hi welcome back in this session i'd like to take on a concept that has acquired a lot of followers among corporates among investors among consultants and that's esg everybody's caught up in it and i have to tell you upfront that i come from a position of skepticism when people claim to find something new and revolutionary in corporate finance and business i've seen over the last three decades i've seen people take concepts that are straightforward and simple that are part of the corporate finance lexicon add a couple of proprietary twists to it i'd put an acronym

on the name and then market it market it to the point where you can overcharge for the concept and tell everybody that this is the magic bullet that's going to solve every one of your problems and with every one of these concepts about a decade after the concept has been introduced and sold here's what happens the truth comes out and people abandon the concept but people have become rich along the way consultants experts services that offer so when esg came along the big question was is this another in a long line of over-marketed concepts now

you could argue that esc in a sense is different its promise is wider and bigger than you're saying businesses will be better with esg it's about making society better and therein may lie a problem in how esg is being tested and debated let me explain first let's talk about timing why now why talk about esg now in a sense the stars all aligned last week for talking about esg in what sense well it's been 50 years since one of the most influential op-eds in the new york times has been published not written by milton friedman

where he said the objective of a business that companies should focus on profitability and value not on delivering on a social mission that is 50 years ago so the 50th anniversary of course the new york times gathered together a list of luminaries and they all opined on the freedmen of it to a person every single one of them these included academics economists um you know social you know social commentator and they all said well friedman was wrong the world has moved on and it's a good time then to examine whether milton friedman was really off

the table in terms of the recommendations he made the second was especially in the context of kobe there have been people who've argued that esg companies companies that are good socially conscious have weathered this crisis much better than companies that are not it's now become part of the accepted wisdom it's been pushed by both not just academics but by investors like blackrock claiming that esg stocks have done better than the market and thirdly there's a longer standing story of how esg has become part of companies in fact there are multiple services that measure esg and

ucsg becoming part of what investors are looking at companies more and more now before we go on it should be it's worth noting that esg is now the establishment the establishment has clearly bought it and let me explain last year the conference board composed of ceos or some of the largest companies in the u.s put out a statement that the objective of a company is to take care of its stakeholders i have no problem with that that's absolutely you know unimpeachable that's a statement companies should make but they went further they said that when you

run a company you should have multiple objectives you should take care of every stakeholder's interest and i wrote about this last year so many ceos are seem to have bought in the notion that this is now part of their mission to play a role in society investors seem to important as well prominently larry fink of blackrock has become a vocal proponent of esg arguing that for investors it's good if companies operate in society's best interests academics seem to have bottom as well in many business schools now you have you know groups that take care of

you know talk about esgt gst and it's become almost part of accepted wisdom that being good as a company will also deliver good results make you more profitable more valuable and the same time make investors better off everybody seems to better off and best of all while doing this you're also improving society now here's the problem the services that measure esg have an issue the issue is unlike financial measures where there are dollar values you can look at esd is based on qualitative fuzzy measures now that by itself would not be an issue because fuzzy

measures have been measured you know have had numbers attached to them before these fuzzy measures there's no consensus in terms of ranking what's what should be important what should let me give you a very simple example if you're a very very very strong environmentalist to you the worst company in the world might be aramco why because it brings oil out of the ground it contributes to global warming climate change but your neighbor who's much more concerned about privacy and politics might view facebook as the devil incarnate in other words there is no consensus your own

rankings and the services struck they do try to put numbers on on the different qualities they bring in but guess what because there is no consensus the correlation in esg rankings across services is low so if you look at the top 100 companies best companies on one services list and the top 100 companies in the second there's almost no consensus there's there's there's correlation but not very strong correlation you're saying that's because there are companies which are lower profile maybe that's what they disagree on in fact in one study i you know looked at you

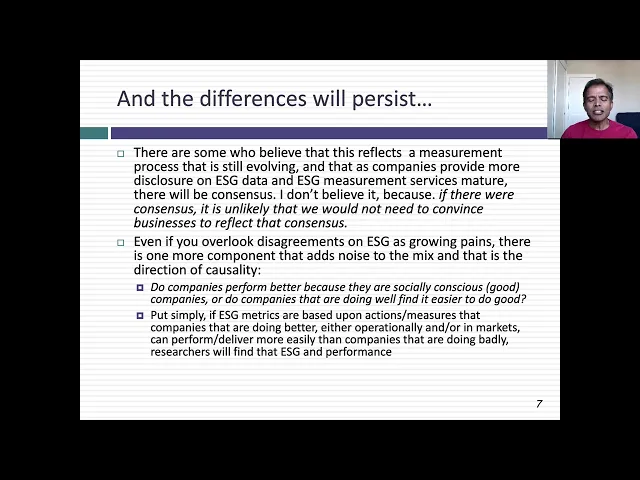

know high high profile companies companies like facebook and walmart and noted how much of a divergence there was between three different services and these are all mainline services measuring corporate governance so even if we agree that corporate governance measures measuring corporate governance is going to be a problem simply because of what you're trying to measure now there are some defenders of corporate esg who claim that this is just a maturing process that as esg matures as a concept there will be consensus that services will tend to agree more i don't believe it for a moment

and here's why if you truly have consensus on something be good or bad you don't have to have esg companies will do it the very fact that you have to lecture companies on what makes them good companies tells us that there is divergence of opinion out there and that divergence of opinion will continue but even if you get past that problem there's one final issue the way we measure esg is we look at what companies do but let's suppose that what we look at is easier for companies some companies to do than others let me

not be mysterious let's suppose we look at how much companies spend on being socially conscious how much they give back to society you know how much time they give off for their employees to play social roles you know what companies that are doing well have an easier time doing that than companies on the edge so if you measure esg based on actions that are easier for profitable and more successful companies to take on you create a causation problem what am i talking about when you say that companies that rank high on esg are more profitable

do better than companies that are not is it because companies that are that are that rank higher on esg are doing better or is it because companies are doing better find it easier to deliver those measures that make them look good on esg it's something that's that's bedeviled researcher will come back and talk about it but the esg promises are what i think has made this train catch the speed that it has and it promises everything to everybody to corporate to corporates to ceos and cfos the esc promises if you're a good company and let's

let's for the moment accept that somehow we figured out what good actually means on the goodness badness scale if you're a good company you will become more profitable perhaps not in the short term but in the long term and be a more valuable business perhaps even less risky so companies are better off from adopting esg to investors the esg promises if you invest in companies that rank higher in est you're going to earn higher returns and to society the promise is if companies are socially good if they do well on esg society overall is going

to be better off who can fight this concept it's everything for everybody it's all good things to all people so i'm going to step back and argue that to address esg honestly you got to look at three separate questions the first is how does esg play hard in value because he she could increase value and at the risk of of of of killing some sacred cows it could decrease value could do nothing for value how does csg play hard value that's the first question the second question is what do markets price in when they look

at companies do they give higher est companies higher pricing a separate issue from valuation because this is a market perspective and there's a third question how do investors get rewarded or punished based on esg how does esja affect value how do markets price it in how are investors affected you're saying why is three separate questions because let me play out a couple of scenarios it is possible the dsg is good for value that if you're a company your value increases by 10 percent by being more socially conscious but being a better company let's say that's

true but let's say markets overreact to your goodness they push up the price by 15 percent sort of 10 do you see where i'm going esc is good for value your pricing has gone up but if investors buy your stock at that higher price they will get lower returns so even though est is good for companies and it's priced in because it's overpriced you're going to get returns that are bad for investors and good companies we need to separate these questions and one of the problems that i see with the esg research is the questions

seem to be modeled when people look at returns to investing in good companies and they discover for instance that returns a higher investing good companies they jump to the conclusion that this must mean that esg is good for value not necessarily so let's start with the question of esgn value now i know in a sense we're operating on a domain where i feel very comfortable now we know what drives the value of a company it's driven by cash flows and risk and i'm not talking about putting any structure on a risk and return model it's

basic common sense what a cash flow is driven by they're driven by a capacity to grow revenues what your margins are how profitable your business model is and how much you reinvest to get that growth and what's your risk going where's your risk going to shop it first shows up as what it costs you to raise equity or cost of equity and what it costs you to borrow money so i'm going to state a proposition that i find incredibly useful when dealing with these acronyms the buzzwords that get thrown on us it's called the proposition

if it does not affect the cash flows and it does not affect risk it cannot affect values what are you talking about what's it you name it it's good it could be something as precise as new acquisitions effect value but in the case of esg the question is does the esg effect value here's the it proposition on esg if esg is going to affect value it has to either show up as higher cash flows or a lower required rate of return or lower funding cost now you can have your own story as to why that

will happen but that's where it's going to show up so i'm going to give you three scenarios linking esg to value since esg is a really is a religion to some i'm going to use some biblical references here the first scenario is where the good are rewarded think of this if you're if you're a christian as a new testament garden a god who rewards goodness good companies get rewarded in what way well good companies produce products consumers buy more of their products are willing to pay higher prices because these companies are good so it shows

up as higher revenue growth higher margins and because they have more more sustainable business models their reinvestment is lower and as a consequence of it being lower they can reinvest less to deliver the same drug higher growth higher margins lower reinvestment higher cash flows and because these companies are good they also benefit in another way investors are willing to invest in these companies because they're good companies and demand a lower rate of return so they have a lower cost of raising equity and lenders lend to them and feel less worried about bad things that companies

who don't charge them a lower interest rate so funding costs are lower and because these companies are good they avoid those disasters and catastrophes that seem to be that seem to kind of get in the way of bad companies so in this scenario good companies get rewarded so goodness delivers its own reward for esg advocates this is your best possible scenario because you can go to ceos and say well just be good and over time everything's going to come up roses there's a second scenario staying with the biblical the biblical terminology think of this as

an old testament called a vengeful god here the bad companies get punished in what way consumers stop buying their products and services they have lower revenue growth they have to charge lower prices they have lower margins and often because employees don't stay on suppliers are are reluctant to to interact with them they have investment markets that require more reinvestment so we have lower cash flows in addition in the market investors avoid their shares what does that mean pushes up their cost of equity so funding costs go up for equity bankers are more reluctant to lend

to them so they have higher costs of debt and overall it translates into higher funding costs and to add some spice to the mix because these companies flirt on the edge of disaster they're bad companies they're more likely to get into catastrophes disasters so this scenario bad companies get punished it's still good for the esg advocates but not as good as the first scenario because here when you make a sales pitch to companies it is don't be bad because that's where the punishment is you can't tell them to be good because there's no payoff to

being good but there's a punishment to being back but still esd advocates should take this because it's the third scenario where if you're a religious person this is your hell on earth you're the bad guys well in what way bad companies have lower costs why because they put their factories they use underage labor whatever you want to make this this your description of a bad company the lower cost they get higher margins they charge lower prices they get higher growth they might be able to reinvest less because the reinvestment parts of the world but there

are very few regulatory and environmental constraints they might actually have higher cash flows and because of higher growth and higher cash flows equity investors might actually like their companies like their shares and which gives them a lower cost of equity and a higher stock price and they might be able to borrow money based on their cash flows so in this scenario bad companies get rewarded at the expense of good companies you say that can't be if this is an empirical question not a moralistic question i'm not asking which would you like to see the question

is what is the truth so let's look at the evidence on esg and value and if you look at the evidence in the esga value i'm going to break it up into three parts the link between esg and profitability has been examined in hundreds of studies of varying quality and here's the bottom line if there's a link found it's a weak link between being good and being profitable a weak link and that weak link is very sensitive to how you define profitability the sample size you use in the time period you look at so the

over if you're asking for an overall consensus there's a very weak link between being good and being profitable there's a stronger link between esg and cost of funding but on the bad company side put simply the studies of sin stocks what is in stocks casino companies tobacco companies increasingly fossil fuel companies have found that these companies are charged a higher cost for investors why because many investors don't want to invest in them but there's a catch to the story bad companies face higher costs of equity but the flip side of the story is investors in

these bad companies actually on higher returns and there's a third piece to the evidence and then on this there the evidence is fairly light right now but there is some evidence that if you're a bad company there's a greater chance of catastrophic and disaster risk and your stock returns reflect that so the evidence is weak on the link between esg and profitability stronger on the risk measures so if i were to summarize the evidence it is the evidence seems to suggest don't be a bad company but he says should i be a good company should

i spend more and the evidence is not there yet let's look at esg and returns yeah now let's start with the basic reality that esg advocates need to confront you know directly if you are optimizing i mean if you've ever done you know operations research and you're doing an optimization problem a constrained optimal can never deliver a result which is better than an unconstrained optimal what are you talking about and let's suppose you took every listed stock in the u.s and you were able to invest in all of them because you have no esg constraints

there is no way you can tell me xnt that removing 25 of these stocks because they're bad companies and making my universe smaller makes me better off i mean you could make i might be just as well but i can't be better off that is a fundamental fact that you got to deal with up front and there are very few esg funds that seem to be honest about this truth just as an example of one fund that seems to tell the truth i am part of the tiaa cref fund as part of as as a

professor at a university that is my pe that's where my money gets invested and they offer re and in going with the fact that esc is now this bandwagon effect they've offered what's called a social choice equity fund to all people investing and that social choice equity fund invests only in good companies with quotes around the word good and in 2017 a year in which that fund delivered lower returns and their benchmark fund they were pretty open about they said that's because in this one do we avoid bad companies and if you remove stocks from

our universe it makes us worse off that's truth in advertising i would have more respect for esd funds if they said that upfront because there is an internal contradiction here in the esg story if you tell ceos and cfos that being good lowers your funding costs you cannot in the same breath tell investors in those companies that being good delivers higher returns to them so when you look at returns in esg they're very tough to read because showing that esg and good returns go together tells me very little and here's one esg can increase value

decrease value do nothing for value you can make positive returns negative returns or no returns from esg but there's an intervening variable which is what's the market pricing in and when you tell me the returns you generate from investing in good stocks without bringing in what the market is doing have a very tough time going from there to whether esg is good or bad for them as an example let's assume that esg is bad for value it reduces value but let's assume that markets under react under react to what sense they you know when esc

is bad for value markets don't drop by enough to reflect that badness so what do you do you buy those companies you will actually make positive returns even though esg is bad for value you're betting on what the market is doing in other words returns reflect market prices relative to expectations so when you look at a study on returns you should expect that confusion to play out and it does and here's how it plays out if you look at the studies that link esg returns are all over the place some studies find that esg and

returns go together that investing in good companies deliver higher returns now some studies find the opposite that investing in bad stocks deliver higher returns since stocks deliver higher returns and some studies are kind of neutral they argue that you know it depends on which period you look at and how you screen your portfolio and even those studies that find esg and returns are positively related they also find that esc tends to be correlated with two factors of long standing one is momentum and the other is growth you see what are you talking about companies that

rank high on esg if you look at the last 20 or 30 years and service rankings esg companies that rank high on esg also tend to be companies with high momentum that have gone up the most in recent periods and high growth companies and that's why a disproportionately large number of companies in esc funds tend to be tech companies so if you correct for those factors and you put esg into the mix it's questionable whether esg is what's delivering the returns or whether it's momentum and growth so i'm going to offer you some glimmers of

hope if you're still hoping to make money in esg there are two scenarios where esg might deliver higher returns the first is a scenario what is a transition period let me explain let's assume that good companies actually increase value but markets are slow in reflecting that in that transition period what you will have is valuable increase up front but markets would slowly catch up in the transition period you're going to make higher returns investing in good companies the intervening variable the market is doing something a mistake that you're taking advantage of so in this story

if you can get ahead of the game invest in companies that are good where you believe that goodness increases value and you back it up but markets are slow and adjusting you take advantage of the slow moving market here's the second potential scenario is it is possible that esg for the most part doesn't show up in your cash flows near discount rates but companies that are bad have more catastrophic risks so you don't see it very often when it happens it blows up your company maybe investing in esg reduces that downside risk which should make

esg companies better investments during crises so what's the investing lesson here there's no easy way to make money on esg if you pick stocks that are ranked high on easy don't expect to be rewarded for it everybody can see the esg if there is a payoff dsg it must be from being dynamic from sensing things that markets are going to price in three four five years ahead of them pricing it in buying those companies and waiting patiently for it to happen there are easy ways to make money why should est be any exception now of

course with corvid in place you have a test of resg stocks better during a crisis and at least initially the conclusion seemed to be that esg companies were doing much better in fact at one level it's not debatable esg companies have benefited from this crisis in terms of how much money has flowed into them this is fun flow into esg stocks during the crisis clearly money is floating tsg stocks for better or worse investors have pushed money into esg stocks but remember esg stocks are also often tech stocks momentum stocks growth stocks so whether it's

esg or momentum and growth that's driving this fund flow we don't know in fact to back this up of esg stocks doing well morningstar looks at esg funds and has noted that during this crisis esg funds have done disproportionately well the way to see this is to see how many of them rank in the top quartile and remember if it's random it should be 25 in each quartile but that's not what you see the best esg file the esg funds overall are more likely to show up in the first quartile than the fourth fourth quarter

so you see this is good esc must be what's creating these returns it's good to invest in esg stocks during the crisis well not so fast a recent paper that looked at esg at this phenomenon during the crisis and correct it for the fact that your growth in momentum stocks found that esc by itself was not adding anything to the returns in fact this study found that in the first quarter of 2020 which was when markets were melting down est was a neutral factor it did nothing it didn't because what was creating the returns was

momentum and growth and in the second quarter when stocks came back esg actually actually acted as a net negative so has cobit made esdsc story stronger well not quite yet so if you're doing victory dances in the end zone because how esg has performed stop so what's the bottom line well i think in many circles esg has become this good everybody is supposed to accept it because arguing against it is viewed as a sign of moral deficiency and i think that's getting in the way of an honest argument about esg much of the research in

esg has been sloppy and agenda driven where people start off with the premise that this is a good thing and that your job as a researcher is to show it's a good thing that's not what research is supposed to be and the more i read the esg research the more i'm inclined to go back to milton friedman because whether you agree with them or disagree with them his argument comes from a position of coherence and consistency so we're going to displace the friedman view that companies should first and foremost be custodians of shareholder wealth and

profitability and financial health and if you're going to be good you first have to deliver on that then i think we need to see more solid evidence to the contrary and i haven't seen it yet i know i i know we all i know this point you're probably saying you you're ethically challenged you're morally deficient i'm okay with those arguments with the with those critiques because i think we share a common objective we want companies to act in the best interests of society we all do the question is how do we get them to do

it my view is esgs marketed now is on a dangerous path because a decade from now i will make a prediction that more companies than ever before will be a dsg bandwagon but they will be no more socially responsible than companies today or companies 30 years ago 50 years ago a lot of people are being enriched mostly consultants experts and esg advocates but society overall will be worse off because what you will have are companies that posture i for one don't want your platitudes from ceos and how good they are and how well their companies

are behaving i want actions and i want those actions to be consistent with financial health if we want companies to be socially responsible we have to make it in their financial best interest to be socially responsible and guess where that responsibility ultimately lies it lies with you and i in what way if we want companies to be socially responsible we have to put money behind those words we have to buy products of companies that we think of as good companies and be willing to pay more for those products we have to invest in shares of

companies that are socially responsible and accept the fact that we accept we will get lower returns on those companies if we do that then companies will become socially responsible for the other hand we want to have our cake and eat it too then all we will have are companies that sound good but don't do good i hope you found the session useful and thank you very much for listening