and last but obviously not the least to report we've got Nvidia the AI chip giant with a market cap greater than $3 trillion dollar will close out the Magnificent s reporting towards the end of November joining us for more we've got toshia Hari he is Goldman Sachs head of us semiconductor research and he holds a buy rating on Nvidia Tosh it's always great to speak with you because you have such great insights into envidia I know that you recently met with Jen sen Juan you also had him speaking at the Goldman Tech conference earlier this

year what is the biggest thing that you learned from those conversations that is going to impact your thinking heading into nvidia's print of course uh thank you so much for having me Madison um you're right we did have Jensen attend our conference uh in early September we were also on the road with him and the rest of the team uh very recently um look there are a couple of things first uh in terms of the demand profile out there um the environment continues to be very robust um if there's a problem it's a supply problem

not a demand problem you've got the large hyperscalers uh which you know we will hear from next week uh from from a couple of them uh they're still in the early stages of the buildout uh from an AI infrastructure perspective uh the customer profile is broadening beyond the hyperscalers into Enterprises and also sovereign states so there is demand uh across the board there um secondly um I think there's there's been this perception historically that Nvidia is very strong in training um yet their competitive position could potentially dilute um as we transition to inference uh as

you look at the most recent models that have come out from open AI the complexity uh from an inference workload perspective uh is going up has gone up and as that proliferates to other models we think that will only grow uh nvidia's growth opportunity set and potentially expand the the competitive mode that they have um so again demand very strong competitive Mo uh very sustainable as well yeah so tshi it sounds like saying that any concern almost of the fact that Nvidia could be slightly losing their dominance or the fact that some of these smaller

players are are gaining maybe more of a Competitive Edge or or or better to better able to compete with Nvidia it doesn't sound like that's worrying you at all it it's something to to definitely keep in mind and and be cognizant of and there you know a handful of of startups that that um are making really good progress uh there are other Merchant uh companies as well that compete effectively uh with Nvidia but when you think about nvidia's ability to really innovate across uh multiple uh components if you will it's not just the GPU they've

got their internally designed CPU the grace CPU they've got mvlink uh which is a switch that essentially connects uh multiple gpus they've got ethernet connectivity they have infin band connectivity and obviously they have a very you know broad Suite of of software that augments their Hardware capability so when you think about their breath and their ability to in at at a 12 18mth C Cadence I think it's going to be very difficult very challenging and expensive for others to compete head-to-head with Nvidia I want to get your response tishia from two things that analysts we've

spoken with have called out in a somewhat bearish case on Nvidia though you can't really be bearish on Nvidia right now but they've talked about the potential competitors something like a cerebrus for example they've also talked about the potential slowdown in demand if we do have a macro challenge moving forward which of those two do you think is more likely or do you think that neither one is actually going to be that big of a headwind for NVIDIA yeah it's a great question um between those two Madison I would say the latter uh probably comes

up more and more in our conversations with investors again I I I don't think the company is complacent in any way they are very paranoid when it comes to competition um but again the bigger debate is really uh how to think about sustainability of demand going forward um you know the majority of investors uh we believe are fairly comfortable with Outlook going into calendar 25 the big question mark is calendar 26 um to the extent capex continues to go up uh at the hyperscalers uh potentially uh negatively impacting their their gross margins their free cash

flow what does that mean for 26 and Beyond um so between those two Madison I would uh be a little bit more concerned about the latter but again at this point uh we remain pretty positive on the stock and on the trajectory going forward talk to me about what you've heard from those hyperscalers about their capex when it comes to Nvidia there's been this big question about whether or not we're going to see a return on that investment from hyper hyperscalers what are you hearing about that as of now Madison um I think again as

a group as a cohort uh the hyperscalers are very much in build mode um our colleagues uh Capital uh spending estimates for calendar 25 the bottoms up number is suggesting sort of mid teens to High Teens growth um we do think based on what we're hearing from uh customers and partners and and the supply chain in Asia there's probably more upside risk to to those numbers so again we'll find out as we progress through next week and a couple of the big customers report uh we do think there's potential upside there um again the big

debate is not so much calendar 25 it's really calendar 26 at this point it's very difficult to prove or disprove uh where things are headed Beyond 25 um to the extent we're sitting here in 62 months and the monetization is not there the ROI is underwhelming uh increasingly we would potentially uh become a little bit more worried about not just Nvidia but the companies that really make up the ecosystem from an AI infrastructure perspective but at this point uh again we remain very constructive so T what does that tell us about where the Stock's headed

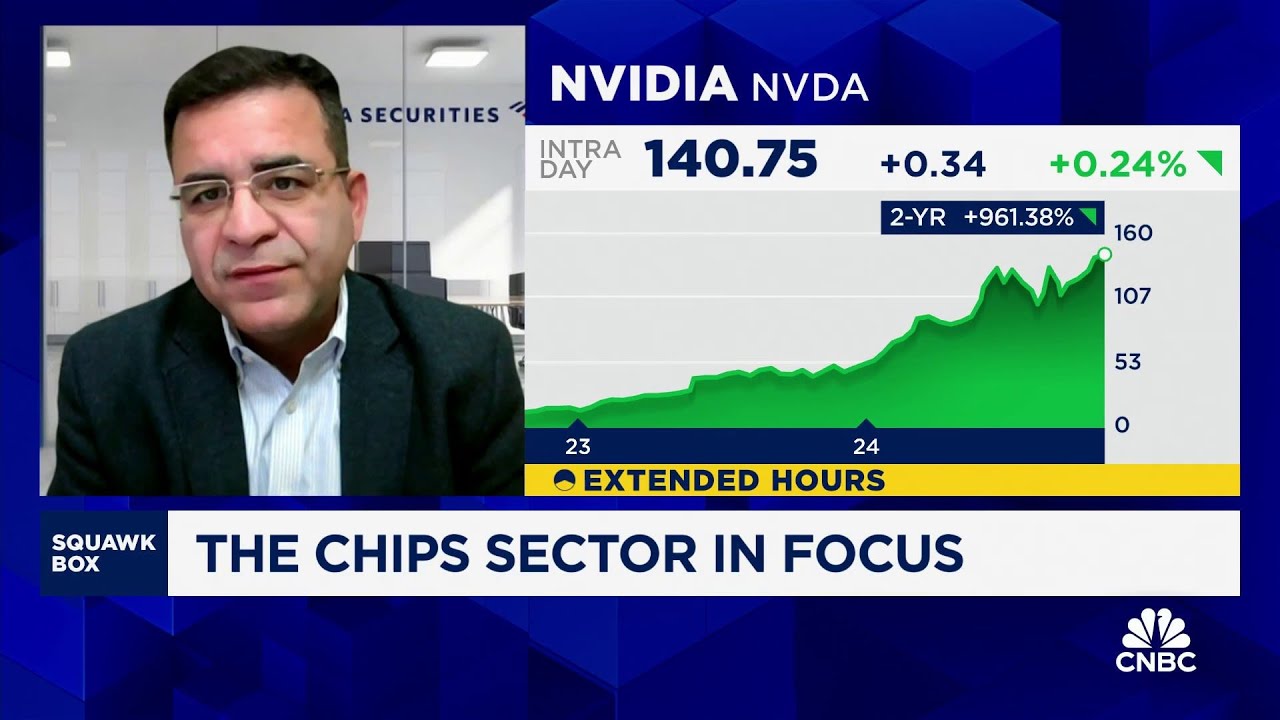

I'm guessing it's headed higher in your view and you see new alltime highs on the horizon that's right uh we do expect upside from here uh when we compare and contrast how we're thinking about the 25 earnings profile the margin profile for the company relative to Street consensus um we're modeling about $465 uh give or take and an EPS for calendar 25 uh as of this morning I believe we're about 15% above Street consensus so you know again we have about a month uh left until the company reports but as we've progressed through earning season

we hear from the hyperscalers we hear from Nvidia in in a month's time we would expect um Street numbers to move up and and for that to to to drive the stock higher as well all right to Hari Goldman Zachs managing director thanks so much for taking the time to join us