pace of runoff uh ahead of this thing but it had nothing to do with anything else he was trying to be very clear on that that we are not being political in one little bit whatsoever we're not going to bow to anyone's ideology we're going to follow our own path dollar supply uh US swap lines will stay

open they have swap lines with five of the Major central banks and he says they're always there there shouldn't be a problem with that us federal debt here uh he had some uh uh harsh words and and I think uh waded in uh to a critique of fiscal policy somewhat which uh for him was uh you know kind of slapping Trump in the face saying hey buddy wake up or tantamount to that uh we are on an unsustainable path but it's not an unsustainable level okay he said that before he said that Under Biden he

started you know saying "Listen the US debt is on an unsustainable path." I think we can all look at that and agree no one's going to fault him for that uh as far as the level he says "We are uncertain as to how high it can go but it is an unsustainable path right now although it's not an unsustainable level." And then he said Medicare Medicaid and interest payments that's where the problem is and none of these are a Fed Issue uh the interest payments uh is related to the amount of debt that's issued which

is a fiscal and treasury issue the Fed has no control over how much debt is issued nor do they control Medicare or Medicaid domestic discretionary spending this is not a problem or an issue it has already been decreasing the issues are in here wow for the Fed chair to start pointing to specific budget line items and saying there's your problem right in There medicare Medicaid your interest payments your debt is on an unsustainable path is being as clear as you possibly can there is no Fed put the effect of trade is going to be negative

on both inflation and employment as far as rising long rates don't look for us to do anything there either markets are functioning as normal this is putting all the blame on the Fiscal how do you think uh how do you think Trump responded so this is uh what uh Trump uh posted on Truth Social uh ECB is expected to cut interest rates for the seventh time and yet too late Jerome Powell he's already given given Powell a name now the too late name once you get a name uh that's the beginning of the harassment right

now he's got a name he's he's he's going to use that name a lot too late jerome Powell of the Fed who is always too late And wrong all in capital letters too late and wrong yesterday issued a report which was another and typical complete mess everything other people do is just a complete mess oil prices are down groceries even eggs are down and the USA is getting rich on tariffs uh too late should have lowered interest rates like the ECB long ago but he should certainly lower them now powell's termination cannot come fast enough

Termination cannot come fast enough not the end of his term but his termination he can be removed for cause but let's keep in mind here cause is going to be whatever he wants it to be if you put a couple of people on the task and say "Go find me cause." If your job is to find cause you will find cause even if your cause is that he is uh a sabotur of your of your master plan Mr president he is actively working against you that is Treasonous that will be cause i uh I uh

am uh of the thinking that he is more likely than not to find cause that he will probably go down that path you cannot fire the Fed chair oh yeah says Trump who never likes to be told what to do even if you tell him that you cannot do this and nobody can do this he will do that just to show that he can do it where nobody else can do it more you say he can't do it the more likely he is to Do it removal for cause he'll find cause this is uh just

a headwind just this fight going on is a headwind for treasuries and by extension the US dollar which are already under pressure because it is a direct challenge to the independence of the Fed uh and if he follows through uh with an appointment to the Fed in line of the appointments he made where those people are loyal to Trump first and foremost before they're loyal uh to anything else The Constitution is a distant second loyal loyalty to the king uh if he has somebody or the market believes that his appointment to the Fed is going

to follow suit uh the independence of the Fed will get questioned uh and that will be really negative for treasuries really negative for the US dollar uh in fact the person uh I guess that uh that is the frontr runner uh for this one uh has urged uh the president to not remove Powell specifically because of that it Would just make his job that much more difficult do not remove him but Powell's termination cannot cannot come fast enough this is the beginning you know what's going to happen from here on in is the name calling

is going to grow the harassment is going to grow the pressure is going to grow i wonder if on poly market there is a bet for when the first death threat on Powell will occur from somebody out there who feels Powell is being treasonous because that is what it Incites is uh I would not be surprised to hear that Powell will have to have extra security um let's have a look at this little chart I drew at the bottom this little graph that I drew um because this is going to be an important setup to

the conversation on the next screen in white is uh our yield curve and I've divided it in between money market rates and capital market rates the overnight rate the Fed funds rate is 4.33% Money market rates will uh be uh a a reflection of the overnight rate so if you lower the overnight rate money market rates should rise and fall with the uh rise and fall of the federal funds rate the capital market curve is set by the market the forces of supply and demand uh in the market so the white line let's just take

that as a uh as the standard yield curve and what we've seen over the last little while are equity prices Dropping if US treasuries are acting as a safe haven and the US dollar is acting as a safe haven what we should have seen is a bull flattener this is evidence of safe haven status as the market value of equities drops in other words we're saying the correlation uh between equities and sovereign bonds is less than zero this is why we hold them in a portfolio is because they act as uh as as insurance that

if our equity prices start to fall we're not going to see our Portfolio values fall because we'll have bonds that then rise in value and protect the overall value of our portfolio we could be 100% equities but then would have to pay money to buy puts to get that kind of insurance this is the kind of insurance that a safe haven asset offers us and because it offers us that benefit we're willing to pay a little bit more than we normally would for that asset which means we tend to get lower yields on it specifically

Because it performs that function well what if it doesn't perform that function are we willing to buy it at lower yields if it doesn't perform that function at that point we would say if it's not a safe haven asset it's just yet another risky asset maybe not as risky as equities but it's no longer a safe asset it's a risky asset i'm going to need a higher yield for that well this is what we've had as equities have come down we've had a bare steepener implying that The correlation between equities and sovereign bonds is greater

than zero if it's greater than zero it doesn't offer us any insurance value any protection value there may be some diversification value if it's correlated less than one but beyond that it's yet just another risky asset in our portfolio if it's not going to provide a protection feature but only a diversification feature maybe we don't need an allocation as big to it so unless it Starts acting like a safe haven it will be allocated to as if it were a riskier asset and not a safe asset the uh bigger challenge comes from the uh foreign

holders of US treasuries if you're a domestic holder holding US treasuries at some point in the future you get your money back all you have to worry about at any point in time is if you want to sell it so you're only concerned with does the price of the treasury go down or the price of the treasury go up i can Always hold it to maturity the foreign investor can do the same thing but has US dollar exposure tied up into it so they have to start thinking of okay sure I can hold it for

the next few years to maturity or the next five or six years but where is the value of the currency going to be at that point in time i could take a significant loss because of it if they're pursuing policies that suggest that less capital is going to flow to the US that fewer Investors are going to uh invest in US assets that there'll be a global movement away from overweing US assets to equal weighting or underweing i must worry about the currency institutional investors can always hedge out uh the value of the currency but

smaller investors couldn't so at the margin there would be pressure on the US dollar uh so because uh uh foreign investors investing in US assets are really buying a structured product they have to think About both legs to give you an idea let's say and I'm just going to make up some numbers here that you're in country ABC that could be whatever country you want it to be and the exchange rate between uh ABC and USD is 140 let's say that uh uh you can um that a $140 USD or uh 140 of your currency

gets you one USD let's go that way 140 of your currency gets you one USD uh and let's say that uh uh the US dollar depreciates over time uh so that You had a th00and uh a,000 US dollars uh which is 1,400 of your own currency and the US dollar is going to depreciate uh but the value of the asset's going to stay the same let's just leave it at that for now no appreciation or depreciation uh but let's say instead of uh a,000 buying 1,400 it now only buys 1,200 because the exchange rate is

now 120 instead of 140 you've lost $200 even though the value of the asset hasn't changed because you do have Exposure to the other investment which is the US dollar you're long an asset and you're long the US dollar at the same time because the asset is denominated in US dollars you can always separate that by saying well I'll hedge out uh the uh value of the currency thereby only being long the asset for individual investors that's not really a viable option uh even for international investors hedging out the value of equity is difficult to

do because what Value do you hedge the value today the value tomorrow what if the value of equities dropped 10% now you're overheaded you actually you're actually now making an active bet on the currency which you didn't want to do so it's not that simple it's easier sometimes to say well let's just not overweight let's uh equal weight or even underweight um I uh explained this before this is the current account and the capital account the current account And capital account must be equal so if you have a negative current account you have a positive

capital account in other words a trade deficit uh is financed uh with um selling foreigners assets when you sell foreigners assets in other words you're just saying "Hey listen we got to come up with some extra money because we're spending more than we make where can we borrow money from?" I know we'll borrow money from foreigners we'll sell them Bonds uh which means foreigners own those bonds so you'd have a positive capital account balance now foreigners are only going to buy those bonds if they're willing they don't have to only if they're willing uh and

if you do not have safe haven status like this uh they're certainly not willing to buy it at safe haven prices which means yields are going to have to be higher to induce them to actually lend you money think about it as a household you earn $1,000 But you want to spend 1,200 that's fine where are you going to get the other 200 from you say "Well I'll pay you 7% interest." Everyone says "Nope i'll pay you nine." "No no not nine you're still not worth it i'll pay you 11." Somebody may say "Well okay

11 I'll lend you 200 here you go now you can spend more than you make you need someone to lend you the money." in uh in in uh macro uh terms that comes from issuing debt whether Corporations issue the debt or whether governments issue the debt somebody has to issue the debt so that they can get the money so that the in the aggregate the country can spend more than it makes uh so if you're going to continue to run a trade deficit uh you have to continue to sell your debt foreigners must be willing

to hold your debt and if you don't have this extra little benefit that you know what holding that debt has this value for us then you're not going To be priced at that on the screen I have two charts the upper one is US trade deficit since 1992 and the bottom one is the fiscal deficit since 1992 96 94 92 I do have it set up for 1992 too so that it uh sort of mirrors this this is monthly this is yearly let's point out a few things let's go to the late 90s you had

uh fiscal surplus and then if we draw a line of best fit I'm just going to eyeball this sort of downward sloping for the next uh roughly 25 years And if we go to the late 90s and do the same thing for the trade deficit off it goes uh it sort of makes sense it has to make sense look at uh 2010 uh almost 10% the uh federal deficit as a percentage of GDP if we go uh here's the recession here you can see uh the increase in the trade deficit look at 2020 it was

uh 14.7% of GDP uh and you can see the effect it had on the uh fiscal or the trade deficit and it has to GDP equals GDI what you make is what you earn uh income equals output if you want to spend more than you make you have to sell your assets that you own in other words you have to tap into your stock of savings or you have to borrow that money from somewhere if you're going to spend more than you earn uh while you have a government 2020 spending 14.7% of GDP it's got

to come from somewhere so it's either got to come from uh your own citizens and your own citizens have Savings but they do have investments as well so whatever is left over from savings minus investments must fund the fiscal deficit or you have to borrow from foreigners uh either way you're still going to have to import the stuff because you don't make it and you don't make it so you're going to have to import it but you can sell off your current assets to finance the deficit or you can borrow from foreigners foreigners are willing

to lend it to you Uh especially to the US because the US dollar and US treasury have safe haven status when things in the world go bad the US dollar gains value and US treasuries gain value and foreign holders say that is a good thing because it has value right when we need it when our assets drop in value these things save us so we are willing to lend the money to the US at a low rate because it has this feature that is what is being called exorbitant privilege is the US's Ability to sell

its debt around the world for a price lower than it normally would simply because it acted this way in tough situations it has safe haven status if it doesn't well then the willingness of foreigners to lend the US money drops at a particular yield the yield would have to be much higher post 2020 look at the the trade deficit here look how bad that got but look at uh what the fiscal deficit was each year 2020 14.7 12.1g 5.3 -6.28 28 that ends just at 2023 i have been critical of this for some time suggesting

that if you went back and even on one of the market outlooks I showed you how to do it if you went back and you adjusted uh GD uh sorry not adjusted GDP adjusted yes adjusted GDP for a balanced budget that if there was no fiscal deficit and you balanced the budget what would have g what would GDP growth have been would Have been much lower uh which means when we when we think about uh the value of US assets at lower levels of growth they would have been lower so this brings us to the

uh term US exceptionalism exceptionalism meaning the outperformance of the US versus any other market that outperformance was mostly financed by government deficits government deficits that were financed through exorbitant privilege at very low Rates if exorbitant privilege is going away if safe haven status is going away or at least at the margin is being questioned uh then US exceptionalism at the margin is going to be questioned you're moving from overweight to uh equal weight to maybe underweight these assets as I explained or as I laid out earlier when we looked at S&P 500 I'm going to

spend some time on this screen getting you to uh my conclusion uh which is uh US Treasury yields uh I think Continue to go higher uh US Treasury prices would then continue to go lower as a result and the US dollar also goes lower as a result the risk premium the US risk premium would have to increase so equity prices would have to come down for the same dollar of earnings if you expect earnings uh to be a certain uh a certain number uh and not change equity prices would still have to drop because of

the higher risk premium if you think equity Earnings are going to drop along with a higher risk premium then prices would have to drop even faster uh that's sort of where I am if the Democrats would have won uh somebody did ask me this "Well what if Harris would have won what would you have done?" Uh I would have sold treasuries right away the hope uh in holding on to treasuries after Trump won was that that uh he was going to uh get that um fiscal deficit to zero that Doge Was going to show some

good results and and you were going to stop this deficit spending that would have been bullish for US treasuries had the uh Democrats won I don't think that they would have put that much emphasis on it i would have I would have decided at that point that uh let's get out of US treasuries but the US dollar well that would have been a wild card i probably would say well stay in US equities but get out of US treasuries the US dollar is the wild Card right now I think get out of anything US US

US denominated until we see about mid4000s on equities until it until we get the repricing to price out exorbitant privilege and to price out uh US exceptionalism um to get you to this conclusion uh I'm going to first introduce a framework in which to think about the people in charge and uh for this we're Going to need uh a 2x2 matrix on one side we have a knowledgeable person uh on the other side we have an intelligent person these are not always the same people uh so let's just do a 2x two matrix and uh

we will do it this way low high low high so that we can have the cells line up nicely when you have somebody low in intelligence and low in knowledge you have a big problem uh the academic literature has a name for this it's called the Dunning Krueger Effect because what you have is somebody borrowing the title of their paper who is incompetent and unaware of it low level of intelligence is the incompetence part low level of knowledge is they're unaware of it because they don't know enough to know that they don't know anything so

uh they are they suffer a a double loss because they they don't have the skill set for something but they believe they do they're unaware that They don't know it uh at the other end of the spectrum you have somebody uh who is high in knowledge and high in intelligence this is what we would expect from the people that we have in charge is that they are both intelligent and knowledgeable but even here there is a name for people in here it's called imposttor syndrome imposttor syndrome because they are intelligent enough uh to uh be

able to uh reflect upon Themselves and they are knowledgeable enough to know that they don't know everything uh and because of that they tend to have this this syndrome called imposttor syndrome where they think that I'm not qualified for this I'm not good enough for this but they are this is who we want in charge of things intelligent people who are knowledgeable now you also have this other uh cell over here where you have Knowledgeable people who are not intelligent uh where you can say here is fact a And here is fact B an intelligent

person would say well if A is true and B is true C must be true whereas an an unintelligent knowledgeable person would say well I know A and I know B but h how are you getting C you'd have to tell them see C and they'd say oh okay I know that now but they couldn't figure it out on their own in other words you would Have to tell them these things i'm sure we've all met people uh like this who they know a lot of stuff but for some reason they just can't put two

and two together even when confronted with stuff you still must get the red crayon out and draw them a picture of everything uh so you do have knowledgeable people who are unintelligent is this administration when we're talking about uh the Steven Mirren's the the Peter Navaros the Donald Trumps are they knowledgeable people who are unintelligent or are they knowledgeable people who are intelligent there's no questioning that Navaro is a knowledgeable person he knows stuff but is he intelligent same with Steven Mirren he knows stuff but is he intelligent right let's uh let's go through this

and depending on where they End up you may you may change your mind on um on what you conclude or if you conclude what I conclude my conclusion just to give it all away is that they're over here we have some very knowledgeable unintelligent people uh who really don't know how to execute on the knowledge that they have nor do they know how to determine whether or not the outcome of what they want to do will be positive or negative they can't they can't induct or deduct Given certain circumstances they lack the intelligence to see

it i think that we're here uh which leads me to this conclusion so let's go through some of this what we what we are seeing or what we're observing is an attempt to achieve balance balanced trade bilaterally having all all these deals with these countries saying we have a trade surplus with you got to buy more from us as opposed to thinking about it multilaterally and saying we want Balanced trade across all the countries meaning that we are going to run a trade deficit with this country over here because all they have are avocados uh

and they don't have enough money to buy anything we have and well we need the avocados so we'll let that go they they don't see it that way that if we're buying the avocados from you we're clearly giving you money why don't you take that money we give you and buy stuff from us so this is what they're Trying to reach that the current account equals the capital account equals zero for each and every country it stands to reason that the sum of it must also uh equal zero as well now this way here US

dollars do not build up abroad so there'd be no demand for US dollars or US treasuries however there'd be lower issuance of US treasuries because if you're running a balanced uh uh if you're running balanced trade you don't Have to issue any debt to finance it so there'd be fewer capital securities that would have to be sold to foreigners thereby preserving the price and the yield on the existing capital securities because you don't have to then find somebody else to buy it because you're not issuing it um that means you'd end up over here x

- m equals z and I've already introduced this identity over here so if you're still going to run a fiscal Deficit net savings must finance that fiscal deficit uh and you get that through lower consumption so uh you have a US consumer that makes up a large part of GDP by consuming you'd have to say listen you got to get that a little bit lower how you can how do you get or induce someone to spend less you give them higher yields you make it expensive for them not to save you can say "Well you

can spend the money or you can lend The government some money to finance their fiscal deficit and they'll pay you 8% 9% 10%." At that point you say "H that's kind of enticing right it induces savings and if you are going to get a yield curve that starts doing this and car loans are priced off the 5-year mortgages are priced off the 10-year it discourages borrowing because to induce me to lend you money as opposed to spend it you have to offer me a higher 10-year yield let's say you make it 6% well then Mortgages

are going to be 8 12 to 9% well there's where you reduce the amount of spending or at least the amount of investment that individuals make with their savings because a house is an investment if I have savings I can either put the money into a home buy stock buy bonds uh if you want me to cut back on my spending and buy even more bonds because you're not borrowing it from foreigners well then you got to give me a higher rate you give me a Higher rate everybody gets a higher borrowing cost so it

discourages borrowing uh and induces savings however it's going to make the fiscal deficit worse why because your interest payments are going to have to go up so if this is the result we end in uh you have to get you have to get out of US treasuries that's where I get to there well what if it's the other way around what if you want to keep the level of consumption where it is and keep the level of Investment where it is saying no no we don't want lower consumption we just want more domestic consumption by

getting more domestic production what we want to do is not run a fiscal deficit but run a fiscal surplus and the fiscal surplus will fund consumption and investment because again this side equals zero and if you have a plus over here you must have a minus over here keep the spending going keep the investment going will do the heavy Lifting on this side how do you get there well it's T minus G lower the G which is government spending well that's what they've been trying to do with Doge although early results are showing nah it's

that's that's not really going to happen well the other side is higher taxes but you ran on lower taxes you ran on the idea that you were going to extend those tax cuts no tax for social security no tax for tips no tax for overtime you get no tax and you get no Tax for a while he was handing out tax cuts like Oprah um well higher taxes come uh two ways you can either raise tax rates or raise tax revenue you can raise tax revenue by making the tax base much much bigger by doing

that you say "Okay well we have 170 million people in the workforce let's get 190 million get another 20 million working let's create jobs for another 20 million uh and without raising tax rates you'll raise Tax revenue because you have more people paying the same tax the same tax rate on their income um if you raise tax rates you can do that with tariffs but you said you weren't going to raise tax rates and if we think that they are knowledgeable and intelligent they would know that they would know that a tariff is a tax

on their own people so they can do what politicians have done since the dawn of time they can lie they can lie to the people and Say it's not a tax we're going to make other countries pay other countries pay the tariff not you guys you can just lie about it but still it is a tax uh on the American consumer so you're going to get lower personal consumption uh out of that uh and lower aggregate consumption unless of course you can raise revenue by raising growth by saying why don't you just build in the

US if you move your factories to the US There will be no tariffs if you build it in the US you can get higher aggregate consumption because you get more people that consume less than they otherwise would had there been no tariffs so you can just lie to them um here's the problem with lying is you have to do it in secret if I'm trying to tell you that you can't trust our group of friends if we're in a group of friends of five and I pull you aside and I say "Listen you can't trust

those Other three people i have to do that quietly i cannot announce it in the room full of people why because now I've made enemies of those three friends if you're going to lie to your own people and say the other side pays the tariffs they're cheating us they're ripping us off they're stealing from us we're going to make them pay you got to do it quietly so the other people don't hear you well everyone heard you so now you have all of this push back an intelligent person Would have seen that and for that

reason I cannot conclude that they are knowledgeable and intelligent they are knowledgeable and unintelligent and because of that they're not going to know uh the full effect of the actions they take they're not going to know how damaging damaging can be they're not going to know when to stop until the house is on fire well I don't want to be in the house when the house lights on fire what did Trump do when he reversed The tariffs the uh equity market had touched a bare market the night before Tuesday night closed bare market territory it

only lasted uh you know overnight and bonds were just were just selling off until he came out and said okay okay 90-day pause cuz he saw it all falling apart an intelligent group of people would have seen that beforehand intelligent group of people would have said "Hey this sounds like a plan and would have had far better Execution." So somebody had said "Uh Peter Navaro has a Harvard is a Harvard PhD how can how can you say he's he's dumb as a bag of hammers?" Oh he's knowledgeable but he's not intelligent the world is full

of knowledgeable and unintelligent people trump had the uncanny ability to assemble the greatest mass of unintelligent knowledgeable people on the planet all in one place uh so this this over here is what I think was their plan is to say we Don't want to hurt domestic consumption uh we want a fiscal surplus uh we need to fix that by either raising revenue or raising tax rates since we can't raise tax rates let's lose tariffs let's just lie to people tell them that it's something else except everyone else heard them lie unfortunately and uh we'll say

this part out loud as well and I think this was the plan overall however uh given the backlash that's going on given uh the uh Uh just the way that it was done uh I don't think that that trade deficit is going to get fixed and I don't think the fiscal deficit is going to get fixed i think they will continue on but I do think they're going to lose exorbitant privilege which means they're going to have to offer higher and higher yields to get people to lend them money they have to stop talking about

taxing capital that conversation needs to end immediately and and somebody from the Administration preferably Trump has to come out and say none of that's going to happen but then who's going to believe him because how many times has he said that's not going to happen and the next day he pivots and changes his mind the cat's out of the bag on this one the conversation's already started even if he says it's not going to happen who's going to believe him because what we have are unintelligent knowledgeable people are They going to know any better uh

so because of this uh because of all of this I feel that uh you got to get out of US treasuries you got to get out of US dollar when I say out uh I I I don't I don't mean 100% out but you do have to equal weight or underweight the US at this point in time uh I have been taking that opportunity with equities that as I on green days I sell and I say "Okay I'm out of this I'm out of that that's Good." Uh I then redeploy that money into the Canadian

market uh I'm doing the same with uh treasuries now i sold a bunch of calls on TLT at 88 they expired uh I get to keep all that money so when the market opens on Monday I will uh take losses in my treasury position equal to what I earned uh selling the premiums uh so I will reduce my position and then I will do it again i will sell premiums uh on on TLT i will sell calls on TLT and very Short periods of time we're talking 2 three days at a time now I'm certainly

not doing it month by month but two three days at a time and if they expire worthless I will take losses equal to that amount and I will slowly start to move uh my allocation downwards from the position I currently have because I got a lot uh I'm not going to zero on either my US equity position or my US Treasury position but I'm certainly going to be moving it down a lot and moving into Either uh Eurodenominated assets or Canadian denominated assets i don't mind eurodenominated assets one of the things that is is sort

of uh enticing there is uh the pivot from Germany to begin to uh spend money uh a trillion a trillion euro uh the um uh European sovereign bond I think is a good idea to increase capacity uh the European sovereign bond is a uh a a structured bond with a senior and a junior tranch which then holds a whole bunch of the individual Count's bonds so you just simply buy these bonds and they're a collection of all the other bonds so you don't have to say well no one single market has the capacity there's not

enough French bonds Italian bonds Spanish bonds Greek bonds German bonds there's not enough but if they were all wrapped up much like mortgages are wrapped up into a mortgage back security and you buy a bond that's backed by a whole bunch of mortgages you buy a European sovereign bond that's Backed by a whole bunch of the individual country bonds with a senior and a junior trench now you have uh capacity uh and if you're going to underweight uh and allocators around the world are going to underweight uh or even move from an overweight position to

an equal weight position on US treasuries they're going to have to go somewhere that has the capacity for it and if they do that just at the margin if they do that will Put downward pressure on the US dollar and upward pressure uh on the euro uh so I think that uh that's probably a good place to be another place to be would be um the yen the yen still uh has h safe haven status uh behavior uh you've seen the yen increase over this period of time uh so I think as more Japanese investors

pull their money from the US that that would probably continue as well uh so I think this whole master plan Idea is attributing intelligence to a group of knowledgeable people where intelligence doesn't belong i think you have a group of knowledgeable people who are unintelligent who if you say A and B could not determine that C would be the result in which case who knows who knows where this goes because you can't count on them to at least have the ability to put two and two together anyways uh let's look at some interesting pictures okay

first Interesting one I want to show you i only have two screens here first interesting one uh I got this uh out of our discord feed uh we have a uh news feed uh which is crowdsourced uh people from around the world say "Have you seen this have you seen this have you seen this?" And ah what a great news feed uh but uh I saw this one graph which then led me to the longer story tariff shock wave leads to collapse in ocean container bookings us imports plunged 64% from March to April and this

is the last week of March versus the first week of April so you have to put it in context it's only those two weeks uh if you look at it from the beginning of the year or year over year you get a different story uh so uh containerized imports are down 20% since January this is saying 64 only down 20% since January they're still up 30% year-over-year the first week of April representing 30% increase year-over-year but it's just to Show you the amount of front running that was done before the end of the quarter one

week this is week-over-week drop in ocean bookings comparing March 24th to the 31st to April 1st to the 8th last week of March versus the first week of April global TEU's book teu is 20 foot equivalent units you know those uh containers you load on ships the really long ones those are 40 ft long uh so they count as two 20ft equivalents this is in uh 20oot equivalents uh global Down 49% week over week down 49% but again still up these are containerized imports to the US yearover still up 30% just to the US alone

year-over-year but you so you can imagine uh what the front running was to get ahead of the tariffs for uh April 2nd overall uh US imports down 64% US exports down 30% imports from China down 64 exports to China down 36% uh so those are some some big drops But again it's just week overw week what we do have to consider is the M component in GDP because our first quarter GDP uh comes out uh at the end of April it's going to be from uh January 1st to March 31st so if you had during

that period of time all of this front running over here the M is going to be very large X minus M that lowers GDP gdp now has first quarter GDP sitting at -2.2% 2% that's including uh gold imports if you take gold imports Out I think they're basically flat uh and this is as of April 17th they have it at -2.2 uh but this this front running is not showing up in there but it's certainly showing up in these numbers here to have that kind of uh drop off um plastics uh this is imports from

China plastics down 45.4% 4% copper down 31.1% wood products down 24% okay I have uh two interesting things on this screen one is a picture I Took uh and the other is a uh screenshot from YouTube the first one the picture I took uh is in Barcelona i'm downtown Barcelona walking around and I see uh people selling stuff on the side of the road and they're all holding uh you can see these ropes all of them are holding ropes and each of the rope goes to a corner of the sheet that they have sitting down

here and I was wondering well what is what's that for Uh and somebody said it's uh when the police come all they do is they pull up that rope and it turns into a like a carrying bag and everything gets trapped inside and they run no way look at that they're all prepared for that they all have these things and then they have one person who's looking around just looking around and uh if they see someone I guess they they yell you know police or whatever and then they just pull this up and all the

four corners uh create a Little bag and everything gets stuck inside the little the little pouch and then they run isn't that clever uh this other one over here uh I was watching CNN uh because uh it was a a story on um Trump wants Powell out of the Fed waiting in the wings as Kevin Wars so I thought ah let me hear what they have to say this is uh what they had up trump again calls for Fed to cut rates and says Powell's termination cannot come Fast enough now this is supposed to be

uh you know journalism you go to journalism school and you learn about journalism part of that is you learn uh English grammar because of course you're communicating you want to get it right that is a plural not a possessive but this is a possessive howell's termination cannot come fast enough that is apostrophe s CNN I should not have to do this is correct your basic grammar this is a basic mistake if you can't get This right if your people are this intellectually lazy how can we believe anything that you say on on on your show

how can we have any faith that anything you're saying is worth listening to come on man if you can't get the little stuff right if you can't get the little stuff right you know what are you doing with the big stuff anyways uh that's it for this week