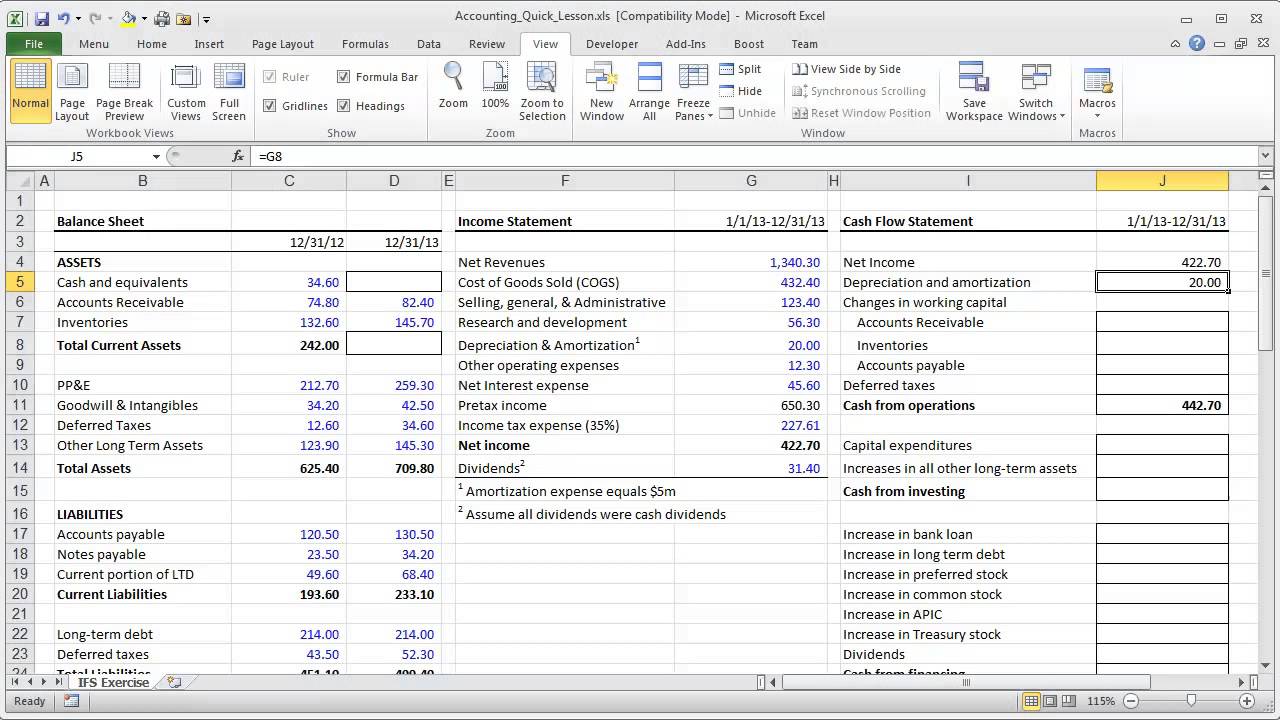

[Music] [Music] welcome students so we are in the process of preparing the cash flow statement and after my say say building up of the theoretical foundation over the cash flow statement and its importance of the MS discussing with you the importance of the cash flow statement now we will learn that how to prepare the cash flow statement actually and for preparing the cash flow statement we have to pass through the three steps first step is we'll have to learn to prepare the basic cash flow statement basic cash flow statement this is called as the basic cash flow statement and this is one first step second is then we'll have to make the further analysis further analysis of the items relating to inflow and outflow of the cash and then finally end up with the preparing the final cash flow statement final cash flow statement I have to end up preparing the final cash flow statement these are the three steps so when this as3 was not there or the final cash flow statement under these three activities operating investing and financing was not required to be prepared then even the basic Ashville no statement was sufficient basic cash flow statement is a summed up process and there we only get to know or verify are able to verify that the cash balance shown in the balance sheet is correct or not and what are the sources of that cash how much cash has actually flow and flown in to the form and how much cash has flown out of the firm and the balance being shown there the opening balance and the closing balance of the cash being shown in the balance sheet we miss that the auditor was verifying in a way that whether that is say adjusting in the bank account also so auditor will have to check the bank account so that that so the cash is available in the bank cash in hand plus cash in bank and second thing was that that cash balance is confirmed that yes it has been received by the business during this year so total cash flow flown into the businesses this much flown out of the business is this much and net balance available is this much so this was the only job to be done by preparing the basic cash flow statement but now that is not going to serve the purpose so we will have to prepare it under the different activities so basic cash flow statement doesn't help us to prepare the cash flow statement that way where we can categorize that how much cash is flowing in from the operations from the investing and from the financing activities so but first we will prepare the basic cash flow statement and will begin from there and in the basic cash flow statement one amendment has been made that when we are preparing the basic cash flow statement in the last column we will have to show because we are taking only three things you account in the basic cash flow statement what we are taking we are taking that is a cash balance at opening so what is the opening balance of cash we start with this then we started this year one particular area for example this ear is 2016 so if any company starts their or their operating period is from January to December so when the business was started or business started his transactions on the first one be 2016 how much cash was there in the company's account so we'll start with this cash opening balance of the cash and then during the year how many transactions were done what different kind of transactions were done certainly the cash must have flown in and flown out and so we'll take in this opening balance of the cash we will add inflows we will be adding inflows so all the influence will be here and then we'll be doing less outflows so outflows will be subtracted and finally the closing cash balance will be calculated here and this closing cash balance should be as same as they're being shown in the balance sheet of the current year so now unless this was serving the purpose but now you have to make one extra column here in the basic cash flow statement also and when they are showing the sources of inflow you have to categorize whether it is operations or operating activities or a source of the inflow is operating or investing or financing you have to put that here but together maybe not say first operations and then investing and then financing no you have to take all the sources of inflow but you have to categorize whether it is operating in flow investing in flow or the financing inflow similarly you have to put here also in case of outflows also whether it is in operating outflow investing outflow or the financing outflow so you have to be careful and we have to say say categorize these sources of inflow and outflow avenues or outflow under these three or different kind of the activities but it's not a final cash flow statement and then we'll have to move to the next step that we are adjusting all the information so we have to take into consideration the balance sheet information given in the balance sheet and then profit and loss account balance sheet and some additional information we have to adjust make a proper analysis find out the balances with the help of further analysis which will bet those balances which will go to the final cash flow statement and we'll have to prepare that activity vise so we will learn now practically how to prepare the cash flow statement and how to analyze the prepared cash flow statement so if you look at the monitor there we have a case of skyline industries limited and we will be preparing the cash flow statement for the skyline industries this is a balance sheet of the skyline industries which is showing the sources of funds first this is the sheer capital then reserves and surplus loans secured and unsecured loans therefore tax liabilities these are the sources of funds the total is three sixty six point two zero lakhs and mis 366 lakhs it means three point six six corrodes and earlier it was two point two it corrodes and then it is application of the funds that where the funds are going how the funds are invested in the form so if you look at this we the fixed assets here which is the grass block then depreciation then that block and capital work-in-progress and then the other items are here that is an investment long-term investment long-term investments short-term investments than the current assets and current liabilities and finally the balance sheet is balanced here we have the total of liabilities 360 6. 20 are related first to twenty eight point five zero lakhs now we have the profit and loss account also for the skyline India Limited and you start with the sales which is again in lakhs given to us and it is 1532 lakhs of the sales then we have the different say other incomes like interest income dividend income total incomes are these then these are the cost part then we have calculated the income before tax and extraordinary items then we have taken made the provision for tax then we had say the total say dividend and other kind of provisions and finally we have the say the balance surplus which is carried to the balance sheet invested or added back in the capital of the company or share capital of the company and here we have some additional information which we have to take into account while calculating the final cash flows under operating investing and financing activities this additional information has to be used so that we will have to check it properly that how much cash inflow and outflow is being shown in the basic as flow statement and how much it is finally moving to the final cash flow statement because in the basic cash flow statement there must be some same changes because format is different the structure is different and sources are so sources are same but style is different structure format is different which is totally different in the final cash flow statement so it means we will have to use this balance sheet information profit and loss information and the additional information and then by say using this three sets of information we will have to prepare the final cash flow statement so now we will start with the basic cash flow statement basic cash flow statement and this is the statement as we have been preparing in the past no changed nothing he said say a traditional cashflow statement and if you look at this cash flow statement then it's very simple to prepare very easy to prepare and for this we will have to start so it means very simple statement you can call it as so it is called as the basic bill basic cash flow statement off Skyline India Limited Skyline India Limited this is the basic cash flow Skyline India Limited we are preparing we have four columns or we can do it with the three also these are the columns we are going to have here this is the one two then it is the three these are the three columns we are going to have and here are the particulars or details then it is the amount and it is the classification of the activities classification classification of activities classification of activities so these are the three main columns so here you have to take the particulars amount and the we have to classify from where the cash is flowing in or the cash is flowing out what are the sources of cash inflow and what are the activities where the cash is flowing out so we are starting with the opening cash balance so what was the opening cash balance here so if you check this opening cash balance we are preparing that balance sheet on a say for the year ending on 31st March 2007 so we will be preparing the cash flow statement for that date itself so along with the balance sheet in profit and loss account now we will have to prepare the cash flow statement also so if you look at the cash flow statement and we start with the opening cash balance so it must be somewhere in current testers so we are here are the current assets and here are the cash and bank balances it is 10 lakhs here and in the beginning we started the process with the 2. 75 lakhs so opening cash balance was amount his 2.

75 lakhs when we started with this balance of 2. 75 lakhs then during the year how the cash has come in from where the cash has flown in and where the cash has flown out now we will try to find out those sources and avenues so now we will be talking we will go back to the balance sheet and in the say the first part of the balance sheet and if you see if you start from the top so let's check that from where the cash is flowing in and where the cash is flowing out moszer to so we'll write here add inflows add inflows add inflows so if you take the inflows here inflows first we start with the share capital so look at what was the sheer capital in the previous year's end sixty two point five zero lakhs and now it has become under lakhs it means share capital worth rupees 37 point 5 lakhs has been issued more in the current here so cash as share capital and this is 37 point 5 0 and this activity is called as the financing activity or on account of financing source the cash has flown in this is called as financing this is called as financing next is the reserve and surplus so our reserve a surplus which was 69 lakhs in the beginning of the previous year misery at the end of the previous year now in the same at the end of the current here it has become one hundred sixty three point seven zero lakhs so it means on account of reserve and surplus also there is it inflow and the reserve and surplus has increased so what is the difference so but how much amount has flown in that is ninety four point it is say I think three zero ninety four point seven zero is ninety four point seven zero worth of a lakh of rupees seven zero have come in but what is there a very surplus source of observin surpluses the profits and profits is the operating income so it is basically operating it is operating we simply have to put here and then we will to prepare the detail to cash flow statement then we talk about the loan front secured loans it means it was zero here previous here but this year we have fifteen lakhs it means 50 lakhs have flown in so we'll write here that yes that is a secured loan is the other source secured loans is the other source of inflow and in this secured loans we have got the cash worth rupees 15 lakhs this year so it is secured loans worth rupees 50 lakhs so it means it is the inflow and when we get the money on account of the loans coming in and that is 15 lakh so it is basically which activity it is financing after that we go to the other loans other loans have also gone up from the 44 lakhs to the 49. 5 0 lakhs so the other loans have others other loans have also become increased wife for point of five point five five point five I'm out that is five point five here it is so loans and loans you are also the financing activity they are also financing activity then we talk about the next thing is the loans are over there for techs liabilities there for tax liabilities have come down from forty five to thirty two it means the liabilities when we pay the liabilities the funds are flowing out this are giving one standard rule we have to follow and you have to learn that when any asset there is increase in the asset it is the outflow of the funds decrease in the assets is the inflow of the funds similarly increase in the liabilities is the inflow of the first and decrease in the liabilities is the outflow of the funds so here deferred tax liabilities when it has decreased from 45 to 32 it means the funds have flown out so we'll count that at the time of the say taking into account the outflows now we talk about the next part and that next part is the say we talk about say your assets and mean in case of the assets if we talk about the gross bilac of the assets it means assets were ninety five point five zero lakhs previous year current period is 174 174 lakhs it means assets have increased so it means there is an outflow not the inflow similarly accumulated depreciation depreciation accumulated depreciation depreciation is always in flow so because it is a non-cash expense so on the one side we take out the depreciation amount from the P&L account and it is increasing the cash balance we keep it in the bank so it means it is 53 lakhs to seventy two point five zero lag so depreciation has increased so it is a inflow so it is the accumulated accumulated depreciation is has it has increased the inflow so accumulated depreciation is by the total amount of this is nineteen point four zero lakhs and here it is operations this is the operating activity depreciation is the operating activity then we have to talk about the next thing that is capital work-in-progress it has also increased so it means capital work in progress also cause the outflow nor the inflow now let's go to the next level that is the investments now investments are there were 105 in the previous year this year they have become 99 that means investments means assets have come down it means the funds have flown in so investments on account of investments investments the inflow has occurred and who say long-term investments how much is the difference it is six lakhs and this is investing activity investments are investing activity then we talk about the next assets we see that in case of the short-term investments have been increased so cash has flown out long term have decreased cash has flown in and short-term investments have increased so cash has flown out now for the current assets and if you talk about the current assets first is the inventory inventory has decreased from 78 lakhs to 28 lakhs it means there is a inflow so inventories inventories is how much I think it is 50 lakhs and this is which activity it is operating activity then is the loans and advances we talk about the next scene that works that does have increased with mrs.

increase in the asset ISA outflow of the funds then we talk about that cash and bank balance see not to take because we are preparing a cash flow statement interest receivable has increased it means it is not inflow so uh no say when you talk about the interest component or interest part we see that it's only receivable so liabilities have increased but not received as such then we talk about the loans and advances yes loans and advances have decreased from 15 to 12 it means it has caused the inflow of the cash so it is the loans and advances loans and advances and if you take the loans and advances about 4 3 lakhs the funds have flown in and this is called as the operating inflow now we talk about the next thing is that is the what is the other source of income we inflow let's talk about the liabilities sundry creditors have gone down it means we have made the payments so funds are flown out interest payable has come down it means interest has been paid so funds have flown out so it means provisions current income tax has come down taxes paid dividend yes dividend part is important here dividend has increased from 12. 5 in the previous to the 15 it means there is an inflow on account of dividend and that is to the extent top that is proposed the dividend proposed the dividend and this is to the extent of 2. 50 lakhs so this is the say this is a category called as financing activities dividend is paid to the on account of share capital this is called as a financing activity and last is the corporate dividend tax corporate dividend tax has also increased so we made the Parisian from the profit and loss account but actually not where the text so this money the form is using this is in flow of the cash so it is a corporate dividend tax corporate dividend tax and this amount is how much 0.

30 this is the corporate dividend taxes this is also financing 0. 30 so I think this is all we have taken into account we have seen and if you talk about this so this balance works out as motor law fee initial cash balance plus inflows so this is 236 236 0. 75 lakhs of the balance be half or the balance we have now and now we'll go for preparing the cash a same is next part we will continue with the statement and take into consideration the outflows less now less outflows less outflows so the first source of cash outflow is what we'll go back and we'll see that what is the source of the cash outflow and the cash outflow here it is then we have taken the share capital it is a in fluid surplus surplus resolved and surplus is the inflow similarly we talk about the secured loans is inflow and others is also inflow then unsecured short term yes short term loans have been paid so it means short term loans have been paid it means this is the from 8 lakhs to 6 lakh so it means first is the unsecured loans we have paid on secured loans so if you say how much restore loans we have paid it is 2 lakhs worth or 2 lakhs and this is the financing activity then the next is loans we have talked about then is the deferred tax liabilities they have come down from the 45 to 32 it means worth of 30 lakhs defer tax liabilities have come down therefore tax liabilities and they have come down by 30 lakhs so it means this is again the financing or operating activity this is the taxes relating to the operation so this is the operating activity we will continue with the statement so therefore tax liabilities after this is a grass block of the S gross professors means that is the answers have increased from 95 point five zero to 174 so it means grass block is grass block of fixed assets and that is how much we are putting here this amount is we are putting here and this is ninety five point sorry this this difference is grass block of the fixed sesterces seventy eight point five and it is on account of say investing activities grass block then we talk about the capital work in progress and the capital work in progress has also increased from 45 to 106.

5 so this is that capital work in progress sorry two point five to five so it means there's the increase outflow that is a capital work in process and this is why two point five capital work in process that is by two point five and this is the called as the investing outflow capital work in process now let's move further to the other parts and if you move further through the other parts then let's check the other sources outflow investments have come down long term short terms have increased so it is the short-term investment it is short term investment and it has increased so when you talk about the short term investment it has increased by twenty one point seven five and this is called as investing activity this is called as investing activity then we talked about the others say long term investments have come down so it was inflow now come to the current assets inventory has caused the inflow sundry directors have caused the outflow so it is sundry debtors sundry debtors and sundry debtors if you talk about buy worth of twelve point five lakhs they have gone up so it is operating then we talk about the next thing that is the cash and bank - not to be taken interest receivable is two to three so because of the interest receivables three is the difference as it has increased interest receivable by three lakhs it has caused the outflow but it is the now you call it as say investing activity interest is the investing activity then we talk about the Sunday debtors now say sundry creditors now we have dealt with the inventory sundry debtors interest and loans Elvises we have already taken as inflow now we talk about the current liabilities and current liabilities are sundry creditors have in decreased it means we have paired the current liabilities so once the current liabilities are reducing it means they are causing the outflow and how much is the say eccentric creditors the outflow is seventy how much it is seventy sundry creditors is from 94 to 16 it is 78 so it is sundry creditors 78 lakhs this is the sundry credited it means it is operating it is a a 78 lat operating cash flows and then we talk about the interest payable we talk about the interest payable interest payable is decreased it means interest has been paid interest payable liability has decreased so it means it has caused the outflow of the funds so interest payable is this much and if you talk about the interest payable part it is by 2. 5 lakhs it is a financing outflow now we talk about the next thing is that is the provisions will be taking current income tax provisions it is 5 to 3 net of the tax paid so it means it has caused the outflow so it means it was a closing verse 5 it has become 3 so it is the current income tax payable current income tax payable so current income tax has been paid this this is to the extent of 2 lakhs so it is operating outflow then we talk about that propose dividend propose dividend has increased so it is a source of funds and corporate dividend tax so it means nothing else is their corporate dividend tax is also the inflow we have increased it so now we talked about the last item that is the miscellaneous expenditure miscellaneous expenditure has increased from 5 to 16 so miss Lily's expenditure is again in outflow miscellaneous expenditure is again outflow and that is my eleven lakhs so this is called as operating activity or the operating on account of the operating expenditure and this is 11 so now if you talk about this this works out as the say unlit we had to thirty six point seven five and if you take that total of this that is to twenty six point seven five so you can easily find out closing cash balance closing cash balance is ten lakhs closing cash balance is the ten lakhs and this is the closing balance given here in the say balance sheet if you look at the cash and bank balances here it was two point seven five lakhs in the previous year at the end of the previous year it was two point seventy five lakhs and in this year the closing cash balance is the ten lakhs so it means we have verified that yes it is correct that whatever the balances are shown cash balances shown closing cash balances shown in the say balance sheet that is verifiable we have identified here by preparing the basic cash flow statement that yes this was the opening cash balance 2.