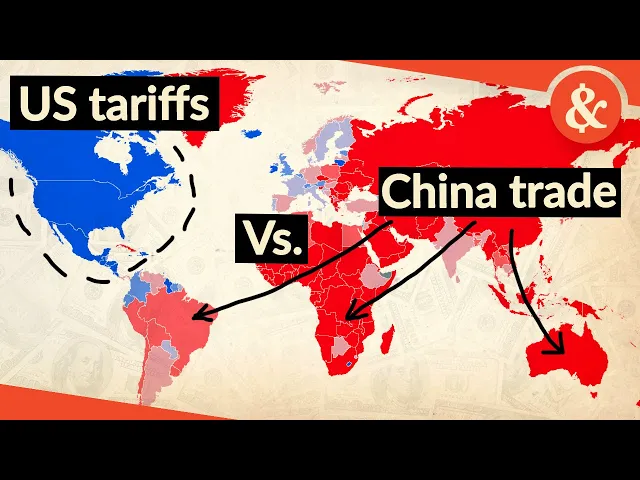

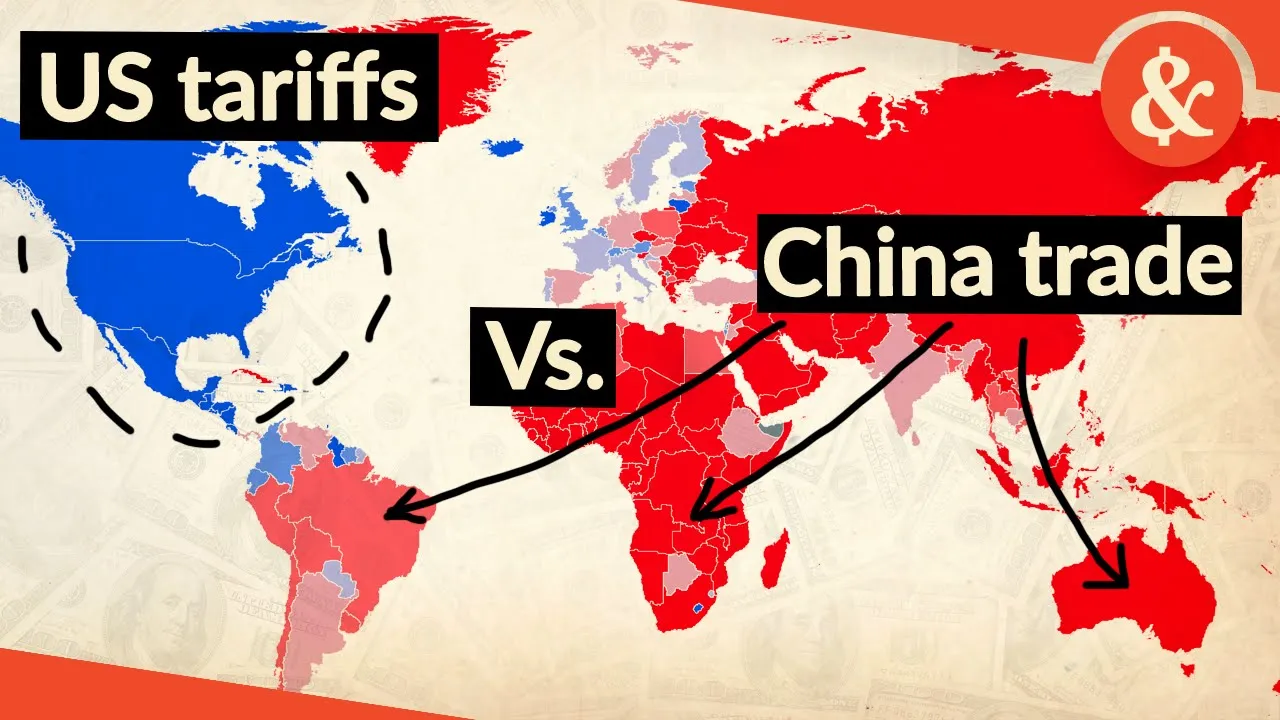

This map shows in blue how the US was the biggest trading partner for most countries in 2001. But as the years progressed, we see the map turned red as China quickly overtakes the US as the world's biggest trading partner. No wonder the US escalated an unprecedented trade war against China.

But is it too late? Or can the US actually contain the rise of China? Many economists have come out and written that Beijing has escalation dominance and that the US will lose against China.

World famous macro investor Ray Dalio is even convinced that what we are seeing today is a classic pattern of how a rising power displaces an old hegemon, first through trade, and then by replacing its currency as the global reserve currency. If that happens, the dollar will collapse and the US will find itself much poorer, unable to pay for its global military presence. While China will suddenly see its power multiply.

And yet US Treasury Secretary Scott Bessent has said that if you look at the history of the trade negotiations, we are the deficit country. What do we lose by the Chinese raising tariffs on us? We export one fifth to them of what they export to us.

So that that is a losing hand for them. And actually, Bessent may be correct. People like Dalio, who argue for the rise of China, often don't take into account how unique the role of the US dollar is today.

Now, that is no longer backed by gold. On top of that, when I studied The Rise and Fall of Hegemons over 400 years, I found plenty of cases where dominant powers managed to contain rising rivals. For example, Britain contained an industrious superior, Germany in 1914, and the US arguably contained a rapidly rising Japan in the late 80s through tariffs and the currency deal.

So who actually has the stronger hand today to win this trade war and become the new global hegemon? The only way to answer that question is to do a proper deep dive into the rise and fall of global hegemons. In this book, Principles for dealing with the Changing World Order, famous macro investor Ray Dalio attempted to plot the relative economic and military power of the world's most powerful countries into a single index.

It looks like this. It shows us that in the 17th century, the Netherlands quickly rose to become the world's most powerful nation, overtaking Spain and China. Then it shows that the United Kingdom overtook the Netherlands to become the dominant hegemon in the 19th century.

The US rose in the 20th century, and finally we now see the rapid rise of China. Based on this research, Dalio argues there is a detailed pattern that can explain why empires rise and fall. But in the past, I've argued that this detailed theory does not hold up very well.

However, the pattern that is great power first tends to become an industrial power and then later obtains reserve currency status. That is not very controversial. For example, while the UK overtook the Netherlands as a main trading nation in the late 17th century, it was only in 1784 that the Dutch guilder lost the reserve currency status to the pound.

Similarly, the UK pound only lost its crown as a global reserve currency in the 1950s, well after the US had overtaken it. Industrially speaking. Why is this the case?

Why do rising nations take the industrial crown before taking the reserve currency crown? To answer that question, we need to talk about gold. You see, for most of the period Dalio studies, all national currencies were directly tied to gold.

So when Dutch guilder, British pound and U. S. dollar could be exchanged for a certain weight of gold because gold is pretty heavy and impractical to divide and to carry around, people ended up favoring currencies that were convertible into gold rather than holding gold itself.

However, this it did, of course, mean that the currency issuers needed to convince holders that they had enough gold in their fold to back up all the paper that they had issued. So, logically, the nations that were able to issue the most currency were those that had the most gold. And how did nations earn gold?

Well, by exporting more than they import Of course, this can explain why historically rising powers needed to become an exporting powerhouse. First, once their superior industries became a gold magnet, it would slowly but surely attract gold from the reigning regiment. Of course, the reigning currency had a big advantage.

It was already used by everyone, but at some point, once the gold in the regiment's central bank would be low enough, that power would face a run on its currency, which would cause it to collapse, after which the rising powers currency would, of course, take over it. This sequence of events is roughly the dynamic that Dalio talks about in this book. In a gold standard world, I think Dalio's analysis holds up pretty well, actually.

The Dutch lost the export crown to the British in the late 17th century, but it took roughly a hundred years for Dutch gold to run so low that the Bank of Amsterdam faced a run and collapsed. Similarly, the US surpassed Britain's industrial market in the late 19th century, but it took the US's superior industry slowly but surely, collecting all the world's gold and a major war before the US dollar could fully displace the pound in the 1950s. Dalio's model can also explain why some challenger powers never made it.

For example, while Napoleon tried to break British industry when he formed the so-called Continental System, the British used the power of their reserve currency to borrow money to fund a war against its weakest link, Denmark. In this case, Napoleon lost the trade war because he had not yet surpassed Britain in industry. The next challenger, Germany, fared slightly better as it hit the first milestone, surpassing Britain's industry around 1870.

However, then it mistakenly started a massive war before it has surpassed Britain financially and ultimately found itself unable to borrow much. While Britain used its incredible financial power not just to finance itself, but also key allies such as France and Russia. However, today we no longer live in a gold standard world.

I have directed Secretary Connelly to suspend temporarily the convertibility of the dollar into gold or other reserve assets, except in amounts and conditions determined to be in the interest of monetary stability and in the best interest of the United States. Therefore, the framework cannot tell us much about whether or not to panic and displace the US today. After all, the US did already run out of gold in the 1970s and rather than perishing like the UK pound and Dutch guilder did before it.

The US dollar became more valuable than ever after that. US trade deficits became bigger than ever, and during this period the US has faced three challengers that exported way more than they imported. The first was Japan, an innovative rising export powerhouse which prioritized exports over everything else.

And in the 1980s, many predicted that Japan would overtake the US. And yet, if we look at the dollar GDP, this is what actually happened. Next we have the European Union, which had a significantly bigger population than the US and overtook US manufacturing output in 2003, and it had an export surplus.

No wonder that some expert economists predicted it would overtake the US dollar as early as 2015. However, much like Japan, after a significant challenge to the dollar, Europe's dollar term GDP stagnated. The reason that exporting powerhouses can no longer simply displace the dollar is, of course, that this is no longer tied to gold.

But if it's not backed by gold, then why do countries around the world want to keep using the dollar as their preferred reserve asset? Well, according to central Bank reserve managers themselves, they choose the dollar over other assets for two main reasons. The first is safety.

Safety from getting your assets confiscated and safety for major volatility. As the dollar is one of the most stable currencies in the world. The second main reason is liquidity.

Liquidity comes from central banks easily being able to borrow dollars from either the IMF, world Bank or feds. But for many developing countries, it also comes from having access to the US consumer. You see, the most stable way to obtain dollars is to export to the US.

And by making this easy. The US is essentially giving developing countries an extremely strong incentive to plug into the dollar system. However, as you can imagine, this is no charity.

The dollar's reserve currency status has given the US a tremendous advantage. It can now keep a military presence all over the world, even though it does not have the industrial markets to really back that up. And yet, as a market economists have emphasized, an expensive dollar does make exporting from the US very costly, leading to the industrialization.

This may become a problem if there is a total war, and this is why the US escalated this trade war. So I would argue that winning a trade war for the US means taking back the industrial crown from rising power China. On the other hand, winning the trade war from the perspective of China would mean ending US hegemony once and for all.

Taking reserve currency status away from the dollar. If China could pull this off, it could become the new reigning hegemon in one fell swoop. After all, if we purely look at the value of all goods and services, if the dollar was not so strong, we would get this graph showing that officially, in terms of raw output alone, China's economy is already bigger than that of the US.

Now, at this point, I do have to mention that there are very legitimate concerns about the quality of official Chinese GDP data. But despite that, the point remains that the increased value of the dollar, despite high inflation in the US, made US GDP and therefore military might much higher than it otherwise would have been, displacing the US dollar. Is that even possible?

After all, before Trump started his trade war, China's dollar value of GDP growth was starting to look an awful lot like that of Japan and Europe going flat. Well, yes, I think there is still a very plausible scenario in which China becomes the global hegemon by replacing the dollar. You see, after freezing Afghani reserves in 2021 and Russian reserves in 2022.

Many countries are looking for an alternative reserve currency to the US dollar. This has only gotten worse now that Trump has made the dollar much more volatile. And now that it is threatening to close American markets, thereby robbing many developing countries of a safe and stable way to accumulate dollars.

In this scenario, the Chinese leadership recognizes this unique vulnerability and also recognizes that their current policies have kept the renminbi usefulness as a reserve currency way down. Therefore, XI Jinping now starts following the advice of economists that I've written about this for decades and takes three steps to make the Chinese renminbi its currency, an irresistible alternative to the dollar. First, the Chinese recognize that foreign central bankers value safety and predictability.

So while Trump keeps bashing the fed, China's leadership moves to make its central bank completely independent. It also changes the rules to freely allow money in and out of China, unless it gives for it, as it orders complete guarantees that she cannot sanction you, let alone move in to confiscate your reserve assets. If, for example, you speak out against China, this instantly gives the renminbi an edge over the dollar for relatively developed countries with lots of reserves like the Gulf countries, South Korea and Japan.

Second, China's leaders realize that they need to make it attractive for developing countries as well to use the renminbi rather than the dollar. Therefore, they make the unprecedented step of opening up their consumer market to a developing nations. This means they copy the US Cold War tactic of allowing these nations to protect their own market somewhat from Chinese producers.

Finally, the Chinese leadership removes policies to subsidize industry, suppress wages and control the value of the renminbi, seeing their wages go up. The Chinese economy finally sees an increase in consumption, allowing for further growth in China. Increased reserve currency usage means that the Chinese renminbi rises, giving the Chinese consumer far more purchasing power globally.

And this then makes the renminbi extra attractive for developing nations, as they can now re-orient their export growth strategy from the US to China. Finally, implementing these long overdue measures makes the renminbi instantly more attractive than the dollar for both advanced exporters and developing countries that need a big consumer market to export, too. So why hasn't this happened yet?

Well, the most convincing two arguments I've heard about it are one ideology and two power. You see, ideologically speaking, Xi has apparently developed a real passion for exports, and not so much for consumption and allowing some industries to move overseas. That's a big no no for him.

Second is politics. This entire plan involves ceding a lot of government power to independent institutions that protect foreign money in China. So far, Chinese leadership has done exactly the opposite, seeking more power rather less.

This means that, sadly for China and frankly, for the world, this scenario has a really low probability of actually happening. In my opinion. Despite Trump's chaos, China is unlikely to actually win the trade war and displace the US as the new hegemon because its leadership is unlikely to implement the reforms that they need to do so.

That is great news for Trump, of course. But does he himself actually stand a chance to win? Let's now explore the scenario that.

The US holds of yet another challenger and remains the global hegemon. Honestly, until Trump came along, it looked like this scenario would happen. China's GDP was going exactly the same way as that of Japan and Europe.

But as I've said in a previous video, I do understand that the Trump team still viewed China's industrial subsidies and recent dominance of new industries as a national security threat. However, in contrast to listening to his smartest advisors who recommended going slow and predictable with the tariffs while copying some of China's industrial subsidies, Trump decided to go hard with the tariffs and follow his hardline advisors while sprinkling his own chaos in between. As a consequence, the dollar has been really volatile lately and the development model of many nations is now in danger, both weakening the attractiveness of the dollar as a reserve currency.

To reverse this, in this scenario, Trump does three things. First, he focuses more on playing golf and less on tariffs. This means that he lets his most competent advisors implement a moderate and predictable tariff and subsidy program to slowly but surely bring some strategic industry back to the US.

Second, he reestablishes the trustworthiness of the dollar by strengthening rather than undermining the rule of law by ensuring that the Federal Reserve remains independent, and by refraining from annexing or threatening to annex territories that belong to allies. Finally, he recognizes that to grow a bigger economy than China, the US needs talented, hardworking people. So while he restricts illegal immigration, he makes it legal immigration a viable alternative.

In this scenario, China continues on its growth path of failing to rebalance its economy. This ensures that, while imperfect, the US dollar remains the only serious reserve currency. On top of that, Trump is helped by the fact that developing countries will sooner or later impose tariffs on China on their own as their markets are flooded with subsidized products.

Sadly, I think again, that this scenario is now pretty unlikely because it requires that Trump completely changes the way that he operates. This is why I think in the end, sadly, we have to answer our main question who will win the trade war by talking about the most likely scenario? Nobody wins a trade war.

In this scenario, Trump's chaos will continue to make the dollar less attractive. But because Xi is unwilling to rebalance the Chinese economy, there will not be a credible alternative. Therefore, we get stuck in a world where there are essentially three big global export clusters; China, Europe and the US.

In this scenario, China remains the biggest exporter, but it is not dominant enough to set the rules of the game for everyone. In this scenario, there are also still three big import clusters. But again, while the US remains the biggest, it is not big enough to allow it to convince all other countries to join it in completely blocking out China from the global economy.

And sadly, while this may sound like a continuation of the global order that we have right now, a new field of economics, geo economics teaches us that Trump's trade war is a sign that the hegemonic power of the US is now in question. We are moving to a multipolar world, and that has major implications for what the global economy will look like. When it comes to investments, inflation, currencies, trade wars and more.

But what the multi-polar global economy in which nobody actually wins a trade war will look like? That will be the topic of my next video. So subscribe and hit the bell icon if you want to make sure that you don't miss it.

And to get an idea about the new global order before that video comes out, I highly recommend you check out the following three articles from our advertising sponsor, The Economist. First, check out this super interesting article about Trump's tariffs and how they are starting to hammer Chinese exporters. Then this article about why Trump's Re industrialization plans will not work.

And then finally, this one about which country's stock markets have benefited and lost from Trump's tariff chaos so far. Indeed, if you want to read all of this super interesting analysis and more, then I highly recommend you use the link below to get yourself an annual subscription to The Economist for a 20% discount. Whether you prefer the digital edition or you are like me and prefer to catch up on the global economy during the weekend, sitting down with a nice cup of coffee and the paper edition, you always stay on top of the latest global developments no matter where you are.

So don't miss out! Click link in the description or top comment or head over to economist. com/moneymacro to claim your exclusive 20% discount today.