Hey there, I'm James you're watching Accounting Stuff and in this video you'll find out how to calculate depreciation using the Units of Production Method Depreciation is the process of reducing the book value of a tangible fixed asset due to use wear and tear the passing of time or obsolescence The Units of Production method of depreciation is a variable cost depreciation method where expenses mirror the actual physical use of the asset Picture this... One day you decide to make the move to the Pacific coast of Canada there are more trees here than you could ever imagine

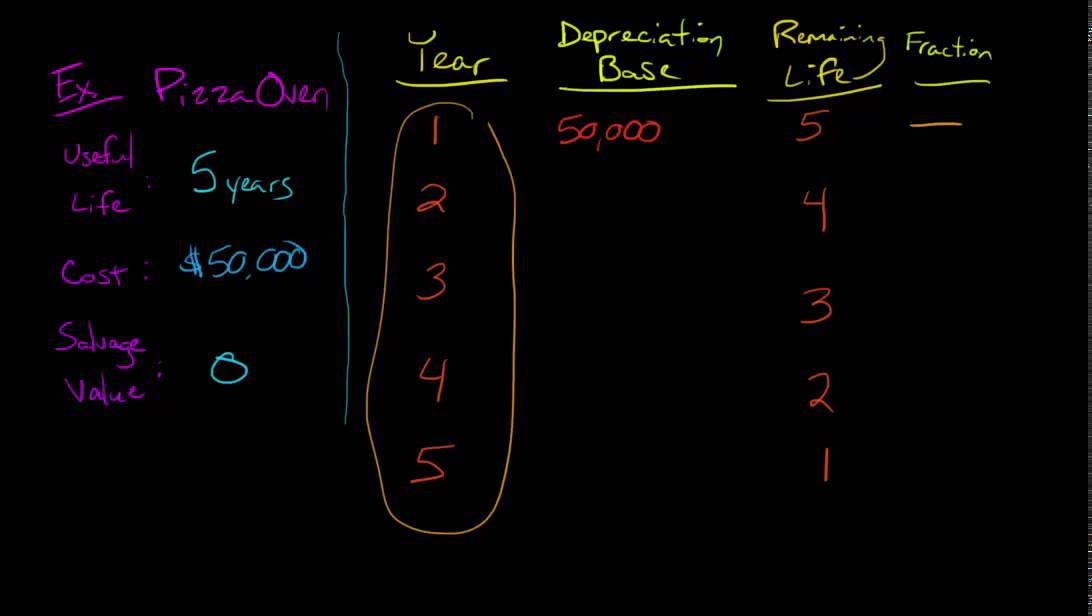

and being an enterprising young person you decide to open up a sawmill So you secure location and buy your first sawmill machine it costs you $10,000 Your sawmill machine is a tangible fixed asset it's tangible because you can touch it and it's fixed because you plan to use it for a long time This one can produce 150,000 units of timber and after that it will be worth $1,000 in scrap Let's depreciate it using the Units of Production method Step 1 Write down what you know Your asset is a sawmill machine and we're going to use

the Units of Production method of depreciation The asset cost is $10,000 it's residual value is $1,000 and we expect it to be useful for 150,000 units We'll calculate the depreciation per unit and depreciable cost in Step 3 Step 2 Build a depreciation schedule A depreciation schedule is a table and in the units of production method it has six columns We have… Year opening book value number of units produced depreciation expense accumulated depreciation and closing book value The number of units produced is an extra column that we include for the Units of Production method we need

to track this period by period to help us work out your depreciation expense Step 3 Calculate the depreciation expense accumulated depreciation and book values for each period Now it's time for us to fill out the schedule and we'll start with year one which is the first accounting period You're opening book value is the carrying amount of your sawmill machine at the start of the year and in year one this is $10,000 the same as your asset cost Your business carefully records the number of units produced and it turns out that in year one that was

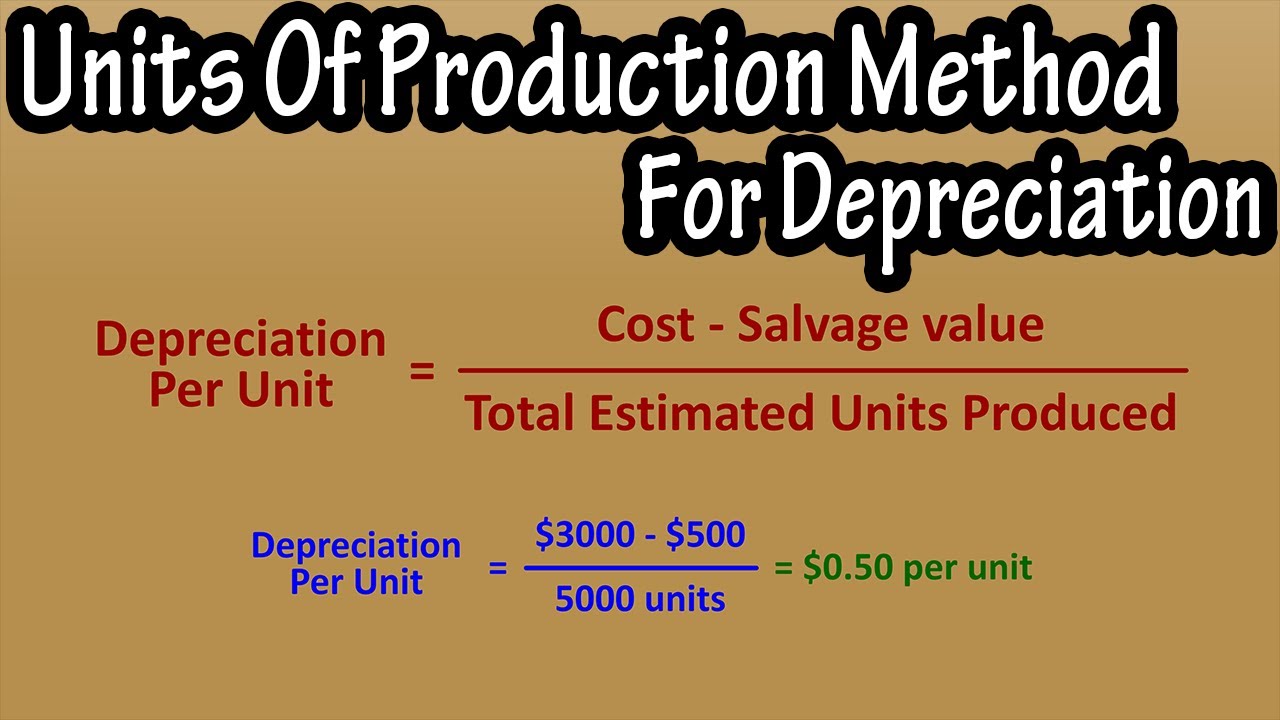

18,000 units of timber Now your depreciation expense is your depreciation per unit multiplied by your number of units produced We can work out your depreciation per unit by taking your depreciable cost and dividing it by the total useful units What is depreciable cost? It’s your asset cost minus residual value it represents the portion of your sawmill machine that will depreciate over its useful life time Your asset cost is $10,000 and it's residual value is $1,000 so your depreciable cost is the difference of $9,000 We said that your sawmill machine can produce 150,000 useful units so

your depreciation per unit is $9,000 divided by 150,000 units which comes to $0.06 or Six Cents per unit By the way depreciation per unit is very similar to the depreciation rate that we discussed in my other videos but depreciation per unit is expressed as a cost per unit whereas depreciation rate is a fraction of an assets useful life As usual you can find this formula on my depreciation cheat sheet and I'll drop links to that and the whole depreciation playlist down in the description Anyway we can now calculate your depreciation expense this is your depreciation

per unit multiplied by the number of units produced You produced 18,000 units in year one so if we multiply that by Six Cents per unit then you've got a depreciation expense of $1,080 this is the amount of your sawmill machine that you’ll write off to your income statement Here's another thing to bear in mind your depreciation per unit is constant but your number of units produced will change each year So your depreciation expense under the Units of Production method is going to be a variable cost to your income statement it’s going to mirror your actual

physical use of the asset Accumulated depreciation is the cumulative total of all depreciation expenses incurred In your first accounting period it'll match your depreciation expense Your closing book value is the carrying amount of your sawmill machine in your balance sheet at the end of the year It’s your opening book value of $10,000 minus your depreciation expense of $1,080 which is $8,920 This then becomes your opening book value for year two Let's say it's a slow year and you only manage to produce 13,000 units of timber this time around Again your depreciation expense is the depreciation

per unit multiplied by your number of the units produced Depreciation per unit is a constant Six Cents per unit and you produced 13,000 units So your depreciation expense is Six Cents per unit multiplied by 13,000 which is $780 Your accumulated depreciation is the cumulative total of $1,860 and your closing book value is your opening book value of $8,920 minus your depreciation expense of $780 which is $8,140 If we repeat this process for the next few years then this is what we're left with Notice that your depreciation expense changes each year in proportion to the number

of units you produced We can see this better on the graph This shows your sawmill machine's book value over time Your asset cost is $10,000 its residual value it's $1,000 and your depreciable cost is the difference of $9,000 Under the Units of Production method your depreciation expense is variable because it changes each year mirroring your actual physical use of the asset I outline of all of this on my depreciation cheat sheet which you can find over here and if you missed out on any of my other depreciation videos have no fear there in this playlist

right here See you next time