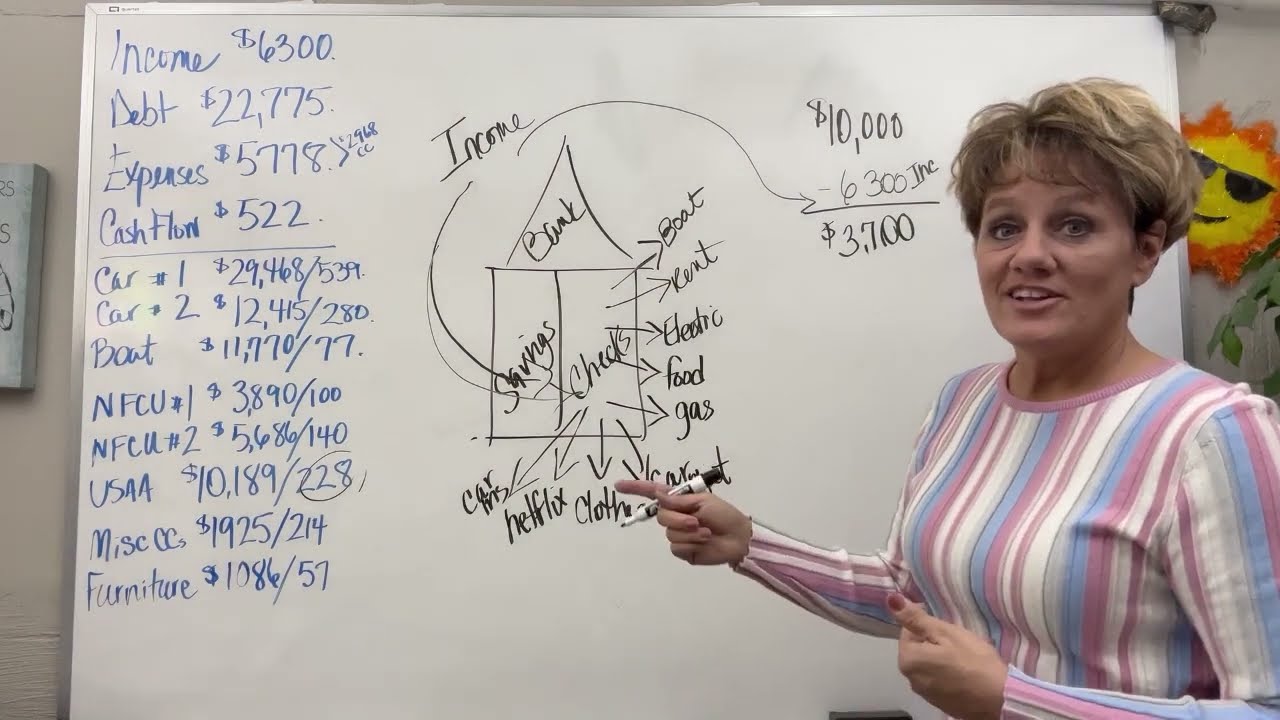

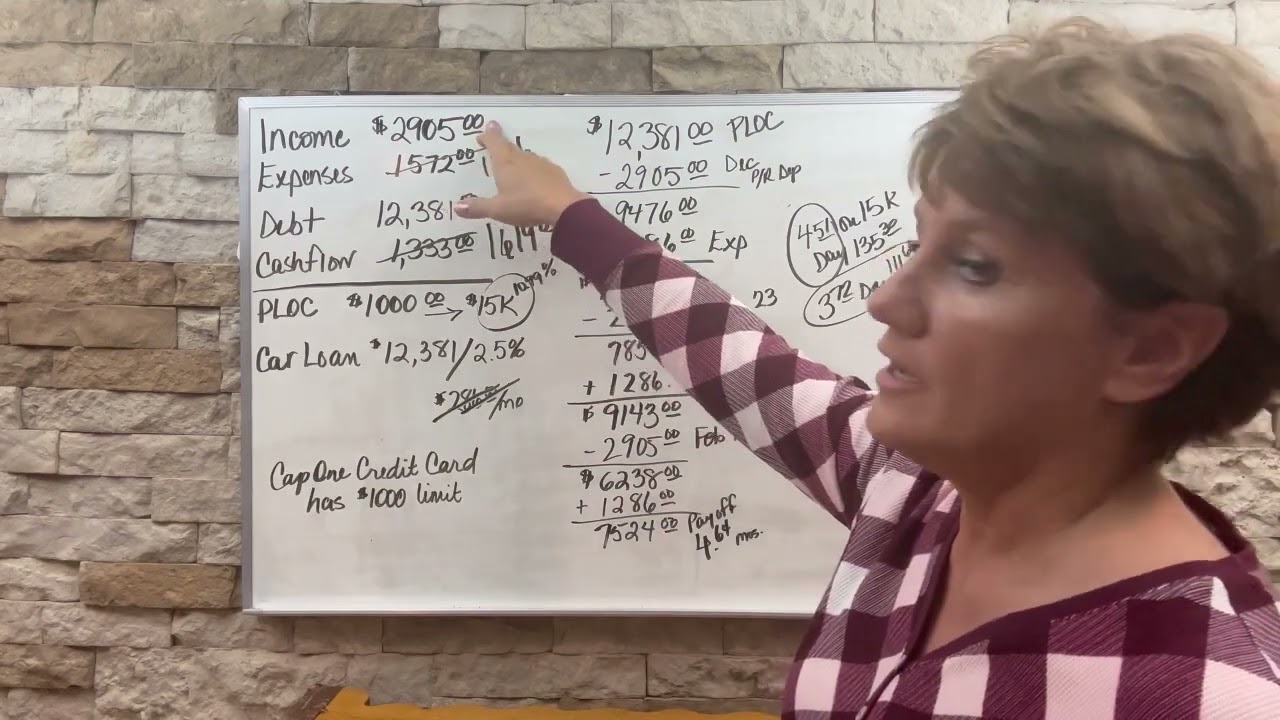

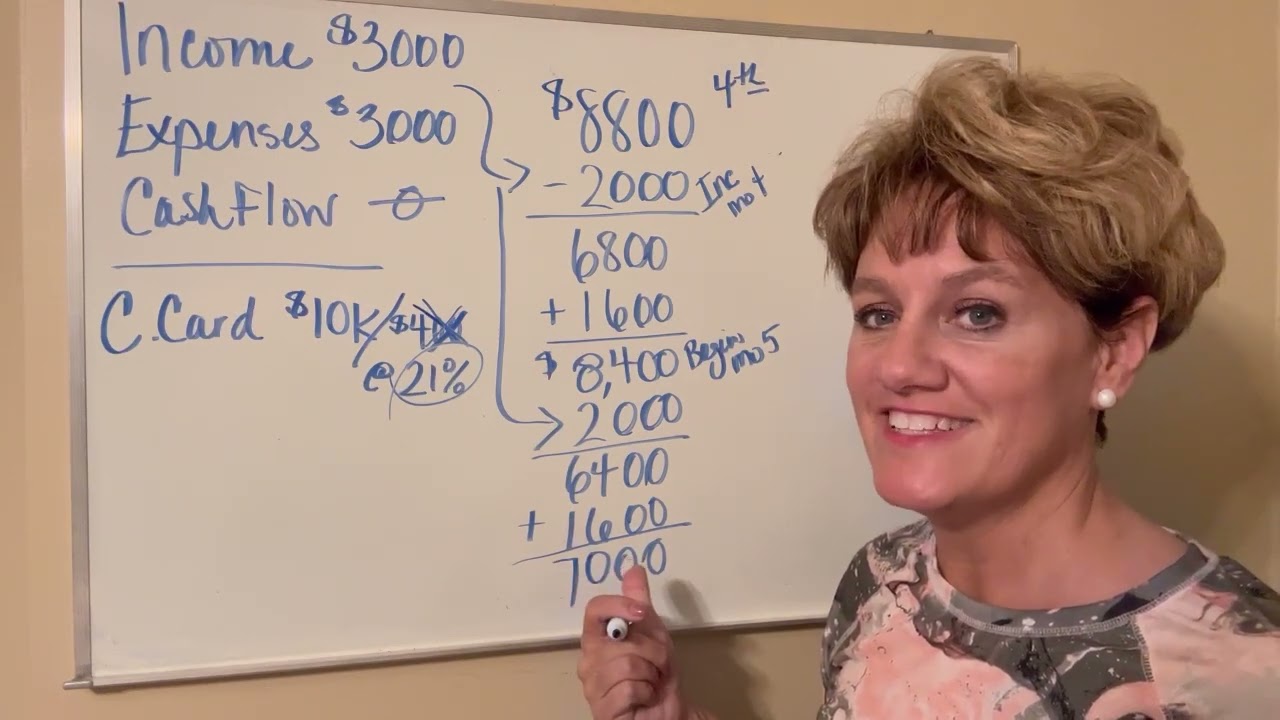

where do I start where do I start it's probably the main question that I get every single day at least 50 times a day I have this situation where do I start the first place that I would start is know your numbers you have to know your numbers you have to know every dime that comes into your home and every dime that goes out of your home what are your expenses all the income that comes in all the expenses that go out all the debt and balances and payments how long do you have to continue

paying on that debt what are your expenses your expenses have to include everything from food gas car insurance car payments mortgages subscriptions memberships any medical expense that you pay and yes even your giving and your tithing all of that has to be included in your numbers when you have your numbers when you know all of your income When You Subtract all of your expenses you then have money left over that is your cash flow you must know the cash flow so that we can make a difference in your debt load next do you have a

line of credit that could be a credit card a personal line of credit a HELOC do you have one if not you need to start looking for one what is your credit score do you need to work on that do you need some pre-game work do you need to work down some debt with your cash flow so that you can build your credit score up and get ready to find a nice line of credit to help you get rid of the rest of your debt what is an Loc an loc is a line of credit

you can find them in personal lines of credit a p lock you can find them in business lines of credit a b lock you can find them in home equity lines of credit a HELOC it can even be a credit card if you have a credit card through your bank or your credit union you can probably take and pull the cash off of that card and put into your checking account when you need to make cash payments such as mortgages car payments student loans Etc it's important to know your credit score because you do have

to have a 700 Plus credit score if you want to look into a first lean HELOC do you need a first lean HELOC a first lean HELOC can do one of two things if you already have a mortgage it can take over the mortgage to where now you've paid off the mortgage and you're just working with that HELOC beautiful source for paying off debt are you looking for a home to purchase if you are you can get a first lien HELOC to buy that home with do you need a second position HELOC the second position

he like means that you already have a mortgage on your home and you are getting a line of credit based upon your equity in your home so with the first lean HELOC and the second position he like you do need equity in your home with the first lean HELOC if your credit score is over 700 then you may be able to be approved for a 90 LTV loan to value meaning that you will have 90 percent of your Equity available to you for your use as needed and the next thing I would do is I

would look at all of my debts and I would determine do I have a line of credit that I can start with right now whether that be a personal line of credit a HELOC or a credit card if you already have one of those debt weapons then guess what you can start today if you need to get one of those debt weapons you need to start looking today they are available I have people tell me every day that they are getting approved for these lines of credit but it does take some footwork you're going to

have to get out there and look for them but it will be worth your while because then we can take action using your cash flow you can get out of debt very quickly and I want to see each and every one of you debt free and in financial peace in control of your debt like never before and it can happen you can make it happen where there's a will there's a way shoot for the Moon and even if you miss you're going to land Among the Stars have a great day and I will see you

in the next video