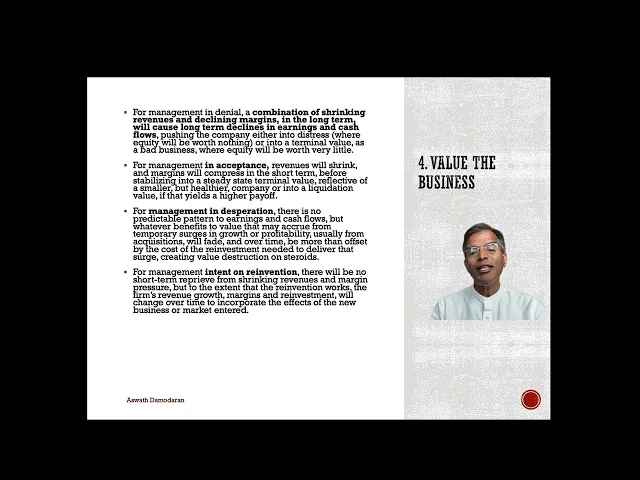

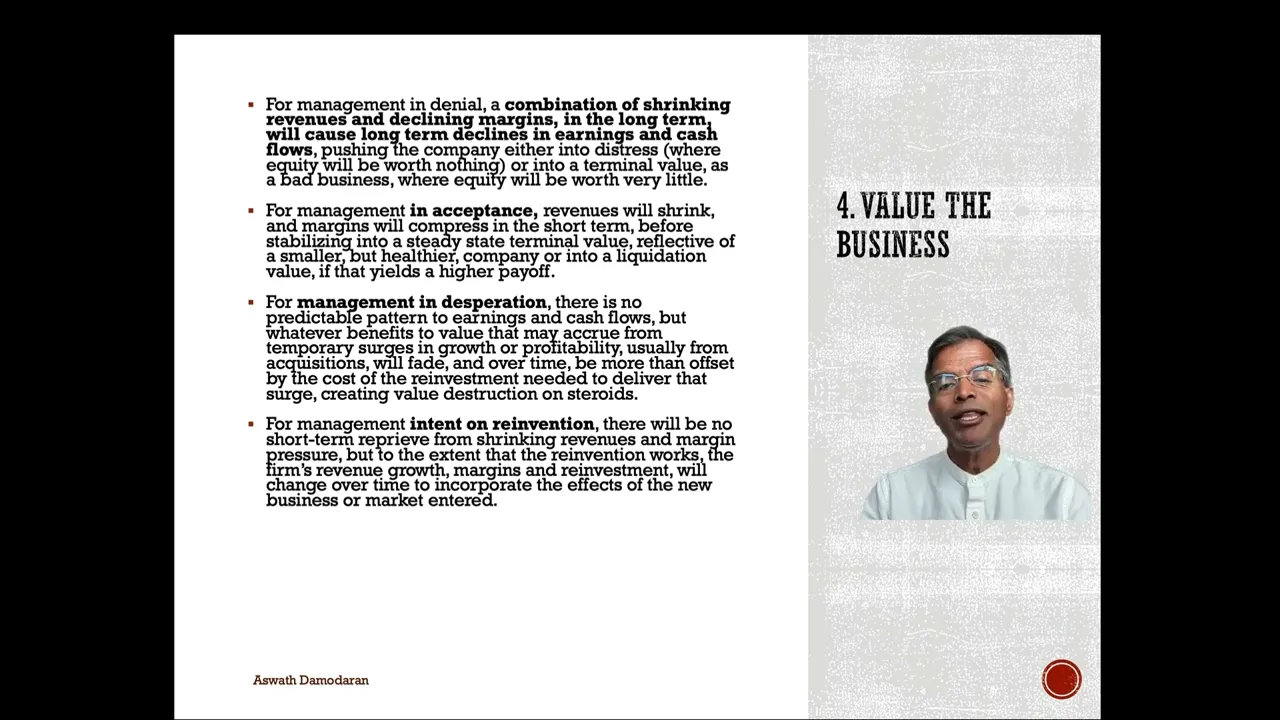

hi welcome back we've talked about valuing startups high growth firms mature firms and in this session I want to talk about valuing declining companies what is it that you look for in a declining company the first is you're going to see revenues that are either stagnant or declining over time second is your margins are under pressure they're either shrinking or maybe even negative the third is this company is selling off stuff rather than investing in stuff they're divesting assets know sometimes to get cash sometimes to make themselves smaller along the way though some of these firms will try to do Acquisitions it's almost like they're trying to reorient their asset base selling some assets buying others and usually at declining firms you're going to see big cash payouts big dividends big BuyBacks and if there is a downside to debt it's in declining firms you're going to see it what's a downside of debt while it gives you tax advantages it exposes you to distress in declining firms you're more like to see the distress effect shrinking or stagnant revenues margins Under Pressure assets being redeployed sold off added on big payouts and distress the distress might or might not be there depending on whether there's debt but those are usually the characteristics so what are valuation challenges when you're looking at Assets in place which should be almost all of the value your declining firm don't be surprised if those Investments that the company's made on earning less than their cost of Capital At first side you're saying that makes no sense why would companies do that remember that when these companies made their Investments that wasn't the case they were actually earning more than their cost of capital but that was 5 years ago 10 years ago 20 years ago maybe even 50 years ago today the business has changed those com those those assets are earning less than the cost of capital that will also mean that when you value these value these assets don't be surprised if the value you get is less than the book value of the assets the second is we talked about these companies making devages sometimes because they need cash and sometimes to restructure their asset portfolio Dev vestages though create consequences in valuation they create discontinuities in the data if I sell off one of the four divisions I have as a company what you're going to see in the revenues and income in the year that happens is going to be a drop in revenues and a drop in income now Dev vestages can also affect know Mar Marin and reinvestment so it becomes much more difficult to assess what the company is earning as a return in invested capital on its assets and finally risk parameters whether they be based on price-based data or earnings based data are going to shift when you devest off significant portions of your company when it comes to growth assets your first response is what growth assets these are declining companies here growth is negative growth the compan is shrinking and the question you're asking is it shrinking in a sensible way what does that mean you shrink in a sensible way it basically means you're divesting assets or shutting down assets that earn well below your cost of capital you're able to get your Capital back but divestures can lead to negative growth rates psychologically that is difficult for us to handle as human beings when we value companies we feel almost programmed to put in a positive growth rate but if a company's divesting in getting smaller you have to be okay using a negative Revenue growth rate your revenues get smaller over time and some declining firms which are in denial what does that mean they don't recognize that are in in Decline they think they can go back to growth will continue to reinvest and as they reinvest and earn well below their cost of capital the more they grow the less valuable they will become so those are challenges that you will face in val declining companies and there are risk components as well now we talked about declining firms often returning cash to shareholders which is a sensible thing to do you're declining and shrinking you sh but those dividends and BuyBacks will have effects on your Equity because every time you pay a dividend to buyback stock you're reducing your Equity you're saying so what if the company is not also reducing its debt this is your pathway to distress your Equity gets small your debt stays where it is and you can very quickly find yourself go going from being a healthy firm to a distressed firm when you devest assets if those assets are riskier or safer than the rest of the assets in your business you got to re-evaluate the effect on your hurdle rate and cost of capital and Fin finally as I said if you don't pay down debt the presence of distress which is going to shorten sooner or later is going to affect all of your parameters your ratings will drop your cost of debt will climb your cost of equity will climb your cost of capital will become higher and more unstable so from valuation perspective the challenges you face with declining companies is you can't do what you're programmed to do in valuation grow yourself out of the problem cuz growth is not the option that is a available here so let's summarize the issues you're looking at a declining firm you ask the four questions what are my cash flows from existing assets you look at my at the past history you see shrinking revenues margins under pressure and along the way you might find that you're being challenged by you know litigation and other issues that come with being a declining firm especially in the in the presence of distress growth can be negative and that's something that you have to accept as a given it's not a good thing it's it's not a bad thing it is what it is as a declining firm your Revenue growth can be negative your company will get smaller your risk can Shi can shift especially if you're selling off businesses shutting down businesses and to the question of when will your firm be a mature firm the true answer was that was 20 years ago I'm no longer mature here your endgame might be liquidation rather than as a going concern in fact you have two end games one is you can liquidate your assets at a point in time or you can become a much smaller B business and perhaps survive as a niche business so in terms of valuation responses by now you know the pathway I'm going to start by telling a story the story for a declining firm is not going to be an uplifting soaring story it might even be a horror story but it reflects the reality that in declining firm your story has to reflect that decline so when you make a diagnosis of why your company is declining that's got to be incorporated in your story because that diagnosis might lead you to believe that this is not something your company can fix but in in your story you got to bring in how you think the management of the declining firm is responding to the decline and there are four four possibilities the first is as we pointed out some managers are in deine are in denial when they're in denial they will keep acting as if as if they're mature growth firms reinvesting for growth when in fact they shouldn't be doing it the second is desperation these managers will try everything will do an acquisition enter new businesses devest random assets the third is acceptance unusual but actually very healthy where you say look I'm a declining firm I'm going to run my company as a declining firm what does that mean you're not going to reinvest for growth you're actually going to shrink you're going to shrink in a sensible way and make yourself a smaller company the fourth is reinvention reincarnation where you find a way a pathway back to being a mature or even a growth company I mean that is a a very attractive option for managers who want to become Legends but along the way they might lose lose a lot of your money trying to get there so when you tell the story for your declining company you've got to actually figure out what the management of the company looks like and how they will respond to decline your second stop is once you've told your story if you're declining company which can be either a denial story a desperation story an acceptance story or a reinvention story I'm going to push back the three p yes is it possible is it plausible is it probable all too often with declining companies you heard the reinvention story we're going to become a great company again we're going to become a growth company and you got to push back and here are some of the factors in whether you think your company can make it back from decline it's easier to map a pathway back to health if you're the only troubled company in a business that's healthy cuz there you could argue that if you just change the way the companies run you could go back to being a healthy company much more difficult to do if everybody in your sector is hurting everybody is in Decline cuz then what pathway are you going to adopt where your competition doesn't try to do the same thing in fact one of the one of the concerns you should have when somebody tells a turnaround story is they act like the rest of the world stays still while they do this turnaround with the company but let's face it if other companies are feeling the same pressures they're also mapping turn around plans and if they're all trying to do the same thing they'll all fail and finally you're looking at the management just as with startups management matters a great deal more with declining companies because if they overshoot they overreach they can very quickly devastate the value of the company so as you look at the 3p test you're asking the question of is this a management capable of pulling off this turnaround now if you think about how your story is going to play out in inputs I'm going to use the four pathway that you see and depending on where you see your company's management going the numbers are going to reflect if your man if you're valuing a declining company where you think the management is in denial your Revenue growth rate will continue to be negative your margins will continue to decline but the company will keep reinvesting as if it's making money and as if it's a healthy company this is in a sense your worst case scenario because you will have negative or low growth declining margins and lots of reinvestment and your value will reflect it your cost of capital though will reflect the fact that the company is in denial you can keep doing what you were doing historically if your company is desperate you can get blips from Acquisitions on new Investments you can see short-term boosts and margins when you try something the first year your reinvestment is going to be all over the place because you're desperate you're doing an acquisition now and an acquisition later it's very it's random almost where you go and your risk is is going to be volatile because you're entering new businesses if you're an acceptance your Revenue growth is going to be negative you might have declines and margin the short term but you should see Improvement because you're shutting down because you're an acceptance shutting down the parts of the business that are the least profitable you will not have reinvestment in fact you will have what's called negative reinvestment you'll be divesting those parts of your business which I which you think are dragging you down and your operating risk will reflect what you see as a risk in that niche business the smaller business you're building if you're Reinventing Your company then Revenue growth can be positive because you're finding a way to reinvent yourself your margins will probably decline in the near term while you're putting through the reinvent but eventually they have to improve to reflect the success of your reinvention your reinvestment early on might be negative for existing businesses because you're getting out of some of the bad businesses but it'll be positive you'll have to be reinvesting in the new businesses you think you should be into and the operating risk and cost of capital for your company should reflect your reinvented company what you think you will look like after the reinvention you can see there are layers to valuing declining companies which requires you to take a position on what you think management will do so you come up with this this this story for your company that reflects the management of the company and where they're trying to go you come up with inputs that reflect that story you put the inputs in and you value the company you're you are going to get a value for the company that reflects the choice you made on management for those companies where you think the management is in denial you will get the lowest value because these companies in a sense will have the worst of all scenarios they'll have low growth NE margins that are shrinking and lots of reinvestment that never seems to pay off for companies and acceptance you might find a map Pathway to Value because these companies are willing to get smaller and maybe there's a version a niche version that can survive as a healthy company and that will give you enough value for these companies perhaps to be Investments you might want to make for companies in desperation it's anybody's guess if you get lucky in that desperate move you make maybe you can become a successful company but all too often what the desperation will mean is bankers and Consultants will get wealthy while you're desperate because you're trying different things most of them will not work they'll end up wasting money at the end of the process you'll have nothing to liquidate and finally for companies on reinvention you could come up with a significantly higher value if that reinvention works that's part of the reason why reinvention and reincarnation is so attractive to businesses because if it works you could multiply the value of your company but the reality is the odds are against you success is uncommon but maybe your company the company you're looking at is the one that's going to succeed so the value will reflect again what you thought about the management of the company and finally on the feedback loop being open as you make your assumptions about know if you're if your story was about Management in denial here's what can shake your story up and cause the feedback loop to C to change your story maybe the management will change the management that was in denial gets replaced by a new management a new CEO new board of directors if you're valuing a company based on desperation managers being desperate the presence of an active investor can change that story very quickly because an activist investor comes in and says hey this desperation is not working it can shut your story down if your story is one where managers will either go for acceptance or reinvention then you're looking for feedback on whether that's working cuz accepting that you're in Decline doesn't necessarily mean that you're aren going to end up with success it improves your odds but you're looking for feedback on the chances of that happening so the feedback loop here is about looking at management and seeing if your assumptions about them work and what can change those assumptions so let's use an example to illustrate valuing a declining for company I'm going to values Bed Bath and Beyond in 2022 for those of you not familiar with this company it's a brick and motor retail company that soared as a retail company in the 1990s one of the most successful growth story is that it worked for a couple of decades and then Amazon and the online retailers laid waste to all of brick and motor retailing already you can see the framing of the story this is not just a trouble a a declining company in a business that's healthy it's a declining company in a sea of declining companies bricking M retail companies the numbers back up the decline story if you look at the revenues for Bed Bath and Beyond going back in time you see the revenues peaked in about 2016 and 17 and they've been down significantly dramatic ically SS and the margins have gone from positive to negative this is a company that's shrinking its margins under trouble you can't blame the economy you Can't Blame a trend this is clearly long-term and working against them so here's my Bed Bath and Beyond story and again you're welcome to disagree with it I'm going to assume that the shrinking in revenues will continue 10% in the next year 5% every year for the next four years but I think eventually there is a much smaller version of bed bth and beyond in some segments of this of the US which will succeed a much smaller version second I am going to assume that this com the company will shut down the stores they should shut down the biggest most expensive stores the stores which have the lowest margins most negative margins and over time I'm going to assume that that Niche company that's going to be created is going to have margins close to that of a US retailer implicitly I am assuming Bed Bath and Beyond is run by managers who have accepted the fact that there's no turnaround here for reinvestment there's no reinvestment needed if you're shrinking but you are going to be shutting down stores but I'm going to assume that the cash flows you get will be from those devest the store shutdowns and those cash flows can augment your operating cash flows for risk they will stay a retail company much smaller retail company but there's a significant chance of failure in 2022 in fact given their B1 rating from Moody's translates almost a 24% chance of failure I'm going to incorporate that and right now they are indebted beyond what they can afford and over time I'm going to assume that as they approach this Niche status they'll find a way to bring their debt ratios down to more manageable levels which will bring their cost of capital down in steady state and stable growth I will assume that that Niche company they create will be able to grow at the same rate as the economy but they're not going to make excess returns you're going to earn your cost of Capital this is not a soaring upbeat story but it's a story that I think fits Bed Bath and Beyond and here's the value that I get from that story my revenues go from 7 billion down to 5. 9 billion I'm building a smaller company my margins improve as I shut down my most expensive stores I actually get cash flows in as I devest assets so that's what the negative reinvestment is and my free cash to the firm actually becomes positive because of those divestures early on and eventually as a Niche company my terminal value reflects at Niche business along the way I am going to assume that the company's cost of capital will decreases its debt ratio becomes manageable debt cost of capital is similar to that of a median retail company so the cost of capital goes from 8. 8 to 7.

5% but I'm realistic given how close to distress they are I'm going to attach a probability of 24% or 23. 7% that they will not make it with those assumptions and those inputs the value that I get for Bed Bath and Beyond is $323 the stock at the time that I valued this was $8. 79 what does it tell me either there's a pathway to reinvention that the market is seeing that I'm not seeing how the market is wrong I mean I would not invest at8 $8.

79 but that is my story and my value driving that judgment now that's EV valuation question you can see the challenges dealing with negative growth distress and those are issues you're going to run into if you try to price declining firms as well if you compare a declining firm in a to a sector where every other firm is healthy the declining firm is often going to look cheap on many metrics because the market sees the decline and if you compare it based on EV to sales the declining firm will look cheap if most of your companies in your sector are dein deining then you got to figure out a way to control for difference or degrees of decline across companies so when you price a declining company you have to be careful that you don't get trapped by just looking at a pricing metric say this company looks cheap I'm jumping in and buying the company it's true you can do forward metrics and many analysts who value declining companies or Price declining companies do it what does that mean instead of looking at the negative earnings today these anals would project out earnings 5 years from an applyer met a pricing multiple to that forward earnings but remember to get there you got to survive so you got to control for failure risk and finally be very careful about using Book value many declining firms will trade it below Book value because they deserve to traded below book book value why because you're in Decline you're often in businesses we're earning less than the than your cost of capital so your return on Capital being less than the con cost of capital will translate into a price being less than the book value you saying why not let's liquidate the company and get the book value back well good luck with that if you're a declining business it's unlikely you're going to get the book value B back so with declining firms it's easy to if you're lazy to find them cheap but you got to be careful to ask the word of questions so in terms of pricing declining companies you know many of the declining companies I said have will have book values that exceed their pricing but doesn't mean much because you can't earn your cost of capital some analysts use replacement cost which is what will it cost me to replace this declining company and if you're trading at less than that you argue for a cheap company but again if you're a declining company in a business where somebody else is taking over the business why would I want to replace your business in the first place the forward operating number again might offer you a way out but if you use it be careful you control for Fairly risk if you have a company with's a 40% chance of failure and you project out revenues 5 years from now earnings 5 years from now price it then and bring it back today and do not adjust for the failure risk the company is going to look cheap again so if I sound like I'm being you know I'm pushing back on finding declining company cheap it's because so many of them will look cheap but they deserve to be cheap now if you're pricing declining firms and you're trying to find a pure group and it be nice to find other declining firms right so brick and motor retail You could argue you can find enough declining brick and motor retail firms it's an opening but remember that the degree of decline can still vary across firms you can have all firms shrinking but some are shrinking faster closer to the precipice so you got to find a way to control for those differences in Decline across firms if you're comparing a declining firm to mostly healthy companies as I said on the surface your company can look cheap but you have to find ways again to control for the differences in health differences in margin difference and failure risk before you make that judgment and finally in controlling for differences across declining firms you have to control for differences in both growth and margins the fact that you have negative growth and negative margins will mean that you're going to get a lower pricing and the question you're asking is after I control for the lower growth and and the negative margins am I still cheap you have to control for Fairly risk and as know what you think about management can make make a big difference if you have Management in denial You could argue that you don't want to buy this declining company even if it looks really cheap because that management and denial will destroy more value going forward so the management can become an issue because it tells you whether the decline is going to lead to more value destruction or less value destruction in the future and that can make it and that can affect your pricing so let's look at a very generic pricing of Bed Bath and Beyond so I took Bed Bath and Beyond took the market cap and Enterprise Value and looked at that as a mult know a scaled revenues and here's what I me what I mean about companies looking cheap Bed Bath and Beyond trades at 0. 52 times revenues the median retail company trades at about 97 times revenues cheap right it's trading at about half the multiple but if you look at Revenue growth and and margin you can see why bed b bath and Beyond has much worse Revenue growth negative Revenue growth relative to the typical company in the business and much worse margins that's what I mean about declining companies often looking cheap 0.