Okay we're very busy thank you community breakfast thank you you would read the slide okay so where were you I missed you the last two plus yeah but he caught up with the glasses right I'm trying to be explained to me designs I don't think you need a reminder that Your next Quiz is a week from today but I'm going to give it to you anyway so it is a week from today for 30 minutes of class I will send you the seating assignments by next Monday or so you'll have you know so again it'll

be three I think we'll be back to three rooms again because I you know the two UC rooms in this one and I'll try my best that's all I can do to make sure that you rotate fairly I think two-thirds of the class have already Been out of this room there's another one third day we'll get first tips on it the final have no idea how I'm going to do I have to toss a coin I really have no idea um the material for the third quiz will cover everything in packet two which we will

finish today so we'll be done with packet two which means next Monday please make sure you download the third and last packet it's a much Slimmer Packet last packet of the class So today we're going to complete our discussion of private company valuation and I started this discussion already with one of the bigger challenges when you value private companies you remember I said when you value public companies you make an assumption and the assumption is the marginal investor is well Diversified what does that do when you make that assumption it allows you to focus only

On the risk that you cannot diversify away an estimated with the beta the minute you use a beta whether you like it or not you're making the reception and I said in a private company that might not be true because the buyer might not be diverse so in fact might be completely undiversified so with today we're going to go through the mechanics of what to do but I want You to give me the intuition as to what is going to happen to your cost of equity and cost to Capital when a buyer is not Diversified

so in a buyers to person focus on beta we come up with a cost of equity in a cost to Capital right let's say you take the same business but now you're looking at a buyer's completely undiversified they're going to put all of their money in that company Will they see more risk in the company or less risk more why because they're looking at all of the risk risk that you can eliminate about so you've already kind of answered the question so what's going to happen to the cost of equity then it's going to go

up the cost of capital is also going to go up today we're going to go through the mechanism of how to do that but to show you why not all private business buyers are made equal or owners Are made equal in on May 9th I have an engagement you can call it that to go talk to the Mets management it's actually a bundled engagement in the morning I'm talking to the 0.72 analysts the afternoon I'm talking to the meds management you know what binds them together right the owner is Steve Cohn on both so somebody

who's in Steve Cohen's office asked you know can you come to talk to the point because I've done that before And I said sure So I'm going to go talk to them about narrative and numbers because these are young analysts they've come through they've made the they made it in a sense to under the peak hedge fund like places and our so I said sure and then later I got a call saying oh by the way would you be willing to come to talk to the Mets management and I said I would but it has

to be understated it's a day before final start so I said I've got to be in the same place so 0.72 is In Hudson yards and they said we'll get the match management down so yesterday afternoon I was putting together my Corporate Finance presentation for the match it's fascinating to think about how decisions get made at professional sports team and one of the issues that I ran into one of the things I was trying to estimate was a cost of equity for the Mets plus what currency should I do it and Let this easy one

US dollar say why go looking for trouble right I could do a Japanese Yen or a Euro but you know what Equity risk cream should I use same equities elsewhere the price of risk of the price of risk which leads me to the question of Bayless right how many publicly traded sports franchises are there in the US one actually just one it's Madison Square Gardens the closest thing you can Get and even that is not a pure franchise it owns the next but it also is all of the other stuff that happens the Green Bay

Packers are technically owned by the people of Green Bay but there isn't a single publicly traded sports franchise in the US there are publicly traded sports franchises in Europe mostly soccer Clips so one alternative is to go with soccer team betas so that beta was like 1.16 the other of course is to focus on Entertainment companies after all once you get to professional sports yesterday I went to a Yankee game cost me a hundred dollars two people but even with the price you know I got a decent price this is like going not just to

a movie but to a concert so I said it's like entertainment the average pay for entertainment companies is 1.10 but no matter which beta I use I'm focusing only on the risk that cannot be Diversified away right But is Steve Cohen an undiversified owner is the only thing Steve gone owns the Mets no it's one of you know he's all I think worth 15 billion maybe 18 billion three billion dollars or four billion dollars whatever he paid for the Mets might sound like a lot of money 99.99 though well but to him it's one of

a bigger portfolio so I'm going to argue for the use of that public company beta there And I'm going to bring up the Yankees all of the time during this session simply to bug the people in that room but this is the one place where bringing up the Yankees it's going to make them feel better with the mats you can use the market beta because the owner is in a sense Diversified right who owns the Yankees come on guys you live in New York even if you've never gone to a baseball game you should know

the answer The Steinbrenner family how much of the standard in a family is tied up in the Yankees you think almost all of it it's a seven billion dollar franchise they're not rich outside of this they might have a hundred million or 100 million there the steinbetter families almost completely undiversified so you know what that means right if you think purely financial terms the match should have a lower cost of equity than the Yankees Right now I don't know how this will play out but file that away for future reference it's not that it's a

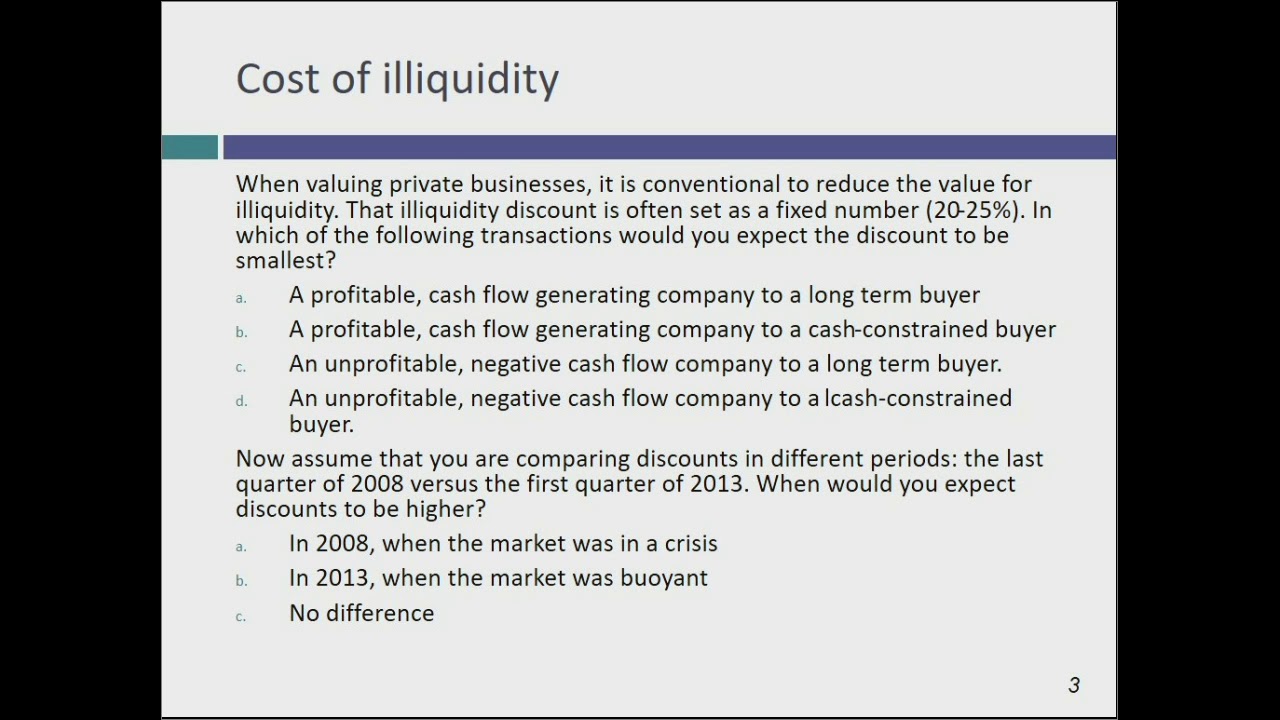

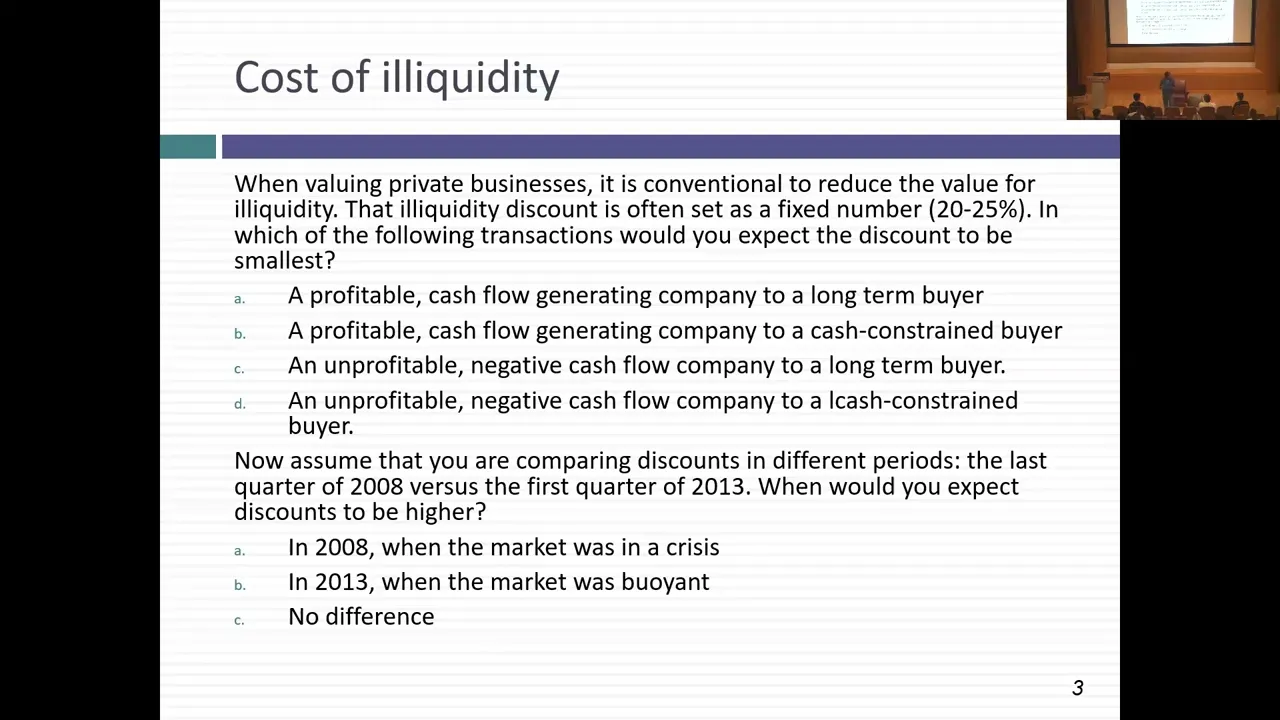

private business but the buyer of the business is not Diversified that's causing you to adjust that cost of equation so we talk about the process of adjusting the other big thing we have to deal with is this issue of in liquidity cost of buyers remotes in the example I gave right you bought something you changed your mind and you sell it back Right away the cost of bias remorse is what it costs you to make that round trip with a publicly traded stock it might be small especially if it's a large widely followed stock heavily

traded but to the private business it can be immense so what do people do they discount the value that they pay for these companies up front for an expected a liquidity event So today I want to talk about how appraisers deal with that in liquidity and private company valuation why I think it's wrong and here's what the appraisers do to deal with the liquidity so there are far more private business appraisers than publicly traded company analysts in the in this country there are thousands and thousands of appraisers and the way the value private companies they

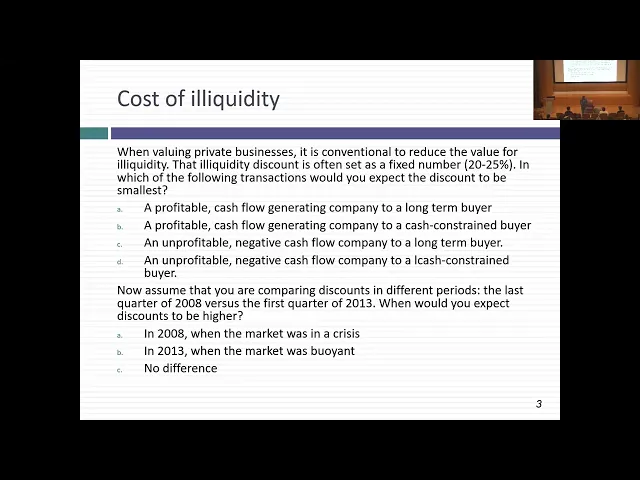

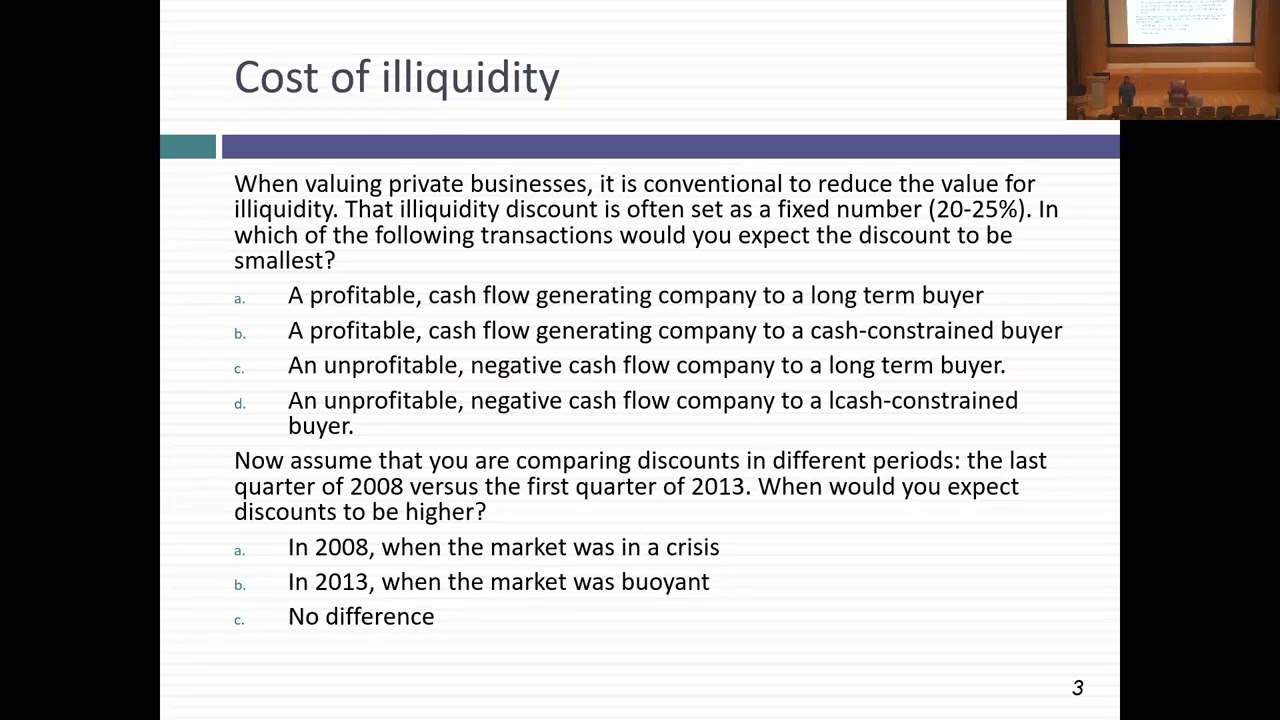

do a version of a discounted cash Flow model I'll talk about how they adjust for lack of diversification but after they do the valuation they will reduce that they'll take 25 off the top it's called in a liquidity discount and they do it for every company they value small large money making money losing and I think that doesn't make sense and to see why I'm going to give you four companies or four transactions and I wanted to rank these companies in terms Of transactions where it has the biggest liquidity discount and transactions will attach the

smallest discount so here's the first one it's a profitable cash flow generating company to a long-term buyer a profitable cash flow generating company to a cash constrained buyer so two different buyers or you can have an unprofitable negative cash flow company to a long-term buyer or cash constraint buyer so let's focus on on first the money making versus the money losing Cash which should have the larger liquid discount the cash flow generating company or the negative cash flow company the negative cash flow company why what's the essence of liquidity you want cash right if you

have a company that's already throwing off cash it's profitable you're actually getting liquidity from the company running if you have a money making cash rich company it's throwing off cash flows you Feel less of a need to have to sell the company to get cash I'm not saying the need goes away but it's less so I'd expect the discount to be larger for unprofitable cash negative companies should the discount be greater for a long-term buyer or somebody who's cash constraint yes people why because you need the cash flow much sooner right you worry about liquidity

you're gonna you see already I'm setting Up a nightmare scenario for you because if I'm a private company owner and I come to you and say Can you estimate what my liquidity discount should be you can't answer the question until you deal with two things one is what kind of company am I am a money making or money losing do I have cash flows that are positive or negative and the other is you can't tell me what the discount is unless you know who the potential buyer is Already that's going to create a layer of

uncertainty about the discounted plan let's build on this liquidated discount so it's going to be very different across different companies depends on the buyer let's say you estimate these discounts at different points in time first time you estimate it is in 2008 Market is in turmoil you're in the middle of a crisis second time you estimate is five years Later Market is doing well the economy is doing well do you think the discount is going to vary across time and if so when is it going to be higher when the market is in a crisis

on its boy yep and tell me why everybody wants cash right everybody wants liquidity essentially liquidity discounts are not Really going to be different depending on the company and the buyers they're going to be different across time so we'll at least set up the framework for thinking about a liquidity today one final point given what I've said so far about potential buyers and diversification let's say the owner of a private business you're thinking about selling your business and you want the best possible buyer Best in what sense you Want to get the highest price and

I give you three different choices another private individuals willing to buy a business the second is a private Equity Fund and the third is a publicly traded company which one do you think is likely to offer you the highest price a private buyer a private Equity Fund or a publicly traded company you sure you want to try that Your one in three chance this time usually I give you 50 50 shots if you can pass if you want okay okay go ahead and tell me what it is that makes it say business right so what

is it that makes your business more valuable to publicly traded company well that's kind of a that's deceptive reason right what's the first thing I started with we talked about discount rates what do we say the When you look at risk what does the risk you look at the risk you if you're a publicly traded company remember your investors are Diversified all you care about is Market risk you can focus on a traditional Market beta come up with the cost of equity a private buyer is usually much more likely to be on Diversified so holding

all is constant I would expect the public company to offer the highest price the private buyer to offer the Lowest price and the private Equity Fund to fall somewhere in the middle today we're going to quantify that impact and let it lay out deeper questions because it because private Equity Funds are there to try to make money right how do they make money they Arbitrage the difference we do not the private company thinks it's worth to a private buyer and what the private companies were to that's how private Equity Funds make their money They buy

it somewhere in the middle and they either take the company public or they sell it to a public company that's their exit so let's go back to where we were in the notes and kind of fill in the details I think we were on page 134 let me take you back to page 134. so let's I'm going to set up the example so let's say you guys are graduated you're working at investment Banks sorry but I blow my nose But you're getting tired of the grind so you're planning to quit and here's what you're going

to do you're going to take all of your wealth and this is critical to the story and you're going to buy this upscale French restaurant why because you've been watching Kitchen Confidential on in the Food Network and you say this sounds like so much more fun than working on spreadsheets I'm the owner of the restaurant I'm also The chef the restaurant is a world regarded in the most recent year and I show you the income statement they made four hundred thousand dollars in pre-tax operating profit on 1.2 million dollars in traffic so I'm going to

give you three years of financials the company has no debt outstanding but it does have a least commitment of 120 000 each year for the next 12 years the restaurant sits on beliefs So what we're going to do is value the restaurant for you the investment bank and remember all your wealth is going into this restaurant and I'm going to start by showing you the financials for the restaurant last three years of numbers big jumps 800 1.1 million 1.2 million but there's a catcher the restaurant has been growing but it's now at full capacity what

does that mean every table is taken for every meal so You can't be growing anymore unless you you know unless you decide to build a second restaurant there is operating least expense I'm doing what accountants used to do pre-2019 treated as an operating experience I wages material other operating expenses but uh one thing I want to mention about the wages is remember I'm the ownership I don't pay myself a Saturday why not because all what's left is going To come to me anyway what's the problem of you valuing this restaurant based on this all even

if you there are no no I'm not putting any Shenanigans here the numbers are what they are if you buy this restaurant based on what you see on this income statement say look that seems like a lot of money what's the problem you're going to run the day after you buy the restaurant you should Well give me the so the next day you're going to walk into the restaurant it's now your restaurant right but you notice there's nobody in the kitchen so why isn't anybody cooking you know what happened right I was a chef I

started the restaurant so what do you have to do you have to bring your cooking skills to play and be Chef you know how quickly the capacity is going to go from 100 to zero percent right because all you can make is peanut Butter sandwiches and I think that's the only thing on the menu you're not going to last as a restaurant so you know what you have to do to actually make this restaurant well you'd have to hire a chef and it's going to cost you and it will build in that cost into your

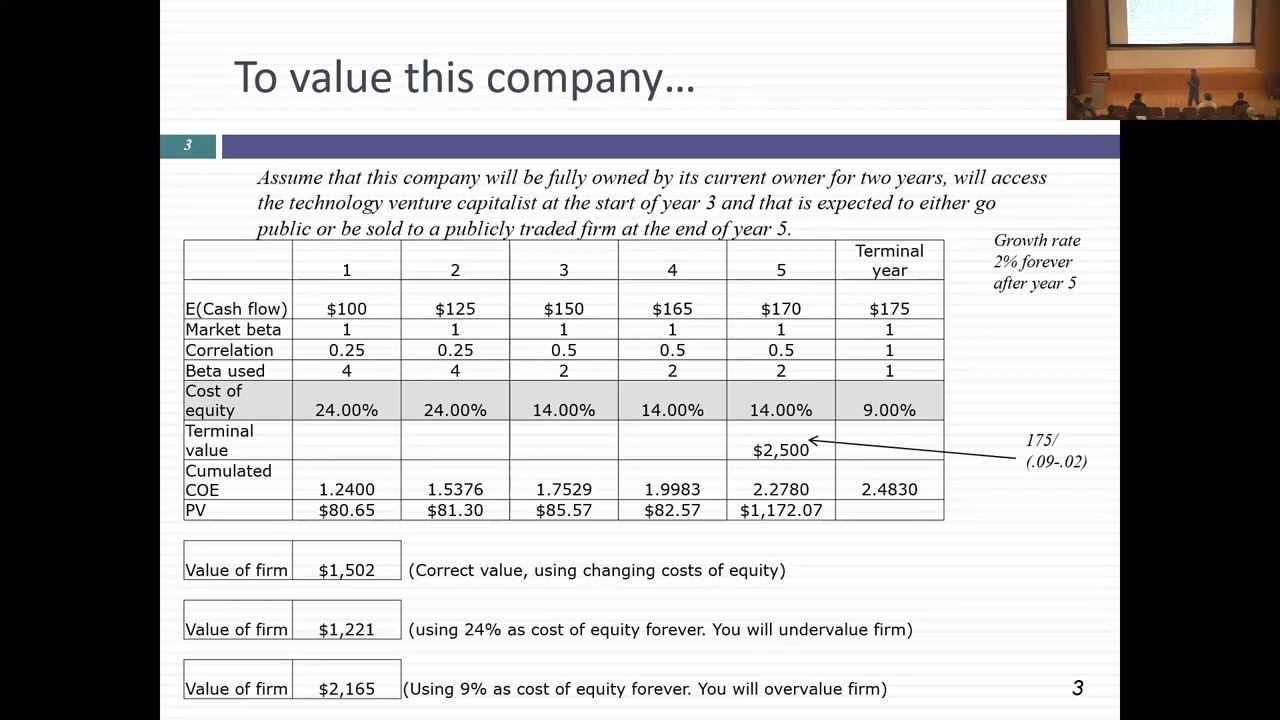

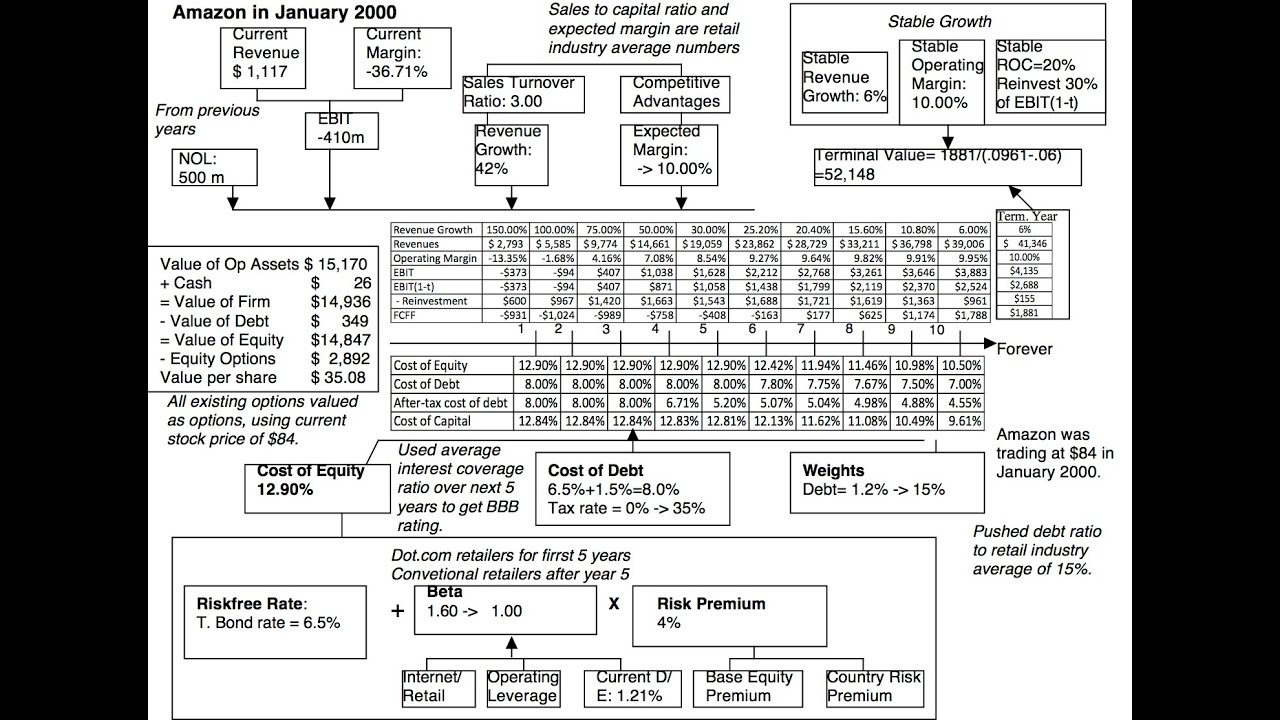

income statement so already you can see the work coming into play to Value this restaurant you need to bring in all the pieces you will need to run the restaurant So let's go through the process of adding the restaurant starting with a discount rate what do we need for a discount rate I need a beta and a it's a risk-free rate and a screen going to come back for sure oh thank you so let's talk about it is it it should be on right now suggestion let's talk about estimating this confidence I need a beta

right so I go to a Bloomberg terminal enter the name Of this restaurant and type in beta what am I going to get nothing can't find the company valuation ends right there saying I can't find a beta but we don't give up that easily right because if you can't find a regression beta you can still get a beta for your company by looking at publicly traded companies in the same space so initially that's what I did I went And looked up publicly traded restaurants and I came up with the beta but it wasn't the kind

of beta that you're going to you're going to be happy with so here I'm going to start exactly the same way that I start with public companies but I still have to deal with that problem of lack of diversification but the beta that I got by looking at restaurant companies reflected a mix of restaurants that were Not similar to the restaurant I was planning to buy this is an upscale French restaurant what I see on my restaurant list are Burger King and chipotle and I mean I mean their their restaurant chains but they're not the

kinds of restaurants so I decided when I value this restaurant to actually use the beta for specialty retailers now luxury retailers arguing that the people who come to my restaurant are the kind of people who Shop at those retail stores be creative when you think about betas I know our tendency is to look at other companies in the same sector and stay focused sometimes you might want to shift that Focus because you want to get look at other companies that do well when you do well and do badly when you do badly here I'm going

with a group of companies that I think is closer to my business in terms of up and down movements than looking at just Restaurants so I got none Levitt beta so that part of the process was pretty similar to what I do with public companies I'm just looking at other publicly traded companies in this space coming up with debate we'll have to deal with the lack of diversification but have an unleaven pain now what's the second step I have to bring in the fact that that captures only the market risk In the company and what

did I say about this and about you as an investment banker you took your entire wealth and you put into this restaurant you're the exact opposite of Diversified right you're over concentrate so what risk are you going to see let me set it up in a very simple way if you look at the total risk in a company there's units of Market risk and units of firm specific risk if investors are Diversified all they care about is The market risk it's captured with the beta if you're not Diversified what do you see you see all

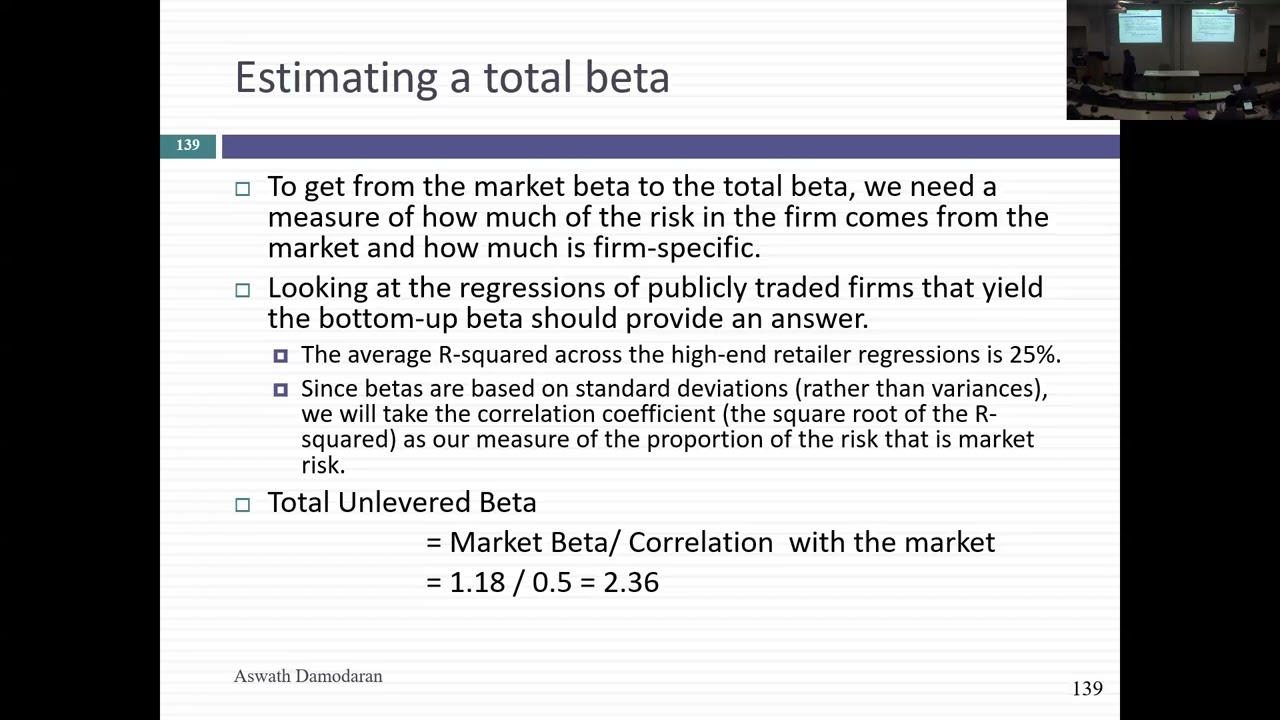

of that risk and you need to bring all of that risk into your cost of equity you know might say how do I know what all of that rest of the risk looks like is a very simple number and it is a number that you get anytime you run a regression that I think you can use to adjust your beta so here's what I did I went into my Bottom-up data page remember I got the publicly traded companies and paid us and if you remember when you when you look at a regression page for your

company in addition to a beta for your company you have an r squared for your company right what does the R square tell me that market regression how much let's be specific how much of what which in this case is The company so basically how much of the volatility in the companies explained by the market right so R square tells me that what does 1 minus the r squared then done how much of the risk in that company is not explained by the market in other words every regression you run tells you how much of

the risk in your company comes in the market and how much is company specific we don't use it usually because we're publicly traded companies We ignore that here I'm going to bring it into play in addition to looking at the betas I also looked at the average r squared across these high-end retailers the average r squared was 25 percent there's little statistical tangent R squares measure the proportions of variance in your stock that is explained by the market beta is a standard deviation measure some you have no idea what I'm talking about right so anybody

remember the full Equation for a beta you might have seen it in one of your foundations class what's in beta is equal to rho JM correlation between the stock and the market times the standard you know you look mystified you've never seen this actually that's that's that's how the regression the slope is computed it's rho JM times Sigma J standard deviation stock divided by Sigma of the market standard deviation amount even if that Went completely overhead it's a standard deviation measure so I'm going to take the r squared which is a variance measure and take

the square root of the R square I want to insult you by asking you what the square root of the r squared is it's obviously going to be the correlation coefficient which is the r so here what I'm going to do is I'm going to take the correlation coefficient which is 0.5 and I'm going To play a little algebra again the 1.18 that I computed was a market bait it captured the market risk in the company and if I were Diversified I'd stop there but you're not Diversified in addition to bringing that risk and you

want to bring the rest of the risk in the company into your beta so dividing the beta by the correlation gives me what's called a total beta the reason I call it total beta is I'm capturing the total risk of the company rather than just the Market risk it's going to give me a beta of 2.36 twice as high as the market beta and the only reason I'm doing this is because the buyer is not Diversified so work it through 2.36 beta is going to give me a much higher cost of equity the much higher

cost of equity is going to give me a much higher cost of capital and it's coming from the fact that the buyer is not divided by but this is still a Non-level beta right so it's a in publicly traded companies after you came up with an unleavid of your company what did you have to do to come up with the beta to use for your stock you have to level the beta and to deliver the beta you needed debt to equity ratio and that debt to equity was it a book Debt or Market debt to

equity ratio after two quizzes I hope you get the Right answer it always is Market debt to equity and with the private company we have a problem you see what the promise there is no Market Equity debt I could dance around perhaps use book Debt but there is no Market equity you can't use book Equity it's completely irrelevant so you're saying what do I do now there are two choices the first choice is an easy one but you might not like it You can assume that if I can you can get the debt to equity

ratio of a publicly traded companies in the space which is 14.33 percent you can assume that private companies also operate with roughly the same debt to equity you're making the assumption that there's something about this business that leads companies to pick the debt to equity ratio data you put the 14.33 and you come up with a levit of 2.56 and a cost of equity of 14.5 Percent but that's assuming that private businesses borrow roughly the same as public companies in that space what if you don't want to do that is there another way I can

come up with the debt to equity ratio for a private company but I don't assume that it moves to the industrial average what do I not have a market value of equity right Why am I doing the value at the end of the evaluation where do I arrive at for your company an estimated value of equity for your company could I use your estimated value of equity as the equity in your debt to equity ratio I don't see why not but there's one small problem right you see what the problem is I'm going to have

circular reasoning Because I need the equity to get the debt to equity I need the debt to equity to get the equity have you ever checked the iteration box in Excel you had to for my fcff kids if you do that you can actually make the debt to equity ratio for a private company a function of your own estimated value of equity so I'm not doing it here but if you want to do it in the spreadsheet you can but just make sure the iteration box is Checked otherwise you're going to get lines all through

your spreadsheet about circular reason so two choices with debt Equity where you can either use the industry average which is what I've done here or you can go with this debt to equity that came from your own estimated value equity I'm almost there I have a cost of equity I need a cost of debt and here I'm going to follow a much more conventional route With public companies which did not have a bond rating remember how I computed the cost of debt I compute an interest coverage ratio I went to a lookup table I came

up with the rating and a cost to debt I can do that private companies as well and here I compute an interest coverage ratio based on the lease expenses I came up with a default spread based on the rating I gave them a double b plus rating and a cost of debt of seven and a Half percent pre-tax and four and a half percent after tax so I've got a cost of equity from the total beta a cost of debt from the synthetic rating my cost to capital for the company is 13.25 percent I've got

my discount rate using a private company evaluation much higher than the discount rate for for an otherwise similar public company because I'm using that total beta second stop I had to clean up the income Statement cleaning up you're basically meant paying for a chef who's actually going to cook 150 000 that pushes up my expenses and I capitalize leases because that's the right thing to do now starting in 2019 accountants have done this with public companies but many private companies people still can expense operating leases so I'm capitalizing and treating it as dead so there's

my restated operating income my operating income is 370 million instead Of 400 million so I've got number I've got a discount rate I've got my earnings step three I'm going to stop and check to see how much of an effect the chef leaving is going to have I've replaced him with a new chef but remember one reason the restaurant is at capacity is because people coming in like the chef they like the food and I don't know how what percentage of those people will not show up next the next day if I buy the Restaurant

with a new Chef so I estimated that loss of Revenue that I'm going to get if the chef leaves to be 20 of my operating income so I'm going to take 370 000 and knock it down by 20 percent this is the key person discount we talked about towards the end of each class it's lower my lowering my operating so I've got a discount rate I started with the operating command adjusted it for the loss of a key person And again as a chef you might try to figure out ways to reduce this loss because

it shows up as a lower value for you and you might stay on for a year or two maybe have some kind of adjustment process where the losses lower but if you don't do that there's going to be a 20 loss step four just because you're doing the private company doesn't mean you can forget all those rules we had in evalued public companies like what to grow you Have to reinvest how much you have to reinvest depends on your return on Capital in this case I've estimated a return in capital of 20 for this privately

owned restaurant and I'm going to give them a very low growth why because they're already at capacity they can't grow more than a certain number because you're you know every seat is taken so putting a two percent growth right two percent divided by 20 gives me a reinvestment Rate of 10 percent so I've got my discount rate I've got my income I've got my reinvestment rate I bring it together in my valuation so there's the key person adjusted operating income growing at two percent next year one minus the tax rate times one minus three investment

rate so that's expected free cash for the firm next year divided by cost of capital minus the growth rate I come up with a value for the restaurant of 1.449 Million I'm almost done because there's one final step I have to subtract out the debt which in this case the present value the leases the value that I get for the restaurant is 521 000 dollars that's the value of equity in this restaurant five twenty one thousand what's the final adjustment for a liquidity right if I buy this restaurant is the investment banker and I put

all my wealth into it what if I change my Mind it's going to be very difficult to back up so to estimate that discount let's talk a little bit about the liquidity so I'm going to reinforce what I said at the start of the class today I mean the standard practice for a liquidity discounts is to knock a fixed number of I call this the bludgeon approach take 20 off every private company evaluation but I think the right practice is to allow it to vary across companies some Companies should have bigger discounts than others healthy

companies over on healthy companies money making over money losing should also depend on when you're trying to do this it's a market in the crisis the market doing well and should also reflect the buyers the buyer long-term buyer or cash constraint buy so now I want that intuition to be acceptable that that discount should vary across companies varying across time barrier across buyers because then We can talk about how to estimate the discount so let's start with that bludgeon discount 25 or 20 or whatever people use randomly those discounts come from two sets of studies

both of which are hopelessly flawed in my view but people keep using them over and over again private company appraisal kind of got its build up from a guy called Shannon Pratt who in the early 1980s wrote the First book unwelling closely of confidence it was a legend in the space the first it's a thousand page book but all the it's a manual on what to do to Value private companies and one of the things of course you have to deal with is the liquidity discount so he set up uh you know set up a

firm in Oregon called Williamette and they started doing research on the liquidity discount and the first sets of studies that backed up the discount were studies Of what are called restricted stock and studies just before IPOs and to see why they give you a sense of what the liquidity discount is let me describe what restricted stock is it's publicly traded companies that issue shares with restrictions on you being able to trade the shares let's take an example let's suppose you have a stock that's trading at ten dollars per share so I come in and offer

you a hundred thousand shares but it said by The way you can't trade for the next two years so you get those shares price right now it's ten would you pay me ten dollars for sure yeah you pay less a number right how much lesser friends right how much you care about liquidity but the advantages I can observe how much of a discount I get so to estimate the liquid discounts I need to observe what the price would be without the discount and the price with the discount with restricted stock I get To absorb this

and there are dozens and dozens of studies of restricted stock and they seem to find a discount of about 30 to 35 percent it's a pretty big discount the second set of studies look at transactions before an IPO so the way these studies are structured is they take all companies that go public and then they look at the two to three months or even six months before the IPO To see how much of a price people charge for selling each other shares so the VC is selling a share to another VC how much of that

they pay relative to the IPO price and there they find discounts for 40 50 percent this is great news for appraisers the discounts is so big you know what what happens if you apply a big discount you get a lower value you say why would that be good what do most private company appraisals For tax purposes Divorce Court you want as lower number as possible so for decades private company appraisers use these studies to back up these discounts they said look private companies you know you should attach a 30 discount we'll talk about the flaws

with it but you can see the basis to these studies now when you look at their restricted stock studies many of the early studies Just looked at the median discount they'd look at 15 or 20 or 50 different restricted stock offerings there aren't that many each year so it's got to be a small sample and they compute the median discount but they stop there that's a 30 25 percent in 1988 Bill silbo used to teach a foundation class he was a legend at Stern did a did a paper it's a paper that I think he

did over a summary he laughed About it and said I never expected to catch on but basically took these restricted stocks offerings and he said rather than give you a meeting I'm going to look at why they vary across companies why are the discounts bigger at some companies and smaller at others and he ended up the paper with the with the regression right so as if you look at the left-hand side of the regression he looked at what the restricted stock price was as a percentage of the market Price so it's one minus the discount

so if the restricted stock price is eight dollars and the stock and the actual the market price before was ten eight divided by 10 is 0.8 so think of the left hand side as one minus the discount and he threw in three variables one is he threw in the level of Revenge his hypothesis was bigger companies should see smaller liquidated Wisconsin smaller companies let me back that up second he looked at you know what how big that Restricted block was his argument was the larger the restricted block is relative to the number of shares outstanding

the bigger the discount has to be so there are million shares outstanding and I'm trying to put a restricted block of a half a million I should see a much bigger discount than if I'm just selling 50 000 shares and he found that that was backed up as well he funded money making company so this Bern is a dummy variable it's a company money Making or money losing he funded money making companies had smaller discounts and money losing companies and finally even through in just to see if there were any any deviations from arms length

transactions whether the person buying the restricted chairs was the customer of the company his argument being you're trying to put restricted shares with a customer maybe they're getting side deals and they're willing to pay a higher price So you ran this regression and I you know it basically became a paper but a few years later I decided to steal Bill silber's regression and use it to kind of come up with the way of coming up with different in liquidated discounts for different companies it's still within the restricted stock study so it's got its limitations but

here's what I did I looked at what the if using that regression what the discount would be For a company as a function of its revenues the larger the revenues the smaller the discount and whether it's a money making or a money losing company so let's say I'm an appraisal firm you come into my office and say hello I want you to value my firm I value your firm and I'm trying to estimate the discount to apply you have 25 million in revenues and you have a money making your money making firm my discard for

you is going to be about 23 percent If you have 25 million revenues and your money losing firm my discount for you is going to be 32 if you're a billion dollar Revenue firm your discount is going to be far lower so in effect I'm not giving everybody the same discount I'm giving smaller discounts to bigger companies and I'm giving smaller discounts to money making companies a way of discriminating across companies but here's the problem with restricted Stock studies that you cannot run away from no matter how much you finesse what did I say has

to happen in a restricted stock offering I've got to offer a big discount right twenty percent thirty percent on the table what kind of healthy companies ever going to do that so if you look at these companies that issue restricted stock it turns out that you have a sampling bias the kinds of Companies that issue restricted stock are small companies and trouble companies because they have no choice the kinds of people who sell their shares before an IPO there's an IPO in two months why do you sell it to share shares at 30 discounts because

you're desperate that's a sampling bias and it took 20 years for the IRS to figure out how to use the sampling bias because with 20 years I know appraisers Had gone to court and said look there's a 35 discount restricted stock study finally after 20 years the IRS actually hired somebody who knew enough statistics to take a look at these restricted stock studies and separate out how much of the 35 discount you were seeing came from the sampling bus there's actually statistical ways of doing this and at the end of the study concluded that about

20 to 25 of the 35 percent Came from having a bad sample only about 10 to 15 percent was the liquidity discount there's a huge moment in private company appraisal because now when appraisers went in front of the court and said we're going to use a 35 discount you actually got pushback from judges saying but 20 of that is a sampling bias why are you using such a big discount so no matter how you slice it there's only so much you can do with restricted Stock studies or IPO studies that too much there's too much

sampling bias I'm not that interested in illiquated discounts it's not I don't work with private companies that much but I've struggled with is there a better way to estimate a liquidity scotch and I think there is and to see what it is remember what I said about buyers remorse to the public company I said there isn't a liquidity discount right it's called a bid ask Spread he said how big can it be for an apple it's tiny 0.1 percent the beta spread divided by the price but if you decided to do this with a small

NASDAQ stock lightly traded you know how much so it's a two dollar stock the bid ask spread could be 50 cents in other words if you buy the stock it'll cost you two dollars one second later you try to sell the stock you're gonna make back a dollar fifty that's a 50 Cent spread on a two dollar Stock that's like having a 25 liquidated discount if I'm willing to define the bid ask spread as in the liquid think of how much bigger my sample is every publicly listed stock has a bid ask spread in the

stock price I can compute that spread for every single store a sample size is 7500 publicly traded companies and about 15 years ago I decided I wanted to see why the spread as a person of price varied across companies The very fact that I have done it since shows you how painful it was that first time I said never again am I coming here but if you're a private company appraiser you might want to go there right I don't care that much but if you cared you could go and look at this so I have

7 500 companies in my spreadsheet I have the spread as a percentage of the stock price for every single company I did what Bill Silva did with his small restricted stock study I tried to figure Out why the spread was higher for some companies and low for others and here were the variables that I threw to my regression I threw it how much the company had in revenues higher Revenue companies had much smaller bidas spreads than lower Revenue companies size the size of the company matter I threw in how much whether the company was money

making or money losing turned out that money making companies have much lower bid aspects and money Losing companies I threw in how much cash the company had as a percentage firm had why because companies with a lot of cash are already liquid they don't need a liquidity discount assume a company is 90 cash why would you have a discounted Company by 20 or 30 percent had much smaller spreads and companies with very little cash and I did throw in a trading variable and not surprisingly companies which have high trading volume have much Smaller bid aspects

in companies that don't trade as much you see what's this Got to Do With Private companies these are public companies are explaining differences differences in bid ask spreads across public companies take a look at this regression it could I get these numbers for my restaurant have the revenues right 1.2 million I can plug it in there is it a money making restaurant Yeah sure it's money making but I put in one I can look at its balance sheet I can get cash as a percent of value and how often does this restaurant trade zero I'm

just going to put in a trading volume of zero that's basically what I did I took my bid ask spread regression plugged in the values for the restaurant in here and I got a predicted bid ask spread for the restaurant 12.88 what does it even mean I'm extending the concept of bid aspects Into the private business space and that now becomes my estimate of the liquidity discount given how public markets are being priced it doesn't have sampling bias it's a huge sample of course I can I like to keep redoing it this is a 15

year old regression so it's it's aged but if you made if this was at the center of your practice you could update this every year the data is there it's easy to do and you'd have an Updated way of estimating what the illicited discount is at any point in time and you can vary it across companies based on the characteristics to show you how different these numbers are going to be than the traditional approaches come out of the restricted stock studies if I do the bludgeon approach where I just take 25 off as opposed to

the refined bludgeon approach where I use the silver regression to kind of adjust it I get 25 27 28 is my discount if I use the bid ask spread approach you you get a much much smaller it might be a much more reasonable discontent value so that 12.88 is what I'm going to use as my liquidated discount which means that my 521 000 that I estimated the value of equity you take 12.88 off gives me a value of 454 000. it took a long journey to get there but in a buyer to buy a private

buyer to Private seller transaction this restaurant is worth about 454 000. you could see why I already private to private transactions are so massive first you can't use baits you got to adjust for the lack of diversification you got to come up with this liquidity discount after you're done to reduce value and every dark force and valuation is working against you as you go along because you have so many things that you Feel uncomfortable about so that's private deprived any questions on private to private transactions so doctors selling his practice to another doctor you run

into all of these issues yeah yes right the r squared is about 35 it was not I mean I could have made it better I stopped after four variables because I just got tired now because the sample Size was 7 500 I could have had seven or eight variables the only thing to remember is you put those variables in they've got to be variables you can get for private companies as well so you don't want to bring in any market-based variables like a dividend yield wouldn't work because you don't have a market price so you

can use any kind of book value based number anything that comes off income statements and balance sheets and if you wanted a Higher r squared you could get there because spreads are pretty explainable and the other Advantage is if you do this on an updated basis they would reflect the marketer and write right now if you're in a crisis this spreads for all companies go up it'll show up in The Intercept so it's a kind of a dynamic constantly adjusted approach where you can get spreads that reflect the time you're in so that's private to

private let's go to The other end of the spectrum they're a private business and you're thinking of selling yourself and there's a public buyer interest so you play the role of a public buyer now public buyer in what sense you're a public company interested in buying my private business first let's go back to the beta you know remember the private to private I adjust the market bait into the total beta if you're a public buyer which Pages should you go with you're a company but you're investing other people's money right your investors in your company

are they Diversified yeah public to private to public I go back to a market beta because I don't have to worry about this diversification issue so instead of using the 2.36 beta I'm going to go back to the 1.18 beta second on the liquidity discount issue you're a public company You're buying this illiquid private company what happens after it becomes part of your company where people can still trade your shares liquidity comes from people having to trade their shares a public company does not have to Discount value for a liquidity because its investors can get

liquidity by buying and selling shares they're not to buy and sell assets so the market beta is going to go back To a total beta I'm sorry total weight is going to go back to Market beta the liquidity discount will disappear so we need to make the beta adjustment you can already see the drop off in my costly Capital so instead of 13.25 I'm going to go with the public company costed capital of 8.76 percent and my value which is 454 000 will now go to 1483. so notice the liquid discount is gone I'm using

a market beta this is very much like every valuation we've done so far In this class so if you have a private company being sold to a public company you can pull up the template you had for valuing public companies and get away with it so you have two values here right for this company as a for this restaurant 453 000 to a private buyer but 1.483 billion a billion to a 453 000 and 1.483 million to a public part so let's say I'm the public buyer and You're the restaurant so you have two numbers

ready for it four fifty three three thousand one thousand four eighty three which one are you going to start your negotiation with let's see if you're you know whether I'm going to get an easy buyer so you're selling your company you have bought these numbers you've computed both which one are you going to start you're going to start at the 1483 and You're going to tell me the story right which I'm a public company I should think about Market beta liquidity doesn't matter how am I what am I going to counter you with which is

I don't care what I look like you're a private company and your next best alternative is a another private buyer so I'm going to start at 453 000. and if I'm the only game in town I'm the only public buyer and everybody else is a private buyer guess who's going to end Up winning this game I'm going to end up getting it for close to 453 000. but if you can get a second public buyer interested in you then we might start bidding against each other and push the value up to 1483 million next week

we're going to just now a week after next I'm going to talk about acquisitions and have a very cynical view that most Acquisitions destroy value at company so when companies try to grow through Acquisition this but there's a there's a big chunk of the process that's going to make it more likely that you will lose value than increase value but I'm going to point to one of the few cases where doing Acquisitions can be value created it's when a public company buys private businesses either to create a roll-up business you're not a roller businesses you

basically buy a bunch of private companies you roll them up into a public company Blockbuster now of course it's gone built itself up as a company by buying small video rental stores around the country bundling them up and becoming a public company Browning fares which is a garbage disposal Company went around the country buying small privately owned garbage disposal companies and but you see why there's a potential for Value creation because what do I do as a public company then when I when I I I offer you up a Premium over the 453 000. you

feel you're winning right because your next best offer is 450. I offer you 550. you think you're you know you walk away from the table feeling good but I walk away from the table feeling good as well because I paid you 550 000 for something that's worth 1.48 million I'm not ripping you off because your next best alternative would be in a private transaction but you can see how this process plays out where if you're Looking for the best potential buyer that best potential buyer for you as an owner of a private business is often

going to be a publicly traded company so again let me emphasize it's not that publicly traded companies are Diversified the investors these companies are Diversified so they don't have to worry about total beta it's not that a liquidity doesn't matter but a liquidity doesn't matter to them because their investors can buy and say yes they Get the liquidity a different way and that's where the increase in value is coming from so I've looked at two extremes here right I've got a private business that's completely undiversified our private buyer is completely undervised by our public company

that's completely Diversified you see where a private Equity Fund Falls between these two spectrums a private Equity Fund is never Completely Diversified they have a sector Focus or Regional Focus so you're partially Diversified so I'll take an example let's say you have a software business you sell it to another individual is completely undiversified you compute the correlation of your company with the market and you come up with like 0.2 so it gives you a high total beta in contrast you take that same software business and you sell it to a software BC who is invested

in 25 software companies so here's my question one software company correlation is point two you take a portfolio of 25 software companies and you look at the correlation with the market is it going to be higher than 0.2 lower than 0.2 what's going to happen when I create a portfolio of software companies it's going to get higher because some of the risk in the software companies very Company specific risk so when I create a portfolio software companies the correlation I'm going to get my 3.4 or 0.5 you see what's going to happen the venture capitalist

is now going to have a lower beta than the individual buyer and the vet and the Venture Capital beta will be lower than uh will be higher than the market beta that is offered by the so you can see this process where you start off with a completely undiversified buyer then you get Partially Diversified buyers and it ends with fully Diversified buyers either because you go public or you get acquired by a public company so it's a process that plays out almost all of the time there are a few private companies that stay on as

private right I remember they they used to have this auction at Stern I don't know whether they still have it but if they have it I've kind of withdrawn from it but they always come to professors and say can You offer something we can sell what am I going to offer other than I'll value a company so I put that into the bed and usually people are better a couple of hundred dollars or 300 they get a business valued they walk away happy I walk away not unhappy so we're we're both okay so one one

auction it ends up that this particular thing goes for a couple of thousand I said why would somebody pay a couple of thousand dollars or just have a company back So I you know I wait and this MBA comes in he's a first year MBA and he's got this big stack of financials with him and he says he says that your company's Financial he says yes and what does the company do he says it makes rump so where are you from it's in Miami you know the company you wanted me to value US Bacardi still

a private leader you're saying why is it privately owned you drink enough Of your product after a while you forget about diversifiable risk non-diversifiable risk total risk I mean they stayed private for 100 or no 150 years it's actually a fun company to value because I mean the corporate governance issues obviously because you had multiple measures like the third or the fourth generation family members all over the place it's obviously a niche product it's got A brand name so that was a case where a private company stayed private notwithstanding the Expressions most private companies so

buckle at some point and either become part of public companies or go public themselves so I want to be make sure everybody gets it private to private use total betas put in a liquidated discount you're going to get a low value private to public use Market balance there's no Liquidated discount it looks very much like a public company valuation private to venture capital or private Equity Fund you're somewhere in the middle you're not your betas are not as high as they were with the private buyer then they're not as low as they will be with

a public buyer but effectively it captures that transition from being a privately owned company to a publicly traded company so let's look at the third scenario Private company evaluation as a lead-in to an initial public offer so now you're valuing the company not because you want to sell to a private buyer or a public buyer because you want to go public so I want to talk about the issues that come up when you value companies ahead of ips is everybody familiar about the process of IPOs a company wants to go public what's the first thing

they need to do they need to file a prospectus with the SEC and around the world there are Variations same thing but you file a prospect what's a prospect is it looks like a 10K for a private company right so it has all of the information that you have in a 10K so one of the nice things about valuing private companies ahead of an IPO is you're now looking at financials that covered by gaap and IFRS so if you have to capitalize leases you've got to do it in the Prospectors as well they'll give you

the history of the company So to start with you're looking at num at data very similar to what you to Value public on but there are issues that are specific to private companies that I want to talk about in the context of an IPO evaluation is a valuation I did of Twitter ahead of their IPO in 2013. usually when companies file their Prospectors if the company I'm interested in I value the company right after the prospect is is Fought I did this with Alibaba I did it with Twitter I do it right after the prospect

is his filed because there's no bias in the process no market price out there there's no banking price out there I have a clean slate I can come up with the number it's kind of on you know unsettling because you have nothing to compare it to but I came up with the value of about 17 per share for the company and if you look at the valuation it Looks very similar to a public company evaluation it's got reinvestment rates and cash flows basically it's a three-step approach Revenue growth margin sales to Capital so you can

take that fcff ginzoo plug in the numbers for any Prospectors you can you can come up with evaluation of the company but there are a couple of twists with IPOs that you have to build into the valuation so if you want to use my spreadsheet Value in IPO here's the first thing you have to think about one is when you go public on the offering day you issue shares to investors and you get cash in return right you have to tell me what you plan to do with the cash you see what do you mean

what do you mean what are the different choices a company has when it comes to cash raised in an offering what can it do Yep one is you get set it aside for future reinvestment obviously you don't reinvest the day after but after the IP you can put into your cash balance and use it to cover those negative free cash flows to equity you had that you estimated are now going to be covered with that cashback so it increases your cash balance okay so that's one choice raise Capital put into cash balance use it a

couple of future reinvestments what Else can it do you know what Spotify did in their IPO they issued shares they got money and they let existing owners cash out so Sony was an investor in Spotify Sony wanted not to be an invest in the public company so they let someone so owners cash out so cash comes in leaves almost instantaneously so second thing you could do is let existing owners cash out the third thing you can do is use the cash to pay it on Venture debt or debt You might have taken on is Bridge

financing to get it off the books you need to tell me what you plan to do with the proceeds in evaluation and every Prospect is there will be a section on what a company plans to do with the proceed so pick up a prospectus of a high profile company read through the Prospectors get to that section because you need that section so we're going to talk about what to do in the case of Twitter the IPO proceeds Were a billion dollars you will notice that it gets added on to the value why because the day

after the IPO your cash balance is going to increase by a billion and Twitter told me that they were going to keep the proceeds in the company everything else about this valuation I've kind of done pretty much what I've done with the public company but let's talk about the issues that our IPO specific Two of these issues are valuation specific one is and I talked about this already the proceeds what do you plan to do with the proceeds the other is the way private companies are built up often requires them to go to venture capitalists

over and over again Twitter had seven BC rounds before it went public you think so what each time you have a VC round you raise Capital prevention Capital you often create a new class of shares Twitter at seven classes of convertible preferred chats reflecting their seven rounds the pain in the neck right and what am I going to do with seven seven class of shares they're also because they were a young company used restricted stock and options to reward their employees so by the time they went public they already had built up this backlog of

trade things that could drain your Equity back that's going to be true in any company But without with young companies going public it can be a particularly problematic issue that's the valuation issues they're also pricing issues which means that in a typical IPO here's how it works you want to go public what's the first thing you do you hire a banker so you find one and what does a banker do for you at least what does a banker claim you will do for you or she will do For you they'll first help you write the

Prospectors so they have the infrastructure for doing that they'll help they'll tell you they will value your company when in fact they will price your company but that's okay we'll let them use the word value what else do I custom for IPOs for young companies planning to go public they will do a road show which means the bankers will wear expensive suits go Around the country do nice looking charts multiple font sizes different colors but along the way they might give you some information about the company what else they will basically get on the old

days get on the phone and get onto clients or portfolio managers look we're going public with Twitter you know would you be interested and they'll frame it in a way if this is your last chance to get into this deal at the ground floor You've heard it right you've got an electronic store you're basically you're getting the banking pitch in a lower form but it's the same kind of thing you know and then they give you one final it looks out they actually guarantee the price they will take you public at that's amazing right what

about a realtor and I said I can guarantee the price I can sell you sell your house at you know why you should Pay nothing for that guarantee what did I forget to tell you I forget I forgot to tell you the price can I sell your price I guarantee I can sell your house at 20 below them anybody can do that and that's what Bankers do they they offer an underwriting guarantee but the guaranteed price is off in 15 or 20 below what do you what they think the price should be and there's one

final thing they do Which is after the company goes public at least in theory they offer what's called aftermarket support which means if somebody's trying to sell your shares they'll often come in and buy the shares to offer support to a limited except they don't have unlimited resources so those are the services that Bankers claim to offer and in return for that what do they get six to eight percent of the proceeds so if you raise 100 million at six to eight Million dollars that is the process companies have used for the last century the

process is getting frayed we'll talk about why but that is the process we use but a key part of that process is an underwriting guarantee so let's talk about the valuation issues first then we'll come back to the pricing issues as I said the three things you can do with the cash one is you can keep the cash the company as part of your cash balance And use it to cover Future Care packs the second is you can let owners cash out and the third is you can use the cash to pay down debt if

you decide to take the cash out of the company let owners cash out I can completely ignore the cash you see why because I raised cash to one window it goes out through the other window it doesn't change my values of company so in Spotify the proceeds from the IPR net don't even show up in your valuation They're just gone if you keep the cash on the balance sheet there's going to be an immediate augmentation of your value by the amount of cash you've raised because that's cash now that increases your cash balance and you

use the cash to pay down debt how does it show up in your evaluation what happens when you pay down debt your debt ratio goes down your cost of capital is different so it might affect Your discount rate it might affect your failure rate remember we talked about failure rates and how they can affect the value of young companies might affect your failure rate so what you do with the proceeds depends very much on what the company plans to use for projects second stop in the case of Twitter they're actually in their prospectus told me

that they're going to use the billion dollars in Proceeds to hold this cash it is required as part of the prospectus to specify what you plan to do with the proceeds and Twitter's you know Twitter says judgment was they would keep the cash balance second cleanup right you all these different claims I can't value the equity in a company when there's seven different classes of convertible preferred stock to deal with luckily for you and companies go public one of the Things that happens is all these different classes of stock will get converted to Common shares

in the case of Twitter what made my life easier was all seven classes got converted into common shares they still had restricted shares that I have to deal with and options outstanding but they did clean up at the time of the prospects and that too should be specified in the Prospectors they'll tell you how many shares there will be outstanding after All of these convertible preferred chance get converted into common shares but in the case of Twitter there's there's two things that I think they left us Loose Ends which I tend to find in most

Prospectors one is there are tons and tons of restricted stock that for whatever reason they excluded from their share company they're actually pretty open they'd say there are 337 million shares outstanding the company oh by the way we have excluded the 73 Million restricted shares why it's because you feel like it sometimes it's because they're non-vested you know what the keyword best studio means right you've got to stay on long enough to get those shares we're going to ignore them because they're not invested that doesn't mean they'll never get busted here's my advice to you

don't take the share count that you see in the Prospectors that the company gives you Look through the exclude shares because many of those restricted I took all of the restrictions and add them on to the share con so my share card is actually very different from the investment banking share con that went out that day because I counted the restricted shares they also had 44 million options what do we do with options publicly traded companies what's the right way to deal with options We value them as options and that's exactly what I did here

with one catch when I valued options publicly traded companies I use the market price to Value the option because I had one here I don't have a market price I use the intrinsic value per share I estimated the 17 to Value the options that value for the options was 805 million I'm going to subtract that from the value of equity in fact you saw that in the big picture to get to the value of equity in The company so I'm doing exactly the same thing I did with public companies just more work with private companies

because you don't have a market price and finally the investment banking guarantee as I said it sounds too good to be true right somebody guarantees a price but the problem is because the guarantee it's Investment Banking guaranteed affects how Bankers said offering prices on ships so let's play a game Let's Suppose your price shares in the company come up with twenty dollars which let's say you've done it reasonably well you feel pretty comfortable that that's the right price twenty dollars per ship you're going to offer me a guarantee on that price right because you're offering

a guarantee you want to Discount the price you give me or add a premium to that price what's going to make your life easier if you set the price at zero think how Much easier life would be you can't do that but you're going to try to discount it by how much it's amazing if you're going to work for an investment Bank in the IPO section if you look at manuals it's actually written right there in the manual value the company now price the company take 15 off it's like a discount that applies all the

time and it's okay so You price the company and how do you price the company we talked about the kabuki dance you can go through of acting like you're doing a DCF but in pricing a company you look at a metric use a multiple you come up with the pricing in fact I showed you my Twitter pricing was based on how many users they had and applying a hundred dollars per user Where'd I get the hundred dollars per user by looking at publicly traded companies in the space and looking at What the market was paying

per user it's my pricing of the company and then once I get the pricing I'm going to Discount that price but that discount creates a little bit of a potential people look at and say the original papers and IPOs actually called it the IPO puzzle and explain a minute why they called the puzzle and here's what they found so you have an offering price and on the opening day of trading you have a Starting price for the stock right so the offering price is set at thirty dollars Market opens for trading doesn't open at 30

it opens at 34 35 36 on the offering day on average the IPO stock price increases by about 15 percent sounds like a way to make money right so tell me how you how you would exploit this to make money start a mutual fund for me that takes this crap and say I'm going to make money on this guy what are You going to do this I mean shorted when after it's gone public because that would require the price to drop yeah the price is jumping you shorted at you can't first you can't short at

the offering price it's not trade it's you'll have to wait till it's traded now so maybe there's a shorting strategy down the road but I want a strategy for the opening day what might you do Yeah starting in a mutual fund here's what you're going to do you're going to buy a thousand shares in every IPO that comes up in the next year you should make money hand over fish right and mutual funds have tried this and they don't make money so tell me what the slip is between the cup and the lip that leads

these the this 15 that you see on paper to kind of dissipate so let's play this through you have 100 IPOs coming up you write to Each banker and ask for a thousand shares in each RPO are you going to get a thousand shares in every IPO yeah because Bankers have to ration based on what demand and supply so if you have an offering which is over subscribed by 500 percent this has nothing to do with playing favorites you're going to get only one in five shares that you asked for because there are five times

more money so you're gonna get 200 shares in that Company if a subscribe if an offering is under subscribed you're going to get all thousand shares to see what's going to happen right at the end when you look at your portfolio you're going to have 200 shares in all the most underpriced companies and a thousand shares in the most overpriced conference so when you look at the Returns on your phone he said what happened what happened was you didn't get an equally Weighted portfolio yeah you got a portfolio that's overweighted with stocks were overpriced and

underweighted it so if you're planning to make money on IPOs you can't just in buy every IPO if you have a way of discriminating across IPOs to figure out which ones are underpriced and which ones are overpriced maybe but that'll require actually pricing the IPO to see which ones are most likely to see this picture so making money on IPOs is not easy Because of this fact that you don't get all of the shares you want in this companies you want you want to get them in but you get all the shares you want the

companies you don't want to get them in and that's not a good end game to be as an investor but there's another aspect of this discount that troubles people this is where the puzzle comes in you're the founder of a company you've spent the last five years Working 20 hours a day building up this company along the way you've accumulated Venture capitalism took a lot of risk has this company built up right you decide to go public and let's say your fair price is twenty dollars and I did put a 15 discount on that price

when I set the offering price out of your pockets and the question that people often ask is why do founders go along with this Why do they allow Bankers to knock 15 off so let's say you have a 10 billion dollar company 15 of 10 billion is 1.5 billion right that you leave on the table or is it that's if you show all of the shares at the offering but in a typical offering you offer only about 10 of the shares but still 15 of that but you might be okay with it why because the

day after the offering what do you see as a Wall Street Journal Article on your company stock price jump on offering day what do you hope will happen other people read this story and then what would they do what human beings have done through the history of investing which is they will now try to buy the stock you know what a lost leader in department stores lost leaders are those things they put in the table to suck you further and further into the store Yeah socks at 20 cents you don't need socks but 20 cents

you know might as well buy them just in case they're not even your size Etc cheap so lastly do you basically selling stuff for below cost because you want me to get to the Ralph Lauren section which is near the fifth table and the moment of weakness by a 200 sweater that I don't need right this is like a lost leader you're willing to accept the discard because you hope it Will draw more people into the stock and push up the stock price so if you're wondering why this existing processes survive the way it has

it's because nobody in this process actually has that many problems with the process as long as you discount about 15 or 20 percent if it stock price doubles in the offering day clearly you're going to be much more upset as a Founder but for a long time people got along with this process But in the last few years people have started questing the process let's go through the services Bankers claim to offer okay first is they help you write the prospectus chat GPT could do it for you have you ever read prospectuses they come out

of a template it's almost like the same guy writes every Prospectors they use the same language so there's not that's not rocket science I could you know you don't need a banker to do It they price your company really this is what they do and the price doubles on the first day that's not great pricing I probably have asked my doorman to price the stock and it'll be better pricing so that's not very good or they sell your company they you know get investors to buy a company that they don't recognize because Goldman Sachs is

battery that might work for a company nobody's heard of but in the day Facebook went public I'll wager More people had heard of Facebook than of Morgan Stanley the lead investment banker I don't need Morgan Stanley to tell the world who I am everybody already knows who I am you see what I'm saying all those services that Bankers used to offer as special services have essentially become less and less valuable and I'm paying six to eight percent so a few years ago bill Gurley said why didn't we cut the banker out of the Equation it

struck there in the hearts of Bankers this is these are not words they want here cut the bank what do you mean cut the banker out of the process he said why don't you just go directly to the market it's called a direct listing the direct listing you know what to do you specify the opening day we're going to start trading on May 15th there's no offering price you're saying what what are we going to do how do markets at prices demand and Supply to Open up there's demand there's Supply there's there's no discount on

the price it's much fairer because nobody's getting the sh the shares at a special price it's called a direct list the only problem with direct listings is right now the the status quo doesn't like it the SEC believe that direct listings are potentially unfair to investors because they have this feeling that investors will be taken advantage of by Fly by Night companies that go Public they feel they actually believe that Bankers are your defense against getting scammed I don't know what the SEC is drinking but I don't see Bankers as my defense so their View

and the way they constrain direct listings in a direct listing today you're not allowed to keep the cash you raise in a direct listing that's why Spotify actually I had to let owners cash out because they made a direct listing it wasn't a traditional IPO so the direct listings have not taken off the way they could Act without those constraints and in the last three years there has been a third way to go public right go to spax what are you doing a spec do you want to tell me describe what is what you don't

expect so you start a spec so first you have to be a high profiler or low profile investor to be a great Question right high profile so what do you do you raise money from people to do a public offering of whom you don't specify I said trust me I'll find a company for you so you trust him you trust them why because they have a track record they know technology they find a company for you and they negotiate and a price for you trust me I'll negotiate a good price for You and for all

of this trust what do you have to pay so much 20 specs take twenty percent of the money so they raise 100 million 20 million goes into this is a great now you see why it started what 16 different specs you take the 20 off and take the remaining 80 million with that 20 cut it's never going to take off but the process is getting shaken up and I don't know how it'll evolve but I Think we're going to see change in the IPO process because the existing way of going public is not working and

the new ways are not good enough yet to make the switch so on Monday please bring your last package so I'll send you the link so you can download it because we're going to talk about option pricing on Mondays if you want to look at your option pricing notes from foundations that's good but I assume not that we started a very quick review and then Going to real options yes