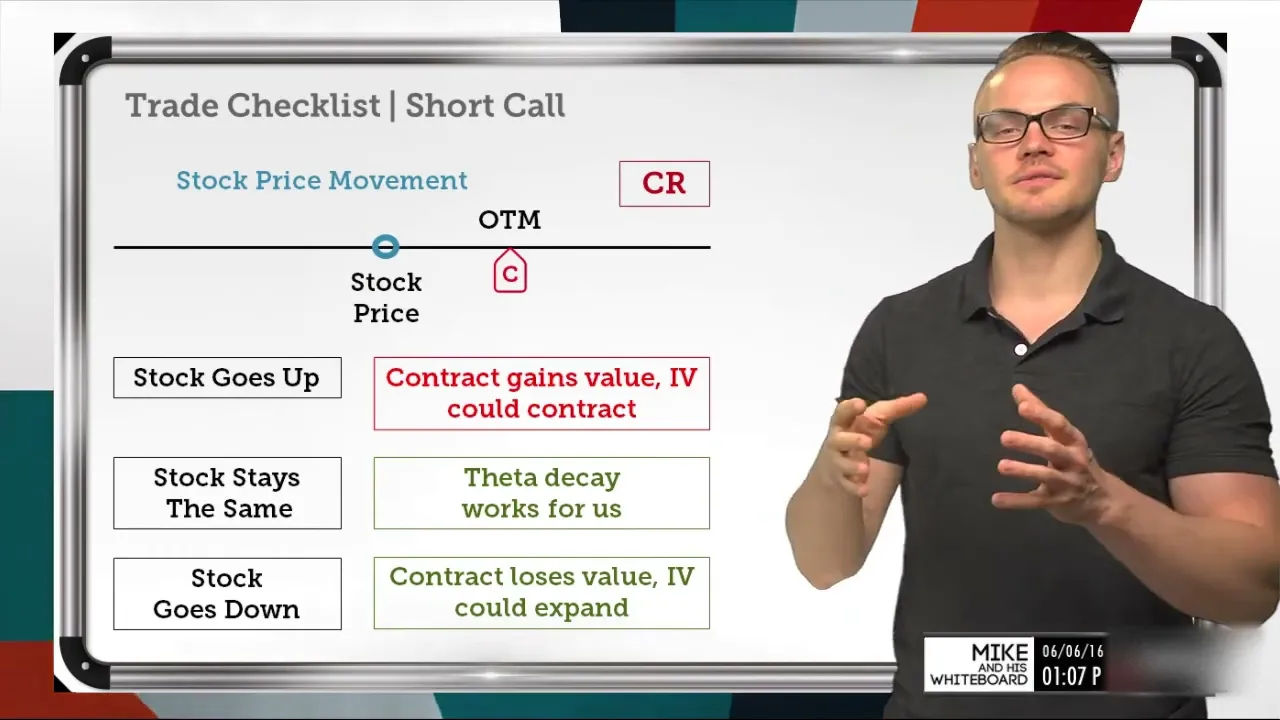

[Music] Hello everyone, welcome back to the show. My name is Mike, this is my whiteboard, and today we're covering the trade checklist for a short naked call. So, we're going to talk about the bearish assumption and really all the things that go into this strategy—what happens when the stock price goes up, stays the same, goes down, and a few others.

So, let's get right into it, and we'll go over a quick review of a short call and really discuss what a call contract is. When we're looking at a short call strategy, we're basically looking to sell an out-of-the-money short call. So, when we're looking at the call, we're going to be considering out-of-the-money options that are above the stock price.

Because if we review what a call contract really is, it's the right to buy shares at a certain strike price. So, if we're selling the call, we're actually on the other side of the transaction. We're basically selling the right for someone else to buy 100 shares of stock from us.

So, that would mean that the out-of-the-money options, where there's no intrinsic or real value, will be above the current stock price at which it's trading right now. This strategy is something that would be routed for a credit. When we're selling options, we're actually taking in cash; it's not profit just yet, but we are taking in cash because someone is buying that option from us.

So, we're selling that option, taking in cash, and the hope is that the option's value will decrease in price over time, which would allow us to buy it back for a lower price. This would result in profit: the net difference between where we sold it and where we can buy it back from. Or, more ideally, if we let it expire out of the money and worthless, that means the total credit that we received would be 100% profit at expiration, as that option would expire worthless as long as it stays out of the money and above the stock price for calls.

Our assumption here, since we want the stock price—or we want the option—to actually lose value for us to buy it back for a lower price, must mean that our assumption is neutral to bearish. Because if we want the option to stay out of the money, ideally we want the stock price to go down; but if it stays right here, that's totally fine, because we're going to have time on our side. If we remember, when people are buying option contracts, they need their contracts to be correct; they need to be directionally correct over that certain time frame.

Because at expiration, if they're not correct, it's going to expire out of the money and worthless, which would be good for us as the seller. So, for that reason, our assumption is neutral to bearish. Just like any other option selling strategy, we want to see a higher implied volatility environment.

When we're looking at implied volatility, it's really just a measure of where the option price action is right now. So, if implied volatility is high, that means that options are being bid up or they're being bought, which increases the price of those options. That's also going to increase the expected implied movement of that stock, which is why there's usually a lot of uncertainty tied to high implied volatility environments.

But all this really does is give us a much higher credit that we would receive when selling an option in a higher IV environment compared to selling it in a lower IV environment. So, if I was looking at this option that was five points out of the money—let's say the stock price is trading at $100, and I'm looking at selling the $105 call—in a low IV environment, maybe I can collect $2 or $1. 50 for it.

But in a high IV environment, maybe I can collect $3 or $3. 50 for it. Because of that uncertainty, the option prices are pumped up, which allows us to collect a lot more, increasing our probability of success and also increasing the amount of money that we can possibly make on that trade.

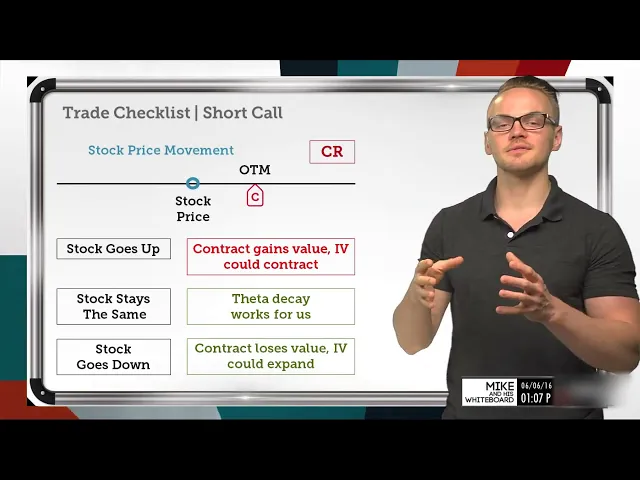

So, let's move on to the next slide and talk about what can happen with this strategy as the stock price moves. The worst-case scenario is highlighted in red here, and that's if the stock price goes up. As we've talked about, we want the call option to actually reduce in value.

So, if the stock price increases, that's going to actually be good for the call buyer, who is on the other side of this transaction, and for that reason, it's going to be bad for us. The contract would gain value, and IV could contract. So, these two factors sort of battle against each other: the contract will certainly gain value as the stock price rises, but IV contracts, which actually helps us as the seller.

Because if implied volatility is going down, that inherently means that the option prices are going down as well. Even though this is going to gain value because of the directional movement, we might see a little dissipation of the extrinsic value there, which is going to be good. So, these two factors hedge each other.

If the stock price stays the same, that's also going to be a good situation for us just because we have theta working for us, and theta is really just the decay of an option's price over time, assuming that implied volatility and the stock price are held constant. So, we're basically looking at freezing the entire market and then just moving one. all, we could still benefit from the decay in the extrinsic value of the option.

Now, let's summarize the main points comprehensively: The day ahead, whatever that theta value is, is the theoretical value that the option price should drop, given the assumption that we froze the market. Of course, we can't freeze the market, so theta is an interesting metric in that way, where it gives us a value, but it's not too practical because we can't freeze the market. However, over time, it does seem to show that it is pretty accurate.

So, when we're looking at the theta decay working for us as option sellers, that's always good when we see no movement, or maybe a slight movement in the market, and a couple of days have gone by. Because usually, that means that the option price will be worth less than it was before, which is obviously going to be good for us as sellers. We're looking at selling it up here, and every single day that goes by, it's going to decrease that price, hopefully.

So, if that happens, where the stock price stays the same over time, we should see the option lose value. But at expiration, the option is going to be worthless. As long as this stays out of the money or above the current stock price, that's going to be good for us.

We can hope to see the stock price stay right here, and over time, we'll be able to either buy that back for a lower price or let it expire worthless and keep that entire credit that we received as full profit. Lastly, the stock going down is really what we want to see when we're selling a short call. The contract is going to lose value because it's going to be further out of the money.

If it's further out of the money, it's going to have a lower probability of being in the money, which means that the value of that option is going to be reduced. However, one thing that's interesting about the stock going down is that we usually see implied volatility expand when we see downward movements in the market or downward movements in a specific underlying. That’s what's interesting about selling a call.

We will definitely have the ability to make some money if the stock price goes down, but if implied volatility expands, that could actually battle against our profitability. If implied volatility is expanding, that's increasing the extrinsic value of that option price. Consequently, we might see a good directional move to the downside, but we might not see as much profit as we might think.

If implied volatility expands way out of our minds, and we actually see a huge implied volatility expansion in some cases, if the stock price moves down just a little bit and implied volatility expands even more than the movement would imply, then we might actually see no change in the P&L there. It's really interesting how short calls work, but because of that, it is more of a natural hedge against certain things. If I've got short calls in SPY, it's a natural hedge against itself because if the underlying moves down, we would be directionally correct here, and if the underlying moves down, we're going to see usually an increase in implied volatility.

So, they kind of work against each other, but there are a few things that I want to talk about. Let's discuss those things on the very next slide. The very first thing that we always harp on is calculating the break-even point.

With a short call, when we're looking at calculating the break-even, we always have to remember that when we're selling premium, our breakevens are going to be improved in our favor. What does that mean for a short call? Well, for a short call, that would mean that my breakeven would be improved to the upside.

All I need to do to calculate a breakeven is look at my short strike and add the credit received. For example, if the stock price is at 100 and I'm selling a 105 call, if I sold that call for two dollars, my break-even would be improved to 107. That's just two points to the upside because at expiration, if my call is actually in the money by two points and the stock price is at 107, I'm going to have to buy back this call for two dollars, which is the intrinsic value it would have.

Since I sold it for two dollars, that completely wipes out that cost that I have to pay to buy it back, which is why my break-even would be zero at that point. Again, the IV factor when we're selling premium: the higher the IV, the better. Not only because we're going to be able to collect a lot more for that same strike, but it also gives us another chance of being correct.

We talked about the stock price movement and how it impacts implied volatility, but when we sell something in a high IV environment where implied volatility has expanded, we actually give ourselves another dimension to be hopefully correct. If I sell an option in a very high IV environment where there's a lot of premium out here in this strike, if implied volatility contracts, so will the probabilities on this strike curve. If I sold an option here, and it had a ton of implied volatility and gave me a lot of value, if implied volatility contracted and got really small, then the option price would decrease as well.

So even if the stock price didn't move at all, we could still benefit from the decay in the extrinsic value of the option. All implied volatility just contracted. If you look at something like an earnings announcement, where implied volatility usually expands and then, after the announcement, it tends to contract, we would be able to see a nice profit, usually in that situation, even if the stock price didn't move at all.

For that reason, when we look at selling premium in high IV, we actually give ourselves another way to be correct. We give ourselves another dimension because now we're playing that short volatility aspect as well. When we're looking at closing this, we are looking at closing it at about a 50% max profit, just like any other option selling strategy that we use.

That's because we are only able to collect and profit by the amount of credit we received. In this example, if I received two dollars in credit for this short call, if I can close it out and capture and lock in that 100% credit or 100% profit by buying this option back for one dollar—which is really where I'm at when I'm at 50% profit—what have I got to lose? Well, I'm basically locking in 100%, which is great, and I'm leaving 100% on the table.

But when you think about it, if I already have 100 dollars and the most I can make now is only a hundred dollars more, but I'm holding all of the risk, it makes perfect sense to manage it at 50%, which is why we do that. Exactly. The more profit we see in an unrealized situation, where we still have all the risk, the more it looks like we're holding a lot more risk than the potential reward will give us for doing so.

So, that's why we look to manage our profit at 50%, close out the trade, and lock in that profit to give ourselves a win on the board. Now, let's wrap all this together with some takeaways for you. The very first takeaway we've got is that this is a neutral to bearish cost basis reduction strategy.

If I were to imagine that I actually had 100 shares of stock and I was selling a call against it to reduce my cost basis, it's very much the same thing when I'm selling a call. Because when I'm selling a call, it's actually the opposite assumption; I'm actually bearish on the underlying. Instead of buying a put, which would actually hurt my cost basis because I would need that underlying to move in a certain way, selling a call actually gives me a way to be profitable.

Even if the stock price rises—which would be bad for this position—it gives me an opportunity to become short that stock at a much better price than if I were to have just shorted the stock from the very beginning. What I really want to harp on is the undefined risk aspect of a short call. When we talk about undefined risk, it really rings true with a short call because there isn't a cap to where a stock can go.

If you look at some of the underlyings like Amazon or Priceline, they all started somewhere, and now they're very high-priced, high-valued stocks. So, when we're looking at a short call, there is no cap to the upside. If I was looking at a short put, however, no stock can go below zero, so my undefined risk is actually really capped at the stock price if it goes to zero.

But with short calls, there's no cap to the upside, so when we're dealing with a strategy like this, the risk is truly undefined. So definitely be aware of that. We can defensively roll the strategy if our strike is tested, and I'm actually going to cover that tomorrow.

If you're interested in three adjustments that I would make with a short call, I'm going to be covering that tomorrow, Tuesday the 7th. Thanks so much for tuning in. If you've got any questions or feedback, shoot me an email here, or you can follow me at Doe Trader Mike.

Stay tuned, though; we've got Jim Schultz coming up next!