using chip to investigate threats to the global supply chain and conversations related to these topics. As you know in chip we have the ability to look across global public discourse across a variety of topics, names, organizations, locations, descriptors and events. So if I come over here, I can see for example in January 2026 on X, we can see which are the most discussed topics and how have they changed month over month with topics related to Venezuela topping the list.

But I can also search for supply chain related topics and see which of those are amongst the largest. Here I can double click into threats to global supply chain and further investigate this conversation. Now here I can see that both on Twitter or X and on Instagram this conversation has been trending down going back to May with a couple of exceptions of increases between say September and October on both platforms.

Now, as we dive further into where and who this conversation is coming from, we can come over here to demo and geo and see the demos, regions, countries, and languages uh that are where and who these conversations are coming from. Now, for example, here I see that 20% of the conversation around this topic in January is coming from India. And a key part of all of our data is that we benchmark it to understand whether that percentage is above or below what we'd expect.

Sure, India is a large country, but is it a large country in terms of population on X across these topics? And so this percentile here helps me to understand that at 20%, this is well overindexed relative to expectation in the 91st percentile. So this topic skews way more towards India than other topics.

Let's see how the contribution from India has changed over time. Looking at the blue line here. So back in May about 5% give or take of this conversation uh was coming from India and that is really shifted over the last few months.

Look, it was at the 50th percentile as indicated by the green dot there. And as you follow the blue line on the raw percentage, you see it gets all the way up to 20% of the conversation in January. We have a pretty notable increase between December and January, almost doubling its contribution.

Now, if we look at some of the other countries, say US, you can see that back in May was pretty heavily concentrated with the US. about 63% of the conversations stayed around 50% uh after that higher contribution back in May and then really plummeted in January coinciding with that big increase in India's contribution. Now we can also look at other areas like go zoom out and look at Asia which of course we would expect that India contribution to be uh contributing to the fact that it went from 10 to 30% over these few months or look at Europe which we can see was at 10% and has also risen over the last couple months now at about 15% of the conversation.

We can also look at the demo. It's really interesting here to see 20 and under overindexed. But more interestingly is to see this trend.

Only about 4% of all threats to global supply chain conversations came from 20 and under earlier this year. And look at how much that has grown in recent months. And that big increase coinciding with India.

shows that a lot of younger Indian uh consumers or nisonens seem to likely be uh driving some of that increase that you see here. We can also look at say high income where we also see some growth here as well though a decline between the months of December and January. or even looking at 45 over where we see that was a much higher percentage of the conversation but in recent months going from October to January that percentage has significantly declined over time.

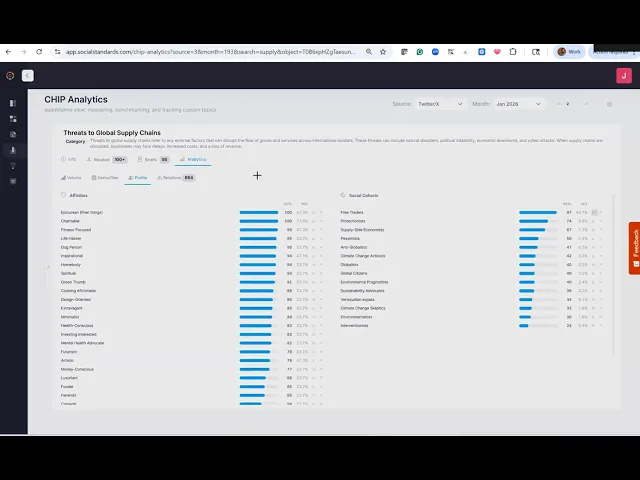

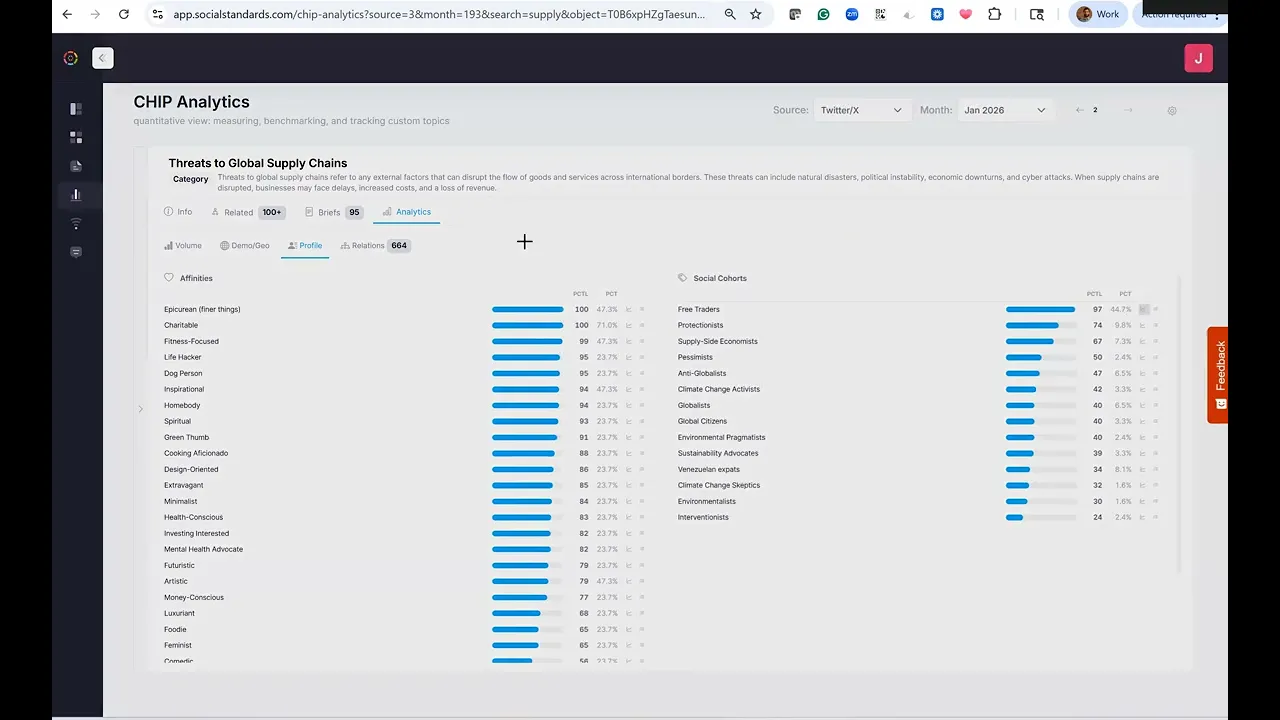

So really what we've seen is that threats to global supply chain conversation has shifted away from older US audiences to younger Asian and Indian audiences over time. However, if we think back, we need to contextualize and keep in mind that overall conversations have dropped over this same time period. Now, looking at the profile, the affinities and cohorts that these users fall within, we clearly see free traders are heavily overindexed in this conversation.

But it's interesting to see that the raw percentages dropped off that it was much more concentrated around this concept and cohort uh earlier this year at 76% and has since dropped uh to 44% indicating that maybe the conversation has shifted more to the everyday person as opposed to people that were very focused on free trade and the markets themselves. Now going over to relations, we can really dive into the context of this conversation. So this column here as we think about co-occurrence tells us what percentage of threats to global supply chain conversation mention one of these topics.

So 38% mention supply chain weaponization or 37% mention security of key North American supply chains. Well, we can see the other side of the ven diagram so to say where over here this says 17% of supply chain weaponization mention threats to global supply chain. Now the percentiles here also show us that these are very overindexing relationships uh relative to the co-occurrence rate of these other topics within other conversations online.

Now as we further investigate this we can look at how some of this has shifted over time. So bearing in mind the overall conversation has declined, how has the context of it shifted? Well, looking at security of key North American supply chains, we can see that went from uh approximately 28% of the conversation earlier this year to now 37%.

or China's role in global supply and chain dominance gone from 22% up to 30% with a big spike going between September and October where it went up to about 40% of the conversation or energy transition vulnerabilities and supply chain risks going from 10% now up to 24%. disruption of international shipping uh choke points. Really interesting here.

You see that was around 18%. It then dropped all the way to 12% in July. It's kind of floated lower on here before rebounding in recent months.

Now back up to similar levels it was at back in May. Security of European supply chains also growing. So, a lot of increased context uh and co-occurrence with security related aspects of the supply chain here.

Looking at food security and supply chain vulnerabilities, it'll be interesting to see how that's changed over time here as well. And we see that that's gone from 10% up to 20%. a small drop off between December and uh January but clearly almost a doubling from May to January.

So lots of shift towards people commenting about the security of these different supply chains increased focus on food security and energy security uh in terms of the context of this conversation and you can see more and more of that as we go further down. Now something like Trump tariffs in contrast at 14% of the conversation we can see that was much higher earlier in the year at 27%. It dropped in June only to go back up in July to 29% and continuously dropped to December where it was at 9% of the conversation before jumping up again in January to 14% of the conversation.

So always an important part but much less important than it was earlier this year. And clearly that was a key driver when this conversation was at its highest thinking back to the volume charts previously. You can also look at China's influence on strategic uh sectors and you can see how that went up heavily between September and October before going back down but much higher than it was earlier this year.

So lots we could dive in further to better understand the context of this conversation and that's where briefs is really going to come into hand because we have a lot of different things that we might want to ask. For example, uh we saw that there was a shift towards Indian nisonens within this conversation. Maybe we want to further dive into that question.

Or we also saw a growth in food security within these conversations. Maybe we want to dive further into that. So that's where briefs comes in.

I can ask that particular question. For example, how are Indian nisonens talking about threats to global supply chains? I have the ability to focus on particular sources or particular months.

So maybe I wanted to focus on those more recent time periods. I can select the country of focus or the language, gender, age if I wanted to focus maybe even more on those younger consumers. and run this brief.

I'll get that brief back in just a couple minutes and I'll come here and dive into the summary that we receive here. So diving in further here we can see that across these posts Indian nisonens most often frame threats to global supply chains as a combination of tar shocks geopolitical conflict and concentrated control of critical inputs especially minerals and advanced tech. The tone is largely concerned about volatility and knock-on inflation, but frequently paired with pragmatic, sometimes optimistic view that diversification away from single country dependence could open up opportunities for India if it can scale fast enough.

Good example of that is coming down here to the India specific angle and resilience in the China plus one opportunity. So they see as other countries go away from China, this could be an opportunity for India. As we think about how this summary is created, what it's doing when we ask the question is it's finding semantically relevant posts and then summarizing them into these different themes.

And then on top of that, say for theme one where we see tariffs and trade war whiplash as a the headline supply chain risk and many posts treat shifting tariffs including US China escalation as a immediate driver for fragmentation. We can come in here and see different posts from Indian users that speak to this conversation and help to support this theme. So with the US potentially imposing 100% tariff on China, what will be the real impact on the Indian market etc.

and seeing other types of posts related to that as well. Now on top of that we could dive further into one of the other questions that seemed to come out of uh the signals that we were seeing here. We saw that growth in the food security portion of the conversation.

So maybe want to better understand what is causing uh there to be more conversation around food security and uh within the threats to global supply chain conversation. And this is where we can dive in further once again. and see across these posts, the main reasons are talking more about food security in the context of global supply chain threats is uh the lived experience of higher more volatile food prices paired with the sense that disruptions are now structural rather than temporary.

Uh you can also see climate change uh or climate impacts are repeatedly framed as the most consistent driver of food system stress and you can see some examples of posts here around that. Uh in addition to you can see geopolitical conflict and trade controls are portrayed as direct shocks to staples uh and inputs particularly uh disruptions tied to Black Sea grain corridor as an example here. So lots of different things that uh seem to be gone into split between a variety of different themes.

Now briefs also helps us to think through additional follow-up questions that we can ask. So for example uh what are the most common arguments uh and evidence netisonens use when claiming market consolidation and price setting is driving food securities and what remedies are most advocated or contested? And immediately we can come here and have that brief immediately loaded up and go ahead and create it and further dive into the context of how users are talking about this.

So all in all, this is a unique workflow that chip enables to help us further better understand how users and netisonens are talking about supply chain and threats to global supply chain.