[Music] So, welcome back to the Options Crash Course Strategy Series. My name is Jim Schultz. I'm glad that you are here with me today.

This is a very exciting moment because we are going to dive into the undefined risk category. We're going to do so headfirst with the short strangle. We’re going to follow the same protocols as what we’ve done with all the other videos up to this point.

We’re going to talk about managing winners, we’re going to talk about managing losers, and we’re going to talk about everything in between. So, let’s do it, and let’s begin with the structure of a short strangle. The short strangle is one of the simplest undefined risk strategies that you could select.

It consists of two legs: an out-of-the-money short call above the current stock price and an out-of-the-money short put below the current stock price. That’s it. Now, on entry, there are a few things that you want to look out for.

Number one: since this is a short premium strategy, it is best suited for a high IVR environment. Now, ideally, this would mean an IVR that’s greater than 50. But at times, an IVR that’s maybe 25 or 30 might be high enough.

There is definitely some flexibility here. Number two: specifically for strangles, we want to make sure that we collect enough on entry. We typically set our minimum bound around one dollar across both the put and the call.

The reason why is very simple: this is an undefined risk strategy, so we want to make sure that we are fairly compensated for taking all of that risk. Number three: also specific to a strangle, a great starting point for your strike selection would be somewhere around the 16-delta mark—a 16-delta short call and a 16-delta short put. This is a classic one standard deviation strangle.

Use this as a reference point to determine where you want to select your strikes. You may want to collect more premium; you may want to increase or decrease your probabilities. That's perfectly fine, but starting with the one standard deviation strangle is a really great foundation.

All right, so now we know how these guys set up. Let’s get to the fun stuff: managing those winners. This is going to be pretty simple.

This is going to be the same procedure that we have followed with our other short premium strategies, such as short verticals and iron condors. We take these guys off at 50 percent of max profit. So, for example, if you sell a strangle for two dollars, you’re looking to buy it back for one dollar.

If you sell a strangle for a dollar fifty, you’re looking to buy it back for 75 cents. It really is that simple. The one thing that you want to make sure that you do here, though, is don’t take the legs off separately.

Don’t lag out of the trade. Our research has shown there’s no long-term benefit to doing this, so keep it very simple: one package off as a package. All right, what about these not-so-fun guys?

What about these losers? Well, I hope you have your Powerade Zero handy because you’re going to need those electrolytes. This is going to be a lot.

First up, if the stock is between your short strikes, don’t do anything. If the stock is between your short strikes, even if it’s moving around a lot, the strategy is working. Let it work.

It isn’t until one of the short strikes gets hit that the adjustment protocol to follow is triggered. All right, so what happens when the stock rallies and your short call gets hit, or the stock falls and your short put gets hit? It’s basically a three-step process with a fourth bonus step that you can execute at your discretion.

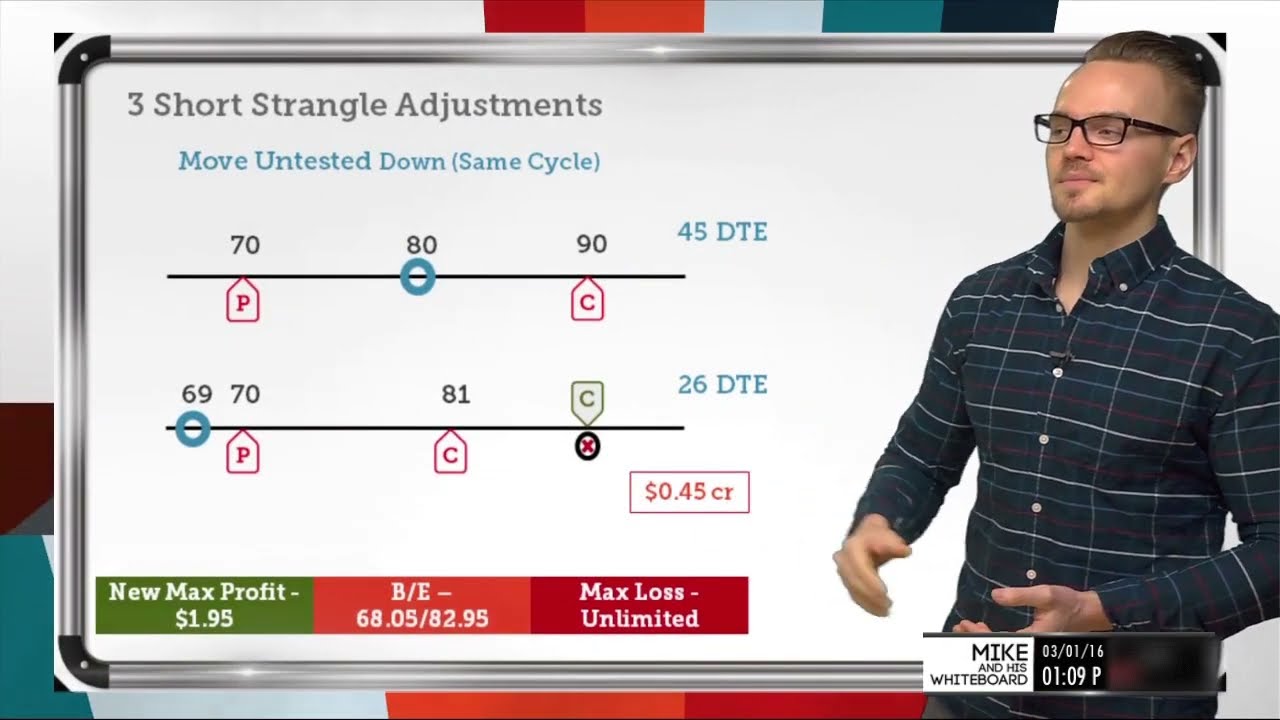

So, let’s get into it. All right, step one: you roll the untested side into a tighter strangle, where your objective is to reduce the magnitude of your deltas by 30 to 50 percent. For example, let’s say you put on that one standard deviation strangle to begin with, so you’re pretty delta neutral on trade entry.

Let’s say the stock rallies up to your short strike or maybe through your short strike. Now your position deltas might be around minus 50 deltas. What you would want to do is roll that short put up until you have trimmed the magnitude of those bearish deltas by 30 to 50 percent.

So, if you’re at minus 50, maybe you’re looking to reduce your deltas to minus 25 or minus 35—somewhere around that 30 to 50 percent magnitude reduction. The same would be true if the stock fell; you would roll your call strike down to again reduce the magnitude of your bullish deltas in this case by 30 to 50 percent. All right, so what if the stock still continues to move against you?

This is where you go to step two: you roll that untested side into a straddle. Now, if the stock is continuing to rally, you’re going to roll that short put strike all the way up until it shares the same strike as your short call strike. If the stock is falling, then you would roll the short call strike down all the way to share the same strike as the short put strike.

All right, but what if that’s still not enough? What if the stock continues to get away from you? The stock continues to move against you?

You go to step three: you’re going to want to go inverted with your strangle. This means you roll your put strike up above your call strike if the stock is rallying, or you roll your call strike down below your put strike if the stock is falling. Doing this will really help to control and mitigate your directional exposure.

The position now, naturally, if I was in your position right now, the number one question that I would have is, "Alright, Jim, how do I know where to set my inverted strike? " Well, to be honest, there is a lot of discretion that you're going to need to apply. There are plenty of pros and cons, plenty of gimmies and gotchas that you need to consider.

But here is a great reference point: consider moving your inverted strike to the new at-the-money strike. The reason why this is a great reference point, a great anchor in the sea, if you will, is that the at-the-money strike always has the greatest amount of extrinsic value. So if you move to that strike, you can be assured that you are maximizing the extrinsic value that you are collecting on the trade.

What you really want to be aware of here is the width of the inversion relative to the credits that you have collected, because your best-case scenario now is the stock stays between your two short strikes, and the two options are in the money. This way, you can buy back that strangle for the width of the inversion. So, for example, if you have a five-dollar-wide inverted strangle and you've collected seven dollars, if the stock were to expire inside of those two short strikes, both options would be in the money.

The total intrinsic value would be the width of the inversion: for five dollars, you collected seven dollars, so you would end up netting a positive two-dollar profit on the trade. You always want to be aware of this relationship because things are a little bit different now from what they were with a regular strangle. Alright, now that fourth step that I promised you—the bonus step—you can always roll out in time.

You can always add duration to the trade, and you can do this whenever you see fit. You can combine it with step one, you can combine it with step two, you can combine it with step three. So how do you know when is the best time to pull the trigger on this bonus step?

Well, remember, we typically like to keep our short premium trades around 45 days to go. So if there are still around 45 days to go in the current cycle, like 47, 43, 40, or 39, then I would consider sitting tight. But if you've gotten to a point where there aren't close to 45 days to go—maybe you're at 21, maybe you're at 25, maybe you're at 30—this might be a really good time to roll this position out, add that duration, and use this bonus step.

Now, a quick disclaimer: that entire protocol is a great guide to follow, and the reasons why are these: all along the way, at every step in the process, you are collecting credits, you are reducing risk, and you are widening your breakeven points. But is this the only way that you could adjust a short strangle? Absolutely not.

Are there other viable, successful ways to adjust a short strangle? Absolutely. But if you are brand new, if you are just gaining experience, and you are just getting your feet wet, then start here.

As you get some more exposure to the markets, as you gain that experience, by all means, man, tweak it, tinker with it, and make it your own. Alright, lastly, what about that dance floor? What about those trades that aren't really winners, they're not really losers, they're just kind of hanging out somewhere in the middle?

Well, this is pretty simple, and it's going to be very similar to what we've done with our other short premium trades: the short vertical, the iron condor. Look at IVR. If IVR is still high, if it's still elevated, then consider keeping it on.

But if IVR has come down, if IVR has collapsed, then consider taking it off. Alright, guys, man, you made it! That was a lot.

By all means, save this video for future reference; you might need to watch it a time or two, or ten, before it finally sinks in. And share it with a friend, man! Share it with one of your trader friends who is learning about undefined risk strategies, who is interested in short strangles.

That would be really, really terrific. And when you are ready, I will see you in the next video—the short put. We'll see you there!