[Music] [Music] welcome students so till my last lecture we completed the process of analysis of the financial statements we discussed the process of analysis of the financial statements and we learned about the two techniques that is say ratio analysis and the cash flow statement and there are some other techniques also so these are the two prominent techniques generally used and there are certain other techniques also so I'll talk to you and just for a minute or two in the passing reference about those techniques and then I will move to the third part that is about the let's say a regulatory framework of the financial reporting in India that is for your reference I would like to discuss so are the other techniques of the financial analysis if you want to learn about there are very easy techniques means any book or anywhere you can easily find if you have any book on the financial and the corporate reporting or the corporate or accounting or financial accounting you will easily find those techniques those techniques are so you can call it as common size statements common size statements and second is the comparative statements comparative statements so these are the other my by preparing other statements also you can do the financial analysis furthermore also if you want to understand about the progress of the company or the say performance of the company and common size statement is other way around you can call them as a common size or maybe the multi-step income statement multi-step income statement and here you call it as horizontal statements so in this case what is what we do in the common size statement that we take that one important figure is common say for example you talk about the sales is a common figure and against that figure we compare what is the percentage of the cost of goods sold similarly what is the percentage of the fan or material similarly what is the percentage of the same manufacturing expenses similarly what is the percentage of other say administrative and selling and distribution expenses so as a percentage of the sales so taking one item is common and then comparing the other figures against that item we do by preparing the common sized statement almost the same thing we did in the multi-step income statement also so the difference in the multi-step income statement was that we calculated the profit at the multi steps we didn't jump to the simple net profit after tax but we calculated first of all the total sales gross sales minus excise duty then net sales and then we say subtracted from this was the cost of raw material than manufacturing expenses then we caught the got the cost of goods sold and then we subtracted other expenses we got the profit before tax and depreciation interest and tax then because the subtracted depreciation then profit before interest and tax then we subtracted interest then the profit before interest and tax so that was calculation of the miss is a calculating the profit or income in in a multi-step way but in the common sized statement we do the same thing almost but we don't compare any profit or income we simply compare the different items which are making the income statement profit and loss account you you can you can easily compare the items of that income statement profit and loss account with one common figure and if you take that against the sales what is the cost of goods sold what is the raw material what is the manufacturing expenses but the administrative and selling and distribution expenses that way we can prepare the common size statement by following the multi steps so this is a one way of doing the analysis and this analysis is largely done with the income statement with the profit and loss account we not do it in the balance sheet for the balance sheet you can use a second it is a comparative statement so for analysis of your a profit and loss account of the inn you can do it in the balance sheet also because in the balance sheet you can take the total assets as a common figure and against the total assets you here you take it as a total assets as a common figure and against the total assets you subtract now what are the fixed assets what is the percentage of fixed assets what is the percentage of current assets and what is the percentage of investments what is the percentage of loans and advances what is the percentage of prepaid expenses you can be done also so means you can take one item is a common in the balance sheet in the financial position statement and then you can compare the other sales a subsequent save parts belonging to that category with against that major category and then you can say that you can easily make out that out of the total assets what percentage of the total asset is fixed assets what percentage of the total asset is the current assets because we want to know that current assets level should be as low as possible and fixed assets should be high so similarly prepaid expenses should also be low there is a loans and advances down investments can be more so we can easily make out that what constitute the fixed assets what's what constitutes that we say liability is also you can take the total liabilities and out of the total liabilities what is the percentage of internal funds what is the percentage of external funds loans and advanced missile owns and the Dementors and then the current liability so that way the common sized statement can be prepared and this is called as a vertical statement this is a vertical statement this is one statement that can be prepared and the one analysis can be done then the second way of analyzing another technique of analyzing the financial statements is that say horizontal analysis by preparing the comparative statement by preparing the comparative statement so normally we do prepare the comparative statement we can use you can do it for the income statement also for the income statement also and for the balance sheet also so far you can put largely we use it for analyzing the balance sheet and if you say prepare the horizontal statement you can take one company and then you can say BC limited and see we can have the figures here say for example you're talking about this is asset site so you can say the assets of the company if you take the assets of the company in the assets total assets of the company you can say that will be it will be taking figure not only for one year we can take that figure of 2014 then we take the figures of the 2015 and then we take the figures for 2016 or we can take the figures for other years also so normally we take the two year's figures so you can take the figures of same at 2 14 15 and 16 and then we make the one column here that is a column for increase or decrease so in C you see that what was the level of your assets say fix SS you talk about so if you take the fixed SS ah here it was hundred and it has become one hundred and ten so there is increase by ten it can be in percentage terms also it can be in the absolute terms also similarly you talk about the current assets current assets were here say 50 and now they have become 60 so there is increase by 10 so you can easily make out that what is how the other things are moving out maybe when you are moving from the one year to the another air Comparative position of the companies what comparative picture of the companies what whether the companies improving this acid base and the fixed song as long-term assets are increasing as compared to the current assets or current assets are increasing as compared to the fixed assets or both are static so your trend can be worked out this is called as a trend analysis also a trend can be worked out so this statement is called as comparative statement this is a horizontal analysis because you do it this way and the common size you prepare this way that is called as the vertical analysis so these are some and here you call it them as a trend analysis also this is going to give you the trend if you put the say in the horizontal endless if you add some more years there were two three four five years if you make and you draw a line it will give you a trend that over the period 2010 to 16 how the assets have moved so you can draw the lines and you can understand the trend of the form and you can understand the whole process so these are some further ways of analyzing the income statements or the financial statements that apart from ratio analysis and the cash flow statement which we discussed in detail you can use the common size statement you can use the comparative statement and you can know the company in which you are interested or you are somebody's and else is entrusted and you are acting as a financial analyst to him or her then you can use these techniques and by doing a detailed analysis by using the third these third some other techniques some other techniques means in the third category common size comparative state homicide statements comparative statements then yes it can be done and it will give you a better picture about the overall financial performance and position of the company in which you are interested or somebody else is interested and you are acting for him and her as the financial analyst so with this I complete the process of the analysis of the financial statements and now in the remaining this class end in the one more next class last class I will be talking for the reference purpose not in detail I will be talking to you about the financial reporting process in India so now let's move to this part that is the regulatory framework of the financial reporting in India and we'll be discussing this to some extent because this largely is a structure and system which is available everywhere different sources are there and this information is easily available but as a student of financial statement analysis and reporting you should be knowing something here and we should be discussing something here so I thought of say say enlightening you about the financial reporting process there's a regulatory financial reporting process in the existing in India that is in the country and let's discuss something about that so this is we are going to talk in the remaining part of this lecture and then in the next one more lecture look when we talk about the regulatory feeling of framework of the financial reporting in India or in any country you see there the different say bodies because in an economy if there is a then there are some rules and regulations of running the business and adherence to those rules and regulations either the companies have to say ensure themselves and companies are doing that also there are certain aberrations like Satyam case or maybe some time such as Matta was the case earlier which created a problem in the securities market then this certain cases there then some you can call it as Vijay Mallya cases there so these are some cases when the things are not moving in the right direction or in the desired direction but generally the things are mister correct and the businesses also say acting is a very responsible stakeholder in the market but sometimes it creates the problem you see that when we were talking about the financial statements preparation of the financial statements is what is the purpose of financial statements means if the business is going on and we are manufacturing certain products or creating rendering certain services in the market we are doing it on the continuous basis and we are getting raw material converting the advent of finished product finished product is going to market form is getting back its funds through sales and it's getting the profit shareholders are getting dividend employees are getting salaries comment is getting the taxes and people are getting the good quality product so what is the purpose of preparing the financial statements why the government has fixed the say say the requirement of preparing the financial statements and why it is a mandatory has been made mandatory to say had the financial statements once in a period of 12 months that is a accounting period we call it as the accounting period why it is necessary why it is required that is a million dollar question here and then mystery arises the need of financial reporting means when we prepare that these financial statements are low these were the two statements that is the income statement and balance sheet which means by using these statements preparing these statements ability to elements it company insures and company reports to the different stakeholders that how the business is going on different stakeholders miss then we talked about the different stakeholders first are the shareholders then means the first are the lenders debenture holders shareholders employees of the company even the customers of the company consumers of the company then the tax authorities and the public means that then the government and then the public at large everybody sometimes remain concerned about the overall financial performance of certain companies so for example now there are some popular companies like reliance industries or Infosys or your Tata Group companies or some other important companies so people generally even general public also remains concerned about it say when we open that newspaper in the morning and on the business page of Times of India when we find that this these are the developments with regard to Tatas growth or Tata has acquired this company or Tatas profit is going to go up this quarter or this say here or Reliance Industries financial performance is that it means it doesn't mean that I am the shareholder of Tata as companies are I am the shareholder of Reliance companies but when I open the page of the newspaper I'm really interested to look at that news at how one important industrial house or the business house in my country is doing so in that case even the general public is also is then a very important stakeholder so by preparing these financial statements that is the say trading and profit and loss account you can call this statement as the income statement also and then the balance sheet we report to the different stakeholders that how we have been doing in the past 12 months whether we have ended up with the profit or with the loss or if there is a profit then how much profit is there and if there is a loss how much loss is there and whether our profit is going up in the current here as compared to previous here or if our loss has come down in the current here as compared to the previous year so all these things are the miss are some objectives which are met with the help of preparing the income statement similarly we prepare the balance sheet and by preparing the balance sheet we confirm that our assets are equal to liabilities and vice versa and we convey it to the in to stakeholders that yes we are doing a good business balance sheet or the financial position is balanced is within control and nothing is wrong in the form and means all the stakeholders should rest it assured that we are doing a good quality business the company communicates and now the third statement is also very important mandatory statement that is the cash flow statement that under the cash flow statement B companies tell to the outside world or to different stakeholders that say a larger chunk of the profit is from the operations if it is a manufacturing organization and is from financing activities if it is a financial company and from the investing activity duties if it is a investment company so that is the wave and that is the objective of the financial statements or preparing that especially the cash flow statement so in this process of say procuring these three mandatory statutory statements the purpose of preparing these statements is means an away reporting of the financial affairs of the company's business organizations and by preparing these statements apart from these statements and you prepare some other statements also but they are not mandatory they are only for the internal control many companies analyze these financial statements they prepare analytical report also by doing a detailed ratio analysis or sometime by preparing comparative statement common sized statements but they are not for the external reporting for the external reporting only these three statements are mandatory and they are prepared this is the one part that preparation of the financial statements in itself is a one act of reporting of the financial performance of the companies now the second question arises here what is the basis of a reporting what facilitates the better reporting of the financial affairs or the business affairs to the outside world or to the rest of the world then we start a discussion on this subject I started with one thing that the basis of preparation of the financial statements is or financial reporting now I would call it as that the basis of that preparation of the financial statements and the financial reporting I have already talked to you is that is the gap generally accepted accounting principles generally accepted accounting principles and when you talk about the generally accepted accounting principles we talked about so many things we talked about the accounting concepts then we talked about the accounting conventions then we talked about the accounting standards and then we talked about the different types of accounts and then we talked about the different rules of passing or recording the business transactions in the books of accounts this all though the large component major components are these three that is the conception of conventions and accounting standards but these are also the insulin airy parts of the gap that is different types of accounts and their rules for recording rules of recording the transactions in the books of accounts so accounting standards are the most important part because when we talk about the accounting standards means in the gap we talk about something that it's a say it's a standardized way to report the corporate information or the financial information of the corporates or companies to the rest of the world so that everybody not in India everywhere if they look at the balance sheet they understand it in the same sense or in the same meaning and when you talk about the gap every country has its own gap right we have US GAAP we have Indian gap we have other countries means every country has a gap they have their own generally accepted accounting principles and a common body which is say connecting each country to the other country and coordinating amongst the countries is the another body which is called as a ia SB International Accounting Standards Board so it means when you talk about US GAAP they have u. s. standards when you talk about the say Indian gap you in India has its own Indian standards and when you talk about the IASB I ESP has also dealt with its own standards which now are called as IFRS international financial reporting standards so first every country's developing its own standards and then they're trying to harmonize their own standards with the word standards they are international snot word standards with the international standards and they are the IFRS currently we have two systems of accounting one is that national system of accounting which is there in every country being observed by say following the every country's accounting standards and then we are because now we are becoming a global village and there are miss boundaries for the business are shrinking it means you see that today if you want to buy any product being manufactured in any part of the word earlier was being manufactured in any part of the world that is available today in India the companies which were micellar now you can call it as external operators they were not allowed to operate in India in because India was a closed economy today you find these companies are working here and not working here sometimes they are manufacturing more here and supplying it to their home country also to the other countries in the world so when you are dealing across the boundaries across the countries in that case it means if India has a want different accounting standards other country has a different accounting standards if production is in India and sales are to be done product is to be transfer from India to UK or to us or to Japan in that case there comes the problem means that what price the product should be sent is inward price it should be priced in India at what price it should be transported or sent to Japan or US or UK so transfer pricing is one important issue so what is going on now slowly and steadily we are moving to a process we have national accounting and we have international accounting and slowly and steadily we are moving from the national and international accounting to the word accounting so what accounting would be that the day when there would be no national and international standards all the standards will be same all around the world all the countries are valuing their fixed assets their current assert their liabilities their incomes and expenses in the same way as one company's doing in India same way that other company is doing in the US so that means we are moving slowly and steadily complete harmonization of the Accounting Standards what we have not done been able to do that so far but the recently the development has been that say we had say common national standards but now most of the international community members means different countries in the world they have agreed that they would like to converge their national standards with the International Accounting Standards means you can call them as the international financial reporting standards given by the International Accounting standard board so Mis that's a process which you will have mr.

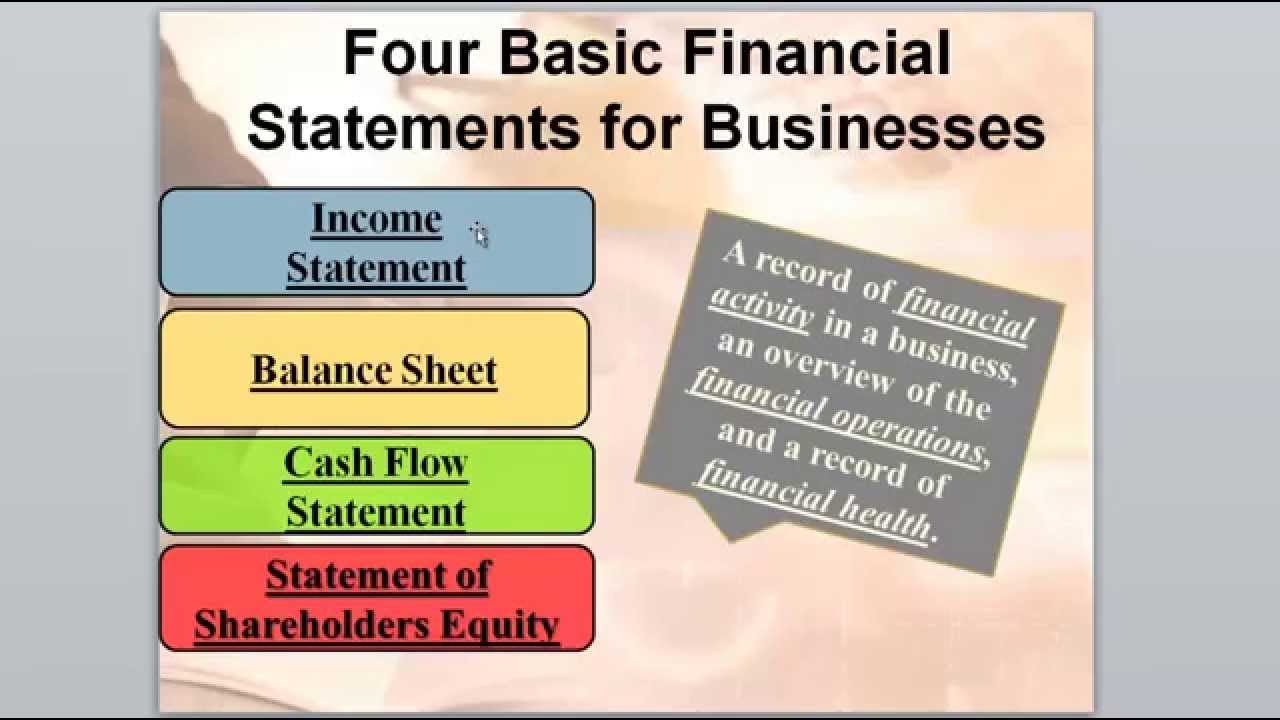

time will come when you have a common GAAP but we don't have a common GAAP today every country has its own GAAP and on the basis of that the financial statements are prepared and financial reporting is done so I will take you through this journey quickly this presentation and later on you can go through this presentation yourself and some broad provisions I have given here and then you can get to know about the provisions of this discussion so first of all let's talk about the objectives of financial reporting in India or maybe not in India anywhere in the world you can say so there are the different objectives first important objective is to provide financial information about the reporting entity that is useful to the existing and potential investors lenders and other creditors in making decisions about providing resources to the entity or that business organization or that company this is the first objective means should you become an investor in this company by buying the share of their company should you lend money as a financial institution to that company or should you supply your material to that company on credit basis you will do that if you funds are secured so that is only possible if the financial reporting is is you are eating through busy help of financial reporting when you are analyzing these financial statements of the companies you are able to make out that it is this is a good company this is a strength full company as we have seen in case of the companies like skyline we have analyzed the skyline or earlier we have analyzed here Grasim industries so if you look at their whatever they are reporting through their financial statements you can find out this they are the word companies and nobody will even think twice to deal with those kind of the companies so there is a purpose second objective is to facilitate decisions involving buying selling or holding equity and debt instruments and providing or settling loans and other forms of the credit very useful information you can get from the financial statement so only because it is a information about the internal affairs of the company so finally you can see it is useful to investors whether to buy the shares of that company or sell the shares of the company whose shares they are already having or hold it for some period of time may be the situation is not good maybe in case of the Grasim industries we have seen that their say price went up to twenty seven hundred rupees two thousand seven hundred seventy eight rupees in January but later on it fell down so maybe people deciding that when it fell down and March and people were holding their share they could have decided hold it further for some period of time again it will go up to two thousand seven hundred or two thousand eight hundred and if it reaches two thousand seven 100 or eight hundred or touches 3000 rupees I'll sell and I'll get to the maximum returns so that way the decisions are taken useful to lenders and other creditors financial institutions lend big money to the business undertakings and they have to have some basis of substantiating their decisions that whether they should lend or not and then it is useful to the creditors also you see that most of the business is on the credit so suppliers supply the lot of inputs through the companies on credit and they have to be sure that how this company is doing so whatever the company is reporting in the financial statements you we analyzed as a supplier and you can take a decision about that so these are the three important objectives of the financial reporting anywhere in the world including India when you talk about financial statements which are important financial statements required to be prepared we have already discussed many times what here for the reporting purpose I'm recalling it for the CSA just a reference purpose we all know that you have to have a the complete set of the financial statements includes that is statement of financial position means balance sheet that depicts the financial position of the firm only for one day then is the statement of comprehensive income means it's a income statement profit and loss account which gives you the details about trading account profit and loss account and overall income and expense position of the forms which is a comprehensive income statement then statement of changes in equity sometimes some company's not in India is not very common but in u. s.