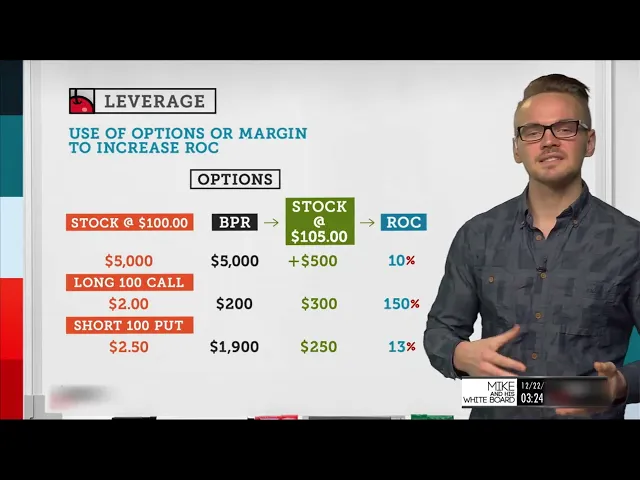

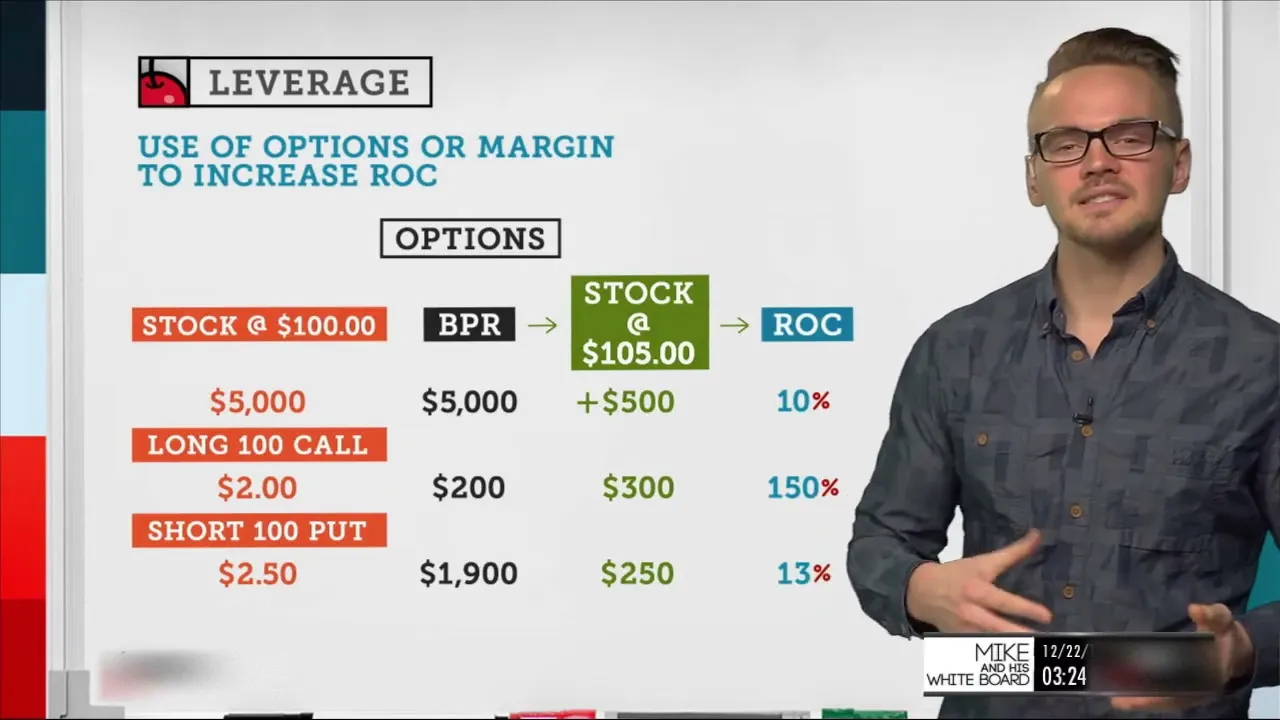

[Music] hey everyone welcome back to mike and his whiteboard my name is mike this is my whiteboard and today we're going to be talking about leverage so when it comes to trading in general and options trading specifically we get a bunch of leverage with that so instead of just buying stock outright and paying the full amount for stock if we have a margin account we get some leverage and using options we have some additional leverage as well in that same very margin account so let's get right into it and we'll we'll talk about a few different examples of different situations where leverage can help us or hurt us so the first thing to understand when we're talking about leverage is that it can magnify our wins but also magnify our losses so anytime we're dealing with a leverage situation and specifically with trading we're talking about being able to put up less cal capital than required for a certain trade which allows us to enhance our return on capital so as you can see at the top here the use of options or margin account to increase return on capital is my definition of leverage so let's go to the next slide and we'll talk about a few examples when it comes to leverage specifically so right here we're going to be talking about a margin account and different ways of buying stock so let's say we've bought long stock at one hundred dollars a share and we're we're going to be talking about 100 shares so everything you see here is going to be 100 shares of stock so let's say i'm in a cash or ira account where i don't have any additional leverage so if i bought 100 shares of long stock at 100 it would cost me 10 000 to do that now let's pretend that along the line the stock ends up moving to 110 so that's going to show me a profit since i bought it at 100 and it's gonna be a thousand dollar profit so if i've got ten thousand dollars that i put down to buy those shares and i've got one thousand dollars of profit my return on capital as you see here is going to be 10 however if i am in a margin account and i actually do have that leverage handy then i'm gonna get two to one leverage on stock so i can buy this the same amount of shares so the same 100 shares at 100 but it's only gonna cost me five thousand dollars to put down because i'm getting two to one leverage so because of that if i'm up one thousand dollars on this position but i only had to put down five thousand dollars that's going to be a return on capital of 20 percent so as you can see when i'm buying stock in a margin account compared to a cash and ira account my return on capital doubles because i'm getting two to one leverage as opposed to one to one or no leverage at all when i'm dealing with a cash or ira account so what's important to note is that when we have leverage it increases our return on capital but it can also increase our losses so let's pretend the stock goes to 90. if i have the shares here or i put down 10 000 to purchase the shares and the stock goes to 90 i would have lost 10 percent on that investment originally but if i'm in the same position where i'm only putting down 5 000 it would magnify my loss i would be at a loss of twenty percent because i would be losing one thousand dollars against five thousand dollars down when you compare that to one thousand dollars against ten thousand dollars down so it's important to note that when we're dealing with leverage it can magnify our our wins but it can also magnify our losses so let's move along to the next slide and we'll talk about leverage with options so when we talk about options there's a few different ways that we can get leverage so in a margin account when we buy options basically it's going to be whatever the capital is that's required or whatever the debit is paid that's going to be our buying power reduction so in any account i should say so whether we're dealing with a cash ira or margin account that's going to be the same so if i buy an option in a cash account or ira account or margin whatever i paid for that option is going to be the amount required for that there's no no additional leverage on buying options however when i'm selling in options that's not the same case so let's walk through a few scenarios here and we'll get down to it so let's say we're buying that same stock at 100 in a margin account so i've got five thousand dollars to put up to buy those 100 shares and if i'm looking at buying power reduction it's going to be the same value as you see it along here so my buying power reduction is going to be 5 000 because i'm putting down 5 thousand dollars to own those 100 shares and let's say the stock goes to 105. so now the stock only went to 105 instead of 110 so i would see a 500 net profit here which is going to give me a return on capital of 10 percent so in a margin account when i just take the max the profit here and divide divide the buying power into that it gives me that 10 value now if i'm looking at buying a long call instead of buying the shares outright again with a call i'm going to have an expiration date so it's going to be it's going to be a lot more cost effective in that sense but because of i have an expiration date i don't have that unlimited reason to be right so i i have to be right in a certain amount of time by a certain magnitude to be profitable so let's say that i was so let's say i buy a 100 call for two dollars and again every option contract is the theoretical equivalent to 100 shares so if i buy it for two dollars it's really going to cost me 200 so my buying power reduction or the the amount reduced from my account would be 200 and if the stock's at 105 my call will actually be worth 500 if i want to go sell it at expiration for full intrinsic value because again if i'm buying a call which controls 100 shares and that strike price is 100 if the stock price is 105 i have 5 points of intrinsic value there but since i paid 200 for that i would take 500 subtract the 200 i paid for it and that gives me the net value or net profit of 300 so taking this all together i put down 200 and i netted 300 on top of that so my return on capital would be 150 which is much higher than the return on capital of 10 but let's say i go a different route and instead of purchasing options we look to sell a put instead so this is something more along the lines of what we would do here at tastytrade so let's say i decided to sell an at the money put instead so i sold a put at one hundred and i collected a credit of two dollars and fifty cents which is really two hundred and fifty dollars so the reason that my buying power is very different than what you see here is because of the fact that when we're selling options in a margin account we do get additional leverage it's not the full amount that's required for the trade so if we know that a put contract is the right to sell shares at a certain value if i'm selling someone else that right to sell me their shares you would think that in an account i would need to put up the full value of those shares but in a margin account that's not the case in a margin account i might see my buying power reduction be somewhere around 1900 so in a margin account i do get that buying power reduction relief but in an ira and a cash account i would not so i would i would have to put up that full value of the 100 shares but since we're talking about a margin account we'll continue on and see what the return on capital is so let's say i have a buying power reduction of nineteen hundred dollars and i collected two hundred and fifty dollars for selling that put if my stock's at 105 at expiration that means that my put is going to be out of the money and it'll expire worthless because if a stock's at 105 and the right that is associated with the put is to sell shares why would anyone who purchase that put sell their shares at 100 when they can sell it in the market at 105 they wouldn't which is why that put would be considered out of the money there's no intrinsic value there and for that reason i would be able to keep that premium i originally collected and it would be profit so i would be profitable to the tune of 250 against my 1900 that was reduced for buying power which gives me a return on capital of 13 so it's just a bit higher than buying the shares outright however what's important to remember is when we're selling options i can be correct in two out of three ways so when i look at these other two options here for me to be profitable when buying stock outright i need that stock to go up it can take its time going up if i own the shares because there's no expiration date but in the end it does need to go up for me to be profitable if i'm looking at buying a call it's the same but it's going to have to go up by a certain magnitude and that magnitude can be measured by the amount i paid for the stock so or the call option i should say so my break even here if i'm looking at a 100 call that i purchased for two dollars my break even is really at 102 and the stock has to go above 102 before the expiration or buy the expiration for me to be profitable in this case it did but if it went to 101 even though this owning the stock would be profitable if the stock went to 101 if i bought by the call and the stocks at 101 it would not be profitable at expiration because i need it to be above 102 to be profitable however if i sold a put my break even is actually helping me on the downside so remember i collected that 2.

50 credit so if i sold a put at 100 for 2. 50 cents my break even is actually at 97. 50 so that's going to give me a lot more room to the downside to be correct and even if the stock stays right at 100 i'll still be profitable and i can keep that 250 credit because the option would still be worthless as long as it's at 100.