within a week of being paid all the money's gone you still have bills to pay you've scraped and pinched everywhere you can but there's just not enough to cover what you need with nothing in savings no credit cards utilizing poor credit What alternative do you have should you visit the dreaded payday lender [Music] payday loans also called cash advance loans are advertised as a short-term relief when you're in a financial bind they are meant to be for small amounts usually up to five hundred dollars which the consumer intends to repay with their next paycheck to

some it may seem enticing to go this route for starters the application process is pretty simple only requiring an ID proof of income and a bank account once the process is finalized you can get your money the same day sounds attractive but to see the real cost we'll have to run the numbers Paula has a full-time job as a server in a restaurant but a bout of covid forced her to miss several shifts coupled with the recent increase in gas prices she's found she doesn't have enough for this month's rent with the moratorium on evictions

lapsed in her State she doesn't want to do anything to aggravate the landlord so she considers taking out a payday loan it's just 500 she thinks I should be able to pay that off she completes the application online presents the required documents and the funds are deposited into our bank account within 24 hours crisis averted or has it just begun obtaining a payday loan is easy but the interest rates are high really high like Woody Harrelson High Paula's lender charges twenty dollars for every hundred dollars borrowed over a 14-day term that's an annual percentage rate

of around 500 percent after another lackluster couple of weeks at work Paula unfortunately only has a hundred and fifty dollars left over far from the six hundred dollars she now owes when the lender tries to automatically deduct it from her account it triggers a 35 overdraft fee from her bank if she pays the 100 of interest on the loan the lender will graciously allow her to roll over the debt for another two weeks Paula has already paid 135 dollars in fees and interest and she's not one inch closer to paying back the loan it's estimated

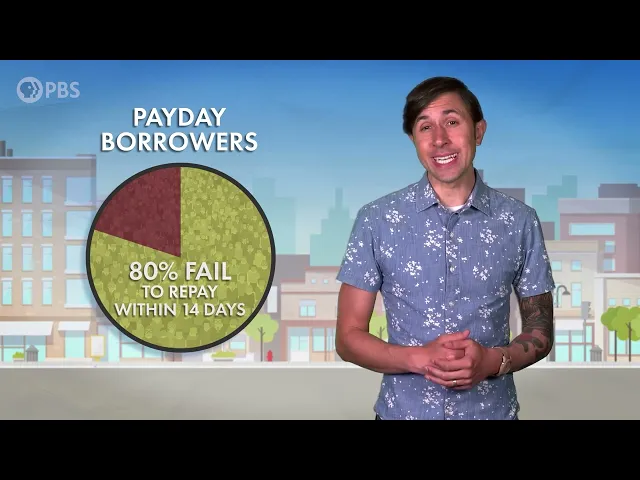

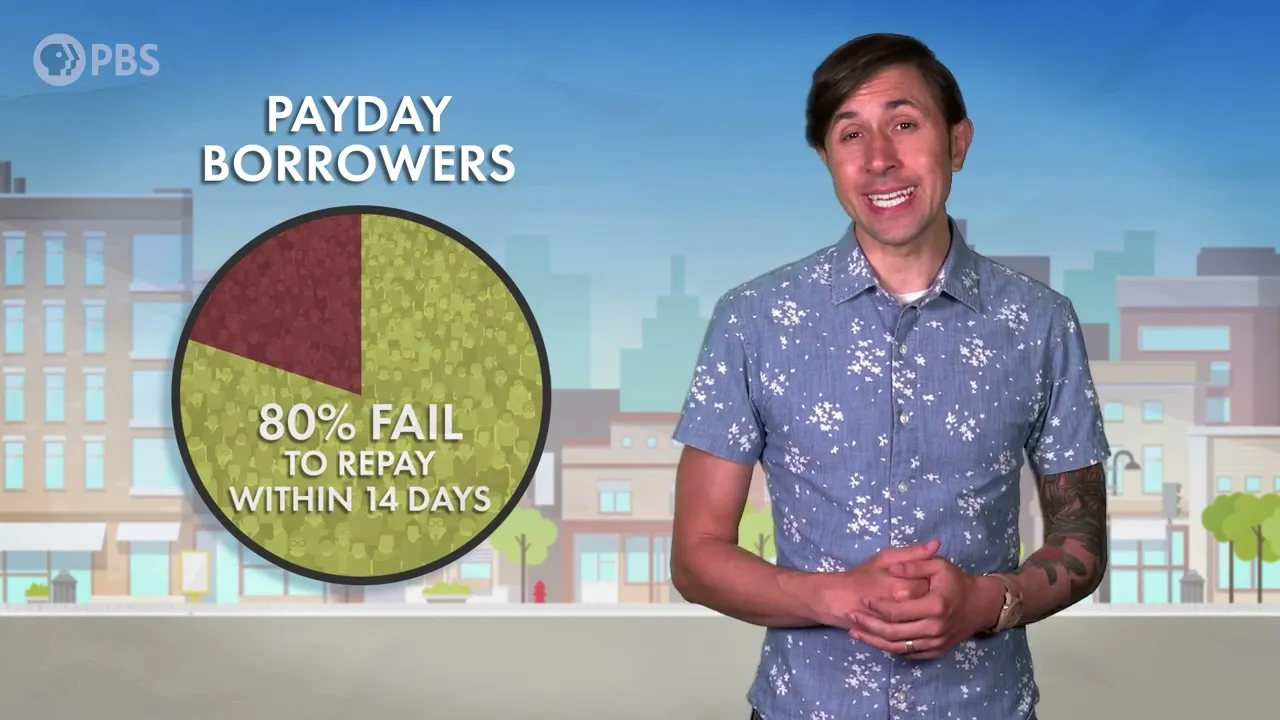

by the Consumer Financial Protection Bureau that 80 percent of payday borrowers fail to pay back the loan in full within the 14-day term and that the average loan of 375 dollars takes an average of five months to pay back by which time the total cost is around a thousand dollars That's not including any late fees or overdraft fees or Banks or credit unions may have charged them payday loans are considered predatory for two main reasons their High interest rates and the fact that they do not practice underwriting underwriting is the process of an investigating a

prospective borrower's finances to verify whether they will be able to pay back the loan if you've ever applied for a mortgage or a credit card you've gone through it but many payday lenders don't bother with underwriting it's almost as if they want customers who won't be able to pay back the loan so that they can track them in a never-ending nightmare of fees and interest in 2017 the cfpb issued a mandatory underwriting rule that would compel payday lenders to check whether a borrower could handle a loan before issuing it however the rule was revoked in

2020 under the Trump Administration after five months Paula has paid close to a thousand dollars in interest and fees without even making a dent in the original 500 loan she's starting to realize that this short-term solution has become a long-term problem so what can she do assuming she's exhausted her options for scrounging up extra cash she could borrow more money like taking out a personal loan from our credit union or paying off the loan with a credit card but most people who resort to Payday Loans do so because they can't qualify for other types of

credit or have already maxed out their cards Paula considers defaulting on the loan after all her credit score is already in the dumps but if she thinks the lender will let her off the hook she's dead wrong payday lenders will refer to delinquent borrowers to collection agencies and even take them to court over sums as small as a few hundred dollars they can put a lien on your house or garnish your wages there is of course the b word bankruptcy but before she considers that option Paula should contact the lender directly and try to negotiate

a settlement lenders would almost always rather get the money directly from the borrower than sell the debt to a collections agency and they're often willing to settle for as little as half the full amount especially if Paula mentions that she's considering declaring bankruptcy and in which case they'd get nothing even if Paula makes it out of this Jam she'll undoubtedly wish that she'd never gotten into it in the first place payday loans are almost always a bad idea if you need cash fast sell some possessions pick up extra work borrow from friends and family even

take out a new credit card almost anything else you can do that's legal is preferable to a payday loan of course keeping a strict budget and having an emergency fund can protect you from even being in such a vulnerable position listen we may all find ourselves in a financial bind at some point and borrowing money can be a lifesaver when unexpected crises arrive but you have to make sure that what you're swimming toward is an actual Lifesaver and not a shark in Disguise and that's our two cents before you go we want you to know

about an incredibly important new digital series from PBS facing suicide shines a light on the power of friends and family during and after a mental health crisis here from suicide attempt survivors their Journeys and explore the healing found in sharing your story with a group of peers click the link in our description to watch it now and we hope it can inspire you or someone you know thanks to our patrons for keeping two cents financially healthy click the link in the description to become a two cents Patron [Music] thank you