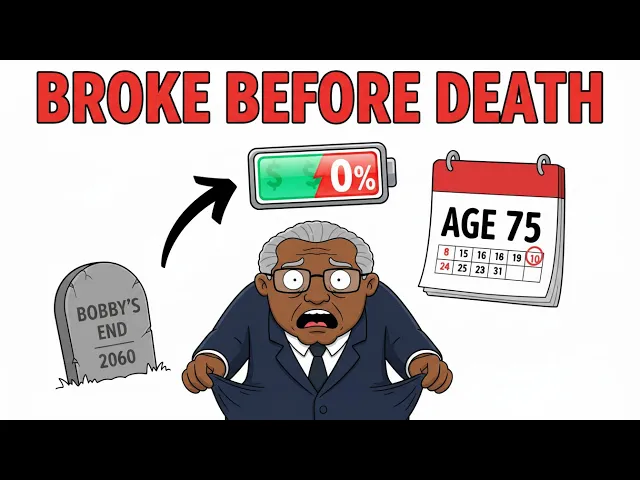

Imagine the absolute worstc case scenario. It isn't dying at your desk at age 65. It is retiring at 40, feeling like a genius, and then running out of money at age 75.

Imagine being too old to work, your skills completely atrophied, staring at a bank balance that just hit zero because you followed a rule of thumb that was written 30 years ago. There is a terrifying quiet crisis happening right now in the financial independence community. You have millions of people blindly chasing a specific number, convinced that once they hit it, they are safe forever.

They hand in their resignation letters, they pop the champagne, and they walk away. But here is the brutal truth that nobody wants to talk about. The math that promised them freedom has a failure rate.

And if you fall into that failure rate, you don't just lose your lifestyle, you lose your dignity. The difference between running out of money and having infinite wealth isn't luck. It comes down to the difference between two multipliers, 25x and 33x.

My name is Bobby and I spend way too much time obsessing over the invisible lines that separate the rich from the wealthy and more importantly the secure from the anxious. If you are someone who is grinding away right now, saving every penny, trying to buy your freedom, but you have this nagging fear that maybe, just maybe, your calculations are wrong. Make sure to hit that subscribe button and give this video a thumbs up because today we are going to audit the most sacred cow in personal finance.

We are going to put the 4% rule on trial. We are going to look at why the 25X standard might be a trap in the economic reality of late 2025 and why the 33X rule might be the only thing that lets you actually sleep at night. This isn't just about spreadsheets.

It's about making sure you never have to greet customers at Walmart when you're 80 years old. Here is the thing about the 25x rule. It is seductive because it is achievable.

The premise based on the famous Trinity study is simple. Take your annual spending, multiply it by 25, and that is your freedom number. If you spend $50,000 a year, you need 1.

25 million invested. The theory says you can withdraw 4% of that portfolio every year, adjust for inflation, and you will likely not run out of money for 30 years. But notice the fine print I just slipped in there.

30 years. If you retire at 65, 30 years gets you to 95. You're dead or close to it.

The math works. But if you're watching this channel, you probably don't want to retire at 65. You want to retire at 40 or 35.

If you retire at 35, you don't need your money to last 30 years. You need it to last 60 years. And this is where the 25x rule starts to crack.

The Trinity study had success rates of 95% over 30 years. But over 50 or 60 years, that success rate drops. And in the volatility we've seen leading up to December 2025 with inflation spikes and market corrections, relying on a model that has a 1 in 10 chance of leaving you broke is playing Russian roulette with your life.

Now you might be thinking okay so just save a little more but we aren't talking about a little more we are talking about the 33x rule. This is the counterargument to the standard advice. Instead of a 4% withdrawal rate you drop it to 3%.

Mathematically 1 / 003 is 33. 3. So you need 33 times your annual expenses.

Let's go back to our example of the person spending $50,000 a year. Under the 25x rule, they needed 1. 25 million.

Under the 33x rule, they need 1. 65 million. That's a $400,000 difference.

For the average high earnner saving 40,000 a year, that is not just more money. That is 10 extra years of working. It's 10 more years of commutes, 10 more years of office politics, 10 more years of missing your kids growing up.

This is the central conflict of modern finance. Do you risk running out of money, 25x, or do you risk wasting your life working for safety you didn't need, 33x? Let's dig into why the 25x rule is so dangerous specifically right now.

It ignores something called sequence of returns risk. This is the financial equivalent of getting punched in the face the second you walk out the door. If you retire with $1.

25 million and the market crashes 20% the very next year like we saw in 2022, your portfolio drops to 1 million, but you still have to withdraw your $50,000 to live. Now your portfolio is down to $950,000. You're cannibalizing your principal.

Even if the market roars back the next year, you have less money working for you to capture that recovery. You dug a hole so deep you can't climb out. The 25x rule assumes average returns.

But nobody lives an average life. We live in specific volatile timelines. If you retire into a recession with only 25x, you are statistically likely to fail.

The 33x rule, however, is a tank. It's built to absorb that punch. If you have 1.

65 million and the market drops 20%, you still have 1. 3 million. You're still above that critical survival line.

33x isn't about buying yachts. It's about buying sequence of returns insurance. However, and this is where it gets really interesting, there is a massive psychological cost to the 33x rule that the safety obsessed gurus ignore.

It's called one more year syndrome. I see this all the time. Someone hits their 25x number.

They have enough, but they're scared. They say, "I'll just work one more year to get to 27x. " Then they get there and the goalpost moves to 30x, then 33x.

They become dragons hoarding gold, terrified to leave the cave. The math of 33x is safer, yes, but the utility of that extra money diminishes rapidly. If you're 50 years old and you keep working until 55 to hit 33x, you have traded five of your healthiest, most mobile years for a slightly thicker safety cushion.

You can always make more money, but you can never buy back age 50 through 55. There is a grim irony in being the richest person in the graveyard. The 33X rule protects you from being broke, but it exposes you to the risk of having wasted your life accumulating numbers on a screen that you never actually needed.

So, how do we solve this? Because obviously, neither extreme is perfect. The solution lies in realizing that retirement isn't a binary light switch anymore.

It's a dimmer switch. The mistake most people make is assuming they'll spend the exact same amount of money every year adjusted perfectly for inflation regardless of what the market does. That's robot thinking, not human thinking.

The smartest approach is what I call the dynamic guard rail strategy. You aim for 25x as your quit the job I hate number. Once you hit 25x, you're technically free.

You leave the high stress corporate gig, but instead of sitting on a beach doing nothing, you coast. You earn a little bit of active income, maybe covering half of your expenses while your portfolio grows in the background. This bridges the gap between 25x and 33x without requiring you to stay in the cubicle.

You let compound interest do the heavy lifting to get you from lean fire to fat fire while you're already enjoying your life. Here is what most people don't realize about the expenses side of the equation. The 25x rule assumes your spending is rigid, but in reality, spending is flexible.

If the market tanks 20%, are you really going to go on that $10,000 vacation to Italy? No. You're going to stay home, cook your own meals, and cut your budget by 10 or 15% for a year or two.

This flexibility factor is what saves the 25x rule from failure. If you're willing to tighten your belt during a downturn, 25x is plenty. If you want to be completely inflexible, if you want to spend like a king, regardless of whether the economy is burning down, then you need 33x.

You're paying for the luxury of not having to budget. The 33x number is the price of rigidity. The 25x number is the reward for flexibility.

There's also a hidden variable that has surfaced aggressively in late 2025. The cost of health care and longevity. People are living longer, but they're living longer with chronic conditions.

The 25x rule often underestimates the explosion in costs that happens in the last 5 years of life. Assisted living, specialized care, these are wealth destroyers. The 33X proponents argue that the extra buffer isn't for your lifestyle today.

It's for your nursing home in 40 years. And they have a point. If you retire with the bare minimum, you are betting on your own good health.

That's a risky bet. 3X allows you to self-insure against the unknowns of the human body. It is the difference between a state-run facility and a private room with a view.

It sounds morbid, but financial planning is ultimately about planning for the decay of your own body. Ultimately, the battle between 25x and 33x comes down to your own personality type. Are you an optimizer or are you a pessimist?

If you're an optimizer, 25x is enough because you know that if things go wrong, you can pick up a consulting gig. You can cut costs. You can adapt.

You trust your own agency. If you are a pessimist, if you have high anxiety, 25x will feel like a prison. You will check your portfolio every day.

A 1% drop will ruin your week. For that person, the extra years of work to get to 33x aren't a waste. They are the price of mental peace.

You aren't buying money. You're buying the ability to ignore the stock market news. So, what is the actionable play here?

Don't blindly aim for a number because a blog post told you to. Run your own simulation. Look at your spending.

How much of it is discretionary? If 50% of your spending is fund money that you can cut instantly, 25x is incredibly safe. If 90% of your spending is fixed costs like mortgage and insurance, 25x is a ticking time bomb and you need to push for 33x.

And remember, the goal isn't the number. The goal is the life the number supports. Don't become so obsessed with the math of the future that you forget to live the math of the present.

If you were sitting there with a spreadsheet open trying to decide if you can walk away, drop a comment below with your number. Are you team 25X or team 33X? I want to see where the community heads are at.

And if this video helped you clarify the fuzzy math of freedom, share it with your FIRE group or your partner. We need to stop looking for magic numbers and start building resilient lives. Thanks for watching and I'll see you in the next one.