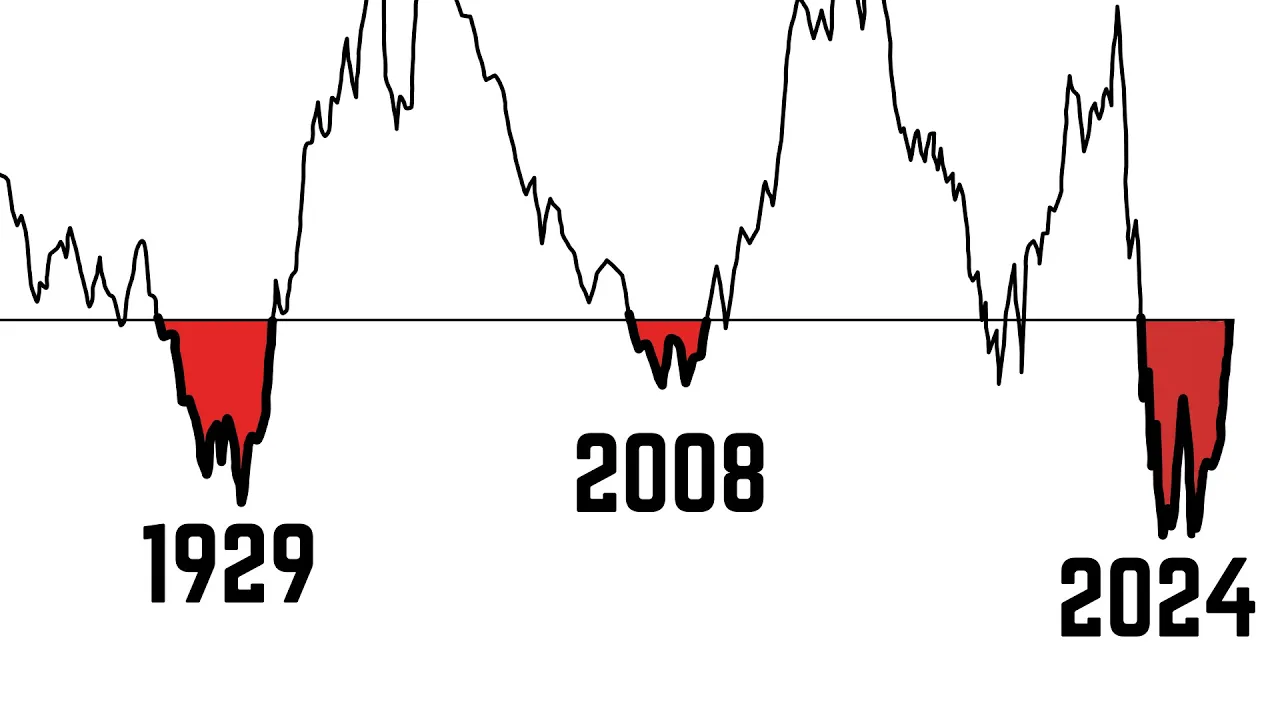

the yield curve has just steepened by a full percentage Point coming out of an inversion the last time this happened was in 2020 during the covid-19 recession before that it was towards the end of 2007 heading into the great financial crisis and before that it was in 2001 heading into the bus every single time the yield curve has done this it was either during a recession or right before recession began and that includes the Great Depression where the yield curve steepened by a full percentage point in OCT October of 1929 the very month that marks

the beginning of the Great Depression yes yes Peter we've heard all of this before when the yield curve steepens that's when the recession is meant to begin so then where on Earth is the recession today GDP growth in the United States is still trending at a healthy 2% according to government data the job market is still relatively strong and in case you don't trust the government data then just look at the stock market it's at all-time highs not really things you would typically associate with a recession right maybe this incredible indicator the yield curve that

was discovered by Mr Campbell Harvey in the 1980s is finally dead maybe it's time to say goodbye to the yield curves Flawless track record let's try and figure out if we're there yet first a very brief rundown on what the yield curve is meant to be and why a steepening is meant to coincide with a recession the yield curve takes a longer term bond yields like the one you get on a 10-year treasury bond and shorter term bond yield like the one you get on the 2-year treasury bond and it looks at the difference between

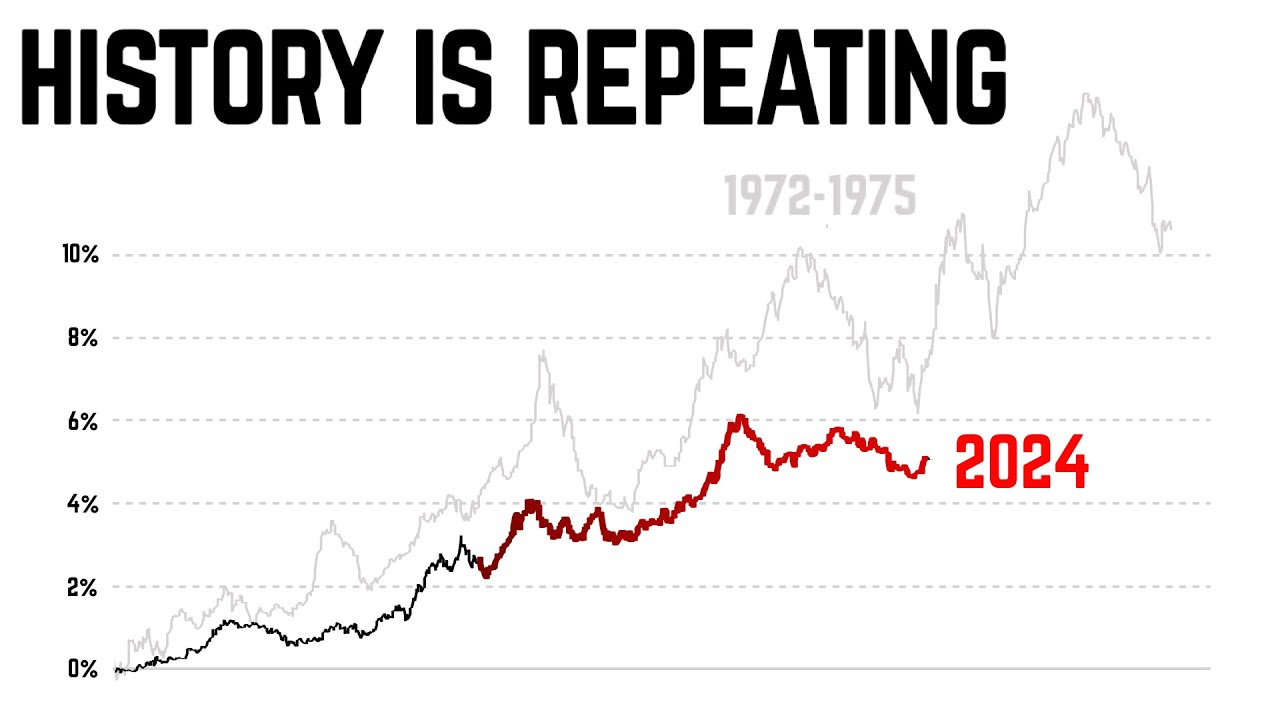

them this is what it looks like this is the yield on a 10-year note minus the one on a 2-year note now most of the time you have the 10-year yield that is higher than the 2-year yield so the yield curve is above zero but sometimes the 10-year yield becomes a lower than the 2-year yield and that's what you call a yield curve inversion now this usually happens because the Federal Reserve has been raising its interest rate they control shorter term yield and so they can deliberately make it so that the yield curve inverts this

this is what they call restrictive policy something you may have heard them say before now for reasons I won't get into in this video restrictive policy isn't great for the economy it makes banks in the United States stop lending and every single time that leads to a recession and that's where the yield curve steepening comes in it's when the yield curve is coming out of an inversion and that happens when the Federal Reserve begins to cut interest rates because the economy is weakening and likely heading into a downturn so now you're all caught up let's

come back to question why on Earth has a recession not yet started today despite the yield curve steepening well when we look at where the yield curve is at the very beginning of the last four recessions it's kind of a little bit different every time for example in 1989 and 2020 the recession started when the yield curve was at 0.1% in 2001 the recession started when the yield curve was at 0.5% and in 2007 the recession only began when the yield curve was at 1% so this right here is the hot Zone where recessions typically

begin today the yield curve is in The Hot Zone for sure but we can't completely invalidate the yield curve as a recession indicator because if you had set that in July of 2007 when the yield curve was at exactly the same spot as it is today you would have been painfully wrong because the recession didn't begin until the yield curve had steepened all the way up to 1% if we assume that the same thing is going to happen again this time around the yield curve could continue to steepen until January of 202 5 before the

recession actually starts now if the yield curve steepens past this level over the next year and we still haven't entered a recession that's when we can say that the yield curves validity as a recession indicator really comes into question but this is a very mechanical way of looking at the yield curve we're merely just observing the levels and comparing the different episodes we have throughout history there is another way that we can assess whether or not the yield curve is going to be correct this time around and that is by looking at the US job

market or more specifically initial jobless claim so the number of people that are filing for unemployment every week if this chart looks familiar that's because it is it's almost the exact reflection of the yield curve itself and that's been the case going back all the way to the 1960s 90% of the time the yield curve is following the exact same path as initial jobless claims why does this happen you can go ask the FED we're just looking at the end result here now you may have noticed that initial jobless claims Rec recently have been particularly

strong despite the fact that the yield curve is steepening so they haven't really been going in the same direction now this is unusual behavior because most of the time when a steepening occurs heading into a recession you tend to see initial jobless claims moving higher and confirming what is happening in the yield curve now we have two potential scenarios here scenario a initial jobless claims never end up moving higher and the yield curve actually ends up rein verting which would delay the timeline of the recession this happened briefly in 1999 when the yield curve steepened

but initial jobless claims continued to Trend lower it also happened very briefly in 2006 the yield curve steepened but the job market remained strong and so the yield curve reined in both of these cases the recession didn't play out immediately but a couple of years later now in scenario B initial jobless claims actually begin to move higher over the next few months and catch up to the yield curve now that's actually exactly what happened in 2007 the yield curve was steepening even though the job market was still quite strong the steepening continued and eventually initial

jobless claims began to Trend higher marking the beginning of the recession so which one is it going to be scenario a or scenario B well there are many experts out there that argue that the economy is nowhere near a recession because of the extreme levels of government spending indeed when we look at us government spending it has been very elevated recently certainly some of the most aggressive spending that we've seen over the last decade but if we zoom out a little bit we see that the US government was also still spending a lot heading into

the 2008 recession perhaps less than today but still it didn't do much to stop the worst economic downturn since the Great Depression from occurring so that puts a dent in the idea that government spending alone can stop a recession from occurring at Bravo's research we believe that we're in the process of seeing scenario B playing out meaning that we expect initial jobless claims to begin trending higher catching up to the signal from the yield curve and for this to coincide with the beginning of the next session and if we're following a similar path to what

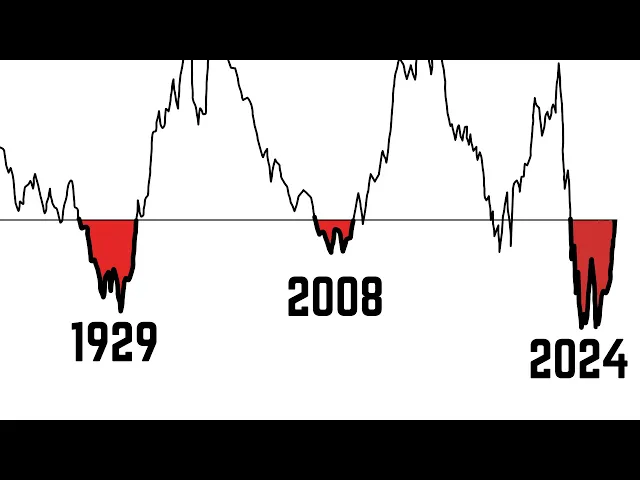

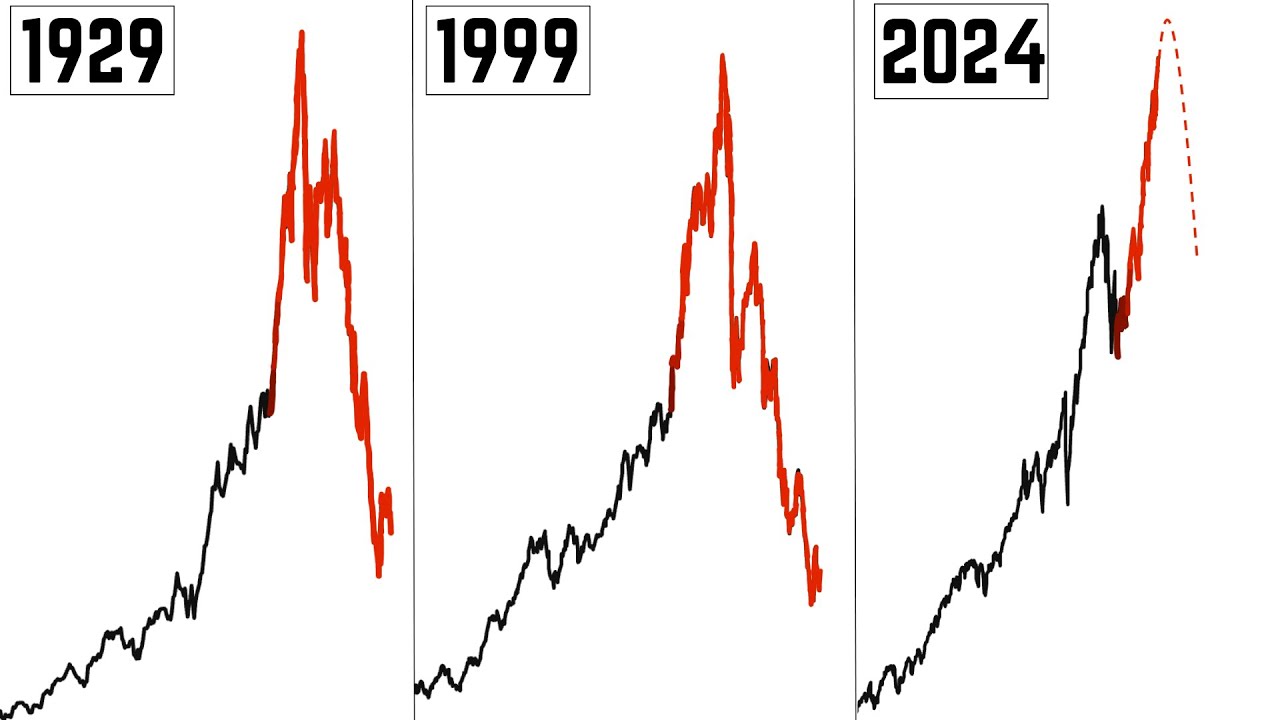

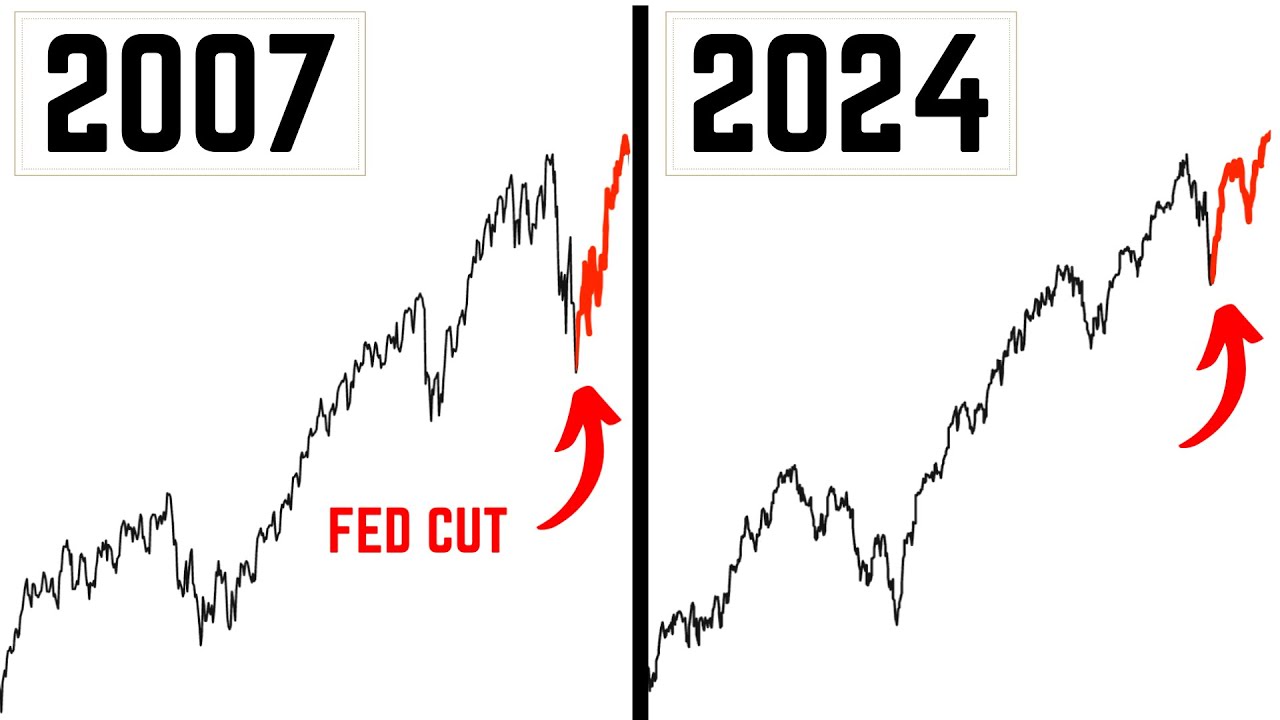

happened in 2007 that could be about 3 months from now now what does that all mean for the US Stock Market that's breaking out to all-time highs you do tend to see the stock market Fall heading in the months before recessions occur that happened in 2000 in the couple of months before the 2007 recession and going back further in history we also saw the stock market Peak well in advance of the 1974 and 1980 recessions this is why most investors that believe were very close to a recession are turning bearish right now after all with

only a few months left before the recession starts stocks should be declining right well history also shows that the stock market can sometimes continue to rise until the very last moment that happened in July of 1990 in February of 1980 and it also happened in September of 1929 this is why we're staying extremely flexible with our Equity strategy today not just because we want to pick up nickels in front of the steamroller but because we're also aware we could be wrong about a recession occurring in the next few months