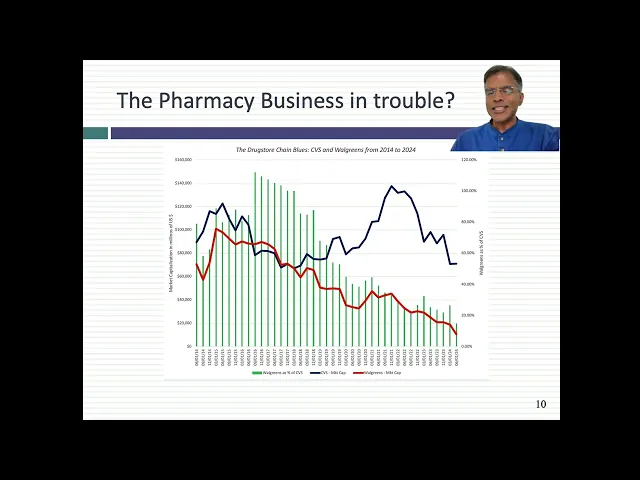

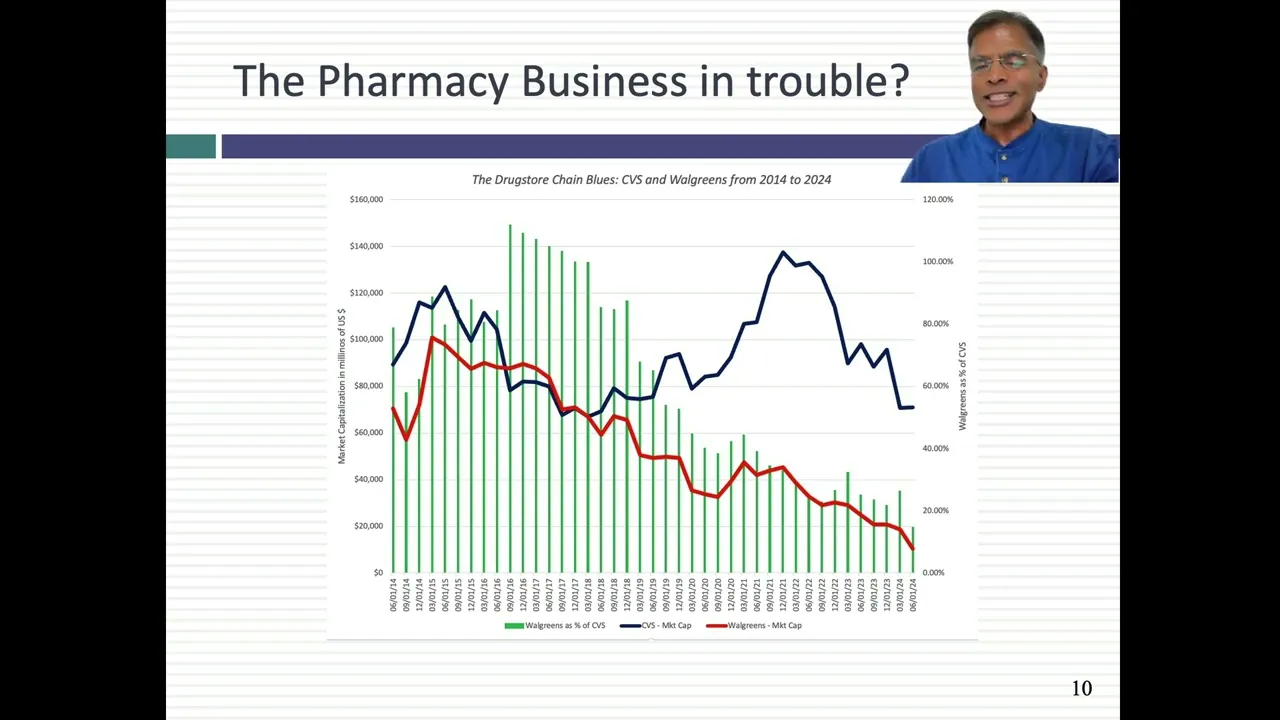

hi welcome in this session I'd like to talk about three companies all of which I think are household NES the first is Intel until very recently a tech Superstar but it's fallen in hard times the second is Walgreens if you've lived in the US or you visited the US you've noticed a Walgreen Pharmacy pretty much around every corn Corner second largest Pharmacy chain in the US and the third is Starbucks and no matter where you live in the world it's a company that's reinvented coffee much to the dismay of the Italians who truly own that right what do they share in common they're all in trouble how much trouble we look at the differences across the companies but clearly the market has turned against them and I want to use this session to talk about what it is that these companies are dealing with and more generally how companies deal with decline this ties very closely to the session I did a few weeks ago on the the corporate life cycle when I published my new book on the corporate life cycle where I talked about how companies age startup is like a baby a to Young companies like a toddler you have high growth companies and you have middle-aged companies mature companies and then you get old you decline and like human beings I said declining companies fight aging I believe that managing and investing in declining companies is often most difficult more difficult than investing in growth companies or mature companies the reason of course is very simple when you manage a declining company you constantly try to make yourself young again why because who wants to get old and companies don't either and you have bankers and Consultants telling you can be young again often giving you examples of other companies that have reincarnated so what I'd like to do is use Intel Starbucks and Walgreens to talk about deine as a process what the choices are and for these three companies at least what the best choices might be going forward both for management and for investors so let's get the show on the road as I said the one thing that these three companies have in common is over the last year or so these companies have all hit hard times with the market the market has turned against them in fact you could argue it's gone longer than that in this graph I've looked at the stock prices of all three companies starting in 2019 going through 2024 The Last 5 Years and over the last 5 years you look at the compounded annual return Starbucks has a compounded annual return of minus 1% a year this is a period when the market has been up 12 15% a year- 1% a year Intel - 18% a year and Walgreens - 30% a year clearly the market has turned against these companies for a variety of reasons and one of the things might be a slowing of growth and how the companies and investors are dealing with that slowing growth so let's start with Tech Superstar a company was that was founded in 1968 but really took off in the 80s and the 9s the one of the people who found it of course was Gordon Moore and you've all heard of Moore's Law and how quickly things change and how much the speed of a of a computer chip you know adjusts over time but the CEO who made Intel the company this today was Andy Gro incidentally Andy joined the company on the day of its incorporation in 1968 he grew with the company became a CEO and essentially helped make the company the superstar that is before he had to step down in 1998 in fact his theme in management was that companies need to experiment and stay adaptive one step ahead of the curve and his T the title of his book was only the paranoid survive arguing that no company should ever get comfortable with where it is perhaps an appropriate book for Intel to take a look at in 2024 now one way to understand how Intel has changed over time is look at its operating history and starting in 1994 this graph looks at the last 30 years it looks at Revenue growth and growth margins and operating margins Revenue growth of course captures the growth part of the business model and how that's changed you can see over time Revenue growth has decreased this is not a problem that started 3 years ago you can see in each decade now Intel's growth declining it's a classic case study of a company aging lower growth as it's get sces up the second met metric I looked at is the gross margin that measures the unit economics and on this Dimension Intel's unit economics have actually improved slightly over time not by much but the gross margin has gone from 56 to 60% at least through 2021 we'll hold off in the 2022 to 2024 and the bottom fell out on the operating margin again pretty healthy margins all the way through 2021 so all that happened in the last decade in intel was growth dropped off but the companies stayed incredibly profitable and then you get to 2022 and 2024 clearly the bottom is falling out Revenue growth goes into rever into negative territory the revenues are shrinking the unity economics seem to collapse and the operating margin is approaching zero at at a pretty fast rate clearly the company is in trouble now we'll look at what might have driven it there but as the operating metrics for for Intel have kind of deteriorated the market has taken notice in this uh table I've looked at the top 10 semiconductor companies B market cap every year from every decade from 1990 all the way through 2020 and then the last you know 2022 in 2024 1919 inel was the fourth largest semiconductor company in the world it was starting its rise by 2000 it ascended to the top it was the largest semiconductor company in terms of Market Gap it stayed there for 20 years that's a pretty long run for a tech company in 2022 dropped to Third and by 2024 it had dropped off the list and of course a superstar emerged Invidia had risen to the very top of the list they saying what went wrong now it wasn't that Intel you know in fact when you look at that table and and and the previous graph you're probably think why wasn't management trying something I think the problem is it was trying to do too much it was trying to do too much two Dimensions one was intel was investing heavily in its in its chip manufacturing business called the the the found Intel Foundry trying to match up to tsmc the biggest chip manufacturer in the world at the same time intel was investing immense amounts on the next new generation of ai ai chips because it wanted to claim market share back from nedia so clearly it was trying to get into both segments of the business and in my view it tried to do too much because it was you know in both both are big markets I'm not denying that but I think on both these markets intel was too late to the game and it given up too many advantages to these companies to go after them in the form that it did a benign reading of course of the Intel Investments is that we're not giving Intel enough time and that the Intel Foundry and the AI chips are going to come out and it's all going to be okay again that's not the assessment the market seems to be making and not so benign reading is that Intel's throwing money at at trying to be me too with these successful companies and that it's going to be money wasted so let's hold that thought that's the first of the three companies the second company is Walgreen Walgreens is an old company it's been a it's a company that was founded in Chicago in 1901 it's more than 120 years old it went public in 1927 it's been public almost 97 years and about 10 years ago in fact almost exactly 10 years ago it acquired Alliance boots to become you know to become a much larger company that it was before and get a get a a global presence that that acquisition we'll come back and talk more about it was was a hefty came with the FD price tag 15. 3 billion let's look at how all this played out in the operating metrics again as with Intel I broke down Revenue growth gross margins and operating margins by decade very business already right if you if you compare the gross margins for Walgreens against that of intels much lower gross margins the unity economics is just not as powerful in this business it's not the company's fault it's the nature of the business remember the heart of Walgreens is their farmacy business and the cost of the products they sell is a significant portion of their revenues but if you look through 2021 again I mean there's a slowing of growth but the margins are holding up pretty well though in the last decade you started to see both the gross margin and the operating margin dropped off and again you get to the last three years you get a much more significant drop off in the gross in the operating margin again clearly in the last 3 years something has happened at the company and the question is is it reversible what is it and to answer that question I decided to take a look at CVS you're saying why bring CVS in the picture remember I said that Walgreen's biggest business is the pharmaceutical business it's the pharmacy business business and the the largest Pharmacy company in the US of course is CVS and I wanted to see how much of the problems we see in Walgreens is business-wide and how much is company specific and if you look at what happened to CVS over the last couple of years you see the drop off in market cap in CVS the difference though is Walgreens market cap collapse has been much more dramatic in fact for a brief period in 2016 Walgreens had a market cap that exceeded CVS's market cap now its market cap is 1110th of the market cap of CVS what does that tell me Well it tells me that the pharmacy business is in trouble but Walgreens has brought on other troubles on top of the pharmacy problems because its stock prices has performed so much worse again you might say well why wasn't management doing something I think it was and but I think it was doing some of the wrong things in 2021 Ross Brewers brought brought into um Walgreens from Sam's Club and she was given this mission of turning the company back to being a growth engine and one of the things she decided to do was to go out and do Acquisitions to acquire growth now if you've listened to me enough you know that I am pretty cynical about growing through Acquisitions the session I do in Acquisitions is called acquires Anonymous seven steps to sobriety gives you some insight on what I think about Acquisitions it's a value destroying exercise for the most part and one of the the things that Miss Brewer bought was Village MD a chain of doctor practice and Clinics and you can already see why right one reason CVS was able to survive the kind of drop off in Pharmacy business was because it had those Minute Clinics in CVS and this was Walgreens attempt again at me tourism that acquisition though cost 5. 2 billion and over the 2 years that the that Village empty has been part of Walgreens it hasn't worked that well in fact in 201 24 Village MD scaled back its growth plan saying hey this business is not as lucrative as we thought it was so again it's not as if management is not trying perhaps they're trying too hard to go back to something that they cannot do so let's talk about Starbucks right I get a Starbucks cappuccino once in a while and um it is quite clear that this company whether you like it or hate it has changed the way we drink coffee fact just as an experiment I went into you know an Italian you know how in Italy they have cafes all over the place with they Ser you know espressos and I went and asked him asked the the gentleman behind the bar whether he would give me a grande caramel macchiato with oat milk he looked at me like I had two heads and he said you know we have espresso we have a cappuccino and I said what if you I want a large cappuccino he said then drink four cappuccinos and that's the difference Starbucks has made is we think think every coffee shop delivers coffee in in in cups the size of Alaska it's huge cups and in 15,000 different varieties early on Starbucks of course you know the the the the name you associate with the Starbucks story is how it shows right you probably might have read his book about know his story for the his notion of Starbucks was a coffee shop so people could gather together have coffee talk to each other he wanted to bring that Cafe experience to the US and he did by opening more and more stores there was a point in New York where you know around NYU in a six block area we had eight different Starbucks you know you could you could just walk from one to another within 3 minutes know they were cannibalizing each other Schulz of course was CEO from the company from 1986 through 2000 but he didn't go away right now he came back again from 2008 to 17 to rescue the company and then you know he left in 2017 but then again he came back in 2022 because Kevin Johnson was the CEO retired and they had no CEO and he filled in until lakman nimman became CEO in 2023 and of course to complete the story after the troubles that Starbucks has had in the market Mrnurman had to leave and we have a new CEO we'll talk more about whether that's going to change the story but again let's start by looking at the operating history and Starbucks the history is a little different than the Intel and and um and Walgreens graphs we saw a big drop off in operations in fact if you look at the Starbucks numbers you really don't see a dramatic drop off between 2022 and 202 it's true Revenue growth is a little lower but not by much right 7.

87% was the 9. 52% in the previous decade gross margins dropped a little maybe the unity economics are a little worse the operating margin a little drop off again so you're saying what's causing the angs will come back and address it but clearly you're not seeing a dramatic drop off in any of the numbers in the last three years there is if you shop at Starbucks so you probably have noticed a pattern now 5 years ago 10 years ago to order Starbucks you had to go into the into the store you ordered the you stood in line you ordered the coffee you got the coffee off and you you sat there and drank the coffee now increasingly though we order our cappuccinos a lot a caramel mariados on our phones and we go in and just pick it up that online ordering model and you can blame Co for this after all we blame Co for pretty much everything under this sun it's kind of changed the business model at Starbucks I think last year almost a third of the revenues came from people ordering online and picking up at the store and it says a logistics of a coffee shop in fact if I stood in line and ordered a a cappuccino it's Starbucks I'm going to be pretty pissed off because you'll have 15 online orders being filled while you're waiting for your order to be delivered it's changed the nature of Starbucks a company and you could argue that perhaps it's changing the storyline and that might be Starbucks biggest problem Starbucks no longer knows what it is as a business and that might be getting in the way of the market attaching a value to it in fact one way this has played out isn't a good way if you look at Starbucks at at its at it you know pre 2008 when they were opening a store you know blocks from each other you know you weren't getting very much in terms of growth from same store sales you're getting growth from opening new stores over the last 10 years 15 years that's changed right now Starbucks gets more sales per store than it ever has so in some way starbu is healthier than it used to be and the Ang I think then has to be what is it that making investors so upset with Starbucks one is I think Starbucks has acquired an investor base that believes it's entitled to growth that they bought a growth company and the company should be delivering growth and Starbucks is stried right the let's face it for Starbucks to deliver the kind of growth it can't be in the US it's a saturated Market the two big markets where Starbucks can go to get additional sales China and India in India Starbucks has kind of cut off that route by having a joint venture with with the Tata group so the real Market that Starbucks was hoping to use to fill in their growth plans was China and in China Starbucks has faced a challenge because Chinese domestic coffee makers like luck and Coffee underprice Starbucks and the Chinese consumers are not as willing to pay Starbucks prices so it's not showing I mean so it's it's relative Starbucks is still growing but maybe not as much as these investors thought they were that's the first one the second is and you all you all know how much I think about you know stories and narratives how a company is not selling numbers it's selling a narrative I think the Starbucks narrative is broken that for a long time The Narrative of being a coffee shop and growing through people coming into the coffee shop was what drove the company right now I'm not sure what the Starbucks narrative is what are they trying to do and I'm not sure Starbucks know knows what its narrative is and that can become an issue in markets and I think it has become an issue and finally I think inflation has had a toll when you order a venti latte cost you $6 you order a venti specialized drink and you had three different things it could be $8 that's a lot of money you know and I you know you could you could argue that that there's a cost issue that's getting in the way of growth as well so all of those things I think are undercutting the star message so with that lead in let's talk about you know what to do when you're in Decline I'm not sure Starbucks is in Decline but let's talk about what it is that makes it so challenging managing a company that is beyond middle Ag and I'm I'm using that word to be polite no old sounds so bad now there's a lot on this page so let me talk a little bit about what I'm trying to do here so let's say your company is entering decline here are the choices you face I've classified them into three groups destructive choices it it depends Choice which could be good or bad depending on how you structure it and constructive choices let's start with the destructive choices the most uh common destructive Choice made in the face of decline is denial where you you look at the decline you have in revenues and your margins coming and depression you always blame somebody else macro factors extraordinary circumstances bad luck it's always somebody else's fought and what do you do you do what you always done you keep doing your ex you stay with your existing policies investing financing and dividend policies cuz you're convinced everything's going to become okay the if you do that and you're truly in Decline the outcome is almost predictable right the truth eventually catches up with you but not before you've sunk tens of millions even billions of dollars into a business that is really uninvestable that's denial second is desperation desperation you realize your basic business is in Decline but you're desperate to go back to growth so what do you do when you're desperate you throw stuff at the wall hope something STI you make big bets this is where Acquisitions come in right and your Bankers will Aid and a bet this process by saying you can do it enter this business you make big Bets with low odds hoping for aead now clearly the outcome here for owners is almost never good you write off those Acquisitions but for managers there is a silver lining in this approach because if those bets play off because even low odds sometimes pay off these managers become Superstars so you denial you got desperation let's talk about survival I misspelled survival but I'll fix that survival at any cost I'm not a great fan of sustainability by itself where you know especially corporate sustain I understand that you want to sustain the planet we're all stuck on this planet we want it to be sustained but sustaining a company at any cost that's a terrible objective to have but if survival at any cost becomes your objective here's what you do you realize your core business is in Decline but you keep the company going because you think your job is to keep the company alive so every every Financial policy you take will be to ensure your company survives as an outcome what's going to happen you have what are called Zombie companies companies that are Walking Dead that companies that survive but they're in bad businesses and they leak value over time those are the destructive choices there's a n depend Choice me tourism what do you do in me tourism you know that your company is declining but maybe there are other companies in your pure group that are not so what do you what you effectively do is I think human nature you try to imitate them you try to do what they do they think of what Intel did in 2021 right they tried to be like tsmc and try to be like Nvidia because they were successful you saying what's wrong with that it could work right but in most cases you're coming to the game late there are established players are better at this than you are and you often end up underperforming and then you have constructive choices and let's look at the three constructive choices the first is accepting where you are in the life cycle and behaving accordingly so you know your com business is declining it's not a great business you know what you need to do right the sensible thing to do if you're an acceptance is you not just invest less you start divesting you start to shrink as a business you bring down your debt you return more cash to your investors you saying but that'll make my company smaller you're okay with that it's better to be a small company in a bad business than a big company that's acceptance easier said than done but for many companies the most healthier choice you could try for a revamp basically what you do is you take your business you accept that it's in Decline but then you try to take your product and service and you either redesign it or you go after new markets not hoping to go back to growth but at least to go back to some mature face where you can keep going with reasonable growth you know so your company reverts back to an earlier life cycle but in a in a slightly different form than the existing one and that is the dream for every company in Decline maybe I can be born again reincarnation Apple in 2000 Microsoft in 2013 you use the cash flows from existing business to enter some new and extraordinarily high growth business so you seek out a new business we can enter with your strengths you invest and grow your businesses and over time you reinvent yourself to become a different company now when you look at your company saying how do I know which one is right for me the are the things that are going to play in first is are you a declining company in a healthy business it's easier to devise Pathways back if you're in a healthy business because there are then the market itself is Big the business is healthy but if you're a declining company in a business everybody's declining much more difficult to P off second do the decision makers in the company have skin in the game do they own Equity it's easy to make big long OD Bets with other people's money if it's your own money you're got to be a lot more cautious the third is when you're in Decline management starts to matter more again if you're a middle-age company or a Growth Company you can get away with an with with AI running your company management quality is most critical early in the life cycle and late in the life cycle do you have the right management and does it fit your company the fourth is does your company have any strengths the fact that you're in Decline doesn't mean you don't have strengths your pathway back has to be built around those strengths and what those strengths are fifth who are your investors are they in a hurry if they're in a hurry they're going to push you down the pathways where they get the cash back a lot of declining companies end up with a private Equity investor often an activist in the ranks makes it much more difficult to say I want to revamp or reincarnate if you have those investors it's easier to devise Pathways back to health if you're in a capital Market where where capital is accessible and it's healthy and finally external factors come in governments for instance know what can governments do well remember after 2008 you're too big to fail governments actually came into declining companies gave them capital and kept them around and you could argue that this is a factor that you know sometimes can make a difference and leave declining companies continuing and that's not often good for the sector and finally luck much as we'd like to act like everything is in our control luck can play a factor in what happens as well this is the framework I'd like to use to look at the three companies that are part of this exercise so let's try this out on our three companies let's start with Ina in my view Ina's prom stem from the fact that they tried to be not just me too but me too in a very big way on both Ai and the chip manufacturing business Intel not just going after Nvidia and tsmc but trying to supplant them be as successful as they are and I don't think they can do that because I think inedia on AI and tsmc have competitive advantages it will make them the leaders but that doesn't mean that there's no hope left these the business is big enough the a market is big enough and the chip manufacturing business is big enough that Intel can grow but under a much more modest space so it's almost like they need to bring their Ambitions down not try to to be leaders it's tough to do when you're a company like Intel which has been at the top for so long and to reflect this I actually tried valuing the company with modest growth and not that high Mar a margin and see if I could get to the $18. 89 cents per share the stock was trading at and if you look at the table there you can see that with a 3% Revenue growth in a 25% margin I get a value per share of 2370 the higher than the price 3% of course is low Revenue growth and a 25% margin is actually lower than the margin Intel used to earn in the last decade so I'm not asking for much in fact you could probably get that combination without succeeding in the AI Market or the chip manufacturing market and even if they can get some success there not even the kinds of top level success they want it's icing on the gate I think the odds are in my favor with inel and I did buy until at 1889 with Walgreens so I think the problem some more intense with Intel at least the rest of the business is healthy even though inidia might be taking a disproportionate share of it with Walgreens a pharmacy business and you saw this with the graph it's broken it's being disrupted and I don't think it's going to come back any time soon does that mean in if Walgreens is doomed not necessarily again I think they they could shut down their least you know least productive stor you know shrinking their presents down to a smaller presence they can surv VI but I have to be realistic when I value the company and I think it's all going to boil down to what the margins will look like in this slim down version of the company in fact if you look at the values that I got per share with 2 or 3% operating margins I end up with values not just below the 877 the stock was trading at but often a negative territory which means the company will not make it I need margins of 4% or higher to get to values above 877 and while there's PL there are plausible paths to get there I'm not willing to make the bet I think the odds are less with me or perhaps more against me on this one so I'm going to steer away from Walgreens which brings me to Starbucks and I'm not sure strabucks ever belonged in this Trio if you remember Starbucks was the only one of the three companies didn't see a collapse of margins the last three years it did have slightly lower growth but I do think it's lost its storyline and I do think that that's going to be the task for the future whether they can find a narrative that investors can latch on to however to set that narrative you need a Visionary and as many of you might know in the case of Starbucks they have a new CEO in place a gentleman named Brian niichel who came to with pretty good know with a pretty good pedigree he's um he's run Taco Bell and chortle and I think he was hired by the board because he had that Logistics experience but does he have the vision we're not sure yet because he hasn't given us that vision that he has for Starbucks and the initial news stories are not exactly promising and you probably read some of them of him living in Southern California and flying by corporate jet to Seattle to run Starbucks I don't think you can be a Visionary CEO and a parttime CEO at the same time but maybe I'm being a little unfair here but as an investor I look at Starbucks and I'm not that excited to to buy it at 9115 in fact I tried valum Starbucks with the combination of growth and margins reflecting different parts of their history in fact if I give them the margins and growth they had in the last three years the value per share I get is 55 well below the 91 if I give them the higher growth and the higher margin they had in the last decade I'm still at 64 if I go to the the 16% growth rate they had between 2 and 2 2011 but the lower margins I'm at 48 like the only way I can get to 991 is if I give them the growth they had between 2002 and 2011 16% and the margins they had between 2012 and 21 15.