hey econ students this is jacob clifford welcome to the microeconomics unit 2 summary video i've made a bunch of individual topic videos to help with all the concepts in this unit but this summary video is designed to get all the concepts back in your brain and get you ready for your unit test or your final or the ap exam so by the end of this video you're gonna have all the concepts back in your head and the way we're gonna do that is with the study guide from the ultimate review packet you're gonna fill this out along the way so make sure to go get this download it and put it out because you're gonna be using that in this video remember i'm using the ap economics curriculum but if you're in a college class you're trying to pass the club it's all the same stuff this is all introductory microeconomics i'm going to start off with demand and then supply and then elasticity with elasticity demand elasticity supply and the two type of other elasticities cross price and income then i'm going to talk about equilibrium and consumer and producer surplus then how these curves shift and changes in the market then we'll talk about price ceilings floors taxes subsidies government intervention and finish it off with international trade okay that's what we're doing so let's do it by this point you feel extremely comfortable with the idea of demand downward sloping show an inverse relationship between price and quantity and remember that happens for three reasons the substitution effect the income effect and the law of diminishing margin utility if the price falls then people are going to buy more because they're going to move away from substitutes substitution effect if the price goes down people are going to buy more because they can buy more that's the income effect and to get people to buy more you've got to lower the price because they get less additional satisfaction from each additional unit law diminishing margin utility this is worth at least 50 noodles and that's completely different than the five shifters of demand these are things other than price that cause the demand curve to increase or decrease these are all things that affect buyers and consumers there's nothing that affects production here because that's supply and inside here there's only two things you got to keep track of remember inside the price of related goods there's substitutes and complements and inside income there's normal and inferior goods you probably feel really comfortable with that so right now take out the study guide and fill out topic 2. 1 demand verify you know those shifters and make sure you can practice what happens when there's a change in the price of a substitute how does it affect the other good topic 2. 2 is supply and again we're talking about production and producers it's got an upward sloping supply curve showing a direct relationship between price and the quantity supplied the reason why it's upward sloping is because an increase in price gives producers an incentive to produce more because they can make more profit and here are the shifters notice that the price of the product does not actually shift the supply curve but the price of resources the inputs to producing the product does shift the supply curve and the thing you got to watch out for here is an increase in supply is always a shift to the right it never goes up don't think of that that's a decrease in supply for example when the government gives a subsidy which is money to producers to produce more that causes supply to shift to the right that's an increase in supply now a tax on producers that would decrease supply shifting supply to the left i'm sure you got it take out the study guide and fill out topic 2.

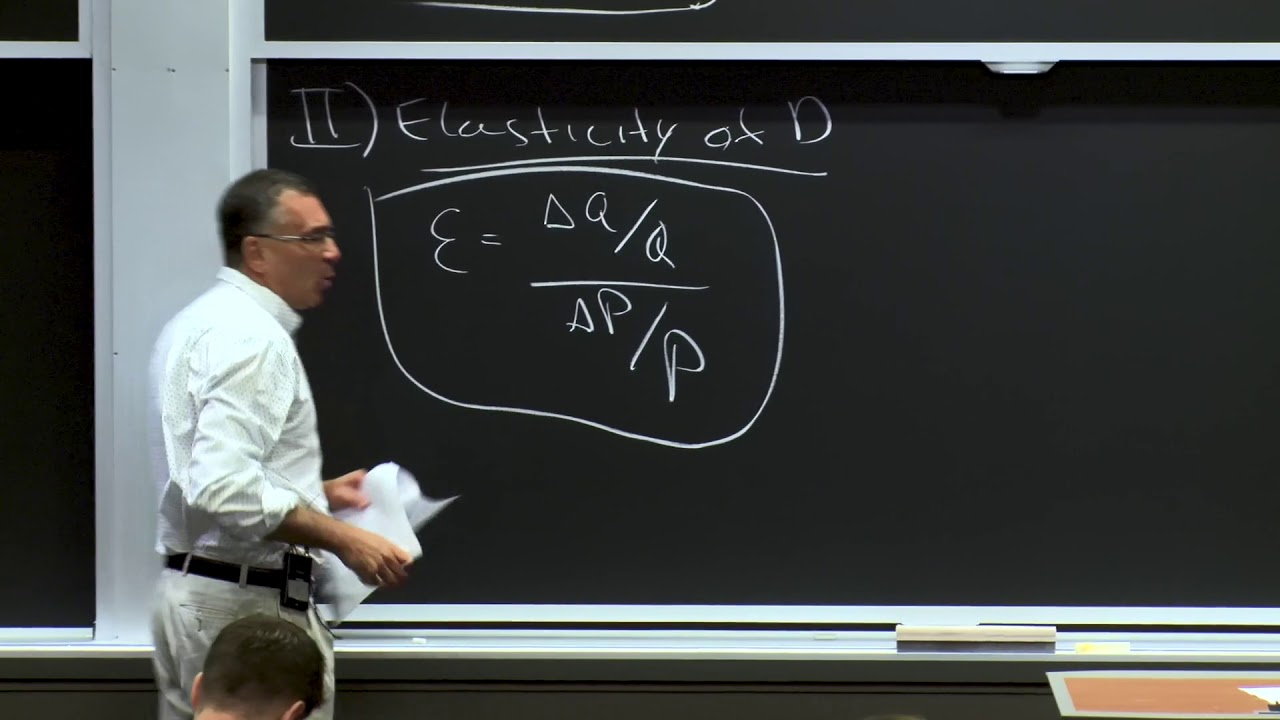

2 for supply make sure you know those shifters a lot of the time your teacher is going to move to putting supply and demand together but before we do that let's jump into elasticity and remember there's four types of elasticity and four different equations you've got to know elasticity demand elasticity of supply cross price elasticity and income elasticity they all show the same idea they show how sensitive quantity is to a change in price and show you the shape of the demand or a supply curve if the demand is really steep then that shows that quantity is insensitive to a change in price so a big change in price leads to a small change in quantity if a demand or supply curve is real flat then quantity is very sensitive to a change in price a big change in quantity from a small change in price and if the quantity changes by the exact same amount as the price then that's called unit elastic that's a gross oversimplification because really it's not about the slope of the demand curve you actually have to do the calculations because on the same demand curve you might have down here that is more inelastic and up here that's more elastic it all depends on the numbers so just remember elasticity is not the same as slope and remember these numbers mean something so if the number is zero that means the demand is perfectly inelastic people are gonna buy this no matter what when the price goes up they're gonna buy the same amount if it's less than one it's relatively inelastic if it's one unit elastic greater than one it's relatively elastic and the last one perfectly elastic and you need to understand that there's reasons for this if the demand is more inelastic that's because it has few substitutes and it's a necessity if it's elastic it has a lot of substitutes and it doesn't really matter if you get it now or get it later when you're looking at the elasticity of demand you can also use something called the total revenue test it only works for demand it doesn't work for supply if the price goes up and the total revenue goes up or if the price goes down total revenue goes down the demand is inelastic if price goes up and total revenue goes down if price goes down total revenue goes up then the demand is elastic so on a test your teacher's probably gonna say okay here's the price it was ten dollars it fell to eight dollars and the quantity increased from 10 to 15. what's that demand curve elastic or inelastic so there's two ways to get the right answer one is looking at the elasticity coefficient that shows you a 50 change in quantity from a 20 change in price that means the demand is elastic because the elasticity coefficient is greater than one or you can use the total revenue test the total revenue before was 100 the total revenue after is 120 price went down total revenue went up elastic demand the point here is make sure you can do the calculations for the elasticity coefficients make sure you understand the total revenue test and make sure you know what those numbers mean topic 2. 4 is elasticity of supply but it's a lot of the same stuff you saw in topic 2.

3 elasticity of demand but instead of looking how sensitive quantity demanded is to a change in price we're looking how sensitive quantity supplied is to a change in price and again that's giving you the shape the curve so vertical is perfectly inelastic supply and then relatively inelastic supply unit elastic relatively elastic and perfectly elastic supply but unlike demand the cause has nothing to do with substitutes and how much people actually want this it has to do with production if a product is relatively easy to produce and resources are available then price goes up the client supplied increases a whole lot elastic supply but if a product is hard to produce takes a lot of time to produce it and the price goes up you can't produce that much more and so quantity supplied increases only a little that's relatively inelastic supply and of course a vertical supply curve means it doesn't matter if the price goes up we're still only ending up with a certain amount we can't produce any more in topic 2. 5 we have cross price elasticity and income elasticity and the equations are pretty much the same as you've seen before for cross price it's the change in the quantity of one product relative to a price change in a different product remember it tells you if two products are substitutes or complements and for income elasticity it shows you the change in quantity from a percent change in income and this shows you if the good is a normal good or an inferior good the one thing to watch out for is notice this is the percent change in quantity and the percent change in the price or the income we're not talking about the raw chain so be careful when they give you the numbers makes you have to calculate percent first i know i'm going really fast through that but you've already seen my other videos and you get a chance to practice right here on topics 2. 3 through 2.

5 on the study guide so fill out that whole section if you can do that you totally get this okay here in 2. 6 we can finally put demand and supply together you come with equilibrium and you understand the idea of consumer surplus and producer surplus consumer surplus is the difference between what people are willing to pay what they actually did pay and producer surplus is the difference between the price and what sellers were actually willing to sell it for when you put consumer and producer surplus together that gives you the total surplus and when this is maximized a market is efficient but what happens if we produce less quantity we end up over here well we end up with dead weight loss which is lost consumer and produced surplus and an inefficient market remember you're going to see dead weight loss a whole lot and you can have it on either side so if we produce too little we end up with deadweight loss here if we produce too much you can also have deadweight loss over here but let's go back to consumer and produce surplus there's a difference between being able to spot it and be able to calculate it make sure you can do the calculations and understand it's one half base times height to give you that triangle so you're gonna have to practice so take out the study guide fill out topic 2. 6 calculate that consumer and that produces surplus now topic 2.

7 is probably the most important one because now you have to take supply and demand start shifting and identify what's gonna happen to price and quantity in the market it starts off by talking about disequilibrium so remember when the price is below equilibrium we have a shortage because the quantity demanded is greater than the quantity supplied when the price is above equilibrium we have a surplus because the quantity supplied is greater than the quantity demanded again a way to help you remember that idea is when the price is below equilibrium it's short that's a shortage and remember the price never shifts the curve a change in the price doesn't shift the demand or the supply at all it just moves along the curve changing the quiet demanded and the quantity supplied not the demand and the supply and that's one of the things your teacher or professor are totally gonna test you on they're gonna say okay if the price goes up for corn what happens to the demand for corn the answer is nothing the demand does not change only the quantity demanded so if the price goes up for corn the quine demanded will go down and we'll move along the curve but it does not shift the curve every year some students like no no you said price does price of substitutes or the price of resources yes price of substitutes affects the demand price of resources affects the supply but the price of that actual product does not shift demand or supply so here's a little trick for you whatever's on the y-axis that doesn't shift the curve so if a change in price occurs that doesn't actually shift either of these curves if this was wage up here wage wouldn't shift the curve that'll probably make more sense we get to future units but just remember price does not shift demand or supply don't forget race and shift the car yar thank you okay now let's talk about shifting these curves it looks complicated but remember there's only four things that can occur demand can go up demand can go down supply can go up or supply can go down and in each of those situations there's gonna be a change in the price and the quantity and that's the most important thing the thing your teacher wants to make sure you understand how to do if there's this change in the market what's going to happen to price and quantity now i don't really have an acronym to help you okay if supply increases the price goes down quantity goes up don't do that instead when in doubt draw it out draw the graph every single time it'll give you the right answer and when there's a double shift you can do the same thing when the demand goes up and the supply goes up at the same time you're going to find out that two different things are going to happen price goes up quantity goes up when the demand goes up when the supply goes up price goes down and the quantity goes up when you combine those results you get the result of a double shift quantity is going to go up the price is going to be indeterminate remember that's the double shift rule when two curves shift at the same time one of them either price or quantity is going to be indeterminate how do you know which one draw it out now i covered that pretty quick and to make sure you got it fill out the study guide topic 2. 7 make sure you can show shortage surplus and show the four different shifts occur and double shifts if you can do this you totally understand the basics of supply and demand okay now we're jumping into 2. 8 which is going to take all the concepts you learn shortage surplus consumer surplus produce surplus shifting these curves and put them all together and talk about government intervention it starts off pretty easy with price ceilings and floors remember it's the opposite of what you normally think a price ceiling if it's binding must go below equilibrium and a price floor has to go above equilibrium to be binding to have an effect on the market if a ceiling is above equilibrium or a floor is below it has no effect price and quantity will stay exactly the same did you get that because i promise you that your teacher or professor is going to make sure that's on the test they're going to put a price ceiling above equilibrium and say okay what's going to happen you go oh there's going to be a surplus nope a price ceiling above equilibrium is not binding it has no effect on the market so here's the rule when you're taking your test and you see the word price ceiling or floor ask yourself first before you do anything else is it binding is it in the right spot price ceiling is a maximum the price it can't go up to equilibrium we end up with consumer surplus produce surplus and deadweight loss a price floor is a minimum on the price it doesn't let the price go down and again we end up with consumer surplus producer plus and deadweight loss and remember your teacher is not just going to ask you to identify those areas you have to actually calculate those areas as well now for most students the hardest part in this entire unit is you go to the next level up and you start looking at taxes taxes shift supply to the left the vertical distance between the supply curves the amount of tax per unit and you end up with a consumer surplus producer surplus total resident goes to the government and deadweight loss i've made two different videos that talk about this concept and help you practice and there's a reason for that this is tough you're gonna have to sit down do those calculations find those areas and find those boxes and the problem here is there's so many different questions your teacher could ask that can say okay where's consumer surplus before the tax or consumer surplus after the tax how much of that tax revenue is paid by the consumers where is the tax revenue in general deadweight loss there's so many questions so you've got to see them all and you've got to practice them and the best way to practice is to fill out the study guide topic 2.

8 you've got the tax right here i gave you both the areas and the numbers so make sure you can spot the area and if you can also do the calculation to actually calculate consumer and produce surplus and get the numbers as well and there's a tax there's a box of tax revenue that goes to the government or a tax wedge and sometimes that's paid by consumers sometimes paid by producers and sometimes it's shared by both for example if the demand and the supply have the same elasticity the tax burden will be on buyers and sellers equally the way you can spot that is looking at the box and seeing how much dug into consumer surplus and how much dug in to produce a surplus watch what happens when the demand curve becomes more inelastic than the supply curve the consumers pay more of the tax they have bigger tax burden than those producers and if the supply becomes more inelastic than the demand then the burden of the tax goes on producers the best way to show it to is like this notice the supply curve is shifting the same exact way for every single one of these the only thing that's different is the demand curve and its elasticity when the demand is perfectly inelastic or vertical then consumers pay all of that tax now the demand is highly inelastic relative to the supply then consumers pay most the tax but producers pay some too when they have same elasticity they share the tax equally when the demand is more elastic than the supply then producers pay more of that tax and last one right here you can see producers pay all that tax and again the best way to remember this is not to try to promote some acronym is to draw the graph when in doubt draw it out drawing that demand of supply curve showing that tax box tells you okay who pays the tax for the majority of classes topics 2. 7 and 2. 8 are the most important and most difficult topics to cover in this unit make sure you can do those shifts show those areas and do those calculations okay the last thing we've got to cover is topic 2.

9 international trade again we're looking at consumer improves the surplus but now instead of a ceiling or a floor we're importing goods from another country like all the other concepts i made a topic video that talks about it in detail so if you need more help go watch that but here's the breakdown if we can buy a product at a lower price and if we produce it ourselves and the domestic amount we produce is here and the amount we're going to import is the difference between that quantity supplied we're going to make ourselves and the quantity demanded that people actually want so people are going to consume this amount that means consumer surplus will be here producer surplus will be here and there's no deadweight loss notice this is different than anything you've seen before because there's not a shortage right here instead we're importing goods from another country but if there's a quota or a tariff then that world price goes a little bit up so the consumer surplus gets smaller and the producer surplus gets bigger this is not really a hard topic it's just a re-application of concepts you learned earlier in the unit but like always make sure you can actually calculate the area of consumer surplus and produce surplus and identify how it changed when there's a change in the world price and if there's a tariff be able to spot and calculate the tariff revenue box so to make sure you can do that take out your study guide answer those 10 questions for topic 2. 9 international trade okay that was an overview of the entire unit you've got the whole study guide filled out of course there's answer keys in the ultimate review packet so go in there see how you actually did if for some reason you're like okay i don't understand that right answer go back and watch the topic video on that topic to verify you're getting it overall this is not a super hard unit in fact i would give it a three out of five in terms of difficulty but in terms of importance it's five out of five you've got to know supply and demand and be able to shift these curves and you're also going to see many of these concepts like consumer and produced surplus and deadweight loss in units 4 and unit 6.