Welcome students. In the last lecture we learnt that how to prepare the ledger accounts, post the journals, which are recorded in the; post the transactions which are recorded in the journal to the ledger. So, we learnt that how to post them in the ledger prepared by the individual.

Ledger accounts for each and every account and balance them. Now, from those ledger accounts or drawing the balance sheet from the ledger account, we will have to prepare the financial statements, important financial statements. First, we will prepare the two financial statements.

That is, the trading and profit and loss account. And, second is the balance sheet. And, from the balance sheet we will prepare third statement.

That is the cash flow statement. Cash flow statement is basically comes under the analysis of the financial statements, especially the analysis of balance sheet. But that is the job we will do later on.

As I told you that directly from the ledger you cannot prepare the profit and loss account or balance sheet. These are the financial statement. You have to prepare one intervening statement.

That statement is called as the trial balance. And, trial balance is basically as I told you earlier also that it is a account which verifies that whatever transactions have been recorded in the journal and whatever the amount has been posted in the ledger, they are arithmetically correct, numerically correct. And, balances extracted out of these ledger accounts are also correct.

So, from these balances in the ledger we will have to prepare that intervening statement and that intervening statement is called as the trial balance. . So, trial balance format is little different and it is very simple.

So, here you have the first column, then you have the second column, then you have two more columns here. And, this is going to be a complete format. It is going to be a complete format.

So, here you have this is called as the trial balance. T r i a l balance b a l a n c e. This is the trial balance.

B a l a n c e. This is the trial balance. So, we will be preparing the intervening statement.

These columns; first is the serial number, this is for head of account; this column is for head of account. And, this is the column for balance; those balance which we have calculated in the ledger. And, this is the column for debit balance.

And, this is the column for Cr is the credit balance. This is for credit balance, Cr; credit balance. So, we will have to put the serial number and head of account and the balances.

And then, see that after when we put all the balances at the right place, total of this column should be equal to the total of this column. The total of both the columns should be correct. Now, for my convenience I have put all these balances on a paper because I have not, I do not have the record here.

So, I have put it on all these accounts and their balances on a paper. You also have recorded it or you know it that what are the balances of those transactions, which were posted to the ledger. So, I will be taking it from here.

So, first account we prepared was that was the cash account. So, it is one, it is cash account. And, the balance of the cash account was 29,650.

And, it is the debit balance. It was the debit balance because debit side of the cash account was bigger side. So, the balance is known by the side which is bigger, so cash account had a debit balance.

Now, we have; second account we had was capital account. And, the balance of the capital account was 50,000 rupees, but a credit balance. This is 50,000 rupees, but a credit balance.

Now, we go for the next account. And, the next account is the furniture account. So, furniture account is having again a debit balance because debit side is bigger.

So, it is furniture account is 500 rupees. Now, we have the fourth account. And that was the sales account.

This account is the sales account and the sales account is having a credit balance of 24,000. So, it is, the 24,000 rupees is the sales balance account; which is 24,000 rupees. So, we have taken it here.

Now, we take the next one that is a Naresh Kumar’s account. Naresh Kumar account has no balance. It is balanced.

Total sales made to him were 8,000 rupees and he has paid 7,600. 400, this firm has given discount. Beta has given discount to him.

So, this account has no balance. It is balanced account. Then, we talk about the next account.

And that is a Vinod Kumar’s account. So, Vinod Kumar’s account balance is; Vinod Kumar and Vinod Kumar’s account. Vinod Kumar’s account and its balance is; Vinod Kumar’s accounts balance is how much?

This balance is credit balance for 2,500 rupees. This is the Vinod Kumar account. Now, we have the next account, that is, Raja’s account, Raja’s account.

And, Raja’s account has a balance of; you call it as debit balance of 6000 rupees. So, it is a debit balance of 6000 rupees. Now, we have stationery account.

Next account is stationary account. Stationary account also has a debit balance of 250 rupees. Then, we have the next account that is like office rent account.

So, it is office rent account. And, the amount of the office rent account is 800 rupees. This is 800 rupees.

Then, we have next is the purchase return account, purchase return account. And, purchase return account has a credit balance of 500 rupees; credit balance of 500 rupees. And then, finally we have; tenth account, we have is discount account.

So, it means discount account's balance is 300 rupees. So, I think all the balances we have put here. We have taken them here.

And, if you think about, then there is no balance which is left I think. Or, some balance is left? Yes, one balance is left.

I think it is a purchase account. Yes, this is the eleventh account is the purchase account. So, cash capital furniture sales Vinod Kumar, Raja purchase account, we had forgotten.

So, you put here the purchase account. This is called as the purchase account. And, purchase account's balance is debit balance of 35,000 rupees.

This is of 35,000 rupees. So, we have taken almost all the balances here. And, if you total it up; so, it means you will find total of debit and credit balances is equal; that is, 50000, 24000 and 74,000 then plus 3, 77,000.

And, total of this side is also I think 77,000, 29, 35, 650, then it is 36, 150, then it is 36, 400, 37, 200. and then it is 37, 500 and then 35. So, it is 29,650.

35,000 done. 500 done, then it is 6000 is done. Then we have 250.

Yes, 800 is there and 300 is there. So, if you take, make the total of this side, I think this is also equal to 7700. 5 and 5 is 0, 1; 6, 7, 12.

Then it is 14. 14 and 8 is 22, 25. And, it is the same balance.

So, it is, if you look at the total of 29,000, cash balance is 29,650. Then, we have the purchase account, 35,000. Then, we have this furniture account; that is, I think we are missing.

Furniture account is. So, balance of furniture account is; now this we are committing. Look, we are committing a mistake, it is 5,000.

So, balance of the furniture account is 5000, not 500. And then, we have Raja’s account 6000. Then, we have stationery account 250, office rent account 800, then we have this account.

So, total of this side is 77,000. So, both the sides are equal. So, you can say that whatever the transactions recorded in the journal, posted in the ledger, they are arithmetically correct.

There is no mistake in this. And, we have done. Whatever is done that is correctly done here.

So, it means this statement is the proof of arithmetical accuracy of transactions recorded in journal and posted in the ledger. Now, here arises one question. For example, as I have done it, you have seen it I have done it wrongfully that we have, I had made it 500.

Normally, the value, actual value is 5000 rupees. But, I had wrongly put it here as the 500 rupees. It may be possible that I have, I may or anybody else can do in the journal also that rather than 500 rupees in the one side, you put 5000 and on the other side you put 500 rupees.

So, that difference of the 4,500 will appear. For example, this trial balance does not tally. And, we have to anyway prepare the financial statements on the last day of the accounting period.

And, if this trial balance is not tallying, so can we proceed further to prepare the profit and loss account and balance sheet that is the two financial statements with the incorrect trial balance? Is it possible? Yes, it is possible.

. For example, it is not tallying, say for example, the we have, we have some problem here. And, we have put here that rather than 300 rupees, the balance of discount account is working out as 3000 rupees.

So, if you look at this side, this side will be more by 2,700 rupees. This will be bigger. So, the total of this side will be 79,700 rupees.

And, this will be 77,000 rupees. So, there will be a problem. So, what will happen that we will put; this means, here this side is now coming out as 77,000, 79,000.

This side is will be 79,000; this side will become as I have made it. . So, this balance, for example, has come out as 3000, instead of 300 rupees.

So, this side will become now 79,700; 79,700. So, I am putting this side is this; so this balance of 27,000 rupees. So, what will we do?

We will extend this statement and we will make one more. So, this way we will extend this account. And, now we will, when we extend this account what you will get?

We will put one item here, which is called as suspense account. So, total of this side is 79,700 and total of this side is 77,000. So, you will put here 2,700 rupees more; suspense account.

And, now the total of both sides will be 79,700. And, it will be 79,700. So, it is tallying now.

So, we will temporarily prepare the profit and loss account and balance sheet by using this figure as; means making using this balance as 79,700, and putting that difference amount of 2,700 rupees under suspense account. We will prepare the profit and loss account. We will prepare the balance sheet.

And, once that everything is done, then we will have to look back. We will have to find out why this balance of difference of 2,700 rupees is appearing in the trial balance. It means something has happened either in the journal or in the ledger.

Something has happened, and because of that this trial balance is not tallying. So, or may be it has happened here only. That I have put this balance of rather than 3000 rupees, I have 300 rupees.

I have made it 3000 rupees. So, this balance is appearing. So, what I will do?

I will have to do this correction. I will find it out that the actual balance of the discount account is 300 rupees. I have to do this correction.

So, I will make it 300 rupees. Automatically, the balance of this account will become 77,000 rupees now. And, both the sides will be having the same balance of 77,000 rupees.

This is also the 77,000 rupees. So, both the sides will be 77,000 rupees. And, I will remove this suspense account now.

And, wherever the corrections are required, I must have shown this balance in the profit and loss account as 3000 rupees. The balance of the discount account in the debit side of profit and loss account, I must have shown that is 3000 rupees. So, I will make a correction there.

I will make it 300 rupees so that the actual amount is 300 rupees. And I will see; what is impact of that in the profit and loss account and I will correct the profit and loss account. So, actual is 300 rupees, not 3,000 rupees.

And, but we will not wait till the trial balance is not tallying. We will put that amount or difference in the another account called as the suspense account and we will prepare the profit and loss account and balance sheet on the due date. And after that due date, we will get the time.

And during that time, we will correct this mistake, this error and we will calculate the real profit or loss and the real balance. In the balance sheet, we will put the real balances in the balance sheet. And, everything has to be arithmetically correct.

So, if any error occurs and trial balance does not tally, put the balance in the suspense account for the time being. And then, after the date of the balance sheet, you re-do the whole; means the whole thing. And, try to find out the error and you correct your profit and loss account and balance sheet that can be done.

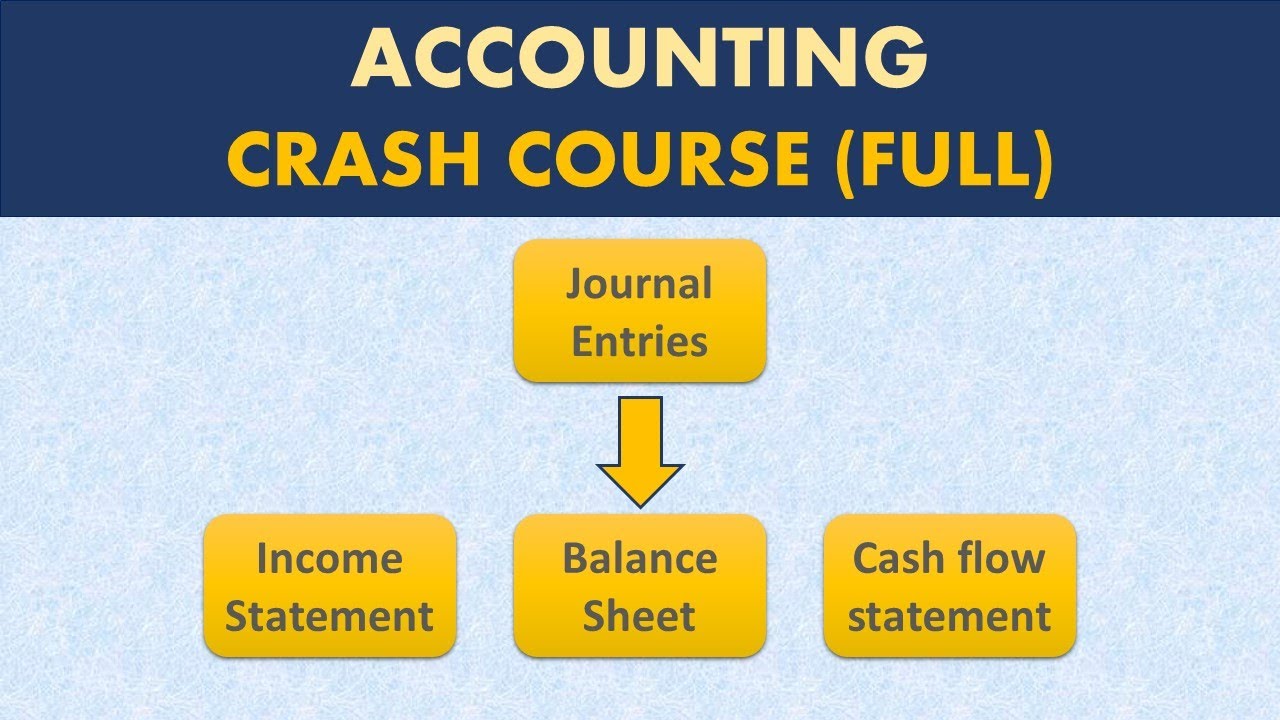

So, this is we have completed three steps so far in the process of preparing the financial statement. That is the profit and loss account and the balance sheet. Now, means, we learnt how to record the first was the transaction in the accounting process; the first step was the transaction, second was the journal, the third was the ledger, fourth one was preparing the trial balance.

And, from the trial balance we will have to now move forward to prepare the profit and loss account and balance sheet. If the trial balance tallies and if it is correct, then we can easily prepare the profit and loss account and balance sheet. There is no problem as such and it can be easily done.

So, these balances can be taken to the profit and loss account and balance sheet. But, since they are not complete balances, both the sides are not complete. So, we will not be able to prepare the correct profit and loss account from this information.

So, for preparing the profit and loss account and balance sheet, we will now take the help of another problem, another illustration. And, this is an illustration where this information we will use and we will have to prepare now the profit and loss account. The first statement that is the trading and profit and loss account.

Out of this information, these balances, this is a kind of a trial balance. The balances are extracted out here. So, we will have to use these balances.

And, by using these balances we will prepare that. We have learnt how to move forward in preparing the financial statements. So, now let us move forward in preparing the financial statements.

That is the next step. That once we have learnt that how to prepare the trial balance, then preparing the financial statements is not difficult. We can easily do it.

And, we can learn because analysis of the financial statements requires, first of all that how to prepare the financial statements. And, if you know that how to prepare the financial statements, you can easily read those financial statements and analyzing these financial statements will not be difficult at all. So, it means we have learnt so far that what are the different steps involved.

We have completed the four steps; that is transaction, journal, ledger and trial balance. Now, we will proceed further for preparing the financial statements. And, the first statement as I told you in my some of the previous lectures was trading and profit and loss account.

And, the second is the balance sheet and third one is again now has become a statutory, it is the part of financial analysis. But that has become a statutory statement; that is called as a cash flow statement. So, we will learn how to prepare all the three statements.

. So, first statement is the trading and profit and loss account. And, as we have seen in some previous lectures the format.

The format of trading and profit and loss account is again same. Again it is a ‘T format’ kind of. It is a kind of a ledger account format, but very simple.

And, we have columns here like or you can say that these two columns on the one side and two columns on the other side. So, this is here, and then this is here. So, we are now learning how to prepare the financial statements.

So, first statement is the trading and profit and loss account. So, here look at this information now. Here, we are asked financial statements problem one.

We are asked a certain gross profit and net profit from the following balances extracted from the books of Alfa associates. Alfa associates may be a sole proprietor organization. So, there is a difference in preparation of the accounts of the sole proprietor, single owner organizations, partnership firms and the company form of organizations.

Step by step we will learn how to prepare the financial statements of the sole proprietors, partnership firms and then the company form of organizations. So, now this is the sole proprietorship. And, for this sole proprietor we will have to calculate the gross profit and the net profit.

And, this is the job of this statement. Whereby preparing trading and profit and loss account, we can get to know; what is the gross profit of this organization, what is the net profit of this organization and trading and profit and loss account statements helps us to know the status of gross profit and net profit. First of all, you write here the title, ‘Trading and Profit and Loss account of Alfa Associates’ of Alfa associates.

If some period is given, then we will write here. Normally, it is for one year. For the year ending on, the date is given here.

So, it is ‘Trading and Profit and Loss account of Alfa Associates for the year ending on so and so’. Since, it depicts the profit or loss of the firm for a period of complete one year. So, we have simple columns here like particulars.

Then, we have the amount. Again it is the particulars, and then it is amount, this column is known as the debit column amount. And, this column is known as the credit column amount.

. Particulars amount debit; particulars amount credit. So, this, on the other hand you will say this is the expense side of the firm.

All the expenses will be recorded on debit side; all the incomes will be recorded on the credit side. And then, balance. If the income is more than the expense, then the difference will be the gross profit, if the expense is more than the income, then the gross loss.

And then, we will move forward to prepare the second part; profit and loss account. So, here in the trading account, we take the incomes here. And, the incomes in the trading account are coming from the two sources.

One is the sales; that normally whatever the firm is producing. That is, they are selling in the market. And, from the sales we are having the incomes.

So, you will write sales. And, if some closing stock is left, some part of the sales for example, if it is given here, if the part of sales are unsold in the market, they will be sold in the future period. So, that amount will also come to us.

So, total of these we will write here. But, we will write here, items this side will be denoted by ‘By’; item this side will be denoted by ‘To’. So, you will write start here.

First of all, we will put all the expenses here. . So we will see; what are the direct expenses.

We say that first of all here it is given here something like opening stock. Opening stock is just normally for the raw material. So, we will take only three items here.

First is to opening stock of raw material; to opening stock of raw material. And, this opening stock of the raw material is 24,000 rupees. Then, second item is to purchases of the raw material.

Here also given ‘To purchases’; to purchases. Only we write ‘To purchases’. This is 91,300 rupees.

Then, we have next item is wages. ‘To wages’; that is, 18,100. And, any other direct item here?

Yes, we have the factory rent. So, ‘To factory rent’. ‘To factory rent’.

Factory rent is 3000 rupees. Good. Take factory rent is 3000 rupees.

Then, we have freight on purchases. You can write here ‘To freight on purchases’; freight on purchases. And, the freight on purchases here is 3000 rupees; any other item?

No. Any other purchase returns are also there; so salaries, general expenses, discount and discount. So, here you have to make one correction.

That is, opening stock of raw materials to purchases is 91,000. But, since we have the purchase returns also, so this will be written in the inner column; that is 91,300. And then, you have to adjust for the purchase returns.

Part of the purchase is what we purchased is returned. So, you write here less. It is ‘Less purchase returns’; P/R.

You can write purchase return, that is, 4000 rupees. So, they are goods worth of 4000 rupees. They are written.

So, it is 87,300 rupees purchases are used in the firm. I think there is no other direct expense. And, now it is the direct incomes.

This is ‘By sales’. So, sales, we have sales amount is, that is, sales amount is given to us top; 160,000. Put it in the inner column, less.

A sales return; as we have returned the purchases, somebody else is returning back to Alfa associates some sales; sales returns. And, sales returns are 5000 rupees. So, this is final amount of the sales is 1,55,000 rupees.

Then, we have to take the closing stock here. ‘By closing stock’; by closing stock’ here; if you take the closing stock, then it is 22,100. 22,100.

And, other items we will not take in the trading account. So, we have taken the sales, purchase, wage, factory, rent, office, freight. Freight on sales is also there.

They have taken freight on purchase is 3000 rupees. Freight on sales, we will take in profit and loss account, opening stock, closing stock, purchase returns, sale returns, salaries, general expenses, discounts and discounts to customers. So, it is discount from creditors and discount to customers.

So, it means these are the only items of the upper part of the profit and loss account. That is of the trading account. So, we will total it up.

So, this side becomes as normally this side should be bigger. So, it is 001. It is 7.

It is 7. So, it is 1,77,100 rupees. I think this side is bigger.

So, 1,77,100. 1,77,100. Now, the difference we will see.

We will have to total it up on a different paper. So, this becomes 24,000; if you total it up, 24,000, then 87,300. Then, it is 18,100.

And then, it is 3000. And then, it is again 3000. So, total of this side becomes 00.

It is 4. This is 11, 5 2 4, 1,35,400. If I am correct, it is 0 0 3 4, 3 and 3 is 6, 8 is 14, 7 is 21, 4, 25, 2 4; 1,35,400.

So, the total of the credit side is 1,77,100. And, total of the debit side is 1,35,400. So, it means you have to subtract it; this 000, this 7, this is 1, then it is 4.

So, 41,700 is the gross profit. Profit depicted by the trading account is the gross profit. This is not the net profit.

So, this is the gross profit. And, the gross profit here is 41,700. Now, you must have a question that out of the total items given here, why I have taken only a few items?

One, two, three here and one, two, three, four, five, six and seven items this side, why I have left out the other items. So, it means what you have to do is we have to take here the only those items, which are the items of direct income. We have to take here the items of direct expense.

It means those expenses are direct expenses without which the production is not possible. If we do not have the material, you cannot do the production. If we do not have the people working on the plant, you do not, you cannot do the production.

If you do not pay the factory rent, without factory you cannot do the production. If you do not pay the freight on purchases, material will not come in the plant. No production.

And, similarly by incurring these expenses what is the output? So, we put the output this side, output, part of output is sold in the market. We sold for 160.

We got back 5,000. So, total sales is 1,55,000. And, now this much of the material, which we will use after incurring these expenses is with us in the stock.

And, 22,100 is the closing stock. So, this side minus this side is the difference. And, this difference is called gross profit.

Why it is called gross profit because this is not the final profit, this is not the divisible profit. Final profit, we will calculate in the lower part when we will prepare the profit and loss account. And that we will do in the next lecture.

Thank you very much.

![#2 Cash Flow Statement ~ Treatment of Tax & Dividend [Problem & Solution]](https://img.youtube.com/vi/q-KZ-INDHNs/maxresdefault.jpg)