making this single mistake will keep you living paycheck to paycheck forever even if you're making millions of dollars per year lifestyle creep or lifestyle inflation is a problem almost everyone experiences whether you're a recent college grad with the first real job an entrepreneur with a growing business or you're climbing your way up the corporate ladder when you begin earning more money it's hard to gauge how much is wise to spend the problem continues to present itself when a raise promotion extra income or sudden windfall arrives as people gradually get used to a more expensive way

of living budget-friendly meals and value-priced clothing loses appeal the extra income becomes disposable income and investments and savings often lose priority thankfully it's easy to recognize this behavior so you can avoid it allowing you to build incredible wealth and reach financial freedom so you can retire instead of staying broke forever my name is chris and i help teach people about money personal finance and investing if you're interested in improving your financial future make sure to subscribe to the channel and hit the like button if this video is helpful lifestyle inflation is when unnecessary spending increases

as your income rises as an individual earns more money their spending rises to meet their pay we've heard the expression the more you earn the more you spend this happens to many people without them realizing it they wonder why they're living paycheck to paycheck without ever getting ahead for some reason whenever you receive a raise or bonus you might suddenly feel obligated to spend all of it any extra money can burn a hole in your pocket if these funds aren't dedicated for a specific goal with powerful marketing from retailers designed to make us spend our

hard-earned money instead of investing more as our earnings rise many people fail to realize that this could be happening to them instead of thinking you deserve it when looking at that brand new car remember that you deserve to have a financially stable future while not being stuck with a car that's over budget lifestyle inflation is the exact reason why 70 percent of lottery winners go broke within a few years of receiving their windfall the phenomenon of being totally unprepared for financial gain does not escape these lucky winners too many people who suddenly find themselves in

a position of what they consider to be great wealth are woefully unprepared to budget save and invest this is something they've likely never done before the obvious consequence is that most lottery winners go broke in a relatively short period of time it's like putting a first-time driver in a race car and expecting them to know how to handle it without planning education or training the outcome is unpredictable at best take for example a middle-aged guy named bob bob's been working at a company and receives an offer for a new opportunity an opportunity for a bigger

office and more responsibility and with that promotion comes a fifteen thousand dollar raise despite having to work more hours spend less time with his family and take on more stress a few weeks into receiving the extra money in his paycheck that extra doe has already found a new home in the form of a newer more expensive car and a more expensive family vacation suddenly that fifteen thousand dollars is gone being spent on something that will only provide short-term value and satisfaction bob has maxed out his budget but he's still happy until a year or two

later when the extra hours at work catches up with him his lifestyle has crept up to his earnings leaving him with no choice other than to decrease his lifestyle or continue working harder to earn more money this is a common problem with young adults getting their first job fresh out of college with that brand new degree young people are ready for that first big career move long gone are the days of ramen noodle lunches and bad coffee made fresh in the dorm room young adults are so burnt out on that dorm lifestyle they're glad to

have that new paycheck that will give them just the opposite it's lunch out with the office gang drinks on friday in starbucks every morning on the commute they have that first brand new car which was either leased or financed with a hefty monthly payment with a steady salary spending easily increases unchecked after all you want to enjoy life while you're still young right new found wealth even at this level isn't immune from the lifestyle inflation any more than the lucky lottery winner it often goes unnoticed affecting its victims for years often until it's too late

to adequately prepare for retirement years without preparation and budgeting money slips away often unnoticed and poor money management habits emerge difficult to break in later years making good habits at an early stage is crucial to one's future and discipline to spend wisely and invest for the long haul is imperative approaching retirement age doesn't mean lifestyle inflation is no longer an issue instead it could be magnified by the fact that it's likely that the home mortgage is paid off and earnings are at or near all-time highs kids likely don't live at home and college expenses might

be paid for leaving the 50-somethings with some extra cash most would find it tempting to buy a third car for the household or a boat for the weekends will that extra money be put towards retirement goals without self-discipline it's not likely unless funds are diligently set aside by stewards who have their financial future in mind without a proper plan near retirees will probably just spend their extra cash inflow on insignificant things continuing the trend that might have sailed them through their entire working career people in their 50s can't afford to continue increasing their expenses to

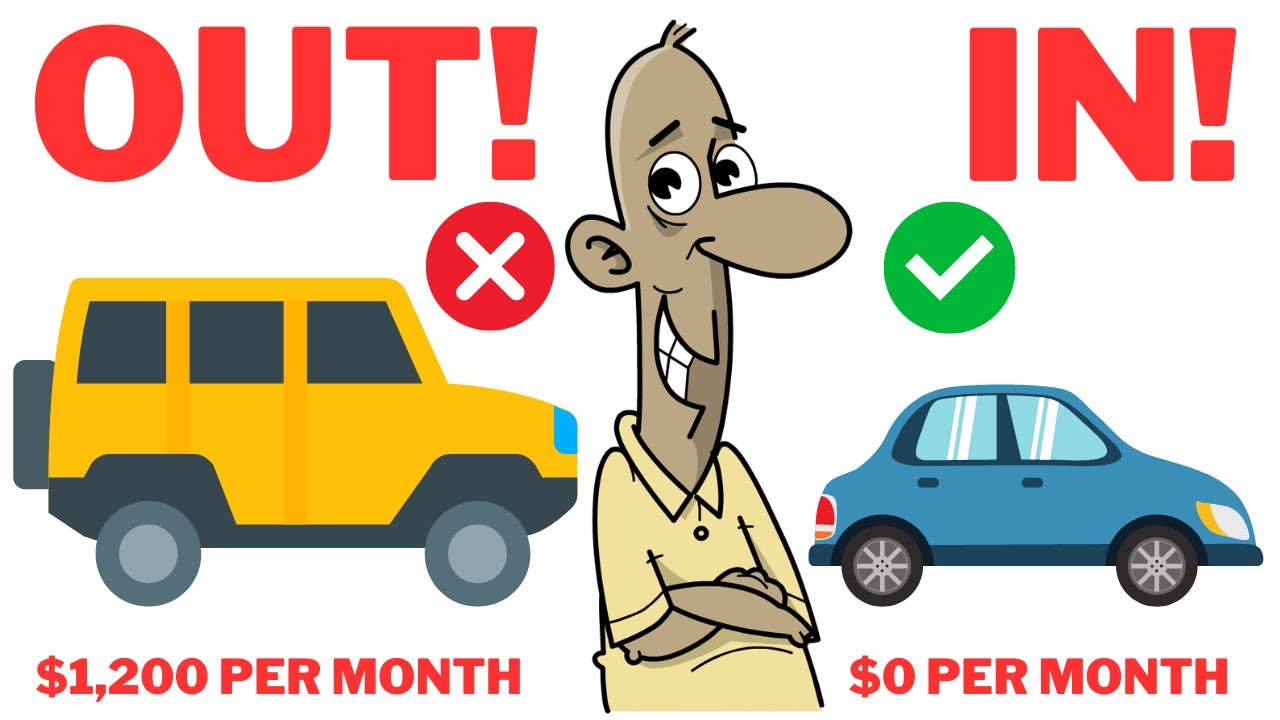

meet their income and expect to live the same lifestyle in their later years unless they plan on receiving a pension large inheritance lottery win or some other form of income luckily limiting and managing it can be pretty simple lifestyle inflation starts small ordering lunch out an extra day every week splurging on the latest phone buying slightly more expensive jeans or hiring a housekeeper to clean your home once a month those seemingly inconsequential expenses have a tendency to develop into larger and more expensive items such as a bigger home tied to a 30-year mortgage a new

luxury car and more tropical vacations those expenses are particularly dangerous when they come with monthly payments the new car is fantastic during the first few months of ownership but what about in five or six years when you're still paying for it while some splurges here and there won't wreck a well-formed budget be aware that small things tend to develop into bigger and more expensive things that will keep you too busy working that you won't even realize what's happening it takes discipline to stay on track with your financial goals and keep your eyes on the prize

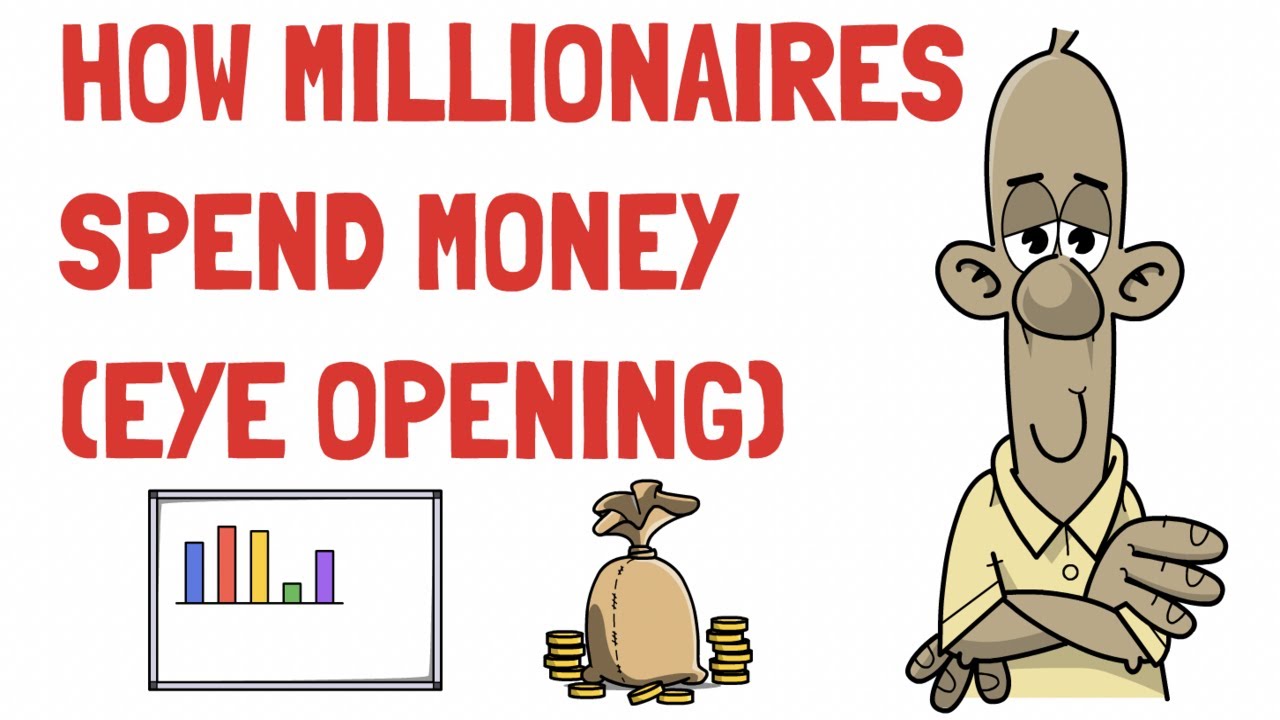

of a comfortable retirement it's smart to take note of the spending behavior of the rich wealthy people don't spend a large percentage of their income the way the middle class does a study by business insider found that the median millionaire spends 90 000 per year while earning 250 000 per year meaning their savings rate is an impressive sixty four percent it's certainly easier to save more of your income when you're making a decent living but the point is that these millionaires aren't spending anywhere close to what they're earning these wealthy people will tell you that

the satisfaction doesn't come from actually making a purchase it comes from knowing they have the ability to purchase an item the best way to manage the common issue of lifestyle inflation is to first recognize it do you really want to spend all the extra money you earn or to provide more satisfaction down the road when directed towards future financial goals if your goal is to become financially free you're going to want to plan for any extra money such as using it to pay off your home mortgage and fund your retirement accounts from our example when

bob gets that fifteen thousand dollar raise he might choose to invest all fifteen thousand dollars which would be fantastic if that would help him with his future goals however a more reasonable and sustainable decision for him to make is to invest twelve thousand dollars and spend an extra three thousand dollars this way he gets the best of both worlds money set aside for future use and a little spending money now for materialistic satisfaction spending a small percentage of increasing income isn't a bad thing because it allows you to enjoy your accomplishments by paying for a

fancier vacation now while still bettering your future ensuring a lifestyle is sustainable for years to come the reward of immediate satisfaction could make it easier to put in those extra hours at work if every time you get a slight increase in pay and you feel inclined to race out and spend the extra money on a new car or a bigger mortgage payment without setting a majority that money towards bettering your future it's unlikely that you're ever going to become financially independent everyone who's built wealth knows that it's critical to keep a portion of your income

to fund your future allowing your lifestyle to creep up slightly is fine as long as you're not like bob and don't become dependent on that extra income if bob decides to step down from that promotion to be able to spend time with his family he wants to have something to show for it when receiving a larger paycheck consider it safe to spend a small chunk of that extra cash while investing a majority keeping your eyes and the prize of financial freedom is more satisfying than the instant gratification of a needless purchase you