I have a feel there he is let's go to the Fed chair Affairs Council to the Federal Reserve Bank of Dallas and to the Dallas Regional Chamber for the kind invitation to be with you today I have just a few brief comments on the economy and monetary policy before we uh move to our conversation so looking back the US economy has weathered a global pandemic in its aftermath and is now back to a good place the economy has made significant progress toward our dual mandate goals of Maximum employment and stable prices the labor market remains

in solid condition inflation has eased substantially from its peak and we believe it is on a sustainable path to our 2% goal we are committed to maintaining our economy's strength by returning inflation to our goal while supporting maximum employment the recent performance of our economy has been remarkably good by far the best of any major economy in the world economic output grew by more than 3% last year and is expanding at a stout 2.5% rate so far this year growth in consumer spending has remained strong supported by increases in disposable income and solid household balance

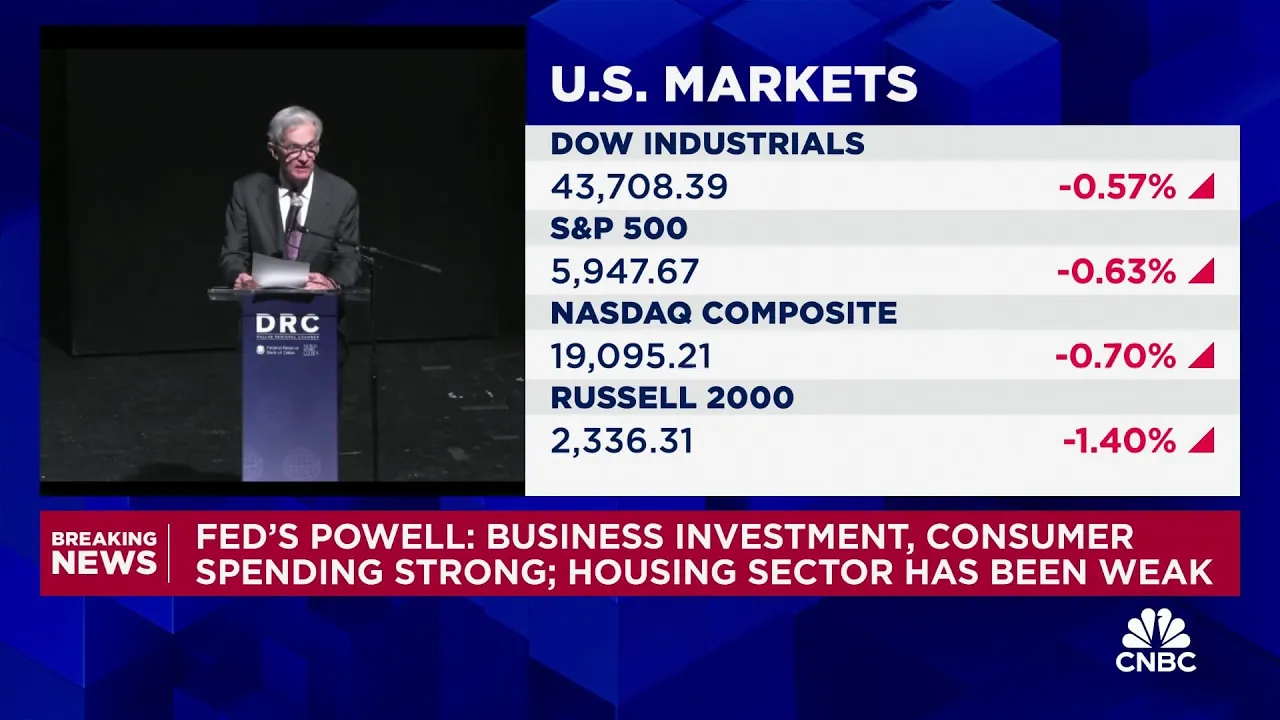

sheets business investment in equipment and intangibles has accelerated over the past year in contrast activity in the housing sector has been weak improving Supply conditions have supported the strong performance of the economy the labor force has expanded rapidly and productivity has grown faster over the past 5 years than its Pace in the two two decades before the pandemic increasing the productive capacity of the economy and allowing rapid economic growth without overheating the labor market remains in solid condition having cooled off from the significantly overheated conditions of a couple of years ago and is now by

many metrics back to more normal levels that are consistent with our employment mandate the number of job openings is now just slightly above the number of unemployed Americans seeking work the rate at which workers quit their jobs is below the prepandemic pace after touching historic highs two years ago wages are still increasing but at a more sustainable pace and hiring has slowed from earlier in the year the most recent jobs report for October reflected significant effects from hurricanes and labor strikes making it difficult to get a clear signal finally at 4.1% the unemployment rate is

notably higher than a year ago but has flattened out in recent months and remains historically low turning to inflation the labor market has cooled to the point where it is no longer a source of sign significant inflationary pressures this Cooling and the substantial Improvement in broader Supply conditions have brought inflation down significantly over the past 2 years from its mid2 22 Peak above 7% progress on inflation has been broad-based estimates based on the Consumer Price Index and other data released this week indicate that total pce Prices rose 2.3% over the 12 months ending in October

and that excluding the volatile food and energy categories core pce prices Rose 2.8% core measures of goods and services inflation excluding housing fell rap ly over the past 2 years and have returned to rates closer to those consistent with our goals we expect that these rates will continue to fluctuate in their recent ranges and we're watching carefully to be sure that they do however just as we are closely tracking the gradual decline in Housing Services inflation which has yet to fully normalize inflation is running much closer to our 2% goal but it's not there yet

and we are committed to finishing the job with labor market conditions in rough balance and inflation expectations well anchored I expect inflation to continue to come down toward our 2% objective albeit on a sometimes bumpy path given progress toward our inflation goal in the cooling of labor market conditions last week my Federal Open Market Committee colleagues and I took another step in reducing the degree of policy restraint by lowering our policy interest rate by a quarter percentage point we're confident that with an appropriate recalibration of our policy stance strength in the economy and the labor

market can be maintained with inflation moving sustainably down to 2% we see the risks to achieving our employment and inflation goals as being roughly imbalance and we are attentive to the risks to both sides we know that reducing policy restraint too quickly could hinder progress on inflation at the same time reducing policy restraint too slowly could unduly weaken economic activity and employment we're moving policy over time to a more normal setting but the path for getting there is not preset and considering additional adjustments to the target range for the federal funds rate we will carefully

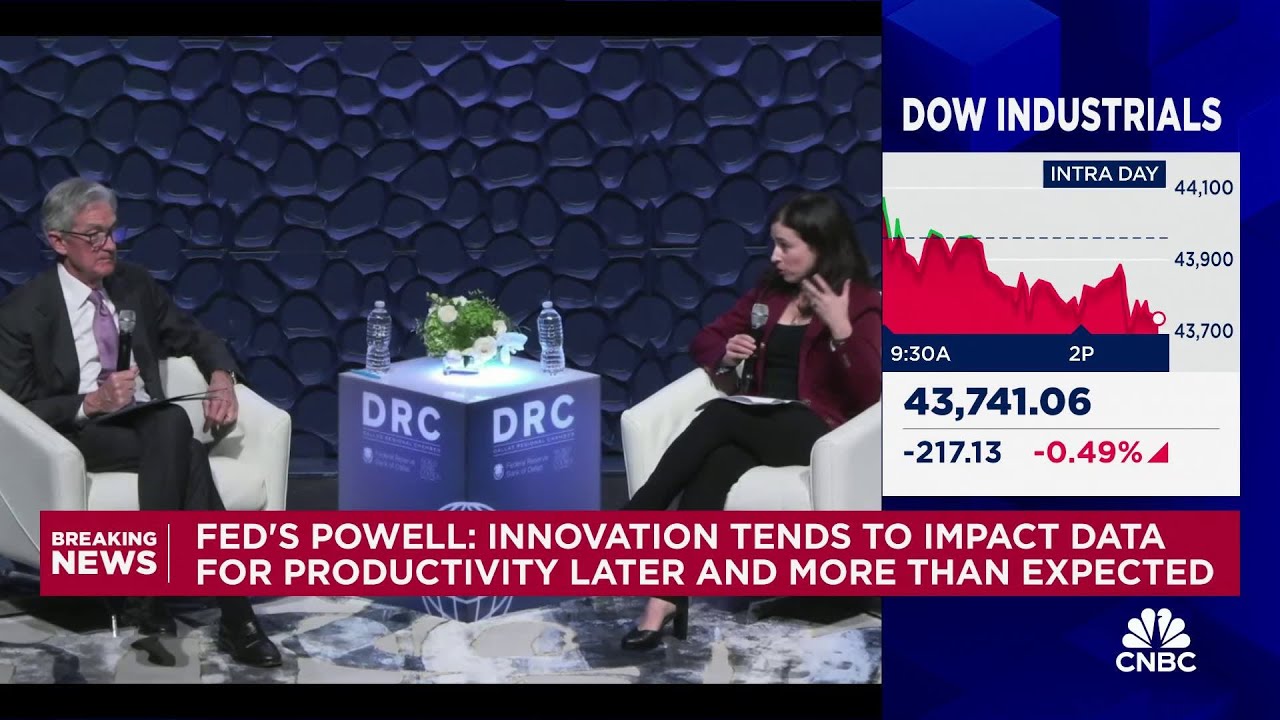

assess incoming data the evolving Outlook and the balance of risks the economy is not sending any signals that we need to be in a hurry to lower rates the strength we're currently seeing in the economy gives us the ability to approach our decisions carefully ultimately the path of the policy rate will depend on how the incoming data and the economic Outlook evolve we remain Resolute in our commitment to the Dual mandate given to us by Congress maximum employment and price stability our aim has been to return inflation to our objective without the kind of painful

rise in unemployment that has often accompanied past efforts to bring down high inflation that would be a highly desirable result for the communities families and businesses we serve while the task is not not complete we've made a good deal of progress toward that outcome thank you very much and I look forward to our discussion