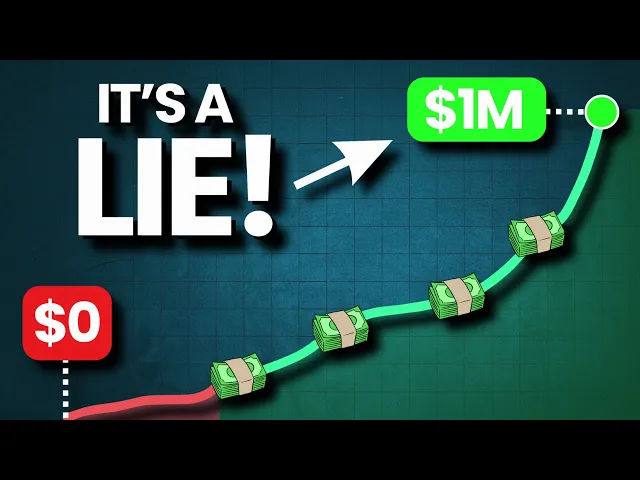

today I want to talk about compounding and how the media sometimes lies to you about this spectacular Financial phenomenon I will unveil four different misconceptions when it comes to the power of compounding that I think every private investor needs to be aware of so without further do let's get [Applause] started all right hi there my name is r zelman and this channel is about long-term investing long-term investing in quality stocks but of course every once in a while I also talk about more fundamental personal finance Concepts I've actually just recently released a video on the power of compounding and outlined why it is my number one wealth building secret and in it I shared the following visualization I'm just going to show it to you again here that nicely Illustrated how over time the power of compounding the wealth building process piix up pace so I was showing that if you are investing just $1,000 a month for 30 years you will end up with more than 2 million us however just reaching the first $200,000 will take you 33% of that entire time period so almost 10 years the other incremental $200,000 that you then gain over time will be achieved much more quickly going from $600,000 to $800,000 for example only takes you 8% of the total time needed to get to the 2. 2 million USS you see at the end going from 1. 4 million to 1 .

6 million us only takes you 15 month so a little more than a year and I guess the key takeaway from this illustration is that you have to play the long game in investing if you want to do well now while clearly the power of compounding might be the most underestimated tool in every Investor's toolkit I think there are a couple of misconceptions surrounding this phenomenon course after all I will show you that the power of compounding in the real world due to a couple of different factors is not as powerful as the media sometimes wants you to believe so again we are going to take a look at a specific case and let me just outline some of the assumptions that I have made here so we are assuming once again that we are investing for the long term 30 years we are investing $1,000 a month so that's $112,000 annually our money is compounding on an annual basis and it is compounding at an annual rate of 10% a year so basically we're assuming an investment in a passive ETF I know some people might point out in the comments down below that going forward the return you can expect from a broad passive EDF is maybe a little lower but we want to simplify it and just use some round numbers here so 10% a year over 30 years $11,000 a month if we put these numbers into a compound interest calculator you will see that after 30 years you will end up with a net worth of$ 2. 08 million us which is not bad for someone who is just earning an average income and contributing an average amount every single month for a long period of time however and I'll get to the point of this video I think there are a few factors that you need need to take into account which will make the final outcome look a little less impressive the first one are fees I just said we are investing in a broad Market ETF and even the cheapest ETFs in the world they still charge you a fee for the service that is provided by the ETF provider some of the cheaper ETFs the broad Market ETFs by the big ETF provider they charge total expense ratios in the range of 0. 1 to 0.

2% so if we head back to our compound interest calculator now and instead of assuming an annual return that is compounding over time of 10% go for 99. 8% this already reduces our final net worth from $ 2. 08 million to just chy above $2 million so over time over 30 years the 0.

2% in fees that I was assuming here will cost you around $80,000 which brings me to the second factor to be aware of and this one is even more meaningful taxes now let me walk you through the Imports and the assumptions I was making here so of the2 million us that we end up with after 30 years around 1. 64 million were capital gains the other $360,000 us were basically our contributions that we made over the 30-year time period but the capital gains they will of course be taxed and I was just taking into account the tax rate that I as someone living in Germany would have to pay once I realize these Gams and the Capital Tax range in Germany as of today is around or maybe not around it's pretty precisely 26. 375% so 26.

371 mil 641 th000 in capital gains represents 4 3,200,000 so of course we have to deduct this from our final net worth which brings us to a final net worth after 30 years of 1. 568 million us all right before we move on to factor number three I would like to know from you where do you live and what is the current capital tax rate in your country please share it in the comments down below and let me know what you think of what kind of capital gains tax you think would be appropriate to charge by the government okay with that being said Factor number three the third factor that is going to eat into your actual returns is inflation because after all often times it is distinguished between normal returns so that that would be your return before taking inflation into account and your real returns which adjust your returns to the inflation rate over that holding period so we just figured out that after fees and after paying capital Tain gain stxs we end up with around a little more than 1. 5 billion US what I was doing now I was taking a look at an inflation calculator that calculates the purchasing power of a specific sum of money considering specific inflation rates and I was assuming an inflation rate of just 2% which is lower than the inflation rate we are experiencing right now but it's basically the the target of most central banks around the world and if we are assuming an inflation rate of 2% over 30 years well then our final net worth the 1,568 100,000 will only have a purchasing power of 86500 th000 in 30 years so again this is also a major headwind and of the three we have discussed over the biggest headwind so the only way to actually tackle this would be to adjust your monthly contributions accordingly adjust your monthly contributions as your salary Rises hope fully in line with the rate of inflation I've actually done the calculation here so if we are adjusting our annual contribution by just 2% annually we will end up with 2, 38300 th000 us after 30 years assuming a rate of return of 99.