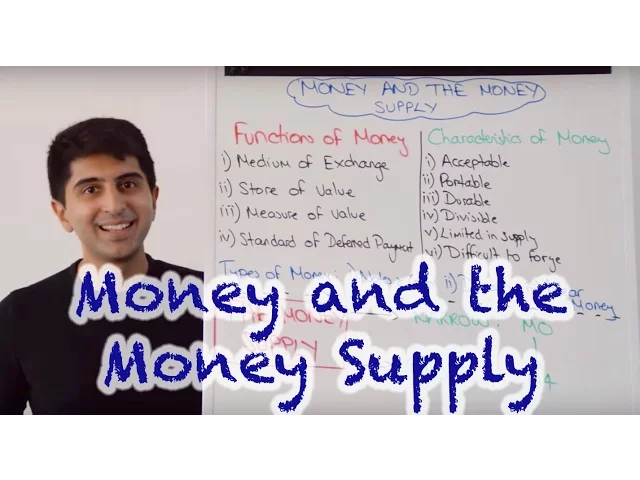

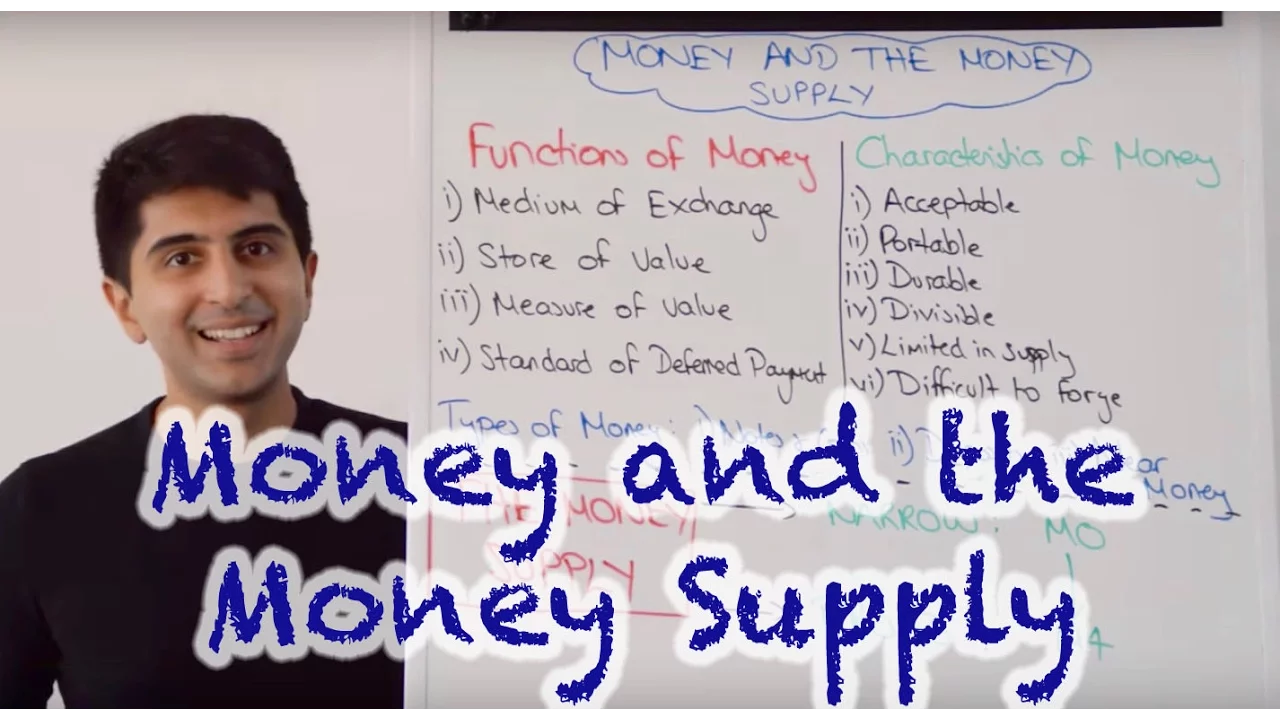

Hi everybody. Money can be anything as long as it satisfies these four functions. It's got to be accepted as a medium of exchange.

And that's really important because the only other option we have is to then barter. And the problem with bartering is for example, if I need pencils, then I've got to hope that the person who's selling me pencils will accept my board pens. If the person selling me pencils does not accept board pens, that transaction cannot take place.

If you have money which both parties accept, then all of a sudden that transaction can take place with money instead. So in a medium of exchange, it's really important. It allows the economy to run.

Basically, money has to act as a store of value. It can't deteriorate over time. For example, if you use commodities like fruits, you know, they go bad over time.

They lose their value. So as a store of value, money has got to satisfy that function. Now think about it.

Inflation over time can erode the value. can erode the store of value function of money whereby a £100 maybe in 10 years time does not have the same intrinsic value to it. So inflation can erode the store of value idea but the basic idea that if you have £100 in your bank account now that £100 is still going to be there in 10 years time even though the actual value of it might decrease because of inflation but you can still store money.

That's important. Money has got to act as a unit of account or a measure of value. So if you have two goods, one good with a price of £10, one good with a price of £25, you know that that good which has got a price of £25 is different in some way to the good that's got a price of £10, right?

It gives you that unit of account function. You know that if there are different prices, these goods are different in some way. That's important.

And also money has got to act as a standard of deferred payment. This is really important whereby people that don't have money right now can borrow it from those that do. meaning that they can pay back that money over time.

That's a very useful function so that people that don't have money now can still buy goods and services paying back at a later date. So standard of deferred payment, the idea of bringing lenders and borrowers together, very important when it comes to financial markets. What are the characteristics that money has to have?

Well, money's got to be acceptable, i. e. act as a medium of exchange.

It's got to be portable. Of course, there's no point having money which is very difficult to carry around. It's got to be easily portable.

It's got to be durable, right? That's important. It's got to be divisible.

Um, whereby it's easy to actually to have it and understand it. It can break down into different units. For example, you know, pence and pounds in in the UK context.

It's got to be limited in supply so it keeps its worth. That's important. And it's got to be difficult to forge.

It can't be easy to counterfeit otherwise people will lose faith in money. Something interesting to know is the difference between commodity money and fiat money. Commodity money is any money that's got intrinsic value.

Intrinsic value. For example, gold. Whereas fiat money, which is what we use nowadays, notes and coins has got no intrinsic value whatsoever.

So if notes and coins become worthless because of hyperinflation, you can't go and trade in your notes and coins for something else. That's it. That money has lost value.

That's fiat money for you. Whereas commodity money has always got some intrinsic value. If you go back 80 years, a lot of countries had what was known as the gold standard whereby your money, your notes and coins were backed by gold.

So if there was hyperinflation which eroded the value of your notes and coins, you know that you could go to your central bank and trade it in for a certain amount of gold. Nowadays, that idea that idea of commodity money has completely gone. We use fiat money, notes and coins.

We have got pure faith in the value of those notes and coins. If anything eroded the value of it, so hyperinflation or a massive currency crisis eroded the value of that money, then that's it. Our savings are worthless.

The money that we have is simply worthless. We have to start again with whatever new money the government decides to to print. That's an important thing to know.

We move on to different types of money. Now, money doesn't just have to take the form of notes and coins. It can vary in liquidity where liquidity is the ease at which money can be converted into cash.

Well, if money is cash, that's the most highly liquid it can be, right? So, yes, money can be notes and coins, what we know money to be. But money can also come in different types as well, which can complicate the idea of what we know is the money supply, which we'll come on to in a second.

But notes and coins, of course, deposits, right? Deposits that individuals have in banks, that firms have in banks, that banks themselves have in the Bank of England, for example, very, very highly liquid that can easily be converted into cash. So deposits are also a very important type of money, highly liquid.

You've also got something called NEA money. These are non-cash assets but can be easily converted into money. So for example, a certificate of deposit whereby you deposit your money in a bank but for a fixed period of time.

You get an interest rate on that over the period of time that you're keeping it in a bank. So maybe 5 years, but your money can't be taken out of that bank account in that 5year period unless you pay quite a significant fee to do so. So in that sense your money isn't as liquid as notes and coins or normal deposits which can be taken out whenever you want but it's still very highly liquid.

You know it's going to become money that you can take out in only 5 years. So it's a non-cash asset but it's still quite highly liquid. Another example of money are bonds for example with maturity dates of one year 3 year 5 years.

You know these bonds will mature in a short period of time but you can also buy and sell them so you can convert them into cash very easily. So not quite as liquid as these two but still highly liquid can be easily converted into cash if you need it. That's what we mean by near money.

Let's now move on to look at different types of the money supply. What the money supply is the money supply is just the total amount of money circulating in the economy. A very simple idea but can get very complex to measure because of all the different types of money that exist.

Right? In the UK, we can look at things in very narrow terms where we have something called M and that is a measure of the money supply which includes simply the total amount of notes and coins out there in the economy but also all the deposits that individuals have in bank accounts. For example, individual savers, for example, banks themselves that have got deposits in the Bank of England, for example, firms that might have deposits in banks as well.

Now, we know that deposits is basically money, right? You can easily take it out and spend with it. Um, so these two are very very very highly liquid forms of money and that's what will be included in M.

You can see how that's a very narrow measure of the money supply. It's only including these very very liquid forms of money and we know there are lots of other types of money that count as well. In the UK we have things like M1, M2, M3 and M4.

And as we move down these different numbers, we are adding more and more non-cash financial assets into our measure of the money supply. Now these themselves are also highly liquid but not as liquid as notes and coins and deposits. So the more we move into higher numbers for the money supply.

So M1 to M2 to M3, we are adding slightly less liquid non-cash financial assets to the point where we finish with M4 which is a broad way of looking at the money supply. Well, yes, we still have notes and coins and deposits in our measure of the money supply, but we also have non-cash financial assets that can still be quite easily converted into cash included. For example, certificates of deposits, for example, bonds.

The Bank of the Bank of England will say that alongside notes and coins and deposits, also what's included and counts as money in M4 are non-cash financial assets with maturity dates of 5 years or less. I that can can be that can be converted into cash in 5 years or less or that can be bought and sold easily and be converted into cash. So just simply learn the broad measure of money supply i.

e. M4 as notes and coins and deposits as M but also non-cash financial assets that is still highly liquid i. e that is still quite easy to convert into cash.

Don't over complicate the money supply. Keep it simple like that. That's it when it comes to money in the money supply.

Thank you so much. Stay tuned for the next video where we look at the quantity theory of money and how we can look at the money supply and the link to inflation.