Let me describe a couple to you and tell me if this sounds familiar. They're both working professionals. She's in marketing making 62,000 a year.

He's an IT pulling in 71,000. Combined household income $133,000. That puts them in the top 25% of American households.

They should be crushing it. They should be building wealth, maxing out retirement accounts, taking nice vacations, feeling financially secure. Instead, they're stressed.

They're living paycheck to paycheck or close to it. They've got maybe two months of expenses saved up, and that's being generous. When their car needed an unexpected repair last month, they had to put it on a credit card.

They both work full-time, sometimes more than full-time. They're exhausted. They rarely see each other during the week, except for a few tired hours in the evening.

And the craziest part, they've done everything right. They got the degrees. They got the careers.

They got married. Combined their finances. Bought a house in a decent school district.

They did exactly what they were supposed to do. So why does it feel like they're drowning? Why does a household making over six figures feel so financially fragile?

If you've ever looked at your combined income and thought, "We make too much money to feel this broke. " This video is going to make a lot of things click into place. My name is Bobby and I spend way too much time thinking about why two inome households are often worse off than single inome households from 50 years ago.

If you're someone who's working alongside a partner, both of you grinding, and you can't figure out why it still doesn't feel like enough, make sure to hit that subscribe button and give this video a thumbs up if this helps you out. Here's the thing. We've been sold this story that two incomes are better than one.

It seems mathematically obvious, right? If one person making 50,000 can support a family, then two people making 50,000 each should be able to support that same family and have an extra 50,000 left over for savings, investments, and building wealth. That's just basic addition.

Except that's not what happened. What actually happened is one of the biggest financial bait and switches in modern American history, and almost nobody talks about it. The term for this phenomenon is the two income trap and it was coined by Elizabeth Warren.

Yes, that Elizabeth Warren back in 2003 when she was still a Harvard bankruptcy law professor long before she became a senator. She and her daughter Amelia Warren Thiagi wrote an entire book about this after studying over 2,000 families who had filed for bankruptcy. And what they found was genuinely shocking.

Having two incomes didn't make families more financially secure. It made them more vulnerable. It made them more likely to go bankrupt, not less.

Families with two working parents were actually more likely to file for bankruptcy than single inome families. Let that sink in. Working twice as hard, bringing home two paychecks, doing everything the modern economy told you to do, and you end up more likely to lose everything.

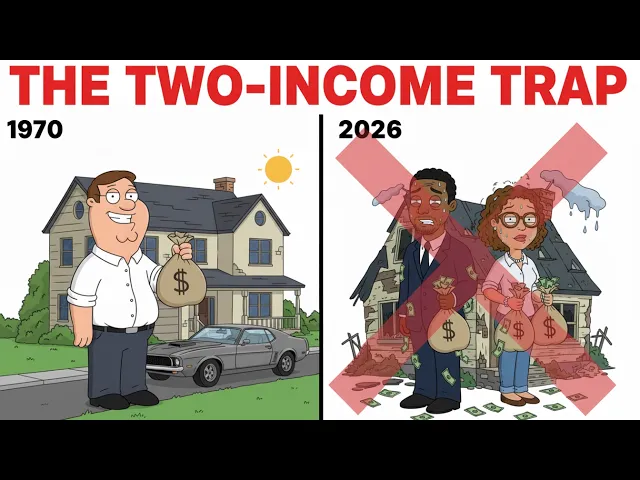

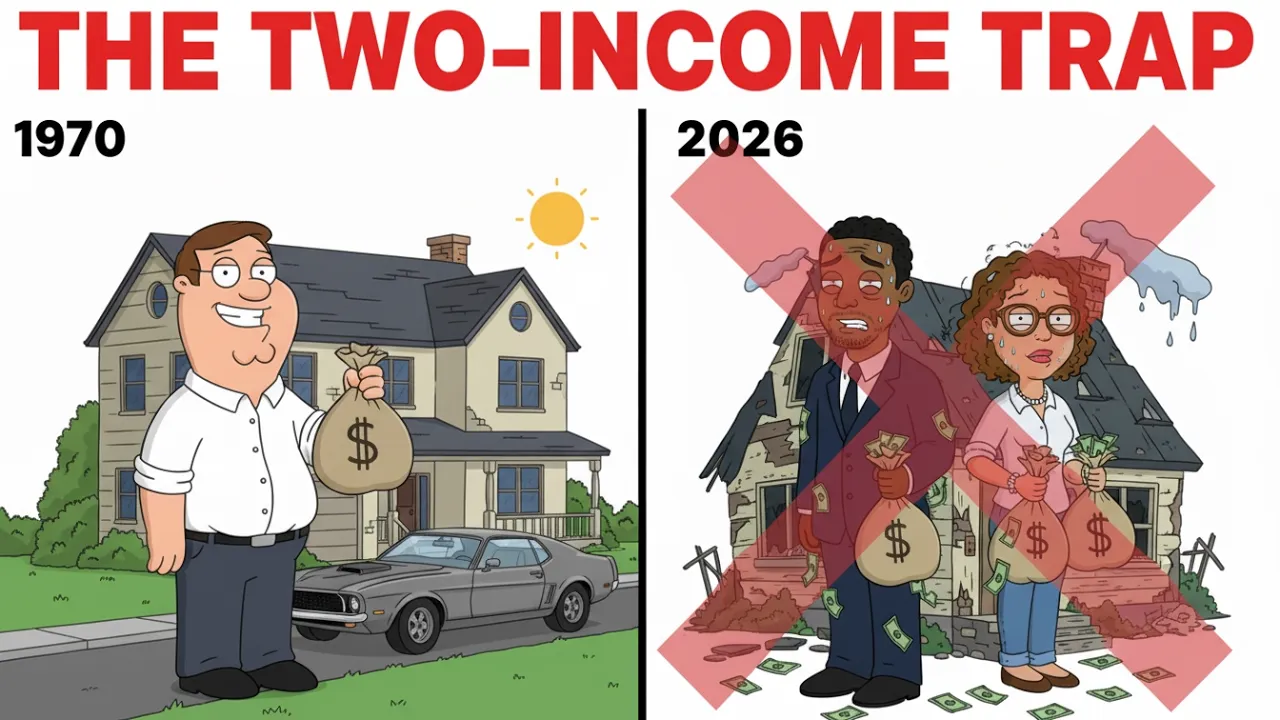

That's not a personal finance failure. That's a systemic trap, and you're probably standing right in the middle of it. Let me take you back to 1970 for a second because understanding the history is crucial to understanding the trap.

In 1970, about 43% of women participated in the workforce. The typical middle-class family had one primary bread winner, usually the father, and one parent at home, usually the mother, managing the household. And here's what most people don't realize.

That single income was enough. Not just barely enough, actually enough. According to data from the Bureau of Labor Statistics and Census Records, a median single inome family in 1970 could afford a median-priced home, spending about 25% of their income on housing.

They could afford to put their kids in public schools that were reasonably wellunded regardless of neighborhood. They could afford basic health care, a car, food, and still have money left over for savings and the occasional family vacation. They had financial margin.

They had breathing room. And critically, they had a backup plan. If something went wrong, if the primary earner got sick or lost their job, the stay-at-home parent could enter the workforce.

That second potential income was an insurance policy, an emergency reserve that could be activated if needed. Now, fast forward to today. Female workforce participation is around 57% and much higher among married mothers specifically.

The two income household has become the norm, not the exception. In over 60% of married couples with children, both parents work. We've essentially activated the emergency backup plan as the default operating mode.

And here's where it gets really interesting. According to the Bureau of Labor Statistics, the median household income in 2023 was about $74,000. Adjusted for inflation, that's significantly higher than the median household income in 1970.

We're making more money than our parents and grandparents did. But look at what happened to costs. Median home prices in 1970 adjusted for inflation were around $200,000 in today's money.

The median home price in 2023 over 400,000. Housing costs have literally doubled relative to inflation. Health care spending per household has increased by over 600% since 1970.

Child care, which barely existed as a major expense in the single income era because someone was home, now costs the average American family over $11,000 per year per child. And that's the average. In high cost of living areas, you're looking at 20 to $30,000 per child annually.

Education costs for college have increased over,200% since 1980. The fixed costs of being a middle-ass family have exploded while wages have merely crept up and all that extra income from the second worker got absorbed. Every single dollar of it.

The two income family doesn't have double the financial security of the single inome family from 1970. They have less because their fixed costs expanded to consume both incomes and they burned their backup plan just to keep up with baseline expenses. Now, you might be thinking, "Bobby, this doesn't apply to me.

We're smart with our money. We didn't let lifestyle inflation eat our second income. " And look, maybe you're the exception.

But let me walk you through the math of what actually happens to that second income. And I want you to be honest with yourself about whether this applies to your situation. Let's say one partner makes 70,000 and the other makes 50,000.

That's $120,000 combined, which feels like a lot. Let's focus on what happens to that $50,000 second income. First, there's taxes.

Because of the way progressive tax brackets work, that second income gets taxed at a higher marginal rate than if it were the only income. The first 70,000 gets taxed at lower brackets, but that additional 50,000 comes in at the top of the stack. Depending on your state, the effective tax rate on the second income could be 30 to 35% or higher when you factor in federal income tax, state income tax, and payroll taxes.

So, that 50,000 immediately becomes something like 32 to 35,000 in actual take-home. But wait, there's more. If you have kids, you need child care.

The average cost of daycare in America is about $15,000 per year per child. Got two kids? That's $30,000.

You haven't even left the house yet. And your $50,000 income is now worth maybe $5,000. And we're not done.

Two working parents means two commutes. The average American commute costs about $5,000 per year in gas, maintenance, and vehicle depreciation. That's if you're driving.

If you're paying for parking downtown, add another 2 to 3,000. If you need a second car that you wouldn't otherwise need, add the car payment, insurance, and registration. Call it 8,000 total for the second person's commuting costs.

Your 50,000 is now negative. But let's keep going because it gets worse. Two exhausted working parents means less time and energy for cooking, cleaning, home maintenance, and all the tasks that a stay-at-home parent might otherwise handle.

Studies show that dualincome families spend significantly more on convenience services and prepared foods. They're more likely to hire house cleaners, order delivery, pay for lawn services, buy pre-made meals, and eat out more frequently because nobody has the energy to cook after a 10-hour day, including commute. These exhaustion expenses can easily add another $5 to $10,000 per year compared to a household where one person has time to manage domestic labor.

So, let's add it up. That $50,000 second income minus $18,000 for taxes minus $15,000 for child care for one childus $8,000 for commuting costs minus $7,000 for convenience expenses and exhaustion spending, you're at $2,000. That's not a typo.

The net contribution of a $50,000 second income can realistically be as low as $2,000 per year. Maybe less, maybe negative, especially if you have multiple children or live in a high cost of living area. Someone is working full-time, being away from their kids, missing family dinners, grinding through traffic, and the household is netting $2,000 for the year.

That's $8 per workday. That's $1 per hour. And here's the psychological trap.

Because the gross numbers look big. Because you see that 120,000 combined income on your tax return, you feel like you should be doing well. You make spending decisions based on that 120,000.

You buy a house based on what two incomes can qualify for. You take on car payments that two incomes can theoretically support. The bank looks at your combined income and says, "Yes, you can afford this $400,000 mortgage.

" And technically, you can as long as both incomes keep flowing forever. As long as neither of you gets sick or laid off or burned out or needs to take care of an aging parent or has a child with special needs or hits any of the thousand unexpected life events that humans encounter. This is where the trap snaps shut and it's the part that Elizabeth Warren's research really drove home.

The single inome family from 1970 had something the twoome family today doesn't have. Financial flexibility. If the bread winner lost their job, the stay-at-home parent could find work.

Not ideal, but it was a backup. It was margin. It was resilience.

The twoinome family has already played that card. Both incomes are already fully committed to the monthly nut. There's no backup plan.

There's no reserve income to activate. If either partner loses their job, gets sick, or can't work for any reason, the family doesn't just lose that income, they often can't maintain their fixed costs, even temporarily, because those costs were sized for two incomes. This is why Warren's research found that two income families were more likely to file bankruptcy.

It's not because they were irresponsible. It's because they had no margin for error. They were operating at 100% capacity with no reserves.

Like a car running with no oil in the engine. Everything works fine until it doesn't and then everything breaks at once. A 2019 study from the Federal Reserve found that nearly 40% of American adults couldn't cover a $400 emergency expense without borrowing or selling something.

40%. And many of those people are in dual inome households making solid money on paper. They're not broke because they don't earn enough.

They're broke because their expenses expanded to consume every dollar of their combined earnings. And they're one unexpected transmission repair away from financial crisis. And here's what really gets me.

The expenses that consumed the second income weren't luxury expenses. They weren't boats and vacations and frivolous spending, at least not primarily. They were housing and child care and health care and education.

They were the fixed costs of participating in the middle class. Look at housing specifically because this is where the bidding war effect becomes clear. In the single income era, families competed for housing based on one income.

When two inome families became the norm, families suddenly had twice the purchasing power for the same houses. What do you think happened to prices? They got bid up way up.

If everyone has two incomes, then two incomes become the baseline requirement. and suddenly you need two incomes just to afford what one income used to buy. It's like an arms race where everyone escalated and nobody won.

The same thing happened with education. School districts are largely funded by property taxes, which means good schools exist in expensive neighborhoods. Parents naturally want to live in areas with good schools.

So, families started bidding up property prices in good school districts, using their two incomes to outbid others. This created what Warren calls the bidding war for educational opportunity. The price of admission to good public schools became a $400,000 mortgage instead of a $200,000 mortgage.

You're not paying tuition, but you're paying the tuition equivalent in your housing costs. And once you're locked in to that mortgage, you're locked in to needing both incomes forever. You can't go down.

You can't go back to one income. The trap has closed. Now, you might be thinking, "Okay, Bobby, but what am I supposed to do?

I can't just have my partner quit their job. We need both incomes to survive. " And I hear you.

That's exactly the trap. You need both incomes to survive the lifestyle you've built around both incomes. But here's the mindset shift that changes everything.

You need to start treating the second income like it's temporary, even if it isn't. Here's what I mean. Most families do the opposite.

They treat both incomes as permanent and guaranteed and they build their fixed costs accordingly. They buy the house that two incomes can afford. They lease the cars that two incomes can support.

They enroll the kids in activities and schools that two incomes can pay for. And then they're stuck. They've built a life that requires two incomes to function.

Which means neither partner can ever stop working, even if they want to, even if life circumstances make it necessary. The alternative approach is what I call the one income foundation. You structure your fixed costs, your non-negotiable monthly expenses so they can be covered by one income alone.

The second income then becomes entirely discretionary. Savings, investments, debt payoff, or yes, some lifestyle enhancement. But the critical difference is that you could survive without it.

You'd have to cut back. Sure, life wouldn't be as comfortable, but you wouldn't lose the house. You wouldn't go bankrupt.

You'd have the margin that modern dual income families have lost. Let me make this concrete. Say your household makes 130,000 combined, 75,000 and 55,000.

Instead of taking on a mortgage that requires a h 100,000 or more in annual income to service, you take on a mortgage that can be comfortably covered by 60,000. Instead of having two car payments, you have one or none. You live in a neighborhood that's maybe slightly less prestigious with schools that are good but not elite.

You buy the house that one income can afford and you bank the difference. That second income or at least the majority of it goes straight into building wealth. Emergency fund first, then retirement accounts, then taxable investments.

Every dollar you invest is buying back optionality. It's buying the flexibility to have one partner step back if needed, to take a career risk, to handle a health crisis, to be present for aging parents, to actually have a choice. This requires sacrifice in the short term.

It means driving past the nice houses you could technically qualify for. It means explaining to friends why you're not upgrading your lifestyle even though you got a raise. It means resisting the social pressure to spend like a dual inome family because you're building like a single inome family.

But here's the payoff. Within 5 to 10 years of this approach, something magical happens. The investments you made with that second income start generating their own income.

Compounding takes over. And suddenly, you actually have what you thought dual incomes would give you in the first place, genuine financial security. You're no longer two job losses away from crisis.

You're building wealth instead of treading water. You can make decisions based on what's best for your family rather than what's necessary to make the mortgage payment. I want to leave you with one final thought because I think it reframes this whole conversation.

The two income trap isn't really about income. It's about flexibility. It's about margin.

It's about having options. Our grandparents with one income had something that we've traded away. the ability to absorb a shock, to change direction, to have one partner focus on raising kids or caring for family without the whole financial structure collapsing.

We traded that flexibility for bigger houses and nicer cars and the appearance of prosperity. But appearances aren't wealth. Cash flow isn't security.

And two incomes aren't better than one if both of them are already spent before they arrive. The families who thrive financially in the modern economy aren't the ones who earn the most. They're the ones who've preserved their flexibility, who've refused to let their expenses expand to consume their income, who've kept their backup plan in reserve instead of deploying it just to keep up with the Joneses.

You can earn your way out of a lot of problems, but you can't earn your way out of a trap you don't even know you're in. Now you know. The question is what you're going to do about it.

If this video helped you see your finances differently, make sure to smash that like button and subscribe for more content that challenges how you think about money.