So, let me paint a picture for you. 5 years ago, you were making $42,000 a year. You were living in a small apartment, driving a used Honda Civic, and you remember thinking to yourself, "If I could just make $70,000, I'd be set.

I'd finally feel comfortable. I could breathe. " Fast forward to today.

You got the promotions. You worked the overtime. You landed the better job.

You're now making $78,000 a year, which is almost double what you used to make. You upgraded to a nicer apartment. You got a newer car.

You go out to dinner more often. And yet, here you are watching a YouTube video about why you're not happy with your money, feeling the exact same financial stress you felt when you were making 42,000. Actually, if you're being honest with yourself, you might even feel more stressed now than you did back then.

And the craziest part, you're already thinking, "If I could just hit a h 100,000, then I'd finally feel comfortable. " Sound familiar? Yeah, I thought so.

My name is Bobby, and I spend way too much time thinking about why more money never seems to be enough. If you're someone who keeps hitting income milestones only to find yourself back at square one emotionally, or if you've ever wondered why you don't feel as financially successful as your bank account says you should. Make sure to hit that subscribe button and give this video a thumbs up if this helps you out.

Here's the thing. What you're experiencing isn't a personal failure. It's not that you're bad with money.

It's not that you're ungrateful. And it's definitely not that you need to just work harder and make even more money. What you're experiencing is one of the most welldocumented psychological phenomena in human history.

And it has a name, the hedonic treadmill. And once you understand how this invisible machine works, you'll finally understand why you've been running as fast as you can toward happiness without ever actually getting there. More importantly, you'll learn how to step off.

The hydonic treadmill, sometimes called hideonic adaptation, is a concept that psychologists have been studying since the 1970s when researchers Philip Brickman and Donald Campbell first coined the term. The basic idea is devastatingly simple. Humans have a remarkable ability to adapt to both positive and negative changes in their circumstances, eventually returning to a relatively stable baseline level of happiness.

You win the lottery, you'll be thrilled for a while, then return to baseline. You get paralyzed in an accident, you'll be devastated for a while, then return to something surprisingly close to that same baseline. This isn't speculation.

This is backed by decades of research. A famous 1978 study published in the Journal of Personality and Social Psychology found that lottery winners were not significantly happier than control groups just one year after winning. And in some cases, they derived less pleasure from everyday activities than they did before winning.

Think about that for a second. People who won life-changing amounts of money ended up enjoying simple pleasures less than people who never won anything. That's not a poverty problem.

That's a brain problem. And here's what most people don't realize. Your brain is running this same program on every single raise, every promotion, every financial upgrade you've ever achieved.

The adaptation period varies, but research suggests that for most positive financial changes, you're looking at somewhere between 3 to 6 months before your brain recalibrates and that new income level feels completely normal. That $60,000 salary that felt incredible in January, by July, it's just your salary. The car that made you feel successful when you drove it off the lot.

Give it eight months and it's just your car. Your brain isn't designed to stay impressed. It's designed to adapt and seek more.

Look, I need to share some numbers with you because this is where it gets really interesting and also kind of disturbing. A 2010 study by Daniel Conaman and Angus Deon from Princeton University analyzed over 450,000 responses and found that emotional well-being rises with income, but only to about $75,000 per year. After that threshold, making more money had no measurable impact on day-to-day happiness.

Now, you might be thinking, Bobby, that study is old. 75,000 doesn't go as far as it used to. And you're right.

adjusted for inflation, that number today is somewhere around 95 to $100,000. But here's the thing. A more recent 2021 study by Matthew Killingsworth at Wharton found that happiness does continue to rise with income past that threshold, but at a significantly diminished rate.

What does that mean in practical terms? Let's do the math. If moving from 50,000 to 100,000 brings you, say 20 units of increased happiness, moving from a 100,000 to 200,000 might only bring you five or six additional units.

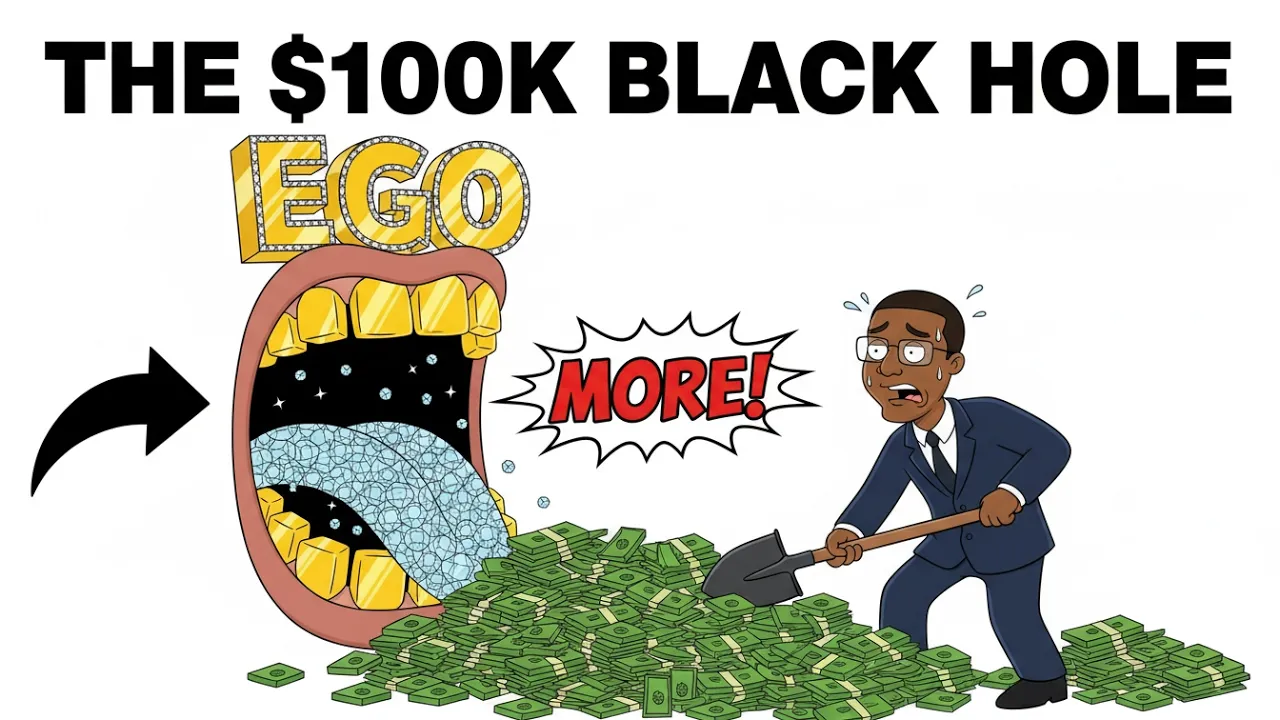

You doubled your income, more than doubled your stress, probably doubled your working hours, and you got a quarter of the emotional return. This is diminishing marginal utility applied to your entire life. And yet, nobody talks about this when they're telling you to hustle harder and stack that paper.

The financial advice industrial complex has a vested interest in keeping you on that treadmill running faster and faster. Because if you ever stopped and realized that the destination doesn't exist, you might stop consuming their content, too. Now, let me show you how this plays out in real dollars and cents.

Because abstract psychology is one thing, but watching your actual money evaluate is another. Let's say you're 30 years old, making $60,000. After taxes in an average state, you're taking home maybe $47,000, which is about $3,900 a month.

Your essential expenses, we're talking rent, utilities, basic food, transportation, insurance, come out to around $2,400. That leaves you with $1,500 of discretionary income. You feel a little tight, but you're making it work.

You get a promotion. Now you're making $80,000. After taxes, you're taking home roughly $62,000, about $5,200 a month.

But here's what happens. You move to a nicer apartment because you deserve it, adding $500 to your rent. You upgrade your car because the monthly payment is only $150 more.

You start eating out more frequently because you're busy and successful, adding maybe 300 to your food budget. You subscribe to a few more services, buy nicer clothes for work, maybe pick up a gym membership you barely use. Suddenly, your essential and quasi essential expenses have ballooned to $3,800.

Your discretionary income, $1,400. That's actually less than before your raise. You made $20,000 more per year, and you somehow have less breathing room.

This is lifestyle inflation and it is the physical manifestation of the hydonic treadmill in your bank account. Now, here's the part that really gets me. According to a 2023 report from Bank of America, 52% of Americans making between 100,000 and $150,000 per year describe themselves as living paycheck to paycheck.

Read that again. People making over a h 100red grand, which puts them in roughly the top 20% of household incomes, are financially stressed on a monthly basis. And before you say, well, that's in high cost of living areas, the data controls for that.

This is happening everywhere. A 2022 survey from PYMTS found that 36% of people making over 200,000 also identify as paycheck to paycheck. At a certain point, you have to stop blaming the economy and start looking at the psychology.

These aren't people who can't afford their lives. These are people whose lives have expanded to consume whatever resources are available. They're running on the treadmill at maximum speed, convinced that they're almost there, just a few more raises away from peace.

But the treadmill doesn't have a finish line. That's the whole point. Now, you might be thinking, "Okay, Bobby, I get it.

The treadmill is bad. But am I just supposed to never want more, never improve my life, live like a monk? No.

And this is where the conversation gets nuanced in a way that most financial content completely misses. The goal isn't to eliminate desire. The goal is to want things intentionally rather than automatically.

There's a massive difference between upgrading your home because you genuinely value space, privacy, and hosting friends versus upgrading your home because that's just what people do when they make more money. The first is conscious spending aligned with your values. The second is unconscious adaptation to external expectations.

The hydonic treadmill runs on autopilot. It runs on the assumption that more is better, that upgrades equal happiness, that your current self will be satisfied by the thing your past self was chasing. But that's a lie.

Your current self has already adapted to what you have. It wants the next thing now, and your future self will adapt to that, too. You can't win this game by playing harder.

You can only win by changing the rules. Let me tell you about something called the experience gap. Researchers have consistently found that experiential purchases, things like travel, concerts, learning a new skill, spending time with people you love, provide more lasting happiness than material purchases.

There's a few reasons for this. First, experiences are harder to adapt to because they exist as memories rather than physical objects. You can't get used to a memory the way you get used to a couch.

Second, experiences often involve social connection, which is one of the strongest predictors of well-being. Third, experiences become part of your identity in a way that possessions don't. You are your adventures, your stories, your challenges overcome.

You are not your car or your watch or your square footage. A 2014 study published in Psychological Science found that waiting for an experience generates more happiness than waiting for a material purchase. And the positive emotions from experiences last longer after the fact.

Now, here's the financial twist. Experiences are often cheaper than the material upgrades people make instead. A weekend camping trip with friends might cost $200.

The SUV you bought, partly to justify those camping trips you rarely take, cost $40,000. A cooking class costs maybe a hundred bucks and provides genuine skill and enjoyment. The kitchen renovation you did because your kitchen wasn't nice enough cost 15,000 and you stop noticing it after 3 months.

We're systematically overspending on things that provide less happiness and underspending on things that provide more. This isn't just bad psychology, it's bad math. This is where it gets really interesting because there's another way off the treadmill that almost nobody talks about and it's counterintuitive as hell.

It's called the arrival fallacy. And understanding it changes everything. The arrival fallacy is the illusion that once you arrive at a certain destination, you'll be happy.

Once you hit six figures, once you pay off the house, once you hit a million in net worth, once you can retire. The fallacy isn't that those things don't matter or won't improve your life. The fallacy is that happiness exists at the destination rather than in the journey.

Here's what the research actually shows. People are happiest when they're making progress toward meaningful goals, not when they've achieved them. The anticipation of a vacation provides more happiness than the vacation itself.

The process of building a business provides more satisfaction than cashing out. Training for a marathon is more fulfilling than finishing it. This means that if you're postponing your happiness, waiting until you arrive financially to feel good about your life, you're making a catastrophic error.

You're sacrificing the journey, which is where happiness actually lives, for an arrival that will feel hollow when you get there. I've talked to people who spent 20 years grinding toward financial independence, hit their number, and immediately felt lost. They adapted.

The goal that sustained them was gone. The happiness they expected didn't materialize, and they realized too late that they traded their 30s and 40s for a promise their brain was never going to keep. So, what do you actually do with this information?

How do you step off the treadmill without giving up on financial success? Let me give you something practical. The first step is to create what I call a lifestyle anchor.

This is a commitment you make to yourself about how much of your future raises you'll allow to flow into lifestyle upgrades versus investments. For most people, I recommend somewhere between a 7030 to 50/50 split with a higher percentage going toward investing. So, if you get a $10,000 raise, $3,000 can flow into lifestyle improvements and $7,000 goes straight into investments.

This serves two purposes. First, it prevents the automatic lifestyle inflation that keeps you on the treadmill. Second, the lifestyle improvements you do make feel more intentional and therefore more satisfying because you're choosing them consciously rather than drifting into them.

The key is to set this rule when you're thinking clearly, not in the moment when you're excited about a raise and already mentally spending it. The second step is to practice negative visualization, which sounds depressing, but is actually liberating. Stoic philosophers have been doing this for 2,000 years.

The idea is to regularly imagine losing the things you currently have. Your apartment, your job, your car, your relationships. Not to make yourself miserable, but to break the adaptation that makes you take these things for granted.

Studies show that this practice actually increases gratitude and appreciation for current circumstances without requiring any external change. You don't need to make more money to feel richer. You need to stop adapting to what you already have.

Try this once a week. Take 10 minutes to vividly imagine your life if you suddenly lost your job and had to go back to whatever you were earning 5 years ago. Feel the anxiety.

Then open your eyes and realize you still have what you have. That gap between imagined loss and current reality is where gratitude lives. And gratitude is one of the only known antidotes to hedonic adaptation.

The third step is to optimize for time, not money. This is where people get it completely backwards. They sacrifice time to earn money, then use that money to buy conveniences that save small amounts of time, never realizing that the trade is deeply unfavorable.

A 2017 study in the proceedings of national sciences found that people who spent money on time-saving purchases reported greater life satisfaction than those who spent on material goods. But here's the key insight. The ultimate time-saving purchase is having enough money that you don't need to work for more.

Every dollar you invest instead of spending is a dollar that eventually works for you, buying back hours of your life. At a 4% safe withdrawal rate, every $25 you invest buys you $1 of permanent annual passive income in just one year. Do that for 10 years while your investments compound and you've bought yourself a part-time job's worth of income that you never have to work for.

You're stepping off the treadmill, not by killing your ambition, but by redirecting it. Instead of running faster to buy more stuff, you're running to buy your time back. That's a race that actually has a finish line.

Look, I want to leave you with this. The hedonic treadmill isn't evil. It's actually a survival mechanism that helped our ancestors stay motivated in a world of genuine scarcity.

The problem is that we're now running ancient software in a world of artificial abundance surrounded by advertising designed to exploit our psychological vulnerabilities. Every billboard, every commercial, every Instagram ad is trying to convince you that you're not quite there yet. That happiness is one purchase away.

And your brain with its tendency to adapt to everything good that's ever happened to you makes this message feel true even when you know intellectually that it's not. You're not broken for feeling this way. You're human.

But being human also means you have the capacity to recognize your programming and choose differently. You can decide that enough is a number, not a feeling. You can track your lifestyle creep and consciously resist it.

You can invest in experiences over things, in time over money, in progress over arrival. You can step off the treadmill not because you've given up on success, but because you've realized success was never waiting at the end of an endless run. It was in learning how to walk away from a race that was never designed to be won.

If this video helped you see your finances differently, smash that like button and subscribe for more content that actually challenges how you think about money. I'll see you in the next one.