[Music] So, welcome back to the options crash course strategy series. My name is Jim Schultz. In this video, the final video of the series, we are going to cover the ratio spread.

We're going to follow the same protocols that we followed to this point. We're going to cover winners, we're going to cover losers, and we're going to cover that dance floor. But first, let's talk about how a ratio spread sets up.

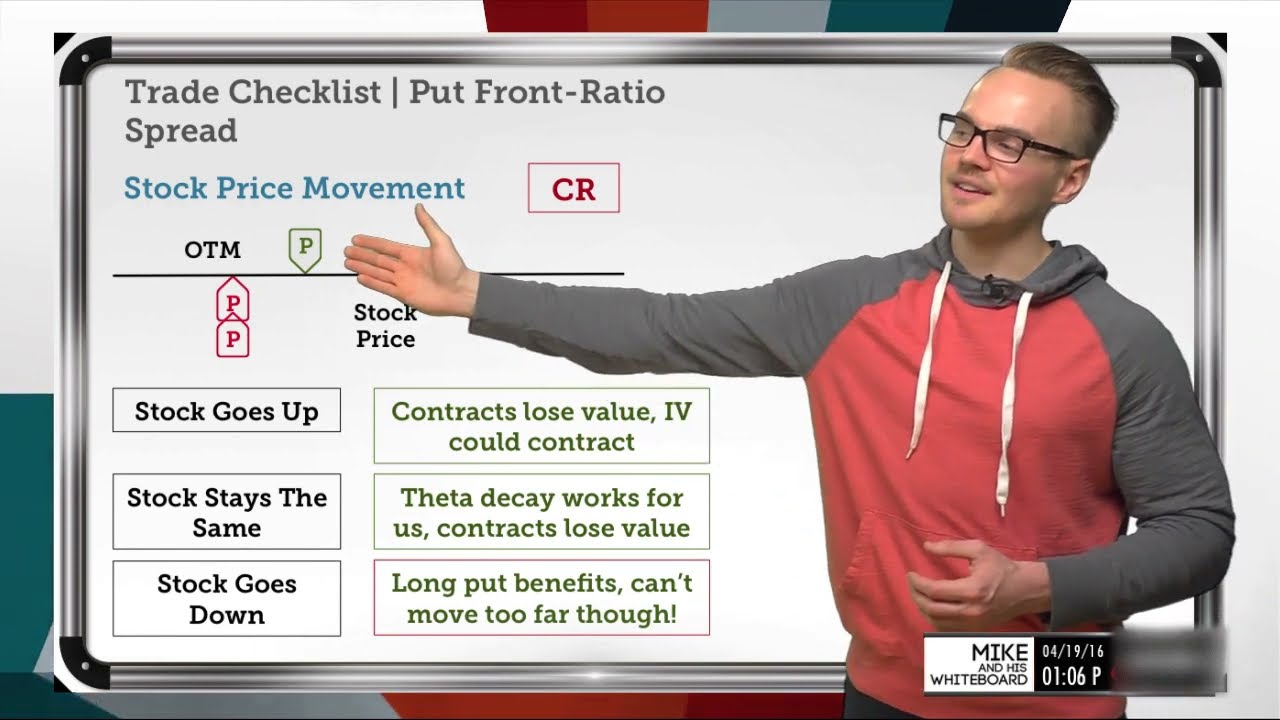

So, the ratio spread—this is arguably the most versatile, most flexible strategy that is available to us—and it consists of two parts. You have one long option and you have two short options. A long option is usually situated at the money or slightly out of the money.

The two short options are then placed further out of the money. Because you have two short options relative to every one long option, this is going to be a net credit strategy. For example, let's say that the stock is at 50.

You might set up a put ratio spread using the 49 strike and the 48 strike. You would buy a put at the 49 strike and then sell two puts at the 48 strike. But let's say the stock is at 75.

You might set up a put ratio spread using the 75 and 72. 5 strikes. You would buy a put at the 75 strike, the at the money strike, and then you would sell two puts at the 72.

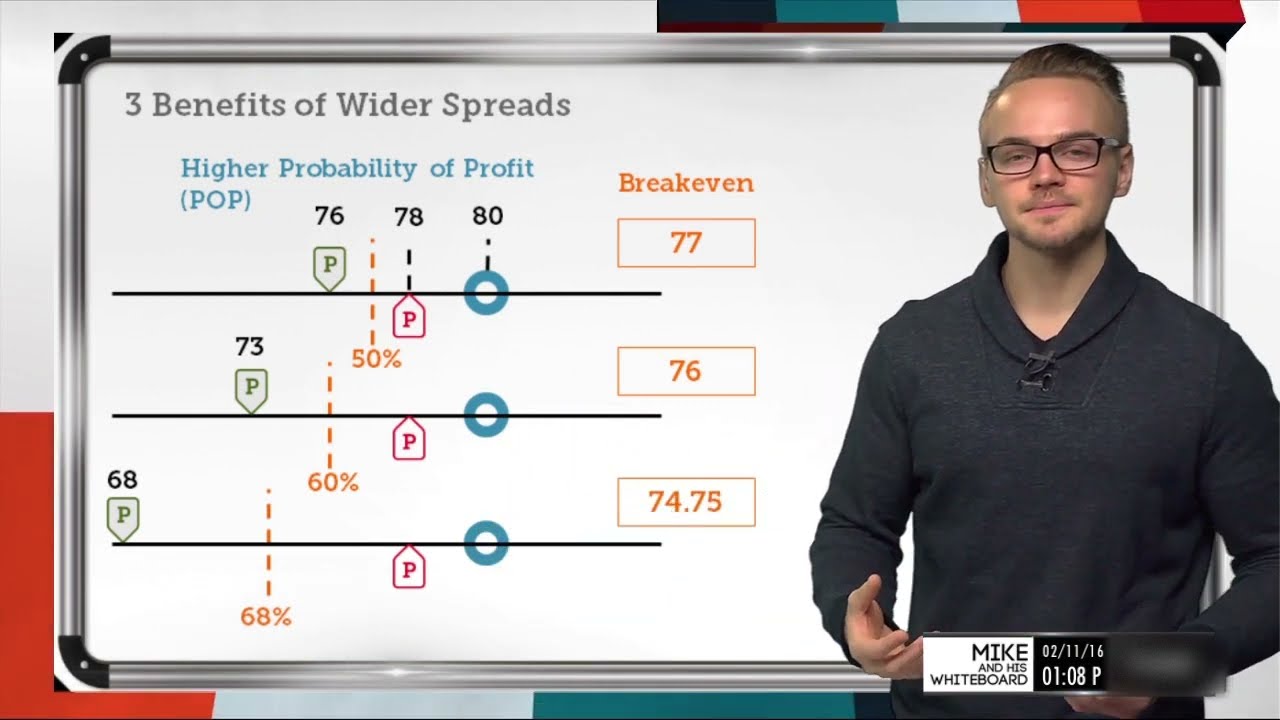

5 strike, the out of the money strikes. Now, there are a few things that you want to be aware of, that you want to be cognizant of when it comes to putting on a ratio spread. First, the wider you go with your ratio spread, the greater your maximum potential profit.

This is because the vertical spread that's kind of baked into the center of the ratio spread could potentially be worth more money. The trade-off here is that the wider you go with that ratio spread, the lower your credits collected. Second, you want to make sure that on entry you collect a credit that is economically significant.

You'll see why in a couple of minutes. Third, we typically prefer put ratio spreads over call ratio spreads, and this is for the same reason that we typically prefer short puts over short calls—the market wants to go higher over time. So, battling a short call over cycle after cycle after cycle in a market that wants to grind higher can really be a stick in the mud.

Alright, so managing winners—everybody's favorite! This is actually going to be a little bit more involved than what we've seen to this point, and that's because with a put ratio spread, you can actually make money in both directions. If the stock rallies, then you're going to keep the credit collected because those options are going to move further out of the money.

But if the stock falls, then you could potentially make more money. This would happen at expiration; if you pin that short strike, you'll keep that credit collected, but you'll also pick up the width of the ratio spread. Since we don't hold our undefined risk trades inside of 21 days to go, we're actually not super interested in that stock falling scenario, since that's never really going to come into play.

So, we want to focus our energies on the stock rallying scenario. How do we manage those winners? Because ratio spreads are so versatile and they are so flexible, you're going to have to use a lot of discretion in handling these situations.

But if the stock does rally and the options move further and further out of the money, you're going to want to look to capture most of the credit that you have collected. So, for example, let's say you put a ratio spread on at entry for 60 cents. If you can buy that thing back for 20 cents a week later, then you might want to consider doing that.

Let’s say you put a ratio spread on for 90 cents. If at some point in the future you can buy that thing back for 30 cents or 33 cents, you might want to consider that one too. Again, there's no hard cutoff point here, so you're going to have to use your experience as your guide.

But do you remember when we said it needs to be economically significant? This is why you want to put yourself in a position to where if the stock does rally and your P&L approaches that credit collected, that it is meaningful. Alright, so now what about those losers?

Well, our reference point for adjusting is going to be that short strike. As long as the stock is above your short strike, then you do nothing. Alright, easy enough.

But now, what do you do if the stock does fall down through your short put strike? How do you handle that situation? Well, the first thing you're going to want to do is check the value of the vertical spread that is baked into the center of the strategy.

If you can take that off for nearly max value, then go ahead and take that off. So, for example, if you have a one-dollar wide ratio spread, then the vertical spread that's in the center is one dollar wide. If you can take that off for 85 cents, that's almost max value.

If you have a 2. 50 wide ratio and you can take off the vertical spread for two dollars, that's also almost max value. Now, where is the cutoff point for determining if it's enough on the vertical spread to take it off?

Well, that's largely going to be up to you, but I can tell you what I do: if I can't get at least 80 percent of the vertical spread's value, then I do not take that off. It off if you are able to close out of that long put vertical for near max value. Now, all you have left is a short put, so manage it in the same way that we did in the short put video.

Just keep in mind that now your total credits collected are the credits on order entry and the credits from selling out that vertical spread. Okay, but what do you do if you can't close out of that vertical spread for near max value? Well, you basically have two options.

First option: you sit and you wait; you do nothing. You can do this here because either one of two things is going to happen: A) the stock goes down. If the stock goes down, then that vertical spread is going to increase in value, and you're going to be able to close it down.

You close it down, you manage that extra short put accordingly, and you move on. Or B) the stock actually rallies. If the stock rallies, then those options could be out of the money again.

This is an even better scenario. But the second option, of course, is you can roll the whole thing out in time. You can pick the whole thing up—the short put, the vertical spread, all the pieces—and roll it out in time.

If you do this, you will reduce your risk and add duration to the trade. Alright, easy enough. But what do you do if the stock just keeps falling?

What do you do if, no matter what you do, the stock will not come back? Well, again, remember if you choose to manage your losers: somewhere around 2x to 3x of total credits received is a really good marker. So, for example, if your total credits from order entry, from rolling out, from closing out that vertical spread—if all of these credits were four dollars, for example, buying it back for twelve would be a 2x loser, and buying it back for sixteen would be a 3x loser.

Alright, so those are the winners and those are the losers. But what about everything in between? What about that dance floor?

Well, since you have that extra short put and this strategy is so flexible, rolling out in time as your default option is not a bad move. But remember, you can always use IVR as your guide. If IVR is still elevated, then keep it on; if IVR has fallen, then take it off.

Wow! You guys made it! The option crash course strategy series has now come to a close.

I sincerely hope that you guys got some value from these videos. If I can ever help you in any way, please do not hesitate to reach out. You guys can email me at jay.

schultz@domain. com or you can hit me up on Twitter at @jsultsf3. So that is it, and I will see you guys next time!