[Music] I picked this paper because I thought it's it's it's quite recent from 2023 and I thought it was really interesting and also there's still quite a lot of uh Trend falling people around there and and make no mistake uh in the in the institutional Finance world so Trend following is still a very big deal and it's actually run there's a lot More financial firms that run Trend falling strategies than there are firms that are running um um say AI strategies so I thought it would be a very interesting and timely topic now when you

um when you look at at the authors zaka Mulin and and also Gina there are no no small um especially zaka moonin he's he's big he's a big guy he's published a lot of papers he's quite well known so usually when you look at what they do it's fairly thorough they Have some interesting um interesting uh ideas and and they come up with some good stuff now what I want to do is first I want to go through some aspects of the paper and I'm not really sure uh but there's probably a lot of as

always a lot of jargon and stuff that a lot of you may not have heard it's not really clear what it means so I want to go through that uh quite a bit and sort of explain to you the all the basic ideas uh that are Combined in this paper because oftentimes we read these papers and I feel the same way and I don't always understand everything that is talked about and and this paper in particular actually combines a lot of these ideas and so what I want to do is really give you the background

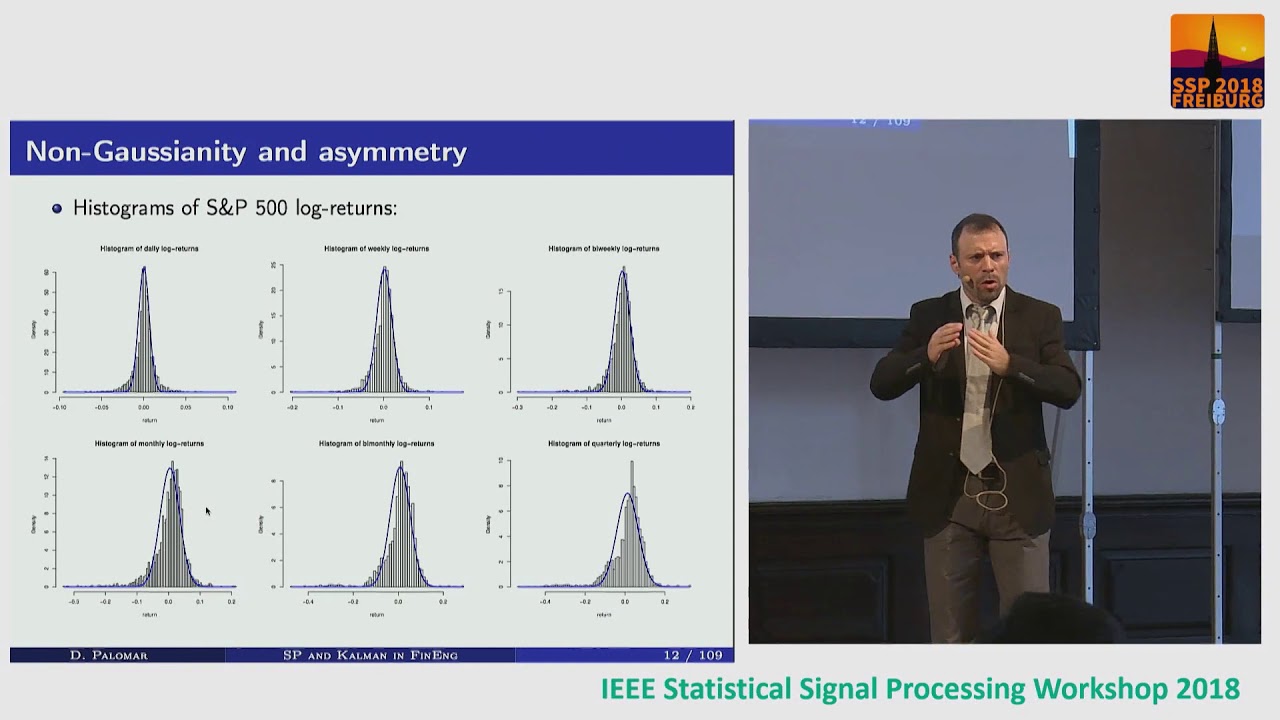

as well and I think actually getting the background can be just as interesting and and and you know when you read these papers actually understanding them you learn a lot about Many many different topics so if you look at the abstract uh the first thing that stands out for me is that sentence however all existing Trend falling rules are essentially at hoc lacking a solid theoretical justification for their optimality this paper aims to address this Gap in literature so what they're really saying is that um you know Trend following is an old thing and probably

quite a few of you have Heard of the turtle Traders um so they're like this famous uh Trading Group back I think in the 80s it was uh that was quite successful they also uh used an early form of trend following and so Trend following is is very old nothing new as I said it's it's been practiced and it's still practiced by a lot of uh uh institutions and what they're saying here is that there is really not much of a theoretical background for that and What I actually want to show is that here is

some Theory and based on that theory what we can do is we can actually find some rules that are optimal under certain conditions and I think that's very interesting because if we actually think well you know my trading uh this is something I want to do is you know Trend following then this sort of uh this sort of practice to actually have a theoretical justification for why you do something Is incredibly helpful because it gives you much more confidence about the things you're doing oftentimes and and I don't know about all of you but but

when I build uh trading algorithms or trading strategies you know I try a lot of things and and I look at them and I go okay this might work this might not work but there isn't really uh necessarily a reason for why this should be the case so finding underpinning theories about that is Definitely helpful so first I want to just give you for those of you who don't haven't got that background I just want to quickly talk about Trend following um just just as a question is is is every anyone not really familiar with

this topic um if you want maybe um you can you can always just say it uh well if if you're all familiar I'll just I'll just I was just gonna say yeah I'm not super familiar but I've uh Um I've see some papers that have been okay yeah okay um all right I'll I'll I'll talk a little bit about it so so what is Trend falling is basically um uses very simple time Series rules uh to exploit Trends now what's important to remember here is that uh Trend fing is often times applied to Futures and

there is a difference between for example Futures and equities equities are often quite correlated so So mostly equities or stocks if you will they have very similar behaviors across the board and so a logical way to exploit them is to actually use cross-sectional rules meaning that for example if you have a list of a 100 different stocks uh you look at you rank them in order for example of what which one has the highest um um value of say say momentum or something and then you go uh long the ones that have the highest and

you go short the ones that Have the lowest it's what you call cross-sectional however in in in Trend following um as it is usually practiced it's done on Futures and it's done in this time series way so rather than actually saying oh you know we we separate into long short based on on a ranking we're actually saying well what does the time series on its own tell me and and based on that uh we actually put on the strategy so normally this is a system that is a lot more popular with Retail Traders and of

course uh uh companies that do Trend following uh usually that's ctas uh commodity trading advisors which is basically hedge funds uh for Futures Trading so so hedge funds usually are more involved in in equities um CT are more involved in Futures and and so because Futures are so diverse there is often not really a reason for why you should rank them because they're so different from each other so what you do is you follow more The time series and that that's mainly the reason uh why this is used in Futures so the um one of

the attributes of trend following is that quite often um you have very tight stop- losses in your your Trend fing systems so when you actually get a trend signal and as soon as the signal goes against you and in in a very small way you actually exit your trade and only if the trend persists for uh longer uh you stay in the trade so if The trade doesn't actually go against you very quickly and the result of that is that in Trend fing often you have uh a lot lower win rate than in other strategies

so in Trend fing you lose a lot but when you win you win big and and usually the wins are much bigger and they outperform all the losses that you may have incurred by exiting early and if anyone's interested uh there is a really good book I like by a guy called Andreas cenov it's called following the Trend uh I think it's an excellent book about Trend following and this is I would say where I learned a lot of my or where I gained a lot of my understanding about Trend following it's also very uh

helpful in learning how to construct portfolios of trend following strategies and so on so if anyone's interested um and check out this book it's it's extremely valuable so the next thing they state in their uh Abstract is uh we show that if a Markov model governs the return process it is optimal to follow the trend using EX and the exponential moving average rule so I will talk about this a little bit later however the mark of model is unrealistic because it does not represent the bull and bare Market duration times correctly it is more sensible

to model the return process by a semi Mar model where the state termination probability increases with age under this framework the Optimal Trend falling blah blah blah so there's quite a lot in here to unpack and especially uh the idea of a Markov model so I will actually talk about this and explain to you what this is and how we can understand a semi uh Mark of model and the other thing is of course uh there's different types of rules trading rules in Trend following for example the exponential moving average rule so I will also

talk a little bit about this and I will show you what These rules mean so first of all I want to uh talk about what is a Markov model and Markov models are quite uh frequently used to analyze time series it's basically a machine learning algorithm that detects uh trading regimes uh using a technique called uh basing inference so uh when you actually build your own Mark of models that quite complicated um in some ways they use a number of different types of algorithms and so Setting them up is no easy feat yourself however there

is a few out of the box packages that can do this and they're very interesting so when you look at the chart on the right side what you can see is this is actually a Time series model that has been and this is actually for Bitcoin USD but but could be anything and that that has been used with a Markov model and you can see there is actually it's separated into three states and when we look at these states You can already see hey that they're quite distinct from each other so for example we see

this red one here this is clearly a strong correction or a bare Market uh well it's not really a bare Market it's more of a strong correction then we see the Green State uh this is more the type of regular trading we would expect it's not really a bull or bare Market but it's more a sort of a regular trading regime and then you can see also here there's Some blue States very View and you would uh probably classify them as an extreme upward correction so so this is a three-state market now what uh people

in the paper talk about is a two-state market and obviously when we talk about a two-state market you know often we think about a bull and bare Market but that's not necessarily always uh the case and you can see this here um you know you've you've got this regular Market but but In this case you know you've got this bullish type Market but then here you also see at the green state is a bearish type market and it's quite interesting because in some sense or in many cases actually we we're not necessarily interested in a

bull or bare Market but we're actually more interested in well is the market a regular type Market or is it an irregular type Market because when we train models we mostly train them on a regular Market operation but Then when the model gets into an irregularity then it it falls over uh you know that's and often if you do this trading yourself you will have noticed that so the notion of like go Bull and Bear and so on is is not always the ideal way of of separating market regimes now what the mark of model

does is quite interesting and and this is we're actually talking about something called a hidden Mark of model here so we can see here here's our three Market States and I oftentimes they're called hidden Market States because we don't necessarily know what these Market states exactly are we we just infer that that they are different states and and the model just separates them in in a sort of more or less automated fashion so there could be Bull and bare markets but there could also be you know regular irregular and and whatever markets now when you

normally deal with a hidden Mark of Model what happens is you have to actually determine how many states you want so you could say well I just want two states or three states or 12 States um depending on what you're interested in and so what we have is we have observed quantities so we have these states and then we have quantities that somehow characterize in which state we're in and these quantities could just be say market indicators it could be volatility Volume maybe maybe an indicator like the relative strength index or something like or the

you know the high low difference of the market uh you know similar to volatility and you know there's there's many many indicators and so what this diagram shows us is that there's two things first we have transitions between these states with a certain probability so for example we could go with a certain probability from State X1 to State X2 we could also with a certain probability stay in state X1 or we could stay in state X2 which is not really shown here and then we could go with a certain probability say from X2 to X3

but as you can see here there's no return path from X3 back to X2 so so once at least in this diagram once we in X3 we're kind of stuck here um but most of the time you know obviously in the market it just jump jumps back and forth between States but it's also staying in States sometimes and then of course um there is a certain a probability that that in state X3 we want to we we observe a variable uh y1 here or Y2 or Y3 and so so you know each state has a

certain probability of observing a set of values uh which is also true right we we we have say our technical indicators and a certain configuration or certain certain uh uh image of technical indicators could be much more uh probable to indicate a bull market Than a bare market for example so for example if the uh fast moving average is above the slow moving average we're more likely to be in a bull market but it doesn't mean we're categorically in a bull market there's just a higher probability of that and uh yeah and so so from

these observations what we then do is we try to infer what state is the most likely state of the market so that's what's called a mark of model now again if you have any questions just Feel free to jump in and ask and and I'll explain Okay now what's a semi Mark of model that they talk about is basically um when we build Mark of models often what happens is that um we actually switch from state to state in in in it's it's quite jumpy let's put it that way so so there's quite a lot

of switching back and forth between different states and then can make the mark of models sometimes a little bit Unstable um and and so so what this also means is the transition probabilities have a certain value and what you do in semi Mark of models is basically you say well uh we have certain transition probabilities but they also depend on how long um how long we have been in in a state so for example if we have been um all things being equal if we have been in a in a in a certain State let's

just call it a bull State uh for uh two Weeks that probability of exiting the state might be lower than if we had stayed in this bull state for two months so what the semi Mark of model does is effectively introduces a Time Factor as well that changes the transition probability based on how long uh this uh State uh has been persisting and in some ways that makes sense you know we we know that that um markets are always changing and and there are is this time element to them and that's what they Refer to

in this paper as the semi Mark of models now um in the next step I want to talk a little bit about uh Trend uh trading rules so so there just these simple rules that uh people talk about in the paper uh that are used for Trend following and that's also quite interesting because when you read for example uh the following the trend book by Andreas cenov you he actually says that well it doesn't Really matter that much um what rules uh you follow they will all more or less uh provide a similar outcome and

in some ways he's right like if you have a a stable strategy it should actually show you you know relatively stable results regardless of the parameters and that's a good thing because if if your strategy is extremely dependent on a specific set of parameters then what usually happens is Out of sample that will just simply not work so you want strategies that are quite robust robust against these changes in your parameters and then the question is of course uh well if that's the case why would we even bother to talk about an optimal Trend following

role well it's it's on one hand it's true that the strategy should be quite robust on the other hand uh an optimal Trend Following rule doesn't necessarily tell you oh this is the perfect strategy that gives you the highest PN L but what it does tell you is this is actually the most uh robust strategy that that is actually really useful all right so uh Trend following rules you see this this is probably the one that most people know it's called the moving average crossover so when you when you have you can see this here

the red line is basically a fast moving average H sorry Sor slow moving no no it's the fast moving average ah sorry it's the slow moving average the red line is the slow moving average uh the blue line is the fast moving average and if the fast moving average is above the slow it indicates for in a trend and when when they cross over such as here we should uh go long and then when we see that the uh blue moving average crosses under the red one and we say well we go short and then

we should be in a bare market and You can see this here we've got this uptrend and then we've got this downtrend now in trending markets this actually works really well and that is basically because you know as you can see here we we we have this right indication and then and then as the trend persists we're we're going along with the trend now one thing you can also notice is for example if you look at this cross and you go straight down Um when this cross over occurs we already are about onethird into the

uh into the bare Market before this cross even occurs and this is simply because moving averages generally have a lag and you can see this here they always lag behind uh and that's just the nature of this there's not much you can do about it so if you actually look and when we enter this so we enter it about here I would say here's the cross we enter it about here and then we exit it about Here you can see that that in fact um you know the the profit opportunity is really just from here

to to about here so it's actually much much smaller than the the actual Trend and that's just generally the case when we do Trend following we never be able to basically go from here to here is it's impossible to actually catch those tops and bottoms perfectly so um there is another uh system that is also based on moving averages it's a macd And macd is similar to this moving average crossover but it has another um it has another line which is basically smoothing this moving average and so so there's different Trend following rules but basically

a combination of this gives you uh the entry and exit exit signals and uh the paper actually explains uh quite well exactly how this rule generally happens one one of the um interesting things about the mecd rule is that that it actually also captures Sometimes Market reversals to some extent so it's a little bit more complicated than the simple moving average and then finally we have uh the momentum Rule and the momentum rule is basically saying well if we had a certain um a certain um um trajectory of our uh price series let's say over

the last 12 months let say say you know a certain uh change in the price of this uh then we expect that this momentum will actually Persist uh sometime in the future so a month or two months or three months into the future and the stronger the momentum that means the stronger the the the the slope of this of this price change uh the you know the more we expect this to persist going into the into the future so you see for for example here we've got the stagnation and then here there's an acceleration where

the momentum increases and then there's a deceleration another stagnation and then A reversal this is a typical Market uh behavior that we can observe unfortunately uh you know we cannot just just easily say that's always like that so so it's not easy to predict the other thing I wanted to say is that when we use these Trend following rules and we're actually in one of these or these moving average rules for one of these stagnation areas here uh they they won't work very well so so often in the case when we have this sort of

scenario then Then uh this this nice moving average usually gets uh obliterated and and and we make quite a few losses in these areas now um all this at least the top two they're based on moving averages and there different types of moving averages there is a simple moving averages where we basically have a window that slid over the prices and then takes the average there's a linear moving average where we wait the most recent data and then we have a linear or or our weights Linearly drop off uh towards the past so if our

window is let's say one year long uh then over uh 252 say trading days uh the waiting gets smaller and smaller until it is zero right at the beginning so so basically that means the last the most recent days get a higher waiting than the past days and that's actually true for the exponential moving average only that instead of a linear waiting here we have an exponential waiting so it drops off faster going backward in Time hope that makes sense let me know so you can actually see this here so this is um um you

know momentum where basically we always have exactly the same waiting um here we have this is actually uh the waiting of a linear moving average so so so so we can see this drops off um here this is exponential um and then there's a few others uh we have for example um here the the moving average Crossover what that means here is that the waiting is basically highest in the middle because we've got the uh the difference between the two moving averages and when they cross over the difference is really small then it gets WI

and then it sort of gets smaller again and if you do the same with cross over with an exponential moving average then it's more of a curve rather than this sort of triangle um Now what what people use said for is so so if we if we look at the paper they do a lot of maths in there and the math is you know it is reasonably complex and so so what they're actually talking about is rather than using prices which is what's normally done in in um Trend following they say well let's use returns

because returns are a bit easier to treat in a mathematical sense but if we do this then we have to take into account these weightings uh to get the Mathematical formulation and this is what this formula shows is basically got this Theta here uh then this is some sort of average uh Theta is the waiting and then this is the return so so actually uh our I is the indicator uh we're actually uh transposing our uh price based indicator to a returns based indicator using these waiting schemes and and that again that that becomes more

important further down when we talk about these Regimes so um the next thing they talk in the uh paper about is auto regression and again if anyone has any questions uh please there's no stupid questions so feel free to ask I know it's quite a bit to to to take in so so I'm I'm happy to explain it to you in more detail so Auto regression um what this means is that past returns are correlated to current returns so um when we when we basically draw a chart where we take all the past returns of

a Time Series and then we shift them by one day and then uh um we we basically regress Uh current returns against the returns one day ago and we can see that as a correlation just like this then our time series becomes somewhat predictable so let's say uh there is a correlation we can say well if there is a positive correlation then we can assume that the returns yes or if we had positive returns yesterday there is a higher probability that we also have positive Returns today day that's what's called positive autocorrelation now um there's

also something called and and this actually positive autocorrelation another word for that is also Trend so so a trend is basically a process where today's returns are correlated positively to yesterday's returns now there's the opposite where we have a negative correlation so that means that if today's uh yesterday's returns were Positive today's returns are more likely to be negative and when we have that process uh we then call that a mean reverting process so here you see the the mathematical uh definition basically of trend and mean reversion so trend is not just something uh price

is going up or down consistently it's a bit more it's a bit deeper than that and actually is it's got a lot to do with the correlation between uh different uh Returns in different days and the reason why I bring this up is because the paper uses this idea of autocorrelation and they're basically saying mathematically autocorrelation and auto regression which is basically this regression process are mathematically uh analogous to this Mark of model so they talk about this Mark of model to basically indic indate uh okay we have um different regimes in the market and

when we have that we can also Say well this is actually similar to uh this this Auto regression which is basically autocorrelation uh but for different time lags so so um you know we can have an autocorrelation uh from today between today and yesterday but we could also have an autocorrelation from today uh to let's say one week ago and and that's actually and you would say well why would we do this this is quite important because for example uh the returns or the return behavior of of Let's say a stock this Friday is probably

more similar uh to the return behavior from the previous Friday rather than the return behavior from yesterday so so just looking at the at the return of yesterday is not always enough you also want to look at well what happened around the same time a week ago or around the same time let's say a month ago so so this is where autocorrelation comes in and auto regression and and where that becomes quite interesting now If we don't have any auto regression in the system we talk about a system that is a random walk and for

those of you who are a bit more mathematically inclined you probably know that with a random walk it is actually impossible to consistently make profits so only if we have some sort of autocorrelation in a system we can actually make predictions about the system okay so um here is a bit of math for those of you who like it uh I talked About the um equivalence between the auto regression and the mark of models and so uh this is what it looks like mathematically here this is uh What's called the transition probabilities of the mark

of models so what it means is we have two states a a a and b and so uh these PS are probabilities that uh our system stays in state a this is a probability our system goes from State a to State B this is a probability of system going from State B to State a and This is a probability staying in state B and then um we also have probabilities uh for the occurrence of the state so that's actually different from this this is the transition between the states so you could imagine that uh just

just from the uh slide we have seen about Markov models that you know we got a lot more green States than red States so so the probability say of being in a green state is a lot higher than of being in a Red state so so these probabilities are not just 50/50 and then when we take these probabilities and these transitions and we plug them in this like quite lengthy equation um then we get this row here and the row is basically uh the slope of our autocorrelation at a different leg so if we go

back uh if we go back to this slide this slope here uh is basically uh this this row and so this is the equation that correlates uh these Mark of uh properties with the auto correlation and so this is the mathematical justification for doing that for those of you who are a little bit more interested in the mathematics so now um this is the figure that that probably is is really interesting um because what this does is it sums up all the considerations we have uh previously looked at so we looked at Mark of models

uh we looked at moving averages we Looked at Auto regression and what this shows is that um the correlations of Auto regression um at different legs are essenti are essentially the same as the weights for our optimal Trend following rules so what they have basically done is they they have taken those um Trend following uh rules and formulations um for the returns and then they optimize them on some insample Le uh data set so the data set is you know It's quite lengthy from I think it starts like it's goes over like 30 years or

so up until the 1970s or so quite a Str slightly strange uh out assemble data set but what they've done is they have basically taken this they have done um found uh uh through optimization and and and and back testing the optimal rules uh for Trend f and what they can then show is that they're essentially uh the same as the weights uh uh from your auto regression And that's really interesting so so what this basically says is if we if you look at uh the system in terms of the auto regression we find that

that they are coinciding with these uh transforming rules quite well and that's great because what this says is that by analyzing um by analyzing uh the these these uh historical data we don't have to really uh guess anymore or do like massive um um parameter sweeps or so to find Optimal rules we can actually Use some theoretical considerations and from those determine the optimal Trend following rules quite easily now um and when you do this uh uh it's it's pretty obvious that one could argue that well are they actually optimal going forward and you know

there's no there's no reason uh to assume that they are because just what you know what worked in the past doesn't really uh doesn't necessarily have to work in the future and so so what they Do is in the paper they actually show well when you do this uh they do actually also work quite well out of sample and the out of sample period is quite long it's I think it's over 20 years or so I need to actually check up on that but when you go through the paper uh towards the end they show

well actually um these rules really keep holding uh for a very very long period going forward and I think this is really the important part of this understanding Of the paper is that those rules are not just uh uh flukes that that are uh you know somewhat plucked out of thin air but but they're actually really uh fundamental uh to the way markets operate and I I think this is this is really quite fascinating so so what they've actually also done is here when they do their optimization of these uh of these rules they optimize

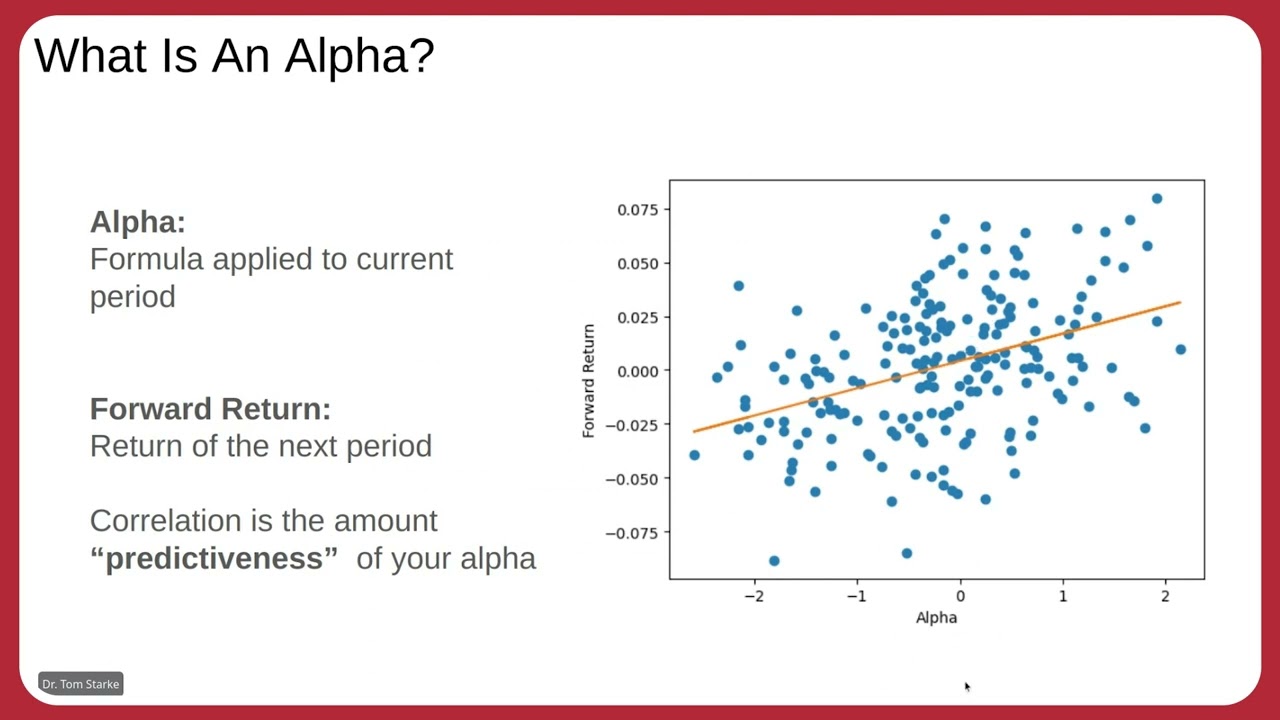

it for two different um for two different uh um metrics one is the sharp Ratio or the Risk adjusted return and the capm alpha so so capm Capital asset pricing model and the alpha basically it's it's a regression where you say well the the the slope of this pricing model is the uh regression line between your benchmark and the actual uh trading strategy and so so the slope is the beta it's basically the correlation between the Benchmark and the trading and the alpha is what you call the idiosyncratic return and it's the uh the return

that Can't be explained simply uh by uh the underlying Benchmark uh performance and so you you know there's different different philosophies on uh what you should optimize and and what's the best but they're probably the most um um common ones so of course I was quite interested in this and I have done my own um somewhat uh smaller and and and and crude because because I'm a busy guy I haven't got much time so so all I did is I used the ideas from the paper and I built my own models and um I basically

wanted to see whether it actually holds up for what I'm doing in my case as well and so uh in this case I just I took about 30 different Futures contracts I used the rules as they were described in the paper I did some optimizations and then I applied this uh in a sort of walk forward way out of sample and what you can see here is I actually get a pretty decent sharp ratio Of 1.1 now some of you may say well you know 1.1 that's not you know that's not a straight line from

the bottom left to the top right but actually um this this is compared to most CDA CTA performances like commodity trading advisor is a shop ratio of 1.1 is actually fairly decent and this is considering that I have really not done any uh optimization or anything here I I literally just got curious about it and I thought oh you know can I replicate This and uh uh getting a shop ratio of 1.1 is pretty good and um one of the things you see here is that the strategy has actually a what you call a long

volatility Behavior so you can see for example at 2008 it does really well and you can also see here in 2020 it does a small blip but then it really uh it really goes positive and this is what you call a a long volatility so so it does really well in strong uh volatility regimes so So as as you can see here initially it it's not so good but then as soon as it picks up on on where it's going and and and picks up on the volatility is actually doing really really well in both

cases here 2008 uh as well as 2020 and you can see it it gets quite flat after that but it can also see that it looks like it might wants to go back up again uh but of course I can't really tell you because I haven't got the data I can't look into the future anyway I Think it's quite interesting and and what I can see is that um I actually use the optimal EMA rule so they have also an optimal MCD rule which they reckon is actually even better than the EMA rule so I

haven't had time to uh do the macd so I just tested this and it worked quite well I would assume if you use macd you probably get even um a slightly better performance um but I don't know yet I can't tell anyway I think I think it's very interesting I think that that Um um the strategy even as it is is definitely not so bad what's also good about the strategy is it's got a fairly low turnover it's pretty robust against um um transaction costs and the other thing is you can also um um use

it on pretty high volumes so you can you know you can definitely use it with hundreds of Millions of dollars of of trading volume so so if you are in a in a larger fund then probably quite an interesting strategy but yeah I mean I'm sure that Could be even improved quite a bit more which which I haven't done um so that ends the uh explanatory part uh uh of the paper now I do have some comments uh by Julia uh which sent them and and I wanted to discuss them but maybe before I do

that um um I wonder if there's any questions uh from any of you uh which uh you know which you would like to have answered can you see me yeah okay um so so are there any are there any questions Uh from your side anything that you want to know if if not I'll I'll just start with Julia's uh Julia's comments and then maybe while while I discuss them uh there might be some of you who uh want to know some something more so comments by you make for sorry go ahead yeah I I was

gonna ask what types of op optimizations would you make for the uh the Futures Trading Algorithm um I know like seasonality is something that can be involved and um you know maybe you could have llm do uh market research and you know correlate news and and that sort of thing so yeah so there is obviously many many many many things that that you can do and like you could use yeah llms I'm I haven't actually used llms for those sort of purposes uh myself but uh it starts basically even much much more straightforward with some

type of Portfolio optimiz ation so um um there there's multiple levels of that and probably the simplest thing you could do is first of all align all your underlying um align all your underlying um um Futures contracts and uh uh you know scale them by by the volatility so you have an equal volatility of your underlying contracts as you apply the strategy and that often um helps a lot uh with getting better strategy performance it's actually I have done None of that here so the first thing I would do is actually get a what you

call a risk parity or you know like like volatility alignment and the other thing that you can then also do is um another volatility alignment uh as as you see the performance of the strategy so so you can actually then uh correct your volatility going forward as You observe the strategy performance because that often actually generates a different type of Volatility now the next step from that is say for example a mean variance optimization uh which probably uh could make things a little bit better uh but there are there's also very well known problems with

that um the next step is uh maybe using neural networks uh to do portfolio optimization so that's something I've been working on I've even got a little course out on on using uh neural networks for portfolio optimization basically using the sharp Ratio as your uh loss function and so on so so there's many many ways you can do this there's also uh things where you could say well in certain regimes um I'm staying completely out of the market uh you know this could be for example also driven by Mark of models where you can say

well these are not really suited uh for my trading style so so I'm not actually trading there at all I'm just staying out of the market um does that answer Your question a little bit or is there anything more you would like to know that's great I think uh the there is quite a bit out there just there is yes yes yeah you know I'm I'm I mean this is my this is my job uh Futures Trading and and developing strategy so there's a lot to talk about I could talk about this for days and

completely geek out but of course we haven't got the time for that um all right any any more questions for Now anyone else um if not I might just jump over to Julia's comments she actually left some really interesting ones so um the first uh she makes four points so the first points she says it seems that the indicator is based on returns estimated by Arma and Arma is an auto regressive moving average uh uh model so it's basically the auto regressive model I've been talking about despite the challenge predicting returns in general so so

one Thing one thing she says is that that um you know what she basically says is that armor models are not really suitable for predicting returns and she's very right because armor models are not are not these days used anymore for actually uh doing any return prediction however um the armor model in in the case of the paper is actually not used uh for return prediction it's actually used uh just to find the optimal weighting parameters of Your model so that's quite a different uh type of approach so she's definitely right in in in the

uh way that that that Arma is not good for return prediction but to actually wait your trading or wait your your trading indicators uh in in this way to find the optimal then then the armor model in my opinion is definitely a lot more robust uh so unfortunately I can't ask Julia for her comments I wish I could and and say stuff back to me but but I hope Maybe we can have a discussion later somewhat and she can see what we're doing here all right so the second comment he says according to the literature

momentum performance is strongly impacted by Bare markets during which interval uh intervals momentum breaks Standard Time series momentum hence mitigates this with volatility scaling note uh one this uh component is missing in the paper's description of the standard momentum Strategy and two predicting volatility is considered more optimistic then returns all right so I already talked about this and I said oh yeah volatility scaling you know that the stuff I just explained is is a very standard uh practice and that you do this now the paper doesn't discuss this because I think it's actually not really

relevant in this case uh it it would add even more complexity to the paper which is already fairly complex and volatility Scaling is really really more related to improving the performance on the portfolio level um so so that wasn't really the point of the paper in my opinion so so I would say well well you know you could not leave this out so so I think it's a good point but but the paper isn't really discussing this is um and then she says on her second Point predicting volatility is considered more optimistic than returns now

again we're we're not really uh pred predicting Returns here um it's true volatility is generally easier to predict than returns why is that because volatility has a much strong mean reverting property and so generally uh there is an easier prediction but what she refers to is that an Arma you know she she basically uh alludes to using the armor model to predict the returns which is actually not what's happening in the paper and so for predicting volatility there is a similar model called the gar model G Model which is called generalized Auto regressive heteroskedasticity complicated

um and so so uh she assumes said that we used the armor to predict and and then we used the garge model to predict volatility but I I think I think this is not really uh in some sense the point of the paper so I would say well the good points but but um the paper hasn't really doesn't discuss this so much now her third point is the paper however looks to use common Weights for the bull and bare markets then it would be interesting to see their prediction of the bull bear switch now um

I'm not really sure what she means with it um um I don't think they really talk about bull bear markets they just talk about General uh using uh General weights for um for you know the market regimes and why you would use uh those weights and basically the point is that that when You actually use what they call an optimal switching mechanism with a semi Mark of model which is similar to the macd model then uh that actually addresses the idea that you have these these Bull and be regimes U more strongly so um I'm

not fully understanding this point but I would say that that um I don't think they're really looking at the switch from bull bear I quite frankly I don't think in my humble Opinion it's actually very easy to to make these predictions in any case and you've seen that um and for example if you use Mark of models they don't necessarily predict uh uh whether it's a bull or bare Market but they might actually tell you oh it's a regular Market or an irregular Market rather than a bull bear so the bull bull bear assumption is

is a very uh is a very simple one and I think in many cases if you want to have successful Trading strategies you need to be a little bit more nuanced uh than just actually separating the market in Bull bear I mean of course this mostly applies to to my own personal experience and to to fully systematic trading however if you are more of a discretionary Trader then that that's a very different story so I'm I'm I just want to say here as a carat that's not what I'm uh what I'm talking about and then

uh finally uh the choice of Insample uh n 1875 to 1974 and out of sample 1975 to 2020 intervals looks a bit odd as a result they not only ignore the impact of Economic and technological changes but it also seems this uh provocatively imply zero impact from economic research on practical applications um good point um I think also that the choice of their in Sample out of sample intervals is a bit odd um however I think what I tried to show in the paper is that even if you choose This very odd uh intervals it

still uh seems to produce reasonable reasonably good results so they actually use a 45e a sample period and uh um I think their point was to show Even if you use something like this uh you can still you you can still actually make an inference about uh or can make make some predictions about the market going forward and I guess uh what I tried to say is that despite all the technological Changes and the impact of the new economies you could still argue that the market hasn't fundamentally changed in a big way if you zoom

out quite a lot and you look at it on a very much on a very large scale so I think it's a really good point uh she makes and I'm not here to defend the paper in any way I'm not saying oh the paper is like right or wrong but I would say uh their point of actually choosing these dates was actually to to make a point to say well Uh look look despite despite all these changes uh we can still uh end up with a quite robust strategy that that holds up for 45 years

and so what I've done in in in my test was actually uh use um a walk forward uh optimization in Sample out of sample uh so it's a bit different uh but it just works very much in a similar way so that was basically um that was basically the comments so I'm wondering If there's any other comments or even if you have some questions that may not be perfectly related uh feel free to ask them um and if not uh then we're um ending the session here uh thanks for your attention thanks for your question

oh there is one Dennis go for it oh Dennis oh Dennis and Rich I think he was just waving um yes thank you oh okay okay no problem Tom I I have a question with uh with how you might Obviously the okay this paper's been designed around equities Trends um and you know an optimal you know 10mon periods and uh you know looking looking at Bull bear in that sense you've applied it to to Futures markets Commodities markets um how how have you found the bull bear differentiation there in terms of uh periods and uh

um you know percentage in in in each and and length of bull bear in in the Futures especially Commodities Area um versus versus the ones described in the paper um yes it's interesting like I find that that actually making uh you know I mean I mean on on on a global scale making the the the case for a bull bear Market Per Se is probably a bit simplistic and I find that actually having having a bit more Nuance in that is quite useful now they're basically talking about a two-state regime and what they're not saying

is that this is actually a bull bear regime or or they Don't even say it's a mean reverting trending regime all they say is we separate uh the market into two regimes um so what these so so the in you know people implicitly assume that that when you have two regimes there should be bull bear regimes but it could actually be that um it's a a regular and an irregular regime so you know you have a market that trades in a regular fashion and then you have a market that is just like in a correction

phase or something Like this and quite frankly I think this is a much more uh a useful assumption in my opinion than than saying bull market and bare Market because when you're um when you're fully when you're trading fully systematically a lot of the the trading strategies that you have are not necessarily centered around that the other thing is that when you look at equities you know equities usually they Have you know equities on average tend to go up because companies generally add value uh to society whereas a lot of the Futures Trading is more

of a zero sum game so so for example Commodities are not uh value generating assets you know that they are what they are and and and currencies definitely are not generating any value um so so a lot apart from equities most of the other uh uh things are zero some games and and so when you trade Futures um making this disting between Bull and bare markets is also a bit tricky because of of the fact that that in many cases they are trading in a quite a different way for to equities now you can really

see that that that equities have this this behavior that that that sort of value adding uh uh Behavior you know you could just look at the S&P 500 you know it's usually going up and then it's got these times where there's phases of Correction and then it goes up and if you look over the 100 years it's pretty obvious um yeah now Futures really don't have that so so you have to actually really look at this through a different lens it's it's important absolutely I mean equities markets in in themselves if you look at an

index uh you know that it's already a momentum system it is a momentum system yes you know the S&P 500 is a survivorship bias of the top 500 at that time and and anything that doesn't Qualify drops out and and it's gone same with you know total market returns um we obviously you you know when when a company deal this for for whatever reason it's it's gone um and yeah uh if it's no longer tradable via normal means we don't have to consider its its eventual demise whereas the Futures Market well you you don't have

that you so I think um I think we you know look at equities you need to always consider It's you know equities indices and total market returns you know they they are already you know full of survivorship bias so we we need to view them with that sort of skew um I the the other thing of course is we have a continuing amount of uh retirement funds are being poured into into the equities market so so you know it's being invested somewhere and uh you know so you you've got the printing press of of of

Retirement funds just just propping the market the whole time so whereas Futures well no not yeah we we consume them consume the quality so not to forget the printing press of the FED quite a quite a printing press and and and I I ful agree it's it's it it actually seems like really simple to trade equities but actually there's a lot of um like when you come at from a systematic standpoint there's a lot of Things it's actually a lot more complex than than most people think even though it seems easy and and you're also

right the specifically the S&P 500 is pretty much a momentum strategy whereas the Russell is I think the Russell is is equally weighted and then that that works quite in a different way right it's it's it's no it's not actually it's it's it's Free Flow Free flow to market cap weighted so oh it's market cap weighted as well yeah yeah but it's only Rebalanced um every every year so so it's it's a I guess a longer term um momentum system so so you can get quite dramatic movements in a year so yes it's it's interesting

actually when I often look at the at the S&P equally weighted index versus the S&P uh market cap weight the S&P 500 and that is it's actually just looking at that there's some fascinating insights to gain just just from from looking at behaviors like this so So the Magnificent Seven yeah yeah yeah at the moment it's pretty uh uh uh interesting but also I mean I mean uh Futures are uh fascinating all the the behavior of different Futures is is quite fascinating too when you when you go into the details and and the differences between

the different underlying asset classes in Futures let just say Metals oil or or energy uh currencies and so on um or even uh Equity Indices you you can see that that there are some very specific Market specific behaviors which can in some cases be exploited specifically now what's interesting in the back test I've shown you is that that I just did this whole thing across the board and um you know I I really didn't put any fancy um um fancy anything in there and surprisingly it it did um it did quite well uh for for

what for you know when when I normally set up stuff like This wouldn't expect uh to have an outcome like this just just on the on the first setup so that that prompted me to say well actually there's really something in the in this paper like it's it's quite it's quite interesting and as I said I haven't done much work on that I just looked at it and like oh okay that that's better than I expected so that was the uh the fascinating uh part of this and and when you talk to a lot of

People in the GTA world for example like their trading strategies are often so quote unquote stupidly simple it's it's like you think well they're all like these automated Traders they should be like really sophisticated and use a lot of machine learning in reality most of them actually use very very simple trading strategies so that's also something that that shouldn't be forgotten you know that that a lot of the professionals they're not Necessarily going for the really complex machine learning systems but for the actual simplistic systems because they often have proven to be really really robust

over long time scales and also the other thing that I want to mention is what I said that specifically this strategy has this long volatility Behavior so what that means is it's it's actually providing a really good hedge for for example uh if you have another Equity strategy running you know if you Run just the S&P 500 and you look at this it actually provides a really good hedge uh uh for correction phases in equities as well because it's got this long volatility Edge to it so I think this is also something that's quite interesting

and noteworthy in this type of strategy so I'm not here to defend this paper I just wanted to present it to show that it's very interesting uh um and you know that that's my main Objective here awesome um anything else anyone well if not then uh thank you so much uh for listening in uh I hope you enjoyed it and I hope to uh see you again sometime soon thanks everyone you thank you that was