in this data set I want to report on total betas by Industry Group I'm part saying what the heck is a total beta so let's step back now when you think about the risk in a company risk can come from many different places some of the risk can be very company specific as in a project going doing better or worse than expected or competition being stronger or weaker some of it can be sector-wide if there a steel company something that affects the entire steel sector will affect you some of it can be driven by currencies

getting stronger or weaker that affects a lot more companies and finally some is macr level risk which affects all companies interest rates the economy political risk so when you think about risk in a company it comes from all of these different places you're saying who cares if you have all of your money invested in this company obviously you're exposed to all of this risk but let's say you're an investor who can spread your bets what does that mean in in addition to owning this company own nine companies on 19 other companies or 99 other companies

here's what's going to happen risk that affects one or a few firms will start to average out it's almost magical but it's really not it's a law of large numbers working out for every company where something bad happens there'll be some other company where something good happens so as you get more Diversified across companies and across the market you're going to see the risk that are firm specific disappear in your portfolio leaving you with just market-wide or macro risk that's at the basis for every risk and return model in finance because much of the risk

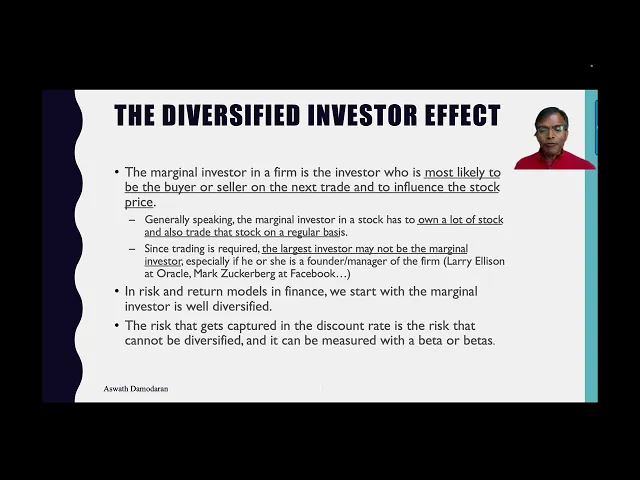

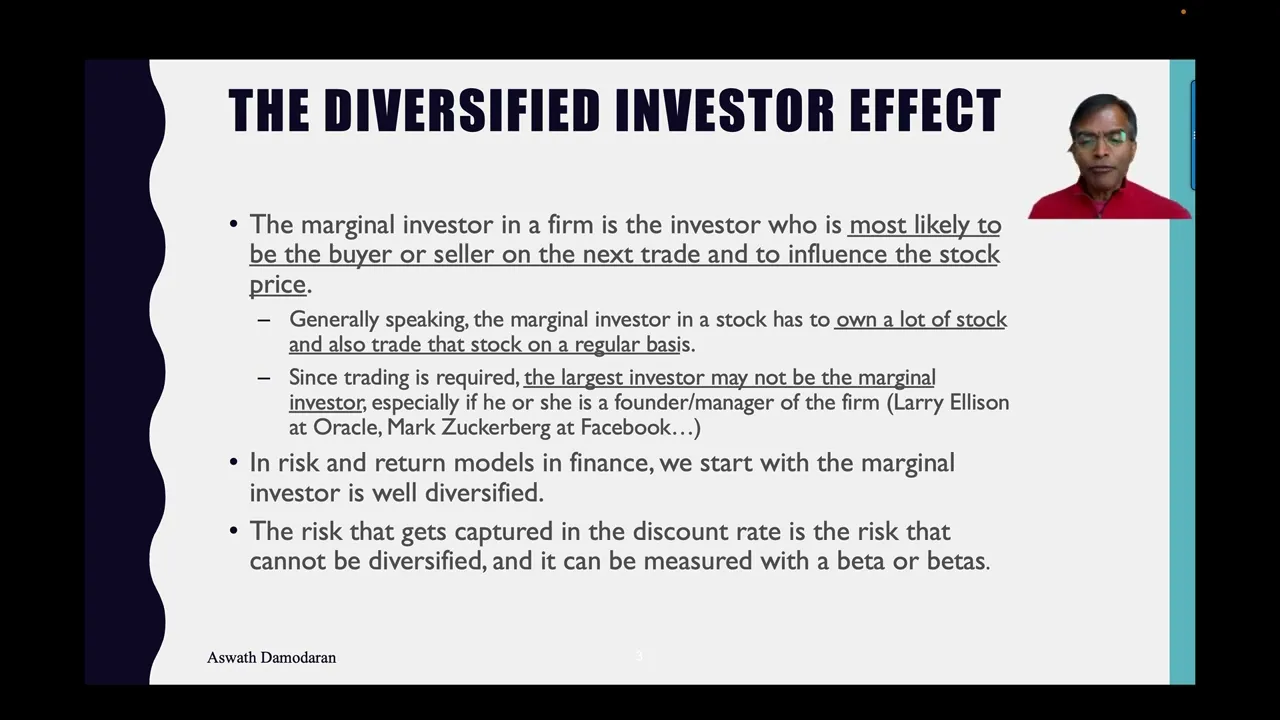

and return in finance was designed for publicly traded companies to measure risk at publicly traded companies and we assume that the marginal investor in those companies is likely to be Diversified you say who's the marginal investor the marginal investor is the investor most likely to be the buyer or seller and the next rate to influence the stock price so to be a marginal investor you need to own a lot of shares and trade those those shares on a regular basis just getting one half of that equation doesn't do it if you just own a lot

of stock and you never trade you're not a modin investor if you trade a lot but you don't own a lot of stock you're not a marginal investor so since trading requires both a big holding and and I'm sorry marginal investor requires both a big holding and trading that marginal investor is likely to be at many publicly traded companies of Institutional Investor not the founder or manager of the company so that's the starting point for how we think about risk and finance and that leads us to a very predictable place if your margin investor is

well Diversified which tends to be true in many companies with institutional investors the only risk that should be captured in your discount rate should be the risk that you cannot diversify away that's what we measure when we use a bet or a betas in a cost of equity calculation so no matter how much you dance around the estimation of betas you have to think about the underlying assumption that to use beta in the first first place you need to assume the marginal investor is Diversified now what if that's not true what if you're valuing a

private business where the buyer might not be Diversified they might be investing their entire wealth in in in the business that you're trying to sell about 30 years ago I concocted a measure and concoct is the key word it's not Diversified extending on what we know about risk and return in traditional Finance I said the market beta is the beta you would see if you're a diversified investor but if you're not Diversified then you're going to see more risk you're actually going to want to bring in the rest of the risk into your beta I'm

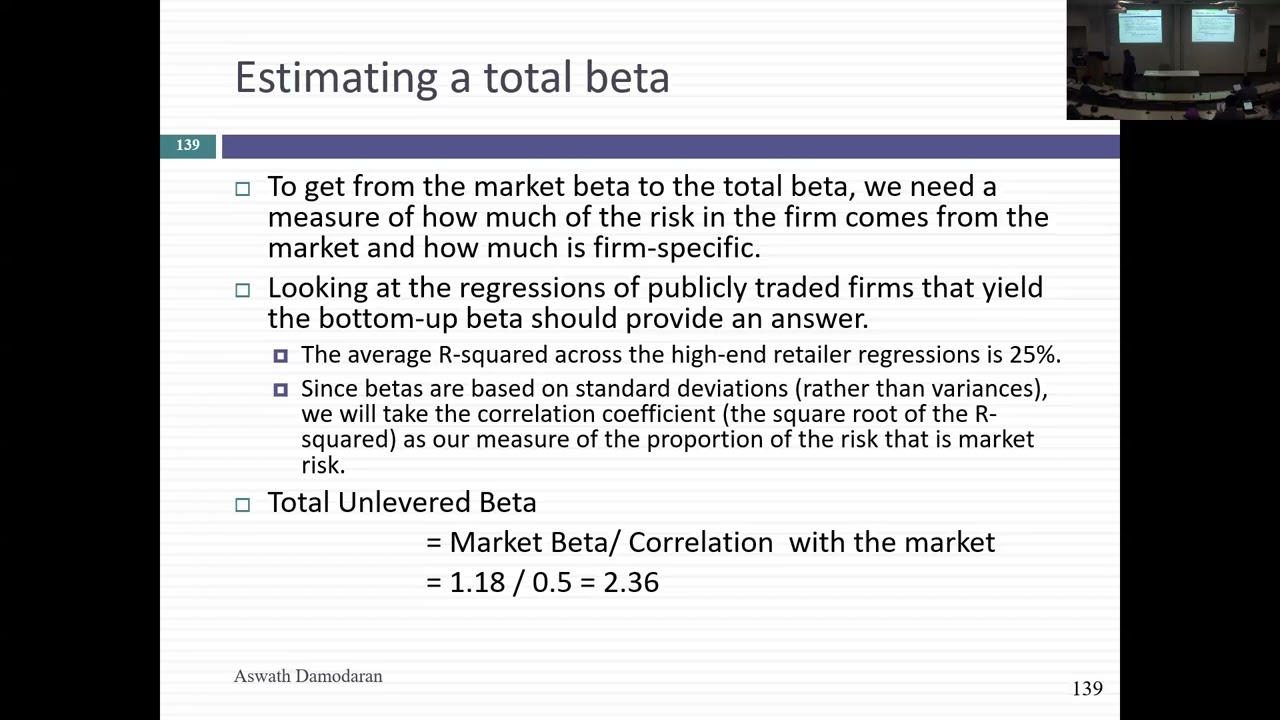

going that's why I call it a total Beta And there's an easy way to compute what that total beta is you take the market beta and you divide by the core relation of the sector with of the company with the market so as an example if your Market beta is one and only 25% of the risk in this company comes to the market your total bait is going to be four because that's the 75% you eliminated by divers so to get a total beta I need a market Beta And I need a correlation of the

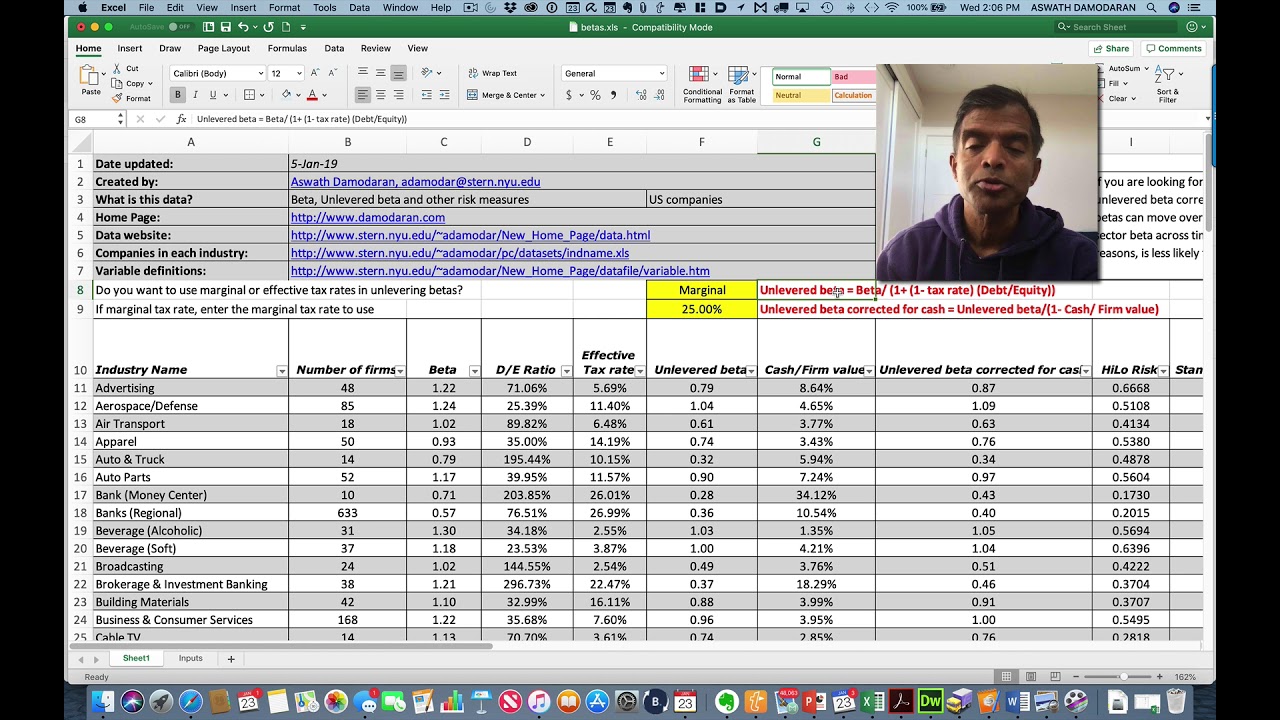

company with the market so if you you know obviously you can get Market betas and correlations only with publicly traded companies but you can get those numbers and ex extrapolate from them what the total beta would be if you're looking at a private company where a buyer is not diversify so the total beta computation you see here requires two details one is it needs UNL beta and it needs a correlation with the market I get the UNL beta the way I get betas for you know public for any you know for traditional publicly traded companies

I take the BET of every publicly traded company in in a group I average it out I clean up for debt and I clean up for cash I get an UNL beta for for for each set for each Industry Group for the correlation I take the r squared through each of the beta regressions again with the publicly traded companies are average the r squared and I compute the r which is a correlation my total beta is just the unlimed beta divide by the correlation with the market the lower the correlation of companies in a sector

with the market the higher the total beta will be so as you look at this data set you're going to see the total betas are three four five much bigger than the betas you used to see that's because they capture all of the risk in a company and we carry to the next step if you use these total betas to compute cost of equity you're going to end up with higher cost of equity for companies where the buyer is completely undiversified now before you use the total beta though remember this is a limiting case this

is applicable only if your buyer is completely undiversified they're buying the business with all of their wealth if you're buyer is a private Equity player there 15 other companies in in his portfolio or her portfolio you might not want to use the total beta you might want to use a number between the market beta and the total beta so if you think about the Market bait is one extreme a completely Diversified investor and a total bait as the other extreme is a completely undiversified investor you have to look at a potential buyer for a private

business and ask where between those two extremes they fall obviously an individual investing is his or her entire wealth in buying a business Falls at the total beta end an investor who is a publicly traded company buying your private business Falls at the at at the at the at the market base end because public companies are investing Diversified investor money and if you're a private Equity investor you might fall somewhere in the middle but think of these total betas as giving you the other extreme and Market betas being the the the two ends of the

spectrum and think about where you might fall between these two two extremes when you think about ass assessing the value of a private company but but steer away from using total betas we looking at public companies these have nothing to do with public companies so if you're looking at a public company just stay with Market betas you know total betas will get you into trouble I hope you found the session useful and thank you very much for listening