accounting for beginners and dummies fundamental principles of financial management by giovanni rigders narrated by connor sullivan introduction are you interested in learning the fundamentals of accounting whether you're a business owner student or consumer accounting information is essential in businesses and daily life accounting plays a major role in tracking income and expenses managing cash flow and filing taxes for businesses it's crucial to understand some accounting fundamentals to understand how to run a business accounting is considered the heart of any business whether large small commercial or non-profit it is the ultimate language of business which you'll need

to get acquainted with if you plan to start your own company this book is dedicated to introducing you to the world of accounting using simplified information you may have tried to learn about accounting standards before but were discouraged by the complexity of the online resources rest assured that this book is designed for beginners and explains everything you need to know about accounting you'll understand what accounting is and why it's important for small and large businesses you'll learn the different accounting standards and principles needed when creating a financial report have you always created budgets but were

never able to stick to them do you understand what happens when your paycheck is deposited into your account when you understand the basic rules of accounting you'll learn how to manage your personal expenses and stick to your budget if you're a business owner accounting knowledge will help you track any discrepancies in your business while you may be dealing with an accounting firm it's very important to learn the basic terms and standards in accounting to communicate better with your financial team were you ever in a meeting with your financial advisor and couldn't understand half of the

terms mentioned did you have to stop and research every single metric in your financial reports once you read this book you'll be able to identify different accounting terms and make significant contributions to your company the whole point of accounting in a business is to inform you of its different financial activities and measure its performance to read an accounting report you'll need to first understand a few fundamentals learning about accounting can improve your decision-making process it will help you learn about various business aspects of a company it can show you how to use limited resources to

gain maximum revenue you'll learn how to anticipate your expenses and read your financial statements this information is essential for making informed business decisions and ensuring your company's long-term viability this book will teach you different accounting terminologies in layman terms you'll learn how to differentiate between credit and debit assets and liabilities and revenue and expenses you'll learn about cash flow balance sheets and financial statements the key to success in any business lies with the knowledge of accounting this knowledge will help you stay organized comply with legal standards and create future business plans and strategies let's get

started with accounting for beginners to get you started on the core of business and finance chapter one what is accounting any business needs specific financial statements to track its accounts this information allows business owners to calculate their profits losses and expenses as a business owner you must be able to pay your debts or else your company will be deemed financially insolvent accounting informs you how much money you need to pay the company's bills and employees salaries whether your business is lucrative how much you owe suppliers and investors and if people owe you money among other

aspects accounting information is essential in defining the economic resources of any organization any business that deals with money people equipment and offices must use financial statements as a form of communication this is why accounting is the ultimate language for any company even non-profit organizations like charities hospitals and governments this chapter will discuss the definition of accounting and its different types definition accounting is the process of collecting a business's economic data the business owner or manager then uses this data to make better decisions this process requires identifying analyzing and calculating financial data and communicating it in

money terms to the people in charge the financial information is also sent to other institutions like tax collectors oversight agencies and financial regulators people inside the organization like the owners top management and human resources employees use financial data to make better investments and assess whether the company should downsize or expand institutions outside your company also require access to this financial data such as investors banks and the irs a small business may have an accountant or bookkeeper to handle different accounting tasks or use the services of an accounting firm a bookkeeper can perform basic accounting tasks

but more complex assignments require the services of a qualified accountant large businesses usually have a finance department with many accountants and financial advisors the accountant or the financial department creates monthly quarterly and annual reports and submits them to the top management types of accounting there are three main types of accounting financial managerial and cost accounting financial accounting aims to provide financial data about a company to stakeholders investors and third-party organizations for example creditors might use this information to decide whether or not to extend credit to a certain organization they need to make sure the business

will be able to pay what they owe another example is stockholders who need to know the financial status of a business to decide on a potential investment internally top managers also use this information to make knowledgeable business decisions financial accounting is concerned with all the financial transactions and operations of a company the presentation of financial information has to be consistent regardless of the type of organization using that information to achieve this there are certain rules that any financial accountant must follow when preparing accounted reports these rules are called gaap generally accepted accounting principles which were

used by the financial accounting standards board a non-profit organization created by the u.s securities and exchange commission these accounting principles allow businesses to compare financial statements issued by different companies in the same industry managerial accounting is the process by which accountants present and provide account related information to management in a structured and proper manner to carry out administrative tasks the accounting department typically issues a report every month or quarter to the business managers a managerial accountant works closely with the managers to plan budgets using forecasting and other financial tools they analyze the company's past performance

and calculate an estimate of its future performance if discrepancies exist between predicted and actual expenses the accountant investigates and reports back to management managerial accounting is not for the public and does not abide by gaap cost accounting is considered a branch of managerial accounting a cost accountant is responsible for manufacturing costs a cost accountant is responsible for manufacturing costs and they determine whether the cost of manufacturing products matches the output business analysts managers and accountants use this information to find out the cost of products money values are used to indicate a company's production rate whereas

in financial accounting they are used to measure a company's overall financial performance there are other different types of accounting like auditing tax accounting accounting information systems public accounting governmental accounting and forensic accounting requirements and skills for accounting accountants are required to abide by gaap rules by implementing a double entry method where financial transactions are recorded in two ledger accounts one for debit and the other for credit to create an income statement and a balance sheet they keep records of daily business transactions and extract information to create their reports they also perform audits from time to

time and prepare any reports needed by the management an accountant has to have a great attention to detail and the ability to track errors and investigate the causes behind any inconsistencies in cash flow costs or any other aspect of financial transactions they need analytical skills and logical thinking skills as they spend their days going through huge numerical records to ensure consistent results they have to organize this information for easy access in case of discrepancies they should be able to adapt to different accounting standards and report accurate information to managers accountants must be able to manage

their time between different clients and projects and have extensive knowledge of each industry they need to communicate complicated accounting information using simple terms and collaborate with different teams and clients a good accountant requires more than mathematical skills to conduct their accounting duties and responsibilities by now you have learned the basic definition of accounting and the usage of financial information for different purposes we discussed the different types of accounting and how they are used in business operations many types of accountants determine performance measures manufacturing costs and other important aspects that entities need to determine the financial

status of any business if you're a business owner you'll need to learn a few accounting basics the core of modern finance chapter 2 purpose of accounting financial information must be accurately recorded and summarized to be used by all organizations involved in the business accounting provides essential data about costs earnings assets liabilities profits losses and other factors needed for business operations evaluating these aspects is crucial for business strategies and creating solid financial records is a requirement for tax reports and other legal purposes this chapter will discuss the purpose of accounting and why it's important to small

and large businesses recording financial transactions the financial transactions of a business are a part of financial accounting its primary objectives are to determine business outcomes and financial status and to oversee all operations a financial accountant creates and maintains a systematic record of these transactions in journal entries whether purchase sales or other subsidiary documents this information is then transferred to account ledgers from which the accountant prepares the financial statement these records allow business managers to measure the company's overall performance setting budgets cost accounting is concerned with setting a budget and anticipating business needs it reflects business

revenue and expenses by calculating an estimate of sales and manufacturing costs it also determines other non-financial needs like estimating the number of employees needed to conduct business nowadays most businesses use financial tools to manage business activities to ensure they don't exceed the initial capital budgeting is the process of anticipating future events by reviewing the company's past performance and integrating this information with the current business plan a budget is usually estimated annually whether big or small profit or non-profit all types of organizations must set an annual budget in their business plan a budget is an outline

of your financial and operating plans a financial plan is shared with external organizations that require budget information for instance if you apply for a business loan the bank will require your financial documents to review your budget to determine if you're financially eligible these documents typically include your budgeted cash flow income and balance sheet an operating plan is shared among stakeholders managers and owners who need to see budget statements to track business resources and determine how to utilize them effectively top management also requires information about the estimated annual profit impacting marketing and sales strategies an accountant

prepares the operating plan for the managers to implement business decisions accounting is extremely important for managers to make informed business decisions conducting a cost-effectiveness analysis can help them decide whether to develop existing products or hire a production company to manufacture the product by conducting a cost-effectiveness analysis this information can save money and prevent future financial obstacles while sometimes developing production lines makes more sense financially some situations require external manufacturers to deliver the required products an executive manager can use accounting information to track the company's performance and compare it with the annual budget to make decisions

in real time using cost-benefit analysis this helps the managers adopt new projects and track the progress of existing projects accounting helps investors determine a company's real value it gives them an idea of setting their price targets and determining whether a stock is worth the investment all these decisions depend on accurate accounting records if you need to expand your company you'll need accounting to tell you when and how to start the process it will help you determine the cost of company growth performance an important measure of business performance is key performance indicators kpis this is an

overview of the performance of different departments in a company using quantifiable data in real time kpis determine financial and operational aspects including the line of credit accounts payable and receivable cash flow payroll labor productivity equipment utilization and task completion status weekly kpi reports are studied closely to pinpoint performance issues they also oversee projects and new initiatives employee performance and potential risks accountability and legal issues creating consistent and accurate financial statements is one of the main objectives of accounting the generated reports must be acceptable by various entities like government organizations tax authorities and different investors the

accountant has to ensure the arithmetical precision of a company's accounts it's also essential when business owners apply for loans to expand the company or pay their debts when a company's financial accounts are properly maintained it increases its value among the business community or individuals in the same industry accounting directly affects a company's brand and reputation either positively or negatively depending on the nature of the financial records the accuracy of accounting affects the company's legal bindings in terms of taxes partnerships or company laws among other aspects official organizations require clear accounting records from any business to

calculate income tax and vat they may reject these records if deemed unclear or don't comply with gaap standards another important objective is allowing the managers to determine and evaluate whether company policies are successful this process entails analyzing financial data of all business transactions and keeping a clear record in the account ledgers there is no practical method to detect fraud or perform cost control without accounting in this chapter we discussed the importance of accounting in any business many businesses may fail under poor financial management especially small companies or startups with limited resources chapter 3 basic accounting

principles accounting principles are the main guidelines and standards that accountants follow to generate their reports when different organizations require these reports it's easier if their format is consistent to make quantifiable data easily comparable between different companies as previously stated gaap is the official accounting standard that governs all financial reports issued by publicly traded companies in the united states the primary goals of gaap are to assure the uniformity comparability and completion of financial statements used by government agencies and investors and expose anomalies and accounting fraud or theft if a corporation wants to be publicly traded on

the u.s stock exchange it must adhere to certain established accounting rules this chapter will discuss some of the basic accounting principles used in businesses accrual principle this principle states that any accounting transaction must be reported as soon as it takes place without waiting to receive the cash flow from that transaction the basic concept is to recognize financial events by recording expenses against revenues when they occur gaap and international accounting standards require the use of the accrual principle an example of using this principle is recording a customer's invoice once issued and not waiting until you receive

payment from them cost principle the cost principle entails recording the company's assets at their original cost when purchased or acquired this amount cannot be altered due to inflation or depreciation the recorded assets may include equity investments liabilities or any short and long term assets the principal records transactions because original prices are objective and prove the assets value conservatism principle this concept is also about recording expenses and liabilities once they occur but only recording assets and revenue when you're certain of their occurrence in other words if you're not sure you'll incur a loss you must record

it immediately but if you're not sure you'll gain a profit you shouldn't record it until you're certain of the outcome your records should always lean toward expecting a loss rather than hoping for a profit economic entity principle this principle states that any business transactions must be recorded separately from the owners or business partners activities these activities include bank and accounting records that shouldn't be mixed with the assets and liabilities of different entities in a business this is done to avoid confusion and financial records and make it easier to distinguish between business activities during an audit

when recording each business transaction it should be assigned to its respective entity which can be a sole proprietor partner government agency or corporation this principle is most difficult to implement in a sole proprietorship because an owner usually intermingles their personal affairs with business affairs consistency principle this concept entails following the same accounting principle to record financial transactions to maintain consistency the only reason to change to another principle is to provide an improved approach to recording business activities the impact of that change should be recorded in the documents within the financial statements this principle ensures results

across different periods are easily comparable auditors are mostly concerned with how businesses comply with this principle full disclosure principle this principle involves recording all information that may influence the reader's understanding of the financial statements however business activities can be enormous and most accounts will only include information with a potential impact on the businesses financial status it may include non-quantifiable aspects like updates on current lawsuits or other legal disputes full disclosure entails reporting the accounting methods adopted by a business this information can be recorded in the financial statement's footnotes balance sheet or in other places in

the financial document matching principle the matching principle states that any revenue should be recorded with the related expenses in the same period if the revenue and expenses correlate they should be reported together but if not the costs are charged to expenses this concept relates to the accrual principle and necessitates recording the cause and effect of revenues and expenses for example if you earn a five percent sales commission recorded in march but paid in april the expenses for the commission must be recorded in march as well materiality principle the materiality principle entails recording a transaction if

ignoring it might affect business decisions by the people reading the financial statement gaap standards do not enforce the recording of immaterial transactions the u.s securities and exchange commission recommends recording items representing at least five percent of all assets on a balance sheet but there are smaller items that are still considered significant enough to turn a net profit into a loss the materiality principle varies among organizations where some minor items are considered material to some companies and immaterial to others reliability principle this concept entails only recording transactions that can be proven by official documents that auditors

review for instance if you bought materials from a supplier the invoice demonstrates your expenses other examples of evidence include appraisal reports purchase receipts bank statements and cancelled checks time period principle this principle mandates creating accounting reports over a standard period most businesses generate financial statements every month quarter and year when the management establishes this period gaap standards are followed to create accounting records in that period this ensures consistency in reporting and allows the managers to compare the company's performance and various metrics with the previous years a financial statement must include the time period of the

recorded transactions while this principle might seem the most obvious and widely practiced by accountants it's mainly intended for trend analysis which plays a major role in business decision making this chapter discussed some of the basic accounting principles as per gaap standards the main goal of adopting these concepts in business is to ensure its financial records are consistent and easily comparable over a period of time no matter which principle you're using in your business you need to include it in your accounting information to be easily understood by other accounting firms chapter 4 debits and credits if

you've ever looked at your bank statement for your savings or investment account or the balance sheet that your accountant sent you you've probably come across the words debited and credited while understanding how your own personal account works are relatively simple analyzing the financial structure of a full corporation may get complicated in some places debit can mean something else and in other places credit will also have a different meaning if you are providing accounting information for someone or just want to understand your financial situation better you must understand this fundamental concept of debits and credits accounting

today if you had to describe how your savings account has been operating in the previous financial year you could easily summarize it as you received x amount of money and you spent g amount of money so if you started off with one hundred dollars added another one hundred dollars and then spent fifty dollars your final balance is one hundred fifty dollars however the problem is that when managing the finances of a business even a small one there is more than one account to manage unlike your bank account a business has different accounts for different resources

for instance a business can spend from cash reserves credit available from a bank or it might exchange certain assets for other goods or services this can complement the accounting system as simply adding and subtracting values is no longer sufficient double entry accounting to solve this problem modern accountants use what is known as a double entry accounting mechanism in this form of accounting there are two entries for every transaction and that is a more realistic representation of how money actually flows through accounts accounts the cumulative value of different accounts will determine the value of the business

and whether it is in profit or loss an account is simply a categorization of different expenses and revenue streams and accompanies different assets and liabilities it is a way of sorting certain transactions into certain groups to make it easier to identify what is happening with the different assets liabilities revenue streams and forms of expenses different companies set up their accounts in different ways some can have just a handful of accounts while others can have thousands for example suppose a company sells 10 different services and 10 different products which are the only ways it can generate

revenue all these items will have their own accounts and collectively they will be the company assets similarly it will account for employee wages rent and operational expenses the expenses will be listed under liabilities when a transaction happens it will affect at least two accounts which is why there is a double entry system for instance if the company sells a product one effect will be that the company earns revenue which increases the cash account at the same time the stock account or inventory account will be reduced by one item the accounting mechanism aims to keep things

balanced this is reflected in the equation assets equals liability plus equity when a transaction impacts both sides of the equation it balances the equation in this way the accounts also remain balanced this means that you always know exactly where the money is and how it is flowing through the system debit and credit there will always be a debit entry and a credit entry when a transaction occurs it will help to think of debit as an entry on the right-hand side of the account and credit as an entry on the left-hand side of the account rather

than thinking of it as addition and subtraction for some accounts a debit will mean an increase while for others it will mean a decrease which is also true for a credit generally asset or expense accounts will increase with a debit and equity liability or revenue accounts will decrease with a debit credit entries increase equity liability or revenue and decrease assets or expenses a good way to remember this is through acronyms credit increases the girls gains income revenue liabilities stockholder equity debit increases the deal dividends expenses assets losses when you understand how separate accounts are increased

you can simply use the opposing input to demonstrate a decline it will assist in understanding some of the different types of accounts under key titles to make this easier to utilize asset accounts asset accounts can consist of cash inventory receivables prepaid expenses vehicles land and buildings expense accounts expense accounts can consist of rent travel utility salaries overhead expenses recurring expenses unaccounted expenses and advertising revenue accounts revenue accounts can consist of sales revenue interest income rental income investment returns and price decreases liability accounts liability accounts include things such as income tax sales tax interest on loans

financial service costs and accounts payable equity accounts equity accounts include stocks bonds mutual funds real estate derivative instruments and securities in any kind of double entry accounting system the use of debit and credit can not be avoided also there are some situations in which a certain transaction can impact more than two accounts for instance if you are selling an asset of the company that is also impacting the value of the company's good will this transaction will impact cash assets and goodwill in this way it is important to identify all the accounts affected by a transaction

and make the necessary changes to ensure that the accounts and the financial statements generated from these accounts remain balanced chapter 5 assets and liabilities when you look at your financial statements you will come across terms like assets liabilities and equity whether you are looking at your balance sheets or income statements these financial reports are incomplete without those key elements businesses and individuals rely on financial reports to understand how their business is performing or how they are performing as service providers this is the information used for everything from tax returns to making decisions about how the

business should be managed in the future and can even be used to understand where the business needs to focus its attention however understanding the assets and liabilities can be more challenging than it seems especially if you are trying to understand how these things impact the business's operations what makes this even more confusing is that there are different accounting standards and various ways accounts can compile these values to give you a final evaluation of your net worth or the total value of the business the differences in the way that the information is compiled are mostly because

of varying tax systems and different legal requirements from country to country and from company to company understanding what these different things are and how they impact your financial statements is key to financial literacy assets assets can be seen as anything that the company owns that holds value and can help the company earn revenue these can provide a monetary benefit or any other kind of advantage to the company however this is usually limited to things that can provide a financial benefit in accounting terms assets are classified as either current assets or fixed assets as the name

implies current assets are good for short-term gain they are current quick and can be monetized immediately current assets will include cash that is available in the till or in the bank short-term accounts receivables and inventory current assets are extremely important for business as they help the company not rely on loans and other financing solutions that would increase liabilities fixed assets are those that are similar to long-term investments in accounting terms fixed assets are those that are going to last over 18 months and will still have financial value to the company for certain companies even their

inventory can be a fixed asset for instance furniture is a product that can easily last decades and it will still have the same value as long as it has been properly stored however fixed assets are usually things like buildings or computer equipment on the balance sheet these are still very valuable things but they also help the business operations rather than just help the business earn more money assets can also be categorized as being tangible or intangible tangible assets are things like buildings or inventory that are physical things that can be physically touched in contrast intangible

assets are things like copyrights or trademarks that aren't actually physical items but still hold value in the digital era intangible assets are becoming increasingly important for instance a business's social media pages are incredibly valuable but they aren't tangible things similarly software digital content a website and all kinds of other electronic resources are all intangible assets for platforms such as facebook their intangible assets are their biggest source of income whereas the organization's tangible assets are worth very little in comparison liabilities liabilities are the opposite of assets and these are things that the business owes to stakeholders

or other businesses for instance one of the most common liabilities for small businesses is the money they owe to suppliers for their inventory unless a business relies entirely on a cash basis it will inevitably have some kind of liability within the liability section there are current liabilities and long-term liabilities when putting together the accounts all liabilities that need to be paid out within one financial year are categorized as current liabilities this can include things such as a 90-day credit cycle with suppliers monthly salaries for employees short-term loans such as bank overdrafts and even pending utility

bill payments long-term liabilities are to be paid back after a year or are payments that are spread out across multiple years for instance if a company has a loan payment a commercial mortgage or a payment plan with a supplier that extends for three years or ten years this will be considered a long-term liability liquidity liquidity is about how easy it is for a company to arrange cash to fund different business processes the more liquid a business is the less they can rely on external financing being self-reliant makes it possible for the business to cash in

on certain opportunities that may arise for instance let's say a business is manufacturing and selling furniture suddenly a competitor is going out of business and selling a large amount of raw material at throwaway prices in this case the business can capitalize on this opportunity if they have the cash to buy the materials right then and there if the business is liquid they can use their own cash to buy the cheap materials and profit from it later because their production cost will be much lower for making furniture from this low priced material if the business isn't

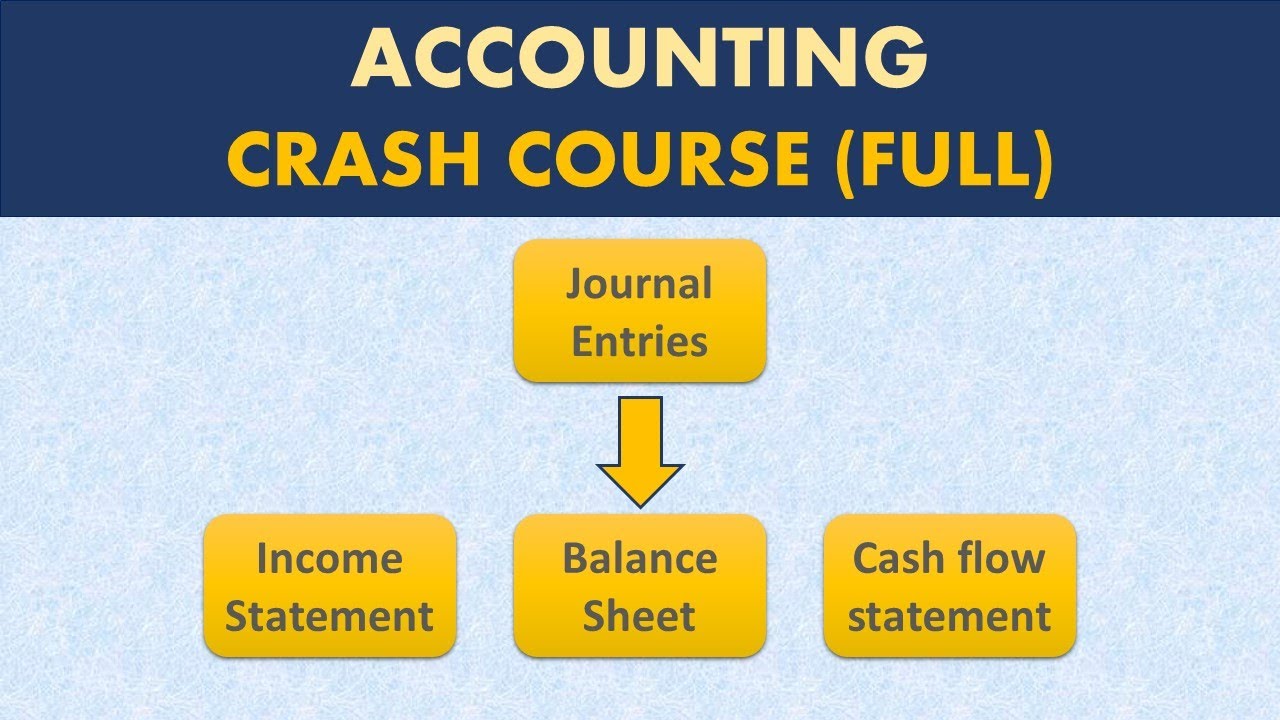

liquid and doesn't have the capital it will have to find external funding increasing the liability when you factor in the interest and transaction fees that are involved it might end up being more expensive for them this is why businesses prefer to be as liquid as possible whether that means having as much disposable cash as possible or having current assets that can be quickly disposed of to create the cash they need chapter 6 balance sheet income statement cash flow balance sheets income statements and cash flow are collectively known as financial statements these three different measurements of

a company's financial health are used to determine how well or poorly a company is doing the financial statements are used extensively by investors stakeholders financial analysts creditors and many others to understand whether or not this is a company they want to invest in technical and fundamental analysis are some of the statements used in that kind of analysis to evaluate a company from a financial standpoint shareholders of public companies are sent these statements on a quarterly bi-annually and annual basis by companies these financial statements show different sides of a company's financial situation to understand how a

company is performing it is important to look at all the different financial statements to get a holistic view for instance if a company are looking to secure a loan for a new building the lender would be interested in checking their current long-term assets and how much of their capital has been invested in fixed assets at the same time the lender would also like to see the cash flow statement to see how well they have been paying their previous lenders and evaluate the risks to ensure that debt is paid on time it is quite easy to

read the different financial statements if you know what you are looking for let's look at what they are and what they represent balance sheet in the previous chapter we looked at assets and liabilities all of these elements are represented on the balance sheet accountants list the assets on the left and the liabilities on the right side of the statement some companies prefer to list assets on the top half of the statement and the liabilities at the bottom these figures are set up in the same way as the accounting equation the goal is to demonstrate how

the company's total assets compare to its entire liabilities when viewing this data the different asset classes and types of liability are broken down under appropriate headings there will be a section for the current assets and one for the long-term assets and some might even differentiate between tangible and intangible assets one of the most important parts of the balance sheet is the shareholders equity section this area shows how much the company has grown or shrunk in relation to the initial capital invested into the business it also shows how well the company has been distributing its earnings

in the form of dividends something that investors are most interested in the challenge with the balance sheet is that it is a static image of the company it does not provide a comprehensive view of the company's long-term success rather it displays what the company's financials looked like on a specific day of the year income statement even though shareholders and investors want to know their potential revenue this is a bit different from what the company actually earns this is because the company doesn't distribute everything that it earns rather the company will set a certain percentage as

the amount it will distribute from its net profit to determine how much the company actually makes in profit one needs to look at the income statement as we discussed in previous chapters debits and credits in various accounts are shown in the income statements the income statement shows how much a company earned over a certain period of time where these earnings came from and where this money is going this is where you can see how much tax the company pays its net profit its revenue and the financial impact of the balance sheet in terms of the

company's performance the income statement is like a funnel at the very top you have the raw turnover of the company and how much it earned from its operations usually known as the gross turnover it is called gross turnover because it has not yet been sorted or refined and expenses have not been considered you remove some expenses as you go down a step and are left with a slightly smaller number as you progress further you can see how much each expense costs and at the very bottom you can see the net profit often known as the

bottom line statement of cash flow this statement is all about monitoring how the cash is being used within the company the statement of cash flow is usually constructed based on data gathered from the other two financial statements rather than showing definite values the statement of cash flows is more about showing the changes in the amount of cash the company has in different operations the three main operations that companies are interested in are operating activities investing activities and financing activities operating activities reconcile the information from the income statement and show how much cash the company earned

from those activities for instance certain things are modified in the section that are not addressed in the income statement itself for instance the adjustment of depreciation the investing activities show what the company has earned or lost from various investments these are usually long-term investments such as buying land or other fixed assets it will also show any changes in the investment portfolio if the company has changed how it invests financing activities show how the company raised capital how much it raised and what these things were used for it will also show how the company managed major

cash related exchanges such as paying back loans chapter 7 revenue and expenses for most businesses there are multiple streams of revenue and various forms of expenses that they have to manage also there are different kinds of revenue such as sales revenue dividend revenue contra revenue and others similarly expenses also come in different forms such as fixed variable non-operating and others revenue when accountants calculate revenue it is very different from net profit or net gain this is because revenue is just the total earnings from sales we don't make a profit until we've deducted all of our

expenses from our revenue also the way revenue is recognized can vary from company to company most businesses rely on the principle of revenue recognition according to this principle revenue is only recognized once the risk of ownership of the goods has been transferred to the buyer or the service has been rendered and it is no longer the seller's responsibility it is important to note that the transfer of money is not considered under this framework this means that enterprises that sell on credit will include credit purchased goods in their revenue rather than in their cash account credit

sales raise receivables but are still considered revenue when cash is paid later it is simply viewed as a reduction in receivables and an increase in cash rather than impacting the revenue amount a lot of businesses use different frameworks to calculate forecast revenue when businesses are small selling small quantities of products or just having a handful of clients they are catering to it is quite easy to estimate revenue a simple database of all the sales and prices at which they were sold can be compiled to see the total revenue when businesses are dealing with millions of

transactions per month and there are hundreds of thousands of products to look after it is easier and quicker to simply use an average of both the sales volume and the sales price to estimate how much revenue they have earned or will earn in the future revenue forecasts help you determine how quickly and how much you want to scale your organization but they're very different to estimate or calculate and must include everything from covering the rent to paying salaries and buying inventory also when a business is rapidly expanding it needs to know how much it will

be earning well in advance to adjust accordingly for instance with an estimate of the revenue for the next year a company can be better positioned to make long-term decisions and formulate a plan about how they want to grow expenses expenses can become extremely complicated in the way they occur and how they are calculated in simple terms an expense is money that a business spends or the costs incurred while the business operates in some cases they can be extra costs that are not directly related to the business for instance if a natural disaster brings down a

warehouse that is a cost that the business will have to bear but it is not something they had anticipated nor is it a standard part of day-to-day business in accounts there is a differentiation between costs and expenses whereas these terms are usually used interchangeably in other fields costs are clearly defined as expenditures incurred in order to purchase an asset on the other hand expenses are expenditures made to generate revenue as a result while all expenses are part of the cost not all costs are expenses when calculating expenses accounts also cater for things that don't use

cash but are an ongoing loss of value for the business for instance depreciation on a vehicle or a piece of machinery is an expense that does not require cash once you have bought the vehicle you have incurred a cost that cost is the investment to buy the car but then this investment also depreciates over time similarly some expenses are incurred once but they are accounted for later or when necessary for instance if you have paid rent for a building for the entire quarter this will not be accounted for in the first month instead the account

that factors in the rent for that specific month even though the entire quarter's amount has already been debited this is done to make the financial statements accurate and appropriate for the time when they are generated if a prepaid cost for the entire year is deducted from the revenue in just one month it will lead to an inaccurate reporting in the same way not deducting depreciation will result in an over-evaluation of the business's assets the income statement gives an overall picture of the company's expenses whether long-term or short-term variable or fixed conclusion accounting is a critical

process for businesses service providers and whether you are a business owner or an employee and need to manage your finances better understanding accounting and how it is used to organize all the monetary resources of a business can help you bring more order to your own financial life on the surface it can seem like a complicated matter looking at all the different financial statements and using all kinds of different formulas to make sense of the numbers on the sheet can be challenging once you know what the different things mean and how they are interrelated it gets

much easier than it looks however as you add more variables to the mix and construct a financial report that meets the demands of increasingly complex frameworks it can get difficult an easier solution for people today is to use software or an app to manage their finances these accounting systems have everything you need already in place and you just need to plug in the values for instance if you want to make a balance sheet rather than build it from scratch you can use one of the pre-made templates and simply build one right there moreover it gives

you the option to build all kinds of financial statements depending on what you want to use them for within these apps and software you can run a large selection of formulas and equations that will help you find the specific things you are looking for it can help you analyze your own information if you need to present it to someone else if you are a small business owner who needs to manage accounts getting accounting software will be an investment that will provide you with a lot of value you just need the software rather than having an

in-house accountant then you can outsource the software management to a freelancer most businesses don't really need an accountant on a daily basis anyway the only time they really need one is near the end of the month when they need to compile all the transactions and evaluate profitability a freelance accountant can be hired for a few hours at the end of the month and they can manage everything directly from your software even if you are pursuing accountancy as a profession it is highly recommended to familiarize yourself with the latest digital accounting tools gone are the days

when accountants had to sit down with stacks of registers and a calculator today with the latest business management solutions most things are being tracked live and they are only being put in order by the accountant using various financial software solutions the real skill is still in understanding the different accounting standards and then creating a statement that meets those requirements accountants will likely stay with us even with the advent of ai and it is still a very profitable profession to get into disclaimer notice please note the information contained within this document is for educational and entertainment

purposes only all effort has been executed to present accurate up-to-date reliable complete information no warranties of any kind are declared or implied readers acknowledge that the author is not engaging in the rendering of legal financial medical or professional advice the content within this book has been derived from various sources please consult a licensed professional before attempting any techniques outlined in this book by reading this document the reader agrees that under no circumstances is the author responsible for any losses direct or indirect that are incurred as a result of the use of information contained within this

document including but not limited to errors omissions or inaccuracies this has been accounting for beginners and dummies fundamental principles of financial management by giovanni rigders narrated by connor sullivan copyright 2022 giovanni rigdurce production copyright 2022 giovanni rigders