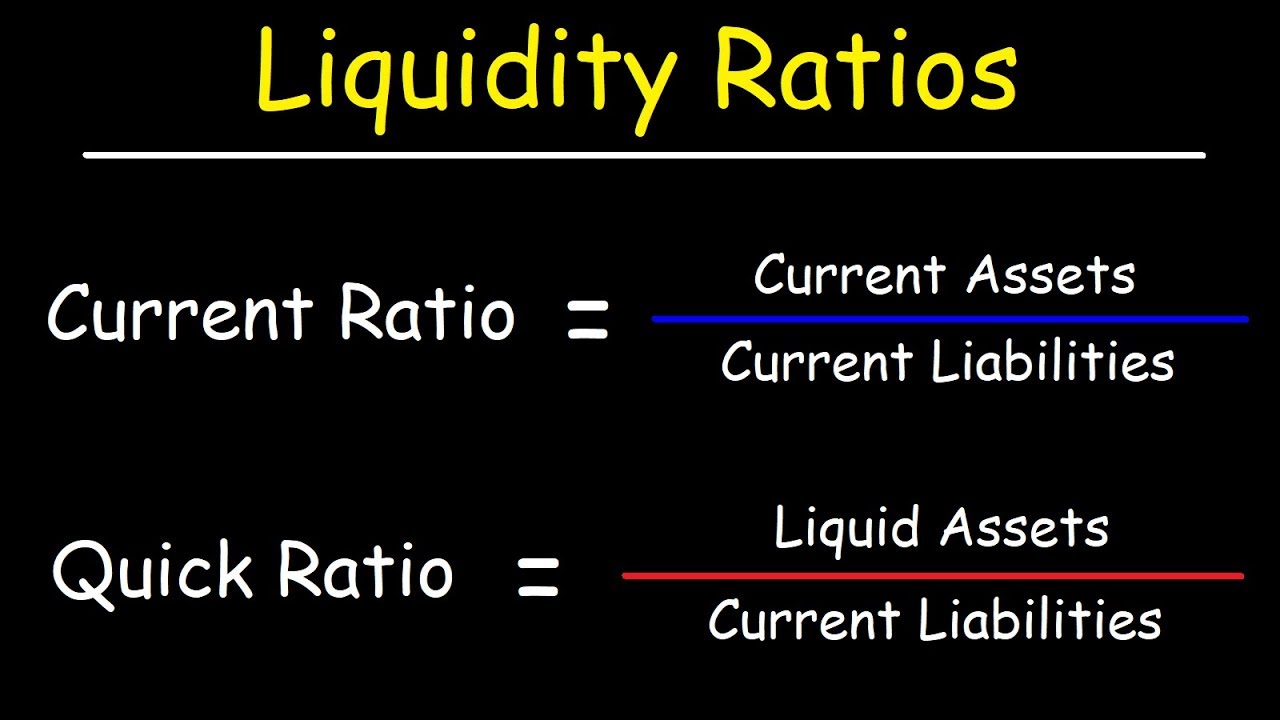

[Music] [Music] welcome students so we were talking about the calculation of the liquidity ratios and in my previous discussion we discussed how to calculate the quick ratio and in the ratio we saw here that current assets minus inventories are to be taken in the numerator but in the denominator some changes are also required to be done and that is current liabilities which are taken as it is current liabilities plus short-term debt that has to be taken as a denominator in the current ratio but for calculating the quick ratio some changes some adjustments should be done in the denominator also so the current liabilities plus we should take that short term loan net off the working capital limit it means total short term loan - the working capital limit whatever the working capital limit is that should be subtracted and that should not be taken into account so in this case when we found in case of the Grasim industries we have seen here that your say entire short term debt is power point number seven all short-term debts represent working capital borings so once these are the working capital borings all it means we will have to subtract that so we subtracted it and then we took in the denominator as only current liabilities and provisions which works out as one four five 0. 06 and when we walked out the limit that misses the ratio that came out as one point zero five is to 1 and 1 is to 1 it means that issue is at the satisfactory level the standard rule of thumb is that is the one is to one and in this case also we have found that the quick ratio is one point zero five is to 1 and 1 is to 1 for the previous here so it means it is valid within the rule and cluck ratio is fine so I was talking to you about that working capital limit net working capital limit so let's just understand what is the working capital limit see when there is a need to the forms for having the short term finance short term finance is required by the forms for meeting its day-to-day short term expenses and in that case we need the funds for buying raw material paying for utilities paying for the wages to the workers maybe after 30 days but you need money so sometimes when the forms face a liquidity problem or they don't know to keep more amount of the cash as cash in that case they get a limit sanction from the bank miss walking capital finance short term finance from the banks can be had by the forms in three manners and these three manners are one is the working capital loan and then the second is the CC limit cash credit this is called as a CC limit and then third one is the discounting off credit sales builds caradhras sales bills so this is the these are the three ways to have the working capital finance from the bank's when you take the working capital loan it becomes the short term debt and that we are including in the current liabilities for calculating that Cooke ratio what what is the CC limit and let's discuss the third first discounting of the credit sale bills as I discussed with you some time back also that when the form sell on credit and the buyer from this form or from Grasim industries say they have to pay after the end of the credit period it means if credit period given by Grasim industries to their buyers is two months it means the form is not going to receive these funds back before two months or sixty days but in the meantime if the form requires funds harassment estate require funds they can go to the bank they can tell the bank that look we have sold to this form if they're having a good credit rating in the market it's a credit worthy form we have sold them on credit they will pay us after 60 days so why don't you buy these bills from us and on the 60th day when the payment will come even though to us or we will direct them to pay to you directly you can adjust that was payment given to us take charge some interest on that and some administrative charges and commission and if some balance is left then you can remit this back to us so this is the discounting of the credit sale bills see see limit walking up at a limit or the CC limit CC limit of the walking after limit is the one where when the forms need the short-term finance they don't want to have the working capital loan because the difference between the CC limit and the working capital loan is that when you take the working capital loan say for example some form has it taken a working capital loan of 1 lakh rupees and that loan is taken on the 1st of January 2016 and on an average during the whole layer of the 2016 the form has been drawn 50,000 rupees out of this and remaining 50,000 rupees are lying unused in the account so now it's not the problem of the bank whether the firm uses entire Val lakh rupees sanction to the form or the form uses 50% out of it firm uses 25% out of it or 75% amount of it or entire amount out of it firm has to pay back to the bank that total amount back how much is used and unused plus the interest on the 1 lakh rupees which is the sanctioned amount so in the entire loan amount whether they use that load because Bank sanctions and they transfer the money to your account as and when you need money you will draw for example form received a truckload of raw material they have to make a payment of 25,000 rupees they're gonna withdraw from this lune account right so on an on an average they found that for the whole of the year they have withdrawn sometimes they withdrew 20,000 a will do 10,000 5,000 so maybe total withdrawal they have done ha for the whole of the ears is 50,000 so they used 50,000 but they are paying interest on the entire amount of 1 lakh rupees so it means that the extra interest they have paid on even on that unused part of the loan so they don't know to take the working capital loan say they want the working capital assistance from the bank or the loans from the bank in the form of CC limits or the cash credit limits now in case of the CC limits what happens when an e-form applies to the bank for having the cash credit limit then that Bank sanctions a limit of one lakh rupees and that amount of one lakh rupees will be credited or will be transferred to the forms current account in the bank so it will be transferred so as and when now the former requires money say for example firm received a truckload of raw material and they required 25,000 rupees out of this one lakh so the firm has withdrawn twenty five thousand rupees next day morning when they got some sales collection to the extent of twenty thousand rupees they deposited back say twenty thousand rupees it means the firm used that 25,000 rupees withdrawn today for buying of a raw material for how much time tomorrow they returned 20,000 rupees out of that and day after tomorrow and they received another five thousand rupees and they deposited back in the CC limit account so they use out of the 25000 rupees withdrawn they use first twenty thousand rupees only for 24 hours one day and second is then another five thousand they used for two days so firm has to pay the interest only on twenty thousand for only one day and remaining five thousand only for two days so this way what happens whether the bank sanctions 1 lakh or 10 lakhs whatever the amount out of the form the bank falls out of the account the form is using firm has to pay the interest only on the used amount withdrawn amount and for the period for which it is used not for the whole of the amount not for the whole of the period now this is the major difference between the working capital loan and the CC limit so most of the forms want that they should get the working capital finance from the bank's through C serum it's not through the working capital loans because this way they have the flexibility they have the funds in their account as and when they need money they withdraw from this account they use it for the number of days they want to use it when that money's surplus becomes surplus with the firm they return it back to the bank and they pay only interest for that much number of days on that much amount which is withdrawn not on the total amount of the limit that is sanctioned and allowed to the firm to be withdrawn but here the negative part of this CC limit is working capital limit is the forms are not allowed to keep two accounts in the bank or any one account in the one a bank and another account in another bank it may not be it may be like this that when you want to withdraw 25,000 rupees for paying the truckload of raw material you will draw from this account but tomorrow you receive 25,000 rupees as a sales collection and that you deposit in the another account that's not allowed that's not permissible that's not allowed you will maintain only one account you will withdraw funds whenever there is a requirement you will withdraw from the CC limit account but when you have collected the sales you have to return it back to the CC limit account and you have to deposit the money in the CC limit account for example it becomes same next a morning when the selections said collections come to the form collections come to the extent of 30000 rupees so form has we're done 25000 rupees and form has got the receipts of 30000 rupees so they will withdraw 25000 rupees so the balance of the CC limit will come down to 75 thousand rupees but next morning when they will get 30000 rupees collect 30000 rupees they will have deposit that 30000 rupees back in the same account balance will become that is that say again what was the how much is our amount withdrawn that is they have drawn 25 thousand rupees so what is the balance left here 75 thousand rupees in this account and next day morning when they got the collections of the credit says that was 30 thousand rupees so now the balance of this account will become 105 thousand rupees it means 1 lakh 5000 rupees so now this 5 thousand extra cannot be kept anywhere else this has to be kept in the same account so sometimes the CC limit account also balance in this account can be more than what is sanctioned by the bank because you see your withdrawal and deposits are through the same account so here if you without the 25000 rupees you use it for two days you will pay then trust only on 25,000 rupees only for a period of two days and for the remaining seventy-five thousand rupees no interest will be paid this is a cost to be borne by the bank a but- part here is that now if the balance in the CC limit account working capital limit account has become positive it is not one lakh it is one like five thousand so on this additional five thousand you won't get any interest so you will also not if there is any surplus amount you will not get any interest or the funds will not get any interest on that amount and other way round then the Falls withdraw only will be paying interest on that part which is withdrawn out of the working capital limit they will not be paying the interest on the whole of the amount sanctioned amount that is one lakh which is happening in case of the working capital loan account so people want forms want that more short term funds should come in the form of the working capital limit not as a working capital loan and then third one is a discounting of the credit sale bills which I have already talked to you so now the RBI he has put after 97-98 monetary policy army has put a given direction to the banks that this habit of withdrawing more money short term finance from the working capital limit should be avoided and the form should be say say guided or should be educated that they should seek more working capital financed through working capital loans so that the pressure on the banks can be brought down and they have fixed a limit now that now though it's only directive mr. not a directive but it's a guideline given to the banks where RBI that if there is a requirement of working capital for any forms equivalent to ten crores or above equivalent to ten crores are above the requirement is equivalent to ten crores or above then eighty percent of the working capital should be given as a working capital known and twenty percent should be given as a CC limit so the ratio should be 80/20 and gradually over the years this limit has to be brought down from ten crores to less than ten crores so that we can from the say the CC element kind of the system to the working capital known and the working capital loan can be made as a most popular way of getting the short term finance rather than through the CC limits so this is the working capital limit and how it works or how it functions and how the forms withdraw money or make use of the short term finance through the working capital limit so as there is a change in the numerator in case of the quick ratio we have from the total current assets we have subtracted the inventory similarly in case of the current liabilities also in the denominator part in the current liabilities we have taken total of the current liabilities plus short-term debt short-term loans but - working net of visitors and net of the working capital limit is how much money is being used as a working capital limit that will not be considered as a short-term debt and we have found in this case that entire short term debt is as a working capital limit from the banks so in that case that amount has not to be considered here so only we have taken the current liabilities hand provisions which 1 4 5 0.

06 corrodes so if you calculate the ratio we have found that it is well within the standard rule of thumb and that is the one is true 1 so they are maintaining a say say a good optimum current Cooke ratio now we calculate the next ratio that is called as the super quick ratio or you call it as the acid-test ratio this ratio is called as the acid-test ratio this is another ratio acid test ratio ad for calculating the acid test ratio we should take here the cash plus marketable securities cash in hand and cash our bank plus marketable security is very short term liquid investment almost kind of divided by the current liabilities plus short-term known net of working capital limit so it means in this case also the denominator will remain the same that the denominator is 1 4 5 0 because the short-term debt is only net of the if you take the short-term loan entirely it is the working capital limit but in case of the numerator now we will have to take the cash and marketable securities so let's see how much is the cash and marketable securities are there any is there any amount of the market really securities here's very short-term investments let us check in the balance sheet if you check in the balance sheet we have the cash and bank balances which is 1/1 6. 38 corrodes but I think there is no short term investment interest on accrued interest accrued on investments investments these are the long term investments I guess because we are given the long term investments here in the assets if you look at the asset side of the Grasim industries yes we have the investments yes this investment is 4 to 7 4. 70 corrodes but they are the long-term investments if you talk about these in this interest this is on the long term investments when we talk about inventory is there any incentive dieter's cash and bank balances and long general advances so it means there is no short term investment there is no marketable securities when there is no short term investment when there is no marketable security we cannot take it so we will take only the cash part and cash is how much this is 116 point one hundred and sixteen point three it corrodes so it is 116 point three eight corrodes and this is the numerator so the numerator here is this much if you calculate this ratio how much it works out s it works out as point zero eight is to one so it is almost 8% of the total current liabilities the cash and bank balances part is only 8% cash and bank balances part is only 8 percent so this is not a very a good amount but if you look at the overall level of the current assets and if you compare it with the current liabilities supergeek ratio keeping 8% of the cashes not bad they are keeping sufficient a sufficient amount of the cash as I told you that keeping higher amount of the cash also is not justified it is also not acceptable it's not worthwhile because the cost increases so I think they are keeping very nominal optimum amount of the cash that is 8% has compared to their liability so the acid test ratio is also been in range and I think the cause of this very you could call it as a prudent financial management the overall performance of the form has improved we can make out that yes this form is managing its operations well this form is managing its finances well this form is managing its the distribution and sales well this form is managing almost all its financial and operating part well so that their overall performance is very good and it is excellent now we calculate the other three ratios there are the turnover issues but they are for studying the liquidity position of the firm and when you talk about the turnover issues here we talk about the debtors turnover ratio so debtors turnover ratio we will we have calculated we have learned that how to calculate the DTR I told you that it should be calculated by we should take the credit sales but since creditor sales information is not available in the balance sheets so we should take the total sales total sales divided by the average debtors total sales divided by the average debtors and total sales and average debtors that is a DTR and if you get the DTR then you have you have to calculate the DCP let us collection period and for debtors collection period you have to do is that is 365 divided by DTR that is 365 divided by the debtors collection period so if you replace this DTR by the ratio so the ratio becomes total sales so it will become reverse so it will be average debtors average debt was divided by the total sales average jebadiah's divided by the total so 365 into average debtors and our receivables you can say average receivables divided by the total sales so in this case we can find out the DCP directly so rather than calculating it in two steps you can ignore this and here if you calculate this data collection period so we fine let's see what is a data collection period for the grapheme industries and if we calculate the DCP for the Grasim industries we will see here that how much is the debtors collection period for gaseum industries what also what is a level of receivables or the sundry debtors for the nursing industries if suddenly data that we 576 point for it corrodes so it is we are taking the closing figure we are not taking the average figure we are taking the closing figures so it is the 576 point for it corrodes for Grasim and the total sales of this form are which we have to take the total sales here let's check what is the level of total sales here let's go to the P&L account if you go to the P&L account PLN and pinellas statement will find the Grasim industries sales level and this sales level we have to take the gross sales so gross ears is 9607 so if you take the gross level is that is 9607 9607 point nine seven and multiply this by 365 so you will find that our closing detrás our 9607 point sarima closing debtors are five seventy six point four it corrodes and our total says inclusive of excise duty they are 9607 point nine seven corrodes into 365 so you can straight away calculate the DCP that is the debtors collection period and if you calculate the DCP debtors collection period for Grasim industries this works out as 22 days for the year two thousand six and seven and five and six it was twenty days so almost you can say largely it is the amount that is revolving around the twenty days 20 days of that say credit this this company is giving to its credit buyers I told you that India if you talk about the average of Indian scenario that normally the credit period which the average form in the market gives is forty-five to sixty days that one and a half month to two months credit period is normally but a Miss is permissible or it's allowable but you see because of the good operating structure of the form and very sound financial structure of the and having a good command in the market or in the segment in which they are operating Grasim industries only running the show by giving only the credit period around 20 days they are not allowing the credit sales beyond 20 days maximum is 20 days credit period they are doing with their giving so it means who can who can minimize the credit period who has the demand for his product in the market though they are giving the credit but they are managing the show by 20 days only one third of the standard credit period in the market so it means they are only selling for twenty days and after 20 days their buyers have to pay back to the aggressive this is the one part very good again so when we talked about the three first liquidity ratios we found current ratio was really wonderful quick ratio is well within the range miss current ratio is less than the rule of thumb then quick ratio is well within the range super quick ratio is very very good only 2% cash they are keeping and many we talk about the collection period collection period is also 22 days or around 20 days so miss again a very wonderful result and then we calculate that one more ratio then we'll close the discussion today that is the credit payment period let's calculate the CPP credit payment period so for calculating the credit payment period again we have to we were taking here the total purchases total purchases divided by say Sundra creditors total purchases divided by Sundra creditors this is the credit creditors turnover a so this will be giving us the CTR creditors turnover ratio but if you say and if you have to calculate the creditors payment period you have to do that is the 365 divided by CTR that is a creditors turnover ratio so if you take this you will be taking reverse of it so the ratio will become like that is that Sundra creditors divided by total purchases total purchases multiplied by 365 now let's calculate this ratio and try to find out that if they are giving selling on a credit for me 20 days how much credit they are getting from their suppliers and then compute a comparison of the two things now let's take that what is the level of Sundra creditors let's go to the balance sheet of the Grasim industries and let's check the level of credit sales Canada says if you talk about the creditors if we talk about the creditors here so we assume that all the current liabilities are the sundry creditors though we are not given the details but we will assume that all the current liabilities are the sundry creditors because they are short term that is the CC limit so let's take this has a sundry creditors and this is total of this certainly creditors this one two six six 0.