[Music] Hello, everyone! Welcome back to the show. Thanks for tuning in.

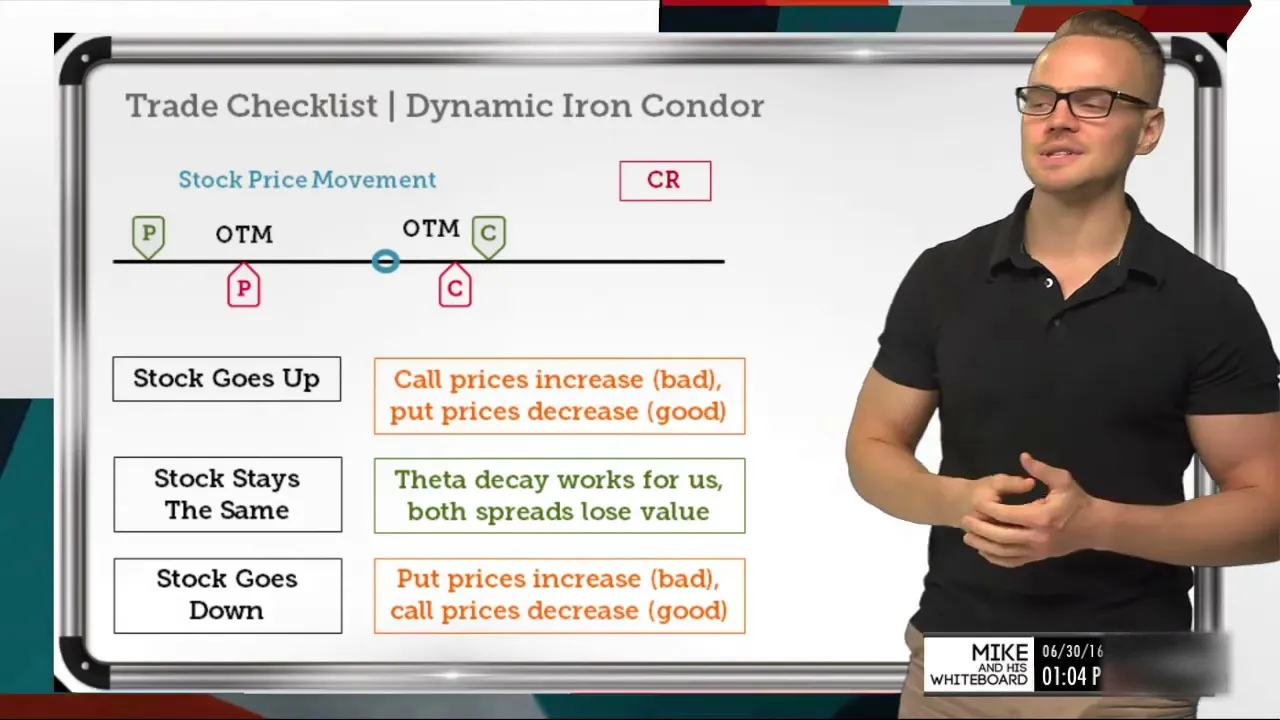

My name is Mike, and today we're going to be talking about the trade checklist for the dynamic iron condor. When we talk about a regular iron condor versus a dynamic one, with a dynamic one, we're really looking at the deltas in the strikes as opposed to making it equidistant. Especially when we have environments like this, where there's a lot of volatility happening, and specifically volatility skew, it's going to give us the ability to get truly delta neutral because we're actually placing the strikes based on the delta values of each of the strikes, as opposed to keeping it equidistant.

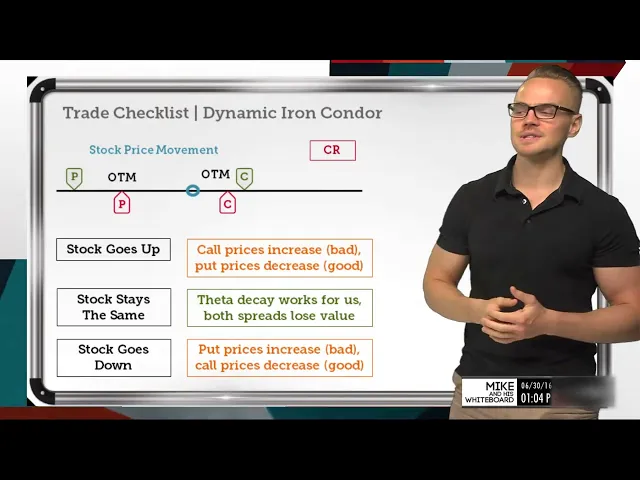

So, let's go on to the first side, and we'll talk about a quick overview of it and how we're going to think of it. As you can see, it does look a little bit different than a normal iron condor. A normal iron condor, we're going to pretty much have an equidistant side on the call side as well as the put side, and the widths of those spreads are going to be equal as well.

None of that is true for the dynamic iron condor. In fact, it ultimately ends up being pretty skewed, like you see here. But at the end of the day, we are able to still collect a credit because we're selling an out-of-the-money call spread against an out-of-the-money put spread, which gives us that ability to collect that credit, which is always going to be good for our position and our theta position overall.

But really, when we're looking at a dynamic iron condor, it's going to be a truly delta neutral strategy. It's going to be defined risk, and it's going to incorporate that volatility skew—whether it's a normal volatility skew, where the puts are trading richer than the calls, or if it's a reverse volatility skew, where the calls are trading richer than the puts. Regardless, this sort of iron condor is going to incorporate that into the strategy.

For that reason, we do have a skew neutral assumption, so we're not just looking at neutral in terms of equidistant on either side; we're actually accounting for that skew and we're really getting truly delta neutral with this strategy. The IV environment is going to still be high at best because, at the end of the day, we're selling the premium. So, we want those contracts to contract in value, which would allow us to buy back that spread at a lower price and ultimately get some profit out of this.

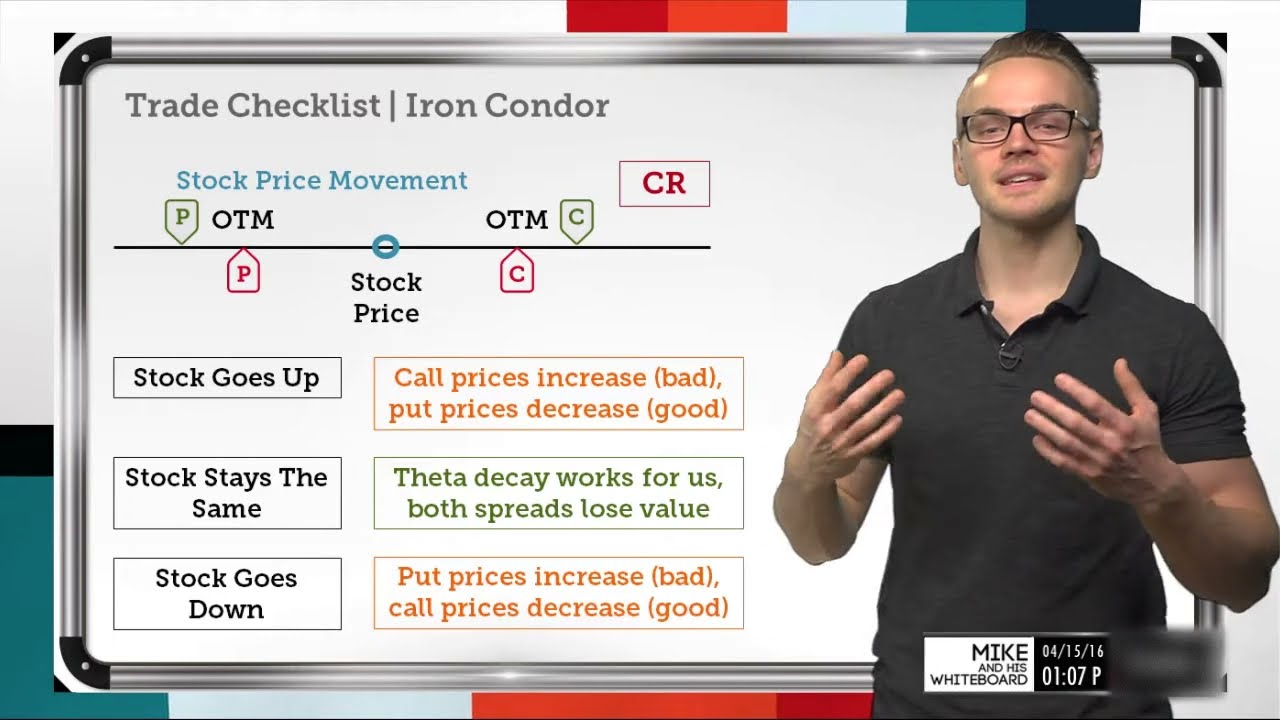

But let's talk about what will happen if the stock price goes up, stays the same, or goes down on the next slide here. So, just like the regular iron condor, it's going to be exactly the same. When the stock price goes up, our call prices are going to increase, and since we sold that call spread, that's actually going to be bad.

We want the call spread to decrease over time, but when the stock price goes up, that's not going to happen. Usually, the call prices are going to increase in value, which is going to put us at potentially seeing a loss on that side of the spread. However, we are going to see put prices decrease, which is going to be good for us overall.

So, depending on what side we've collected more on or what side we're taking more risk on, one side seeing some losses might not be the worst thing in the world, which is why I've got it highlighted in orange here. But ideally, we would want this stock price to stay pretty close to where we positioned the strategy in the first place. So, if the stock price was here when I put this on and I was completely delta neutral, I would want it to stay right around there or maybe even, if it came down just a little bit, that would be ideal because we're going to have the out-of-the-money options be pretty far out of the money over time, which is going to allow us to collect that premium and buy it back for a lower price.

So here, I've got this highlighted in green because this is the best case scenario. We're going to want the stock price to stay in between that range there and really let that theta decay work for us, which is just the daily rate of decay of all of these options. Since we sold the options closer to the stock price than the ones we purchased, we're going to have a credit that we're collecting, and for that reason, we have a positive theta effect.

Every single day that passes by where the stock price stays in this range, we should see this spread lose value over time as long as implied volatility does not increase very much or as long as the stock price doesn't drastically go towards the put side or to the call side. So, ideally, the stock staying the same is going to be the best case scenario. However, the stock could also go down, which is also going to put us in this orange area because the put prices are going to increase, which is going to be bad for the position, but our call prices should decrease.

So, if we see the stock price go down, these calls are going to be even further out of the money, which is going to reduce their value. Now, depending on whether implied volatility spikes up very high or if it stays around the same, if implied volatility spikes up, we might see a little trouble with the call side losing value. But if it stays the same, then we should see these options lose value, which is going to help offset any losses we would.

. . See, on the put side, so just like a regular iron condor, there are a few things that we want to talk about, and we're going to give tips on the next slide here.

So, the first thing we want to talk about is that breakeven calculation. The breakeven is just going to be the same as a regular iron condor; all we're doing is looking at the short call strike and the short put strike, and we're measuring the breakeven from there. Since we're collecting a credit, our breakeven is always going to be improved.

So, whatever total credit I received — let's say I received a dollar for this strategy — and let's say that this was a 75 strike call. If I received a dollar and that call strike is 75, my breakeven to the upside would be 76. All I'm doing is taking that short strike and adding the credit because that's where my breakeven is going to be improved.

Now, let's say that put strike is a 60 put strike — we collected a dollar overall — so all I would do is subtract the credit, which would improve my breakeven to the downside. All I would do is take that 60 and subtract one dollar, which gets me to 59. So, in this example, I would have a breakeven to the downside of 59 and a breakeven to the upside of 76.

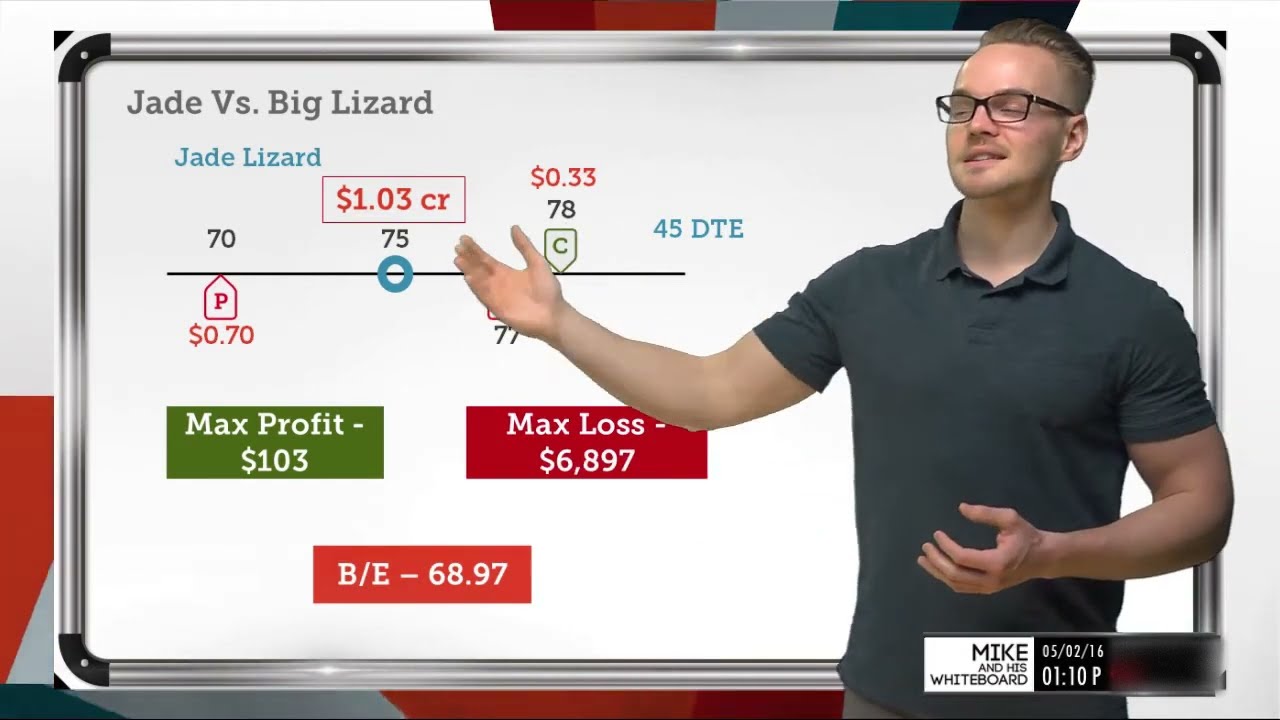

So, really, what we need to focus on when we're looking at breakevens and max losses is the fact that these strategies are not going to be equidistant. If I have an iron condor that is five points on the upside and five points wide on the downside, where if I've got a 75 strike here, that would mean I would have an 80 strike call here. On the downside, if I've got a 60 strike put, that would mean I would have a 55 strike long put.

Both of those spreads are five points wide, so the loss that I can incur is going to be equal on each side. If I'm collecting a dollar, if the stock price blows through the call side, I would lose four dollars. If the stock price blew through the downside, I would lose four dollars.

But with these strategies, we're going to have calls and puts that are usually asymmetrical. So, we're not going to have the same spread width on either side, as you can see in this image. It's really important to realize that our max loss isn't going to be equal on either side.

If this call spread is only three points wide and I've got a put spread over here that's six points wide, I have to realize that if the stock price goes down, I'm going to see much more losses on the put side than I would on the call side here. So, it's really important to realize that usually when we're deploying these strategies, the spread width is not always going to be equal. In fact, usually, when implied volatility is higher, that spread width is usually going to be more different.

A higher skew is usually going to be in place, and for that reason, we would usually see a higher implied volatility environment give us something like this. In a lower IV environment, maybe there would just be a one-strike difference, but in a high IV environment, as you can see, especially with a normal skew where there's a lot more opportunity to the downside for things to go wrong, we're going to see these options have higher probabilities on the put side because of the value there. Because of that, we're going to have to move further away and create a wider spread on that put side.

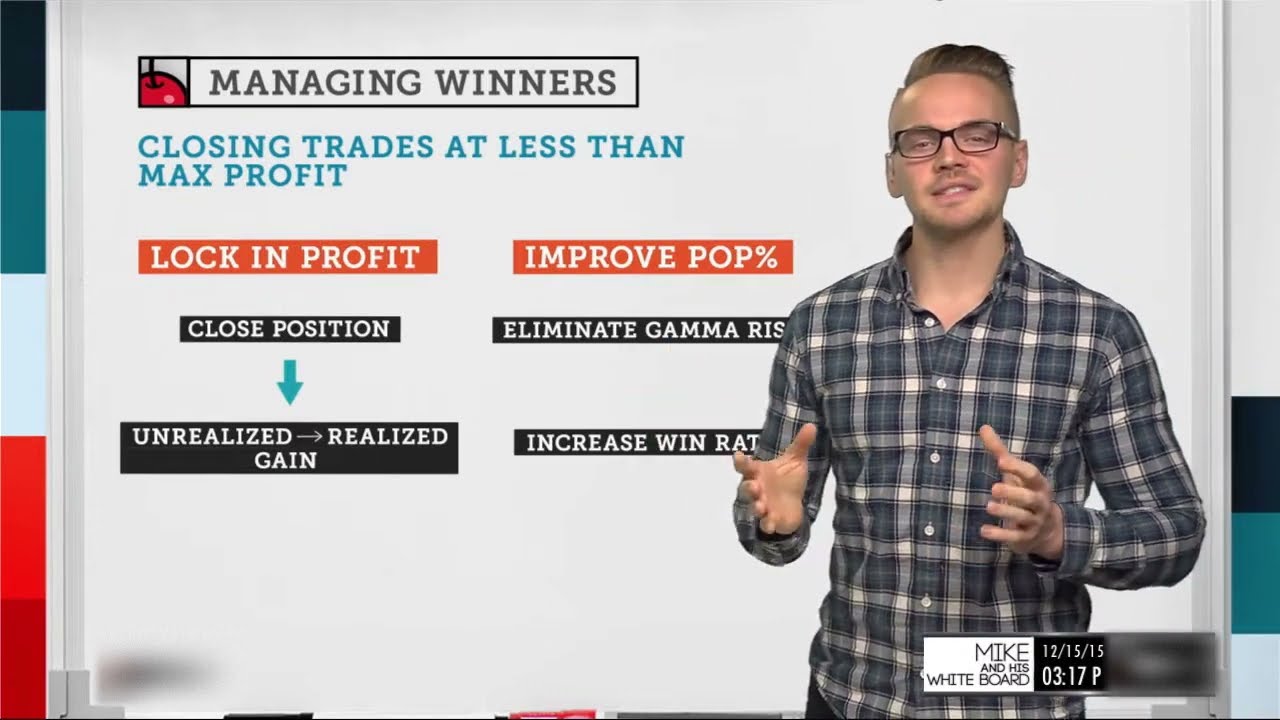

So, it's really important to remember that just like a regular iron condor, when we're talking about managing our winners, we're going to be looking at that 50% max profit. If I'm collecting a dollar on this spread, I would love to be able to close it back or buy it back for 50 cents. That would ultimately yield a 50% return on that investment that I had originally collected.

So, when we're looking at setting this up and creating this dynamic iron condor, we're not just selecting random strikes; we're actually using specific deltas for each value. So, if you remember this, then you'll be in a good spot for the future. What we like to do is create an ideal setup where we have a delta value of 10 on the long options and a delta value of 20 on those short options.

So, basically, what we're doing, instead of creating an equidistant spread, is looking at the strikes and the expiration, and we're pinpointing the deltas. We're going to the call side and we're saying, "Okay, this short call here has a 20% probability of being in the money, or it has a delta of 20. " So, I'm going to select that strike, and then we’re going to go further out and figure out what long call I can purchase that has a delta of 10.

Then, we're going to go to the put side. So, we're going to say, "Okay, I'm looking for a short put that has a delta of 20. " We find that strike and then we go even further out of the money and find the long put strike that has a delta of 10.

So, if you remember this 10-20-2010 situation for setting up these dynamic iron condors, that's really what we're looking for. When we do that, we're going to get that truly delta-neutral strategy because we're going to have a short delta here of 20. A long delta here of 20, and a long delta here of 20, and a short delta here of 20.

If you imagine this being the put side and that being the call side, as we're looking to hone in on those deltas, we're actually going to create a very delta-neutral strategy. But, as of course, delta can always change, so we might have to manage it throughout the life cycle to continue to have that delta neutrality. But let's wrap all this together with some takeaways for you.

So, the first takeaway is, again, this is a truly delta-neutral trade as opposed to a regular iron condor. When we create a dynamic iron condor, we're actually looking at those deltas. So, instead of just creating symmetry on either side, we're looking to capture that delta neutrality, and also it does account for that volatility skew.

So, when we have a symmetrical iron condor, what we'll find, especially with a high skew market, is that even if we have some symmetry on either side, we're usually going to see either a short delta or a long delta just slightly. So, if we make this a dynamic iron condor, we're actually going to be able to hone in on that zero delta value. We're still going to close the trade at 50% profit, assuming we have a high enough credit.

If I sell something for 30 cents with four legs, I might not be inclined to want to buy that back for 15 cents because I'm just racking up commissions, which is not what I want to do. So, as long as we're collecting somewhere around a dollar, that's usually the point at which we would be able to buy this back and still be able to clear commissions on this trade. And again, for that ideal setup, think about that 10-20-2010 situation and set up for the short put spread and the short call spread.

So, again, we're looking for deltas of 20 on the short options and deltas of 10 on the long options. And if you're looking for defensive tactics, you can just refer to my previous whiteboard, which was the three iron condor adjustments. Even though this is dynamic, the application is still going to be the same in terms of what we like to do when we're defensively managing these strategies.

So, check that out if you haven't seen it. Thanks so much, though! If you've got any questions or feedback, shoot me an email here, or you can follow me at Doe Trader Mike.

Stay tuned, though; we've got Jim Schultz coming up next.