Since the rise of the first popular retail trading newsletters in 2008, individual traders and investors have been lied to on the most fundamental level about the reality of building profitable trading strategies. In fact, the lies run so deep that a lot of the retail traders watching this video have probably never even tried to build their own trading strategy because they've been convinced the first step to making money trading is buying or learning a public trading strategy, something from social media or a paid course. I'm making this series in an attempt to finally disrupt the billiondoll lie that has been sold to retail traders for the past 20 years by gurus, influencers, and other financial info products.

And to equip them with the knowledge and tools necessary to conceive of, build, test, optimize, and deploy real, statistically valid trading strategies using the real institutional workflow. By the end of this series, you will know how to test the predictive power of any idea you have with statistical rigor using programming before you ever build a strategy around it. You'll be able to design and build programmatic trading strategies around valid ideas that you find.

How to programmatically back test your strategy over decades of data. How to use code to rigorously validate and stress test a strategy before you ever risk dollar trading it. And how to deploy that strategy only once you've tested it rigorously and professionally.

I'd like to structure this series like an academic textbook. So this first video will be my motivation. Retail trading and retail trading education never became what they were supposed to be which is in my opinion an extension of the tools research and methodology employed by institutions.

Retail trading education from the very start should have been aimed at democratizing [music] these things for the individual trader. But instead its primary aim has always been on selling strategies, signals or stock picks. I'm sure virtually every single retail trader has watched a strategy breakdown video like this before.

In previous videos, I've discussed alpha decay, which is the process by which signals in financial markets lose their predictive power over time. When I explained this phenomenon that is extremely well documented in the financial literature, I was met with a ton of blowback. This was my first time realizing that retail traders are not familiar with the idea that when edges are made public, they cease to exist.

This is why real profitable alpha generating trading strategies are never ever shared. This goes for both institutions and individuals. Hence why institutions will go after even a single trader who tries to run away with one of their edges.

So knowing this, knowing that a strategy which is public cannot be a winning strategy, why have retail traders been convinced that this is the workflow of trading? Step one, pick a public strategy to learn. Choose an influencer, a guru, a mentor, or a course and learn somebody else's pre-existing strategy.

They tell you that to validate this strategy, all you have to do is back test it manually. And all they do is site metrics like P&L, average RR, and win rate on those manual back tests. So, not only do they never talk about programmatic back testing, but they don't even tell you what to do with a manual back test that you've conducted.

It's extremely naive. The next thing they tell you to do is to hone your trading psychology. People say psychology and discipline is 80% of trading, 90% of trading.

It will make trading become easy. So, once you've studied and back tested and dialed in your psychology, the last step is to just be consistent and never give up. Because the only traders that fail are those who gave up.

People emphasize the idea of the trading journey and tell you that it'll take a very long time, a lot of losses to finally win. Here's what's really happening. Step one [music] is to force you to buy something before you start.

It insinuates that it's impossible to start without somebody else's strategy. The brutally naive manual back testing is to make it impossible for you to determine if the guru's strategy actually has an edge. They don't even begin to mention the statistical tools necessary to properly validate a strategy.

Because of course, if you had them, they couldn't sell you a useless strategy. They then massively emphasize trading psychology and discipline to make sure it's your fault if the strategy doesn't work. There's a popular line in the retail trading community that says that every strategy works with the correct discipline and psychology.

If every strategy works when executed with perfect discipline in psychology, then why are PhDs in math and physics hired for tens of millions of dollars a year to [music] develop strategies that will be traded on computers that will be executed by machines with perfect discipline and no psychology? Couldn't they just deploy any strategy on those machines? [music] In step four, of course, be consistent.

The only traders who lose are those who give up. I'll propose an alternative. Insanity is doing the same thing over and over again and [music] expecting different results.

Losing for a long time before figuring things out is not something that should happen. There should be no prolonged and inexplicable losing in your trading because if there is, you're trading something that you haven't validated. The entire retail trading narrative is built around extracting maximum lifetime value from you.

And honestly, I don't blame people for buying into this at all because this is all that comes up when you try to research trading. Trading is the only science where attempting to do research online yields more YouTube thumbnails with gurus and Lamborghinis than it does peer-reviewed articles and textbooks. It is perfectly reasonable for people to fall into this.

My dad is an institutional trader, which gave me a wildly different perspective on this industry really early on. It's a story for another time, but he gave me a correction of course when I first started trading that changed things for me forever. That's ultimately what turned me on to math and programming [music] applications to finance and steered me away from all of this stuff.

Had I grown up without that though, I don't think it's unlikely that I would have fallen into trading these guru strategies and wondered what the hell was going on and never gotten an answer. And that's really why I started posting on social media in the first place at all. I saw this industry of people profiting off of lying to hardworking and ambitious people just continue to grow and grow and just set record years showing that more people are being lied to and scammed out of their money than ever before.

while nobody did anything about it. So, I started posting on short form social media and I mostly started by busting myths, starting to debunk a lot of these crazy almost cultish lies that are taught by retail trading educators. And the feedback I got to that was mostly people saying, "I don't care if it's true or not.

I just care that it works and it does. " So, then I started coding influencers strategies. I coded some strategies and ideas from some really popular people like TJR, a guy named Justin Worlin, and some others.

I showed that many of these strategies and ideas perform terribly, and all of them perform worse than purported. And this is when I started getting comments saying things like, "If TJR strategy doesn't work, then what do we trade? If ICT concepts don't work, then what do we trade?

" That's when I found out that most people really think that step one in trading is learning a strategy. And that couldn't be further from the truth. And in the past, I had shown examples of old strategies of mine that have now been armed out.

And a lot of the comments said, "How did you come up with this? " The strategies I showed required me to build out a bunch of custom infrastructure. These weren't [music] simple trades, and a lot of the comments said things like that.

I think people were entertained by the videos, but they weren't actually anything actionable. And so I thought, how can I show people that this is the right way to do things and it's applicable for the everyday retail trader, the everyday retail trader who mostly trades futures on properform accounts. So that's what I did.

I built a programmatic trading strategy specifically for passing a funded account challenge. If you don't know about these proper challenges, they're basically like a financial carnival game. You have to win a certain amount of money before losing a certain amount of money or you lose your account.

I built and optimized a strategy through Monte Carlo simulation that had a 93% chance of passing the topep account. Then I bought my first ever funded account challenge and passed it on my first try in the minimum number of days. But of course, the two 3minute videos I made on Instagram and Tik Tok about how I built this Monte Carlo simulation, ideated on the strategy, created it, and optimized it to [music] pass a prop from account challenge isn't actually going to enable anybody to do that.

The same way that some short form content about coding guru strategies doesn't teach anybody how to code them, or how content about my own old strategies doesn't show people how to build things that are similar. I've realized over this last year and a half that it's not possible to make the difference I want to make by posting short form content. I can't expect people to see my short form videos and go seek out a comprehensive trading re-education through textbooks, research, literature, and Ivy League education like the one that I was able to have and access to an institutional trader as a dad.

That's why I'm making this series. I want to make it possible for retail traders to build, test, optimize, and deploy their own strategies the right way. I want to make the retail trading industry an extension of the institutional trading industry, which is what it should have been from the start with the same tools and the same methodology just made simpler and more accessible to everyday people.

But I know that no matter how comprehensively or clearly I can explain that workflow, it's not going to be actionable for almost anybody. I knew that walking people through this process in long form while I show myself coding feature analyses and coding strategies would be completely unactionable, just like the short form content. videos of me coding feature analyses or coding strategies or running these strategies through customuilt software for validation doesn't help anybody.

And this was the underlying problem in my short form content too. Every time I showed something, people asked how to do it and I had to say, "Sorry, I built whatever this is. Sorry, I built this strategy or I coded this feature analysis or I coded this risk simulation or the prop from Monte Carlo simulation.

" I can't expect to change how retail traders trade by showing them things that they don't have the tools to do. I realized that retail trading will stay broken until retail traders have the tools to build and test their own strategies. And once they have that, gurus aren't the only place to turn.

They'll be able to build their own strategies privately. That's why I've spent the last 7 months building this infrastructure myself and packaging up every single stage of the institutional workflow from strategy ideation to building to testing and optimization to deployment. And you don't have to code a single line.

I call it quantpad and it's the actual process [music] that institutions use to create trading strategies exposed end to end and made operable and usable by anybody. You don't start with some public edgeless trading strategy. You start in the same place that institutions start with an idea, a feature or features that you can engineer using quantad.

If you're not familiar with that term feature in quantitative finance, a feature [music] can be anything from the weather to if you're an ICT trader, maybe a fair value app or the day volatility. Anything that you think might have some sort of predictive power over other financial variables, you describe that idea and QuampPad writes code to determine if it really has any predictive value. It'll pull the necessary financial data, compute the features that you've described, and then analyze if there are any relationships there, even using machine learning if you want it to.

You can describe any signal or confluence in natural language, and Quampad will determine whether it affects market behavior, how strong that relationship is, and under what conditions it breaks down or thrives. Once and only once an idea shows statistical evidence of an edge, you can start building a real executable [music] programmatic trading strategy around it using a gentic AI to make every aspect of Quampad truly plug-and-play. The strategies are implemented in Trading Views Pinescript, which means you don't have to do any of the stuff you'd have to do if the strategies were coded in Python or C++, for example.

The LLMs that code in Pinescript are fine-tuned specifically for developing quantitative trading strategies in Pinescript. Not only that, but they also have access to a bunch of tools that make the strategy development process so much easier and so much better than if you actually just tried to code it with one of the frontier models like chachypt. I won't get into the weeds on this, but you can compare for yourself quad versus any frontier model like claude or chatpt or anything for coding pine script and you'll see the difference.

I'm really really proud of it. This AI can build really complicated stateful strategies with dynamic risk protocol, lots of confluences and all sorts of things going on. And if you insist on trading a discretionary strategy, it's also very proficient in creating indicators.

Indicators can compute and visualize features that you found on the ideation page so that there's no human error in the data processing process. And if you're trying to build a human in the loop trading system, you can create indicators that give you entry and exit signals based on your entire strategy, but you make the final call to accept or reject trades based on discretion. And again, the strategies and indicators are written in Trading View's PineScript language.

So you literally just copy them from Quantpad to Trading View and they're on your chart. You're not setting up a Python environment or interfacing C++ code with a notification API or anything like that. The barrier to entry here is non-existent.

I made sure that everybody can use this. Then comes the part that retail almost never does, right, which is validating the edge. Quad uses bootstrapping and Monte Carlo simulation to show you the distribution of possible outcomes.

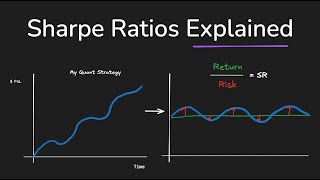

It uses resampling to construct alternate timelines of your back test and stress [music] tests it. Quad has a ton of really important tools for validation that we're going to get into later on in the series. But the important thing is that it goes way beyond just determining whether your back test P&L is positive or negative.

It answers the question of how statistically confident you can be in your edge, whether your back test results are true edge or just luck that'll get you rinsed if you deploy the strategy in real life. From there, Quantpad helps you determine exactly why your strategy is behaving the way that it does. It computes hundreds of features in the background and then reveals the ones to you that are statistically correlated with important things like your draw down, your runup, and your P&L.

It computes and reveals invisible factors that are influencing the performance of your trades, possibly without you even knowing things related to regime, volume, trend, volatility, and a ton of other categories. And then finally, deployment. If you deploy your strategy live on a real account with real money, you do so with an understanding of the risk of that strategy and the expected performance of it that retail almost never has.

And if you trade funded accounts, QuampPad treats them like institutions would, like structured products with probabilistic payoffs, which is the same way that I treated them when I built that strategy that passed the prop firm first try in the minimum number of days. By resampling your strategies back test, it's able to simulate your odds of passing a prop from account challenge. You start by picking from some of the most popular prop account challenges and then you simulate them.

So, Quamped will simulate pass odds, draw downs, resets, fees, and expected value over many different account challenges before you ever risk a dollar. This is the part I want to be really clear about. Quampad is not making retail traders trade smarter within the existing broken framework.

It finally replaces that framework altogether and moves retail trading away from psychology and buying courses from gurus and hoping that something works and wondering why it's not working and to hypothesis testing and statistical validation and datadriven decision-making. That's what this whole series is about. We're going to walk through the entire process that institutions use from step zero to a fully deployed strategy.

And Quampad is the tool that makes that process accessible to retail and makes every single thing I'm going to say actionable to every viewer. This is where the retail world is finally going to start doing things the real way and the right way. I'll be using Quampad starting in the next video, which will be the first lesson, but if you want to check it out now, the link is in the description.