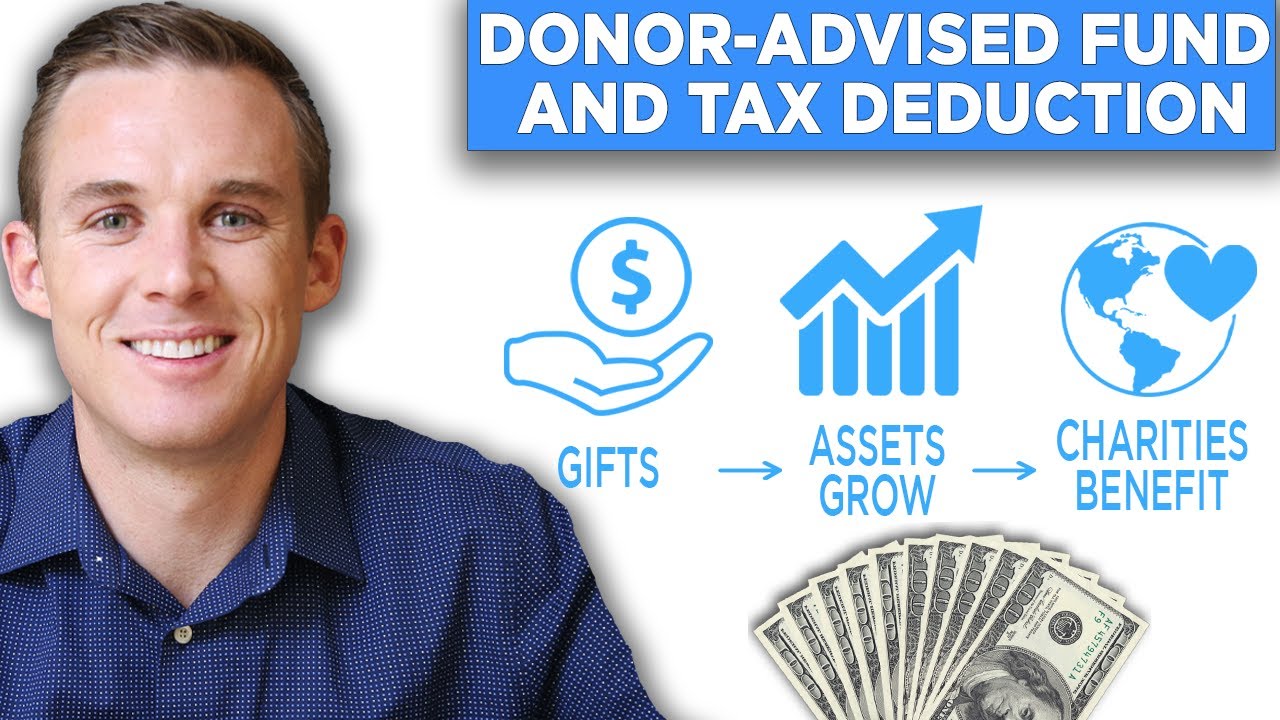

in today's video I want to talk about a powerful gifting strategy that if used strategically can give you a double tax benefit this is a gifting strategy available to all ages and in my opinion is the second best way to gift to charity towards the end of this video I'll talk a little bit about what I think is the best way to gift let's get into it the charitable vehicle we are talking about today is a Donor advised fund now some of you might be familiar with a Donor advised fund but I frequently see it

used in the wrong way but first what is a Donor advised fund a Donor advised fund is a vehicle that allows you to gift money or assets today gain a tax benefit for that gift but then grow and release that gift to a charity on a later schedule of your choosing for instance you could gift $50,000 into a donor advice fund this year invest that $50,000 to keep your gift growing and then you could give $5,000 a year to a charity of your choice and because of that growth you're likely to get more than 10

years worth of of gifts from that charitable fund this distribution schedule is completely customizable but it's worth noting that you only gain a tax benefit on the initial gift not on any distribution to the charity the reason a donor advice fund is so important in today's tax climate is because I see so many people giving to charity but gaining no tax benefit from it now our gift to charity shouldn't be only focused on the tax side but it is something we should take advantage of if possible the reason achieving this tax benefit is so difficult

is because right now we have such a big standard deduction in 2023 the standard deduction is $27,700 for a married couple under 65 gain a tax benefit from your gift your gift plus other itemized deductions needs to be higher than your normal standard deduction let's say that a couple givs $122,000 to their Church they have an additional $10,000 in state and local tax deductions and then they have some deductible mortgage interest combining these gives us an itemized deduction of 24,500 which means this couple receives zero tax benefit from their $122,000 gift they'd be better off

in this instance taking the standard deduction than they would be itemizing you only gain a tax benefit if you itemize your deductions so here's where a Donor advised fund or what I'll referred to as a daf comes in we want to batch gifts together to gain the biggest tax deduction from it say this couple gives $122,000 to their Church each and every year and plans that do so indefinitely they could batch together 5 years worth of gifts and give it all at once the problem with this is they might not want to gift $660,000 to

their Church all in one year and then give nothing for the next four years so what they can do is they can batch these gifts and instead contribute to a Donor advised fund now their itemized deductions will total 72,500 which means they they definitely should itemize and take that itemized deduction further they can invest that $60,000 and then release $112,000 per year to that charity and do so over 5 years and do the exact same thing they were doing before but now gain a tax benefit from it clearly this benefits the donor far more now

there are some important things you need to know about with donor advice funds first you can gift either cash or assets into this charitable Fund in a minute we'll talk about the beneficial option of gifting assets instead of cash further there are no contribution limits you can uh contribute as much as you want in a given year to that daf but there are some limits on how much of a deduction you can gain from that gift in a given year any gift you make is irrevocable and cannot be clawed back in any way the gift

must also ultimately go to a registered 501c3 then when we talk about the limits of the deduction you can take from your gift that limit is tied to your adjusted gross income for a cash gift you can gain a deduction up to 60% of your AGI for an asset gift that limit is cut in half however you can carry forward gifts for up to 5 years the only thing to note with this carry forward is that you're only going to gain a tax benefit in future years if you can itemize and gain more of a

benefit than the standard deduction now I want to talk about the double tax benefit of gifting appreciated stock from your taxable account to that Donor advised fund like I said before you can gift assets so let's say you invested in apple more than a decade ago and your original $10,000 investment has grown to a whopping $125,000 now if you sell this position in the future for let's say income you're going to owe a lot in taxes because of those large unrealized gains at an 18.8% long-term rate this would result in you owing $21,000 Plus in

taxes instead why not gift this Apple stock right to your Donor advised fund despite this low cost B basis you get a gift deduction based on the full value of the stock at the time of the gift so $125,000 deduction at let's say a combined rate of 30% gives you a $37,500 tax benefit from this contribution now here you did two things you eliminated a large future capital gains tax bill but then you also gained a massive deduction in this given year and you gained that double tax benefit growing to nearly $60,000 in taxes saved

from the strategy and if you're someone who let's say really loves Apple know that you can simply buy it back the next day and start with a brand new cost basis there are no wash sale rules or anything of the sort to deal with here you just need to keep in mind those deduction limits that we talked about and so we can see that a Donor advised fund can be quite beneficial as a charitable vehicle a lot of investors of all ages can benefit greatly from using this fund within their charitable giving that is until

they reach a certain age once you are in your 70s know that there is another charitable strategy that I think eclipses a Donor advised Fund in most situations and that's a qcd or qualified charitable distribution a qcd is a direct gift from your IRA and the best thing about a qcd is that you don't need to itemize expenses you get an above the line deduction which means you get a full deduction whether you itemize or take the standard deduction now I really do like the idea of gifting highly appreciated stock into a Donor advised fund

but at the end of the day you are gifting an asset that is taxed at a more preferred long-term capital gains rate and you could potentially get a step up in basis on that highly appreciated stock when you pass away qcds give money from your IRAs and count towards your rmd for a given year so it eliminates higher taxed dollars the constraint here is that you have to be over 70 A2 to use qcds now one other thing to note about donor Adis IED funds is that not all custodians allow for these types of accounts

the big custodians like Fidelity Schwab and Vanguard do but know that each has constraints to consider first Vanguard has minimums for the initial contribution as well as ongoing contributions whereas Fidelity and Schwab really don't further across all providers know that an annual admin fee can be quite high at 6% per year now this isn't crazy high to the point that it rules out the potential benefits of a Donor advised fund no there is little you can do about this but it is a cost worth noting then investment fees will obviously vary depending on what you

choose to invest in you can stay as simple as investing in a money market account or you can get more aggressive and invest for growth that Donor advised fund can pass through gifts instantly or gifts for the next 30 Years these are highly customizable and so again don't make the common gifting mistakes like making a gift but receiving no tax benefit for it there are options available to you that can be quite powerful now we briefly covered qcds in this video if you want to learn more about this charitable strategy click here thanks for watching

and always remember you don't need more money you need a better plan we'll see you in the next video