well oil prices remain high as and as mentioned staying close to three-week highs on Rising demand from Asia and the continued conflict between Israel and Hamas in the Middle East and big names like BP Chevron and Shel have all reported their second highest annual profit in a decade on increased production let's bring in Kim fusier Fier HSBC oil gas research director to discuss how to navigate the energy space Kim it's good to talk to you today are there additional Tailwinds here that could push uh the profits higher or is this as good as it gets

thanks for having me on the show um I think as always oil and gas prices will be really key to the sector Outlook um if you look at consensus for Brent this year it's already about $82 which is bang in line with spot prices so right now we can't count on earnings upgrades to live the sector higher um in the near term we do think oil prices can be supported around current levels or even rise if there further escalation in the Middle East U that said let's not forget that OPEC has ample spare capacity over

5 mlion barrels a day and that should cap the upside maybe around 85 or $90 um in the second half of the year in fact we expect oil prices to slide back under $80 when OPEC and and Saudi Arabia bring volumes back to the market um I think I should also mention another downside risk for the sector which is natural gas prices prices in Europe have fallen back to almost normal levels just 2 years after the 2022 energy crisis and that's really surprised us also in the US natural gas prices have cratered recently because of

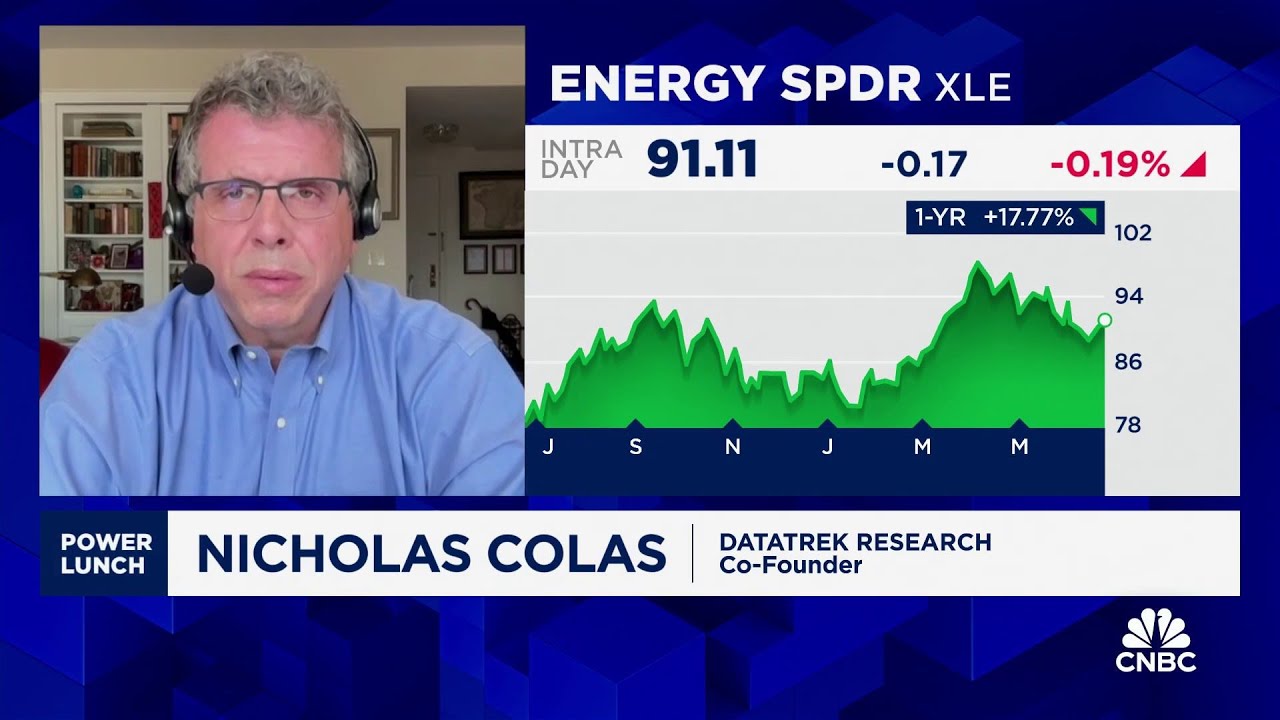

warm weather but if you take a step back in this environment it's still a very solid macro environment for the oil and gas companies and they're still able to return a 10% Total distribution yield including dividends and BuyBacks balance sheets are in pretty good shape so companies are able to absorb short-term macr volatility and so Canim with that in mind then who are your top picks your top three picks here uh in the oil sector the energy sector as a whole is cheap and unloved and so we would expect the sector to rates if the

companies are able to demonstrate good performance quarter after quarter our top three picks are BP shell and Chevron so for BP and shell we think they are good rate of change stories they've got new leadership teams um BP surprised positively at Q4 results by giving much more visibility and stability in its quarterly buyback program shell is also executing better and becoming more consistent and then Chevron we think is a good growth story where its organic growth has been further boosted by the hes acquisition and it trades at a uh decent discount to Exxon uh Kim

the broader narrative within the industry has really been about this transition or whe whether in fact there will be a significant transition away from fossil fuels you named BP as one of your picks there I mean this is one of those companies that has been more aggressive in that uh in that transition into clean energy under previous leadership with Bernard Looney um is that diversification important as you sort of assess where these companies are going to proceed at least in the medium term how significant a headwind or Tailwind does that provide I think if we

take a step back Global oil and gas demand is still growing we can see that in the statistics um and so despite continued pressure from ESG investors particularly in Europe the the European Majors including BP and shell recognize that and so they have to strike the right balance really between being forward leaning um investing into into clean energy but also making sure that they've got valuable businesses and continuing to invest in oil and gas and that's exactly why you seen both BP and shell tilting back towards growth in oil and gas at least in the

medium term for the next two three four years and then at the same time pulling back from Renewables but not abandoning Renewables altogether Renewables still represent something like 20% of BPS and Shell's capital investment programs so that is still definitely something that investors need to continue to care about and Kim in terms of the both on the supply and demand side here where do you think that's going to be coming from especially people still waiting for that that China demand to unlock I think what we saw last year was probably the last of the post

covid Rebound in oil demand we can't possibly expect that to happen again in 20124 there is no more pent up demand that needs to come back uh from the from the covid lockdowns so I think what we're going to see this year is most much more of a steady state on Trend growth in all demand we're forecasting 1.3% growth an oil demand and that can be entirely met by OPEC as well as non OPEC sources including us Shale as well as Guyana Brazil Etc so as time goes on it is going to be harder and

harder we think for OPEC to continue to maintain control over this oil Market they've got five million barrels a day of spare capacity on the sidelines that will need to come back at some point in time and at some point it will become an overhang uh Kim finally I wonder how you assess um this pause in approvals of LG exports coming through from the Biden Administration certainly a lot of push back coming from the sector here but you know at least in the short term here what ises that ultimately mean for prices well the first

thing to say is that existing and under construction us cell andg projects are not affected it it only affects projects that have applied but not yet received approval um so the near-term impact really on prices is minimal the US and Qatar are driving a big wave of capacity additions and the LG Market is going to be oversupplied probably from about 2026 onwards and so the impact of the ban will very much depend on how long it lasts um a one-year delay is not a GameChanger but a longer pause could affect new lery supplies in the

longer term and then that could tighten the market it could also damage confidence in uslg and it could benefit projects outside of the US in the Middle East in Africa maybe even Russia from a domestic perspective let's not forget that ly exports had a few useful benefits um they made it easier for producers to produce oil from gassy Shale formations because that gave gas a place to go so the more the longer the ban stays in place the more you'd expect us gas prices to stay low because they have nowhere to go that's not great

for domestic producers but it would be good for companies that are able to play the Arbitrage between us gas prices and international gas prices and we do continue to track that natural gas year to dat down about 38% continuing to see that pressure I appreciate you joining us with your insights Kim fusier HSBC oil gas research director thank you so much thanks for having me