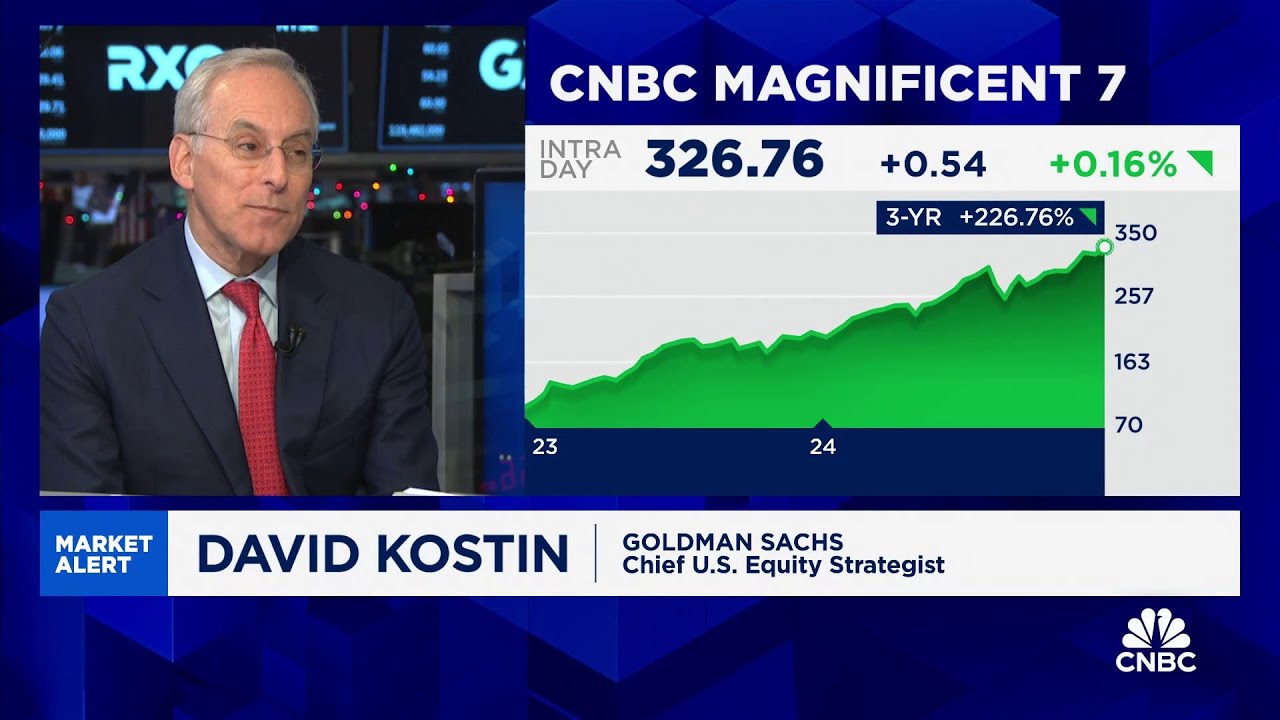

We have been talking so much about these record highs we've been experiencing. But within those record highs, there's a tremendous amount of stock market concentration here. There's few stocks that have benefited so disproportionately.

How do you invest through that? Well, first, it's a lot easier to be a quant at these times. We do run some traditional portfolios, but a lot of what we do are long and short, and it's very common for us to be long.

About 750 stocks around the world and short about 750 balanced by industry. So we do the the the courageous thing and run away from this problem. We've had we've had very good years with the Mag seven soaring, even though value strategies are part of what we're doing.

The opposite hadn't happened in a while. The opposite could happen. So.

Concentration is a problem for a typical active manager and for us in some places when you're only allowed to go long against the benchmark because a lot of your information, if you're a good active manager, is about what not to own and when some things are so concentrated and big, it shrinks the size of everything else and makes that information less relevant. When you're long, short, or even in a traditional portfolio that allows you to do a little bit of shorting. If that really goes away and you don't have to think a lot about the Mag seven, you just have to think about what you like and don't like.

So I mainly run away from this problem. You know, speaking of running away from the problem, you have one fund in particular. We're taking a look out.

My colleague Justine Ali pointed this out. You have an equity market neutral fund that is up about 23% this year. You're beating the market.

I'll take your word for it. And that fund, I'm interested in it because traditional value factors, generic ones out there in the market have not performed that well. What do you do differently with value?

Where I have literally a piece on our website saying we are not all about value, except occasionally when we are when the world goes into absolute bubble mode, anyone who cares about price is affected by it, but value is only a component of what we do on some particularly strong things over the last few years have been and this year have been quality strategies, profitable companies that are stable, low volatility, low beta, some of the more proprietary things that people at my firm will tell me if I try to talk to you about, but more EML an alternative data kind of thing. So we've we've we have had you quoted it. They get mad at me if I quoted, but we've have had a very strong year.

Our versions of value when you go global and you don't take big industry bets by about flat on the year, it's not been a terrible year. You get very distorted. The value indices are cap weighted and we all focus on the US, so they really are mag seven against everything else.

Real world, particularly quants, but even non quants are often much more subtle in what they're in, what they're doing. So not a terrible year for value as we define it, but that's not been the driver, it's been the other stuff that's made it kind of fun this year. And so I don't want to instill a bunch of time.

I no, no, I just mean the year is not over. I hate I hate year to date until December 31st, 4:00. You really want the family to say how you do?

Yeah, I'm a superstitious quant. Okay. There you go.

I will say you can say anything on TV1, so feel free to talk about your returns. Single stocks. And I do want to get your thoughts on size, because the phenomenon that we've been discussing is the fact that you don't have a lot of small cap IPOs anymore, that companies are waiting in the private markets until they're a little bit bigger.

So maybe they bypass the small and mid-cap index. And that's spurred the idea that maybe the small cap premium has disappeared as a factor. I would love to hear your thoughts.

Yeah, well, this one again, I'm going to I'm going to turn the question around on you like a quant. Okay. We don't think there's ever been a small cap premium.

What does that mean? Well, certainly sometimes small caps, wind, but a premium means they win on average that on average you make you make extra money. The early tests to this were in the early 1980s when the so-called small firm effect was discovered.

I arrived at the University of Chicago about five years after this was. But it was there. It was being done, and it showed that after adjusting for their betas.

Another thing quants do and non quants, if you're making extra money just because you're a 1. 5 beta and markets go up, you'll make more money than a one beta and small cap does tend to be more sensitive to the to the market. The early tests had to estimate the listing returns.

The database's just say delisted. So you have to guess at how much you would have recovered from that. And they overestimated how much you recover.

And they didn't adjust enough for the fact that the traditional statistical method, you know, I love statistics, but they grossly underestimate the the market sensitivities, the betas, the volatilities of things that don't trade every day, and a lot of small caps on trade enough when you adjust for both those things. There's not been historical small premium. Now today it's interesting I do think this effect of thing companies waiting longer it's probably more we don't trade on this it's just an opinion.

But the small world is probably a more distressed value world even than it normally interest is. So I don't think that necessarily I mean, if you believe in the premium, I don't think it necessarily means it's gone. It could just be suffering along with value strategies in in general.

I know a fair amount of people who look at this think the spread between cheap and expensive in small is even wider than it is in large cap, where it is wide versus history. So it could be a sea change or it could be bad things that have happened that lead to good things. I have a sea change question, please.

So I pay. Like half of my income to the US government in taxes. Here in the capitalist free market.

Cliff wants to help you. The city of New York? No, no.

But I lived for like ten years in Germany, right? Socialist Germany, where I paid less in taxes than I do here. And I got free health care and child care there.

So when I see a story about reducing my tax liability, I'm reading it. Justine Lee wrote a great story about you guys, quote, Giant AQR cuts Income Tax Bills for Wealthy clients. Yeah, I hated the title, but.

Okay, well, how can I get in on this? Like, what am I missing that I'm, you know, losing half of the money I earn and not getting anything back for it? I'm well, getting even bigger.

Picture the difference in Germany, in the US, you raise a fair general point. People don't realize that at least when it comes to income tax, the US tax code is more far more progressive than a lot of other countries that are thought of as more progressive. So you're not imagining it.

You are paying a very high rate for us. It probably started about ten years ago. We always co-invest with our with our with our clients who are almost all tax nontaxable institutions, pension funds, endowments, foundations, sovereign wealth funds.

And we knew this was kind of stupid in some ways. We believe in our strategies, but you shouldn't invest the same for a taxable investor as a non taxable investor. It always shocks me when people are like, You do that for them.

I'm like, Yeah, you remember we're fiduciaries. We have to do what's best for the client. And classic example is if there's a stock you loved a year ago, you made a lot of money on its 11 and a half months later and your model or your process or even your active managers, if you're not a quant, want to want to sell it.

If you're a tax free institution, you just sell it. If you're an individual, you're crazy to not to wait two weeks, right? I don't know anything about the next two weeks.

I wish I did. I'd be I B Jane ST You just talked about them. If I knew if I knew about the next two weeks.

So you wait two weeks and they're going to do they designed some silly things in the tax code like the difference in selling something after three years or 64 days at a gain and during 66 days is dramatically different in your tax bill. So we don't do a darn thing different in terms of gross alpha. We are basically all you have to do except for make holding in another two weeks or something.

We are still running mostly about making money before taxes, right? We're running our standard process. But the major things which turn out to matter a lot if you do them systematically, are if we're running your money after tax and you're and you're an institution and we're running your money pre-tax and we decide we hate a stock we used to love, we'll sell it for you and we'll wait 15 days to to sell it for you.

That doesn't sound so powerful. But when you're long short and you have 750 longs, 750 shorts, and when you're us, which we got kind of lucky on this, our average holding period is just under a year anyway, right? So we are making a ton of decisions naturally, part of the pre-tax alpha process around that key decision point.

If you're a high frequency trader, you can't do very much here. You're realizing it all every day, right? If you're Warren Buffett, you already have a good tax plan.

It's it's eventually to hopefully not for a long time, but to to die and to pass it on to your heirs or charity. Tax free. One year is a beautiful time because the tax code is kind of silly about it.

The tax code I would write is not necessarily the tax code that I will as a fiduciary, manage my clients to. I want to talk about the after tax return a little bit more because, of course, there's always been a focus on after tax returns, but it feels like there's more and more products that are coming to market that are focused on the after tax return. I think about what's going on in the ETF space where I live and there's an attempt here to make exchange funds in the ETF wrapper and to get a little dystopian.

I wonder if that's like the future of asset management after tax return products and leverage single stock ETFs. I mean, I have strong opinions on what's the best way to do this exchange funds. I watched some of them at Goldman Sachs 30 years ago.

They always struck me, Yeah, you know, we like to do really natural things, like we're doing our process anyway, but we're going to wait two and a half weeks to do this. You know, those always struck me as like an alchemy kind of, Yeah, I'm not super comfortable with that kind of solution. But what you said in general, a larger focus on after tax.

I have been waiting for this for my entire career as a as a as a little kid in this business. This is not genius. I think a lot of people did it.

I was like, why does everyone why do taxable people focus on pre-tax returns? I mean, they've been studies that look at mutual funds and say the money flows to the largest pretax return, which is often. For the obvious canonical investor, not the best post-tax return.

Rob Arnott, who's been a frenemy of mine for a long time, we've written articles back and forth, but he wrote a brilliant piece on this and I think in the eighties it might be saying, but nobody cared for a long, long time. So I think it's a positive development, I think. But you have to have pre-tax alpha.

You can't do things that are just about taxes, but once you're doing it, you should make more money different for your taxable investors. And that is shockingly new. It should have been a long time ago.

Let's switch back to something you were talking about a little earlier. We were talking about places. Let's talk about it in terms of places to find out what because you would want there.

Where outside of the stock market are you finding it? You've made a lot of money in recent years on commodities. A lot of people have been talking about bonds.

You're weeks away from putting around new capital markets assumptions. How do you think about diversification? What's the new 6040?

The new 6040? Still 6040? We I don't know who on earth has ever invested in 6040.

Somehow that became you have to do 6040, if you like, write a piece like we do on the prospective returns of 5050. The world goes, I can't I can't deal with this. This is 5050.

We do think both stocks and bonds and this will be reflected in our piece that's coming out soon. We do these capital market assumption pieces. They really are client service.

We're interested. We don't trade on them. They're like ten year signals.

I've had a couple of bad years in a row that I can survive. Things that only work over ten year horizons are not very practical and they often give you kind of weird indicators. They'll say things like, We expect this right now.

We expect to make less on the next ten years on 6040, particularly on stocks, than the long term average, because they're expensive. You know how hard it is to make money with the phrase make less. What if you underweight or short them if they go up less than normal at the end of ten years, you tell your client we lost you money, but we lost you less than we would have in the 20th century.

We talk about this and people don't get very excited about that. Having said that, everyone's got to plan their life from individuals to pension funds. How much am I going to make on my assets to cover what I have to cover?

So these numbers are very important if you're going to make less. It's important. But I want to be clear, it's not a trading signal, but cos we think less of the markets.

We think diversification away from 6040, which to be honest, we always believe in. So I'm singing a song I would sing all the time. But we do think it is somewhat more important when markets are probably offering you less trend following strategies.

Long short equity strategies that are truly short. Not not long short because that's just, you know, window dressing is the best advice you would give to somebody who is primarily an equity investor. It's kind of like what David Carson was saying a couple of weeks ago at Goldman Sachs.

If you're standing at these valuations and you're worried about long term returns and you're investing today, how do you play just equities if you're playing just equities? It's in your question, you are stuck with just equities. Then it's about can you add alpha to it?

And we think some of the more publicly known things, buying high quality companies at reasonable price, what Warren Buffett does, we think it's still going to work. Going forward, it doesn't fix the equity risk premium. To fix that, you have to go outside of equities or be willing to short some equity.

So within equities, we still think there's alpha for active managers who have a disciplined, rational process but too cheap. The question, I think to really move the dial on an all equity exposure, you know, why are you all equities? You've lived through one of several, but a golden age for equities and people tend to look at ten years and extrapolate that forever when in real life at that horizon, there's at least some degree.

Again, it's not a daily tradable strategy, but there are at least some degree of mean reversion. So the world on average gets us a little backwards. They get all excited and are comfortable with 100%, whatever it is, 100%.

One thing when that one thing has one. Same thing for us versus non-U. S.

US has crushed the world. Most of that has been the US getting more expensive than the world. The fundamentals have come in somewhat better on the US, but as we measured, that's about 10 to 15% of the US is victory.

85% is people being willing to pay more for those multiples. That's not something you want to extrapolate Fundamental performance. You can argue maybe there's something better in the US, maybe it is not, but just price multiple moves.

Yeah. So I think number the number one thing is to cheat your question and go. You've lived through a tremendous period of reckoning, particularly for a US investor.

I'm not saying dump them, but I'm saying to assume that's going to happen again is a little crazy and doing some other things we do the things we like or whatever you think. Can I add value? That's not just a straight bet on equities.

Rising is always important. You always want to build the best portfolio you can. Is more important now than it normally is.

This is what Oswald Thomson was talking about with Linda and the fact that we're in a pricey market right now. It's about momentum and vibes more than fundamentals. I want to ask about we have a really cool function on the Bloomberg.

We can go and go and you can. We have I now powering a search through companies earnings reports and I ran a search here to see how often people mentioned machine learning and AI itself and obviously you know it's blown up in 2023. And whenever I started thinking about this, at first I thought a lot about you and AQR, because how often do you think about me?

Well, with QAnon, you know, I mean, I love to think about quants and how they can put this kind of thing to use. And I remember a couple of years ago reading a story about how you were hiring all of these, you know, computer science guys from University of Chicago, and how much can you put AI to use and gain an edge over other people who are, I hope, doing the same thing? Sure.

Well, that's that's a separate question. And I do think I'll skip to the end on that. Yeah, I do think the AI world will be far more dynamic than what you might call the quant factor investing world.

You you do a very good version of what Warren Buffett's doing. You'll have bad times. But if you stick with it, I think I think the whole world can know about it and you can still make money from it.

But we don't have to throw away the Benjamin Graham book. Now, a big data alternative data set will be, I think, a more constant arms race where you have to keep reinventing what you do. I'm actually optimistic we can do that, but it will have more of that element.

Air is a really complex topic to even discuss about how a firm like ours is using it. If you guys want to give me a three hour segment and kill your ratings forever in a slump, I know that's hard to do in 3 minutes, but at our firm we're using at least three different ways. One is signal generation, literally, you know, quant signals we've always done that could be done better.

The classic example is using natural language processing to look at at written and verbal information and turn that into Is this good news or bad news? Quants have done this forever. They've done it with word count.

You see the word increasing. You do a plus one. Hmm.

That was very coarse. If the actual sentence was massive, embezzlement is increasing, then plus one was probably not. Not your best call Quanta only have to be right about 53% of the time, so that's okay.

It turns out NLP machine learning is better than our old method at doing that. A second way we're using AI is how to combine our factors, how to wait them. This is a little annoying because you know the old joke or recession is when your your neighbor loses your job or depression is when you lose your job.

AI's coming for me now because I've always been one of the AQR and makes kind of the final call on on weights, on how much you know, I don't do this every day. We're not traders. But what should be the final weights are not all model driven because you can over fit that way.

Air is taking over some of that role. Turns out it's annoyingly better than me. So that's another way.

Finally, just as a productivity tool, which is the most mundane but just a code, AI is making everything faster and probably moving what you talked about that innovation cycle itself. I for a to use I yeah. Is there the other really kind of cool way to think about AI and I probably slowed our firm down by a year or two on this.

I think sometimes the old man's job at the firm is to slow things down when there's new stuff. But forever. We've talked about not overfitting, that a danger of quantitative processes is you see things in the data that were random.

You think you can trade them, but but they weren't real. A. I.

And the way you combat that, by the way, is is to combine data with theory and common sense. I, to be honest, pushes us a little on the spectrum away from some of the traditional things we've talked about. And it was uncomfortable for me.

You are surrounding yourself a little bit more to the machine. If there's limited data, you still need some economic priors. If there's a lot of data, you sometimes don't.

One of my partners, Brian Kelly, has written a paper with a title I love called The Virtue of Complexity, because everyone always talks about the virtue of simplicity. Even I've had to adjust to a world where maybe simplicity isn't always the goal. Complexity can be the goal, you know, over and over and over.

We have one Wall Street executive after another saying, AI is not going to take your job, but you've come here and said, I'd even come in for me in some respects. What does that mean about a job on Wall Street over the next five, ten, 20 years? That's the the operative question is over what time horizon not to get philosophical, but on significantly long enough time horizon.

It's coming after all our jobs. Right. This which is not necessarily a bad thing depending on the transition.

You know, we get to a world of Star Trek where we have a replicator that can make whatever we want. That's not necessarily terrible news. But it could be a lot of upheaval on the way to that.

I think it clearly so far as you are. It is certainly we've we've not shrunk because of. It has made our existing people more productive.

Forecasting five or ten years down the road is, of course, a lot harder. And I'm not sure a crank who lives for diversification is the guy you want doing this. But increasingly you have a job like doing an RFP.

Your client wants questions answered. Right. That's going to get much more air over time.

I doubt even on a ten year horizon, we'll get to a point where no human has to look at it. Right now, we are not. At that point, I would not release something that was pure chat to a client, but but it's all about time horizon.

All this is coming and I'm not the guy to do it, but how society adjusts to it. That's the question. You cannot stop.

Technology and I always laugh when I hear about people like we're going to stop automation. I'm like, Yeah, good luck with that. You can slow it down a little bit and maybe let some other country beat us at it.

But it's coming for all our jobs. My wife went on a quest for our four children, all in their early twenties, right at one point saying what job should they pursue that are most safe from a from AI? And she concluded at the end, you just do what you're interested in.

I can't figure it out. She's pretty smart. Yeah.

Yeah. So, Cliff, we have less than 2 minutes left with you. I want to talk about market mechanics here, and I want to talk about leverage.

Single stock ETFs. I was speaking with your new friend Mike Green from Simplify on Friday, and we were talking about these leveraged MicroStrategy ETFs. His belief is that that's helping to fuel this record premium that MicroStrategy has to Bitcoin itself, not specifically about that product, but you think about the proliferation of these types of products.

What do you think that means for the market structure and the motion of markets? All right. I'm drifting from quant now.

Whenever I give, like, broad opinions about market psychology. Yeah, you should. You should weigh my opinion somewhat less than when I'm talking about AI or diversification, because I'm a little out of my wheelhouse.

But I do think if you look at valuation differences, we're still at a time of extremes. And that's not just the magic seven you could do it with in any industry you want and add them up. We're I wouldn't call it a bubble.

Four years ago, I would have called it a bubble, but we still are in a time of extremes. I think animal spirits are high. I keep hearing that it's, you know, that's I don't know how to judge this exactly, but it's partly quantitative, looking at just the spread between what we think are reasonable and unreasonable priced stocks.

And part of it is qualitative, the part you shouldn't trust me on. But but the part you shouldn't trust me on looks at the rise of, say, aggressively levered ETFs and says nobody needs those. And then you combine it with 24 seven trading, you know, if you're waking up at 2 a.

m. and you need a levered bet on I until then, then you might want to reconsider not just your financial plans but many things in your life. Extremely levered ETFs, if you hold them long enough, are almost that.

I only say almost for legal reasons are almost certainly going to lose their money. The volatility drag is very large if you rebalance them religiously, it depends on the costs that are embedded in them. If you use them for very short term tactical views, they can make some sense.

And then I ask, why do you have very short term tactical views? Because very few of us and certainly including me, certainly in concentrated non quant, not Jane Street, but, you know, two stocks, I don't think I don't think these people have any information on it. So I do think it is a speculative tool, a symptom of some some things that are still pretty extreme in markets.

And this is clearly not investment advice, but I wouldn't use them. And speaking of, by the way, that was investment advice. And speaking of speculation outside of your wheelhouse, my bosses want me to ask this question.

I'm like, he's a client, but how are you investing in Asia? With the backdrop of Trump tariffs, your bosses are asking me a stupid question. I would never insult you guys, but I'm very comfortable.

No, I'm kidding. We're investing like quant. We are relatively actually really close to balanced by country and industry around the world.

We don't that doesn't make us riskless. We have bad periods when the one style is we like reasonable companies at good prices that are starting to turn around, are not being favored. Not going to be a fun time for us, but we have been very good over time at avoiding the big thematic themes, like tariffs are a lot about specific countries and specific industries.

That's where they can play havoc. They can make real winners and losers. But can we use Trump 1.

0 as a blueprint for Trump? 2. 00.

There are a lot of jokes that right themselves here. I think we're in a time it could work out very well. I'm not necessarily a pessimist, but I think we are at a time of elevated, uncertain.

We can measure that. That's not just an opinion. You can look at dispersion and forecasts of earnings, of economic forecasts.

You can look at how bad they're missing. When the numbers come out, up or down. Dispersion is just about the size of the mist.

It's elevated and has a soft sense. Whether you love it or hate it. The Trump wall is going to be very different than the prior world.

So I do think economic uncertainty is larger. I'll give a blatant commercial. I think things like trend following strategy strategies that are what are called positively convex.

So the geek term for they tend to do well in tumult. Yeah, are probably a better time. But mostly when it comes to picking individual stocks.

We run away from your question. We have it wasn't a stupid question. It was just not the right question for a quarter.

Another Trump question for you. We do have less than a minute left here, but do you think that the tax cuts, if achieved, will be a fuel for the market, as certain investors believe they usually are in the short term? I'm.

We do have a You don't need me here to tell you we have a bit of a deficit problem that it doesn't appear that either party wants to take. We could talk about government getting more efficient. We could talk about the doge.

Do they still pronounce it Dodge? So those even in this, the Department of Government Efficiency? I think so.

That's doggy. I'm copying this from Twitter. Someone else said it, but it cracks me up that we have two guys heading the Department of Government Efficiency.

Yes. It's like first thing, fire one guy. Yeah, that's what either of them would do.

And I'm not saying which one I'm not. No, I'm not going there. I'm, I, I do think we are in a world of, of more uncertainty.

I think when it comes to stimulative things, the the budget deficits are going to matter at some point. Many of us would have thought they matter 20 years ago and have been dead wrong. So I'm not going to do the sucker's game of trying to time when that matters, but at what point we consider something stimulative versus, oh my God, we've gone too far is something I would be terrified to trade on.

So I'm not trading on that. But that point does exist, so I won't make any firm forecasts. I just think we're we're in for an interesting ride in one direction or another.

Coming up. Cliff, we thank you so much for joining us here in studio. Of course that is Cliff asked us of AQR capital on the markets on I come in for our jobs sorry I hope I'm so I'm going to be so happy when I'm sitting in that chair that moves around the spaceship with my giant icy, you know, like this.

There is universal basic income or so. Yeah, well, you know, it actually has to come with that. Yeah.

A world of superabundance means people have to be able to participate in that abundance.