hi welcome to this my fifth data update for 2025 I know I know it's we're in February already and it's taking a while but I had a few distractions along the way deep seek tariffs and in this session I want to turn the focus away from the US Centric view I brought to the first FL because I looked at US Stocks I sliced and DIC US stocks and at interest rates in the US in this session I want to talk about the rest of the world I'm a Disney fan I've been a fan for a long time I've taken my kids to Disney now I take my grandkids to Disney and I've probably gone to to Disney theme parks a hundred times in my life and I wouldn't say it's one of my favorite rides but a main stay of every Disney visit that I go to is it's a it's an iconic ride it's a ride that's in every Disney theme park in the in the Magic Kingdom portion it's called It's a Small World After All now if you've never been to Disney park and you end up going and you have kids under the age of five this is your perfect ride why it's peaceful they're not going to find any scary things it presents the world the way Disney sees it all full of peace and happiness and Goodwill I'm not sure about you but I don't live in that world so in this session I'd like to focus I I want to take you through my own version of It's a small world through the world we live in and guess what it's not full of peace and happiness and Goodwill a lot of chaos and anger and violence but we got to live in the world we're in not the world we wish we're in so let's get the process started I want to start by looking at what 2024 delivered as returns across the world so I picked a few Global indices and if I left out your favorite index don't take it personally I just could fit this much on the page across the globe and I looked at the percentage return in the index the US is the S&P 500 Argentina is a m Brazil as BPA Etc so in the last column you see the percentage change and if you look across markets you see widely Divergent numbers Argentina was out of this world 172. 5 2% return and if you go across there are markets that didn't do well Qatar was down 3. 25% Indonesia was down so it was a good year for the most part but in some parts of the world Brazil Indonesia I Qatar you actually saw markets go down now as you look at these returns there are two things to worry about when you look at index returns first these are Returns on indices what's wrong with indices while they might be widely used they reflect a subset of companies you take the Dax it's not every German stock it's the 30 largest German stocks and I'm not even sure it's the large the 30 stocks that happen to be in the Dax it's a subset of the market the second is the returns are all in local terms remember those Argentina returns are 172.

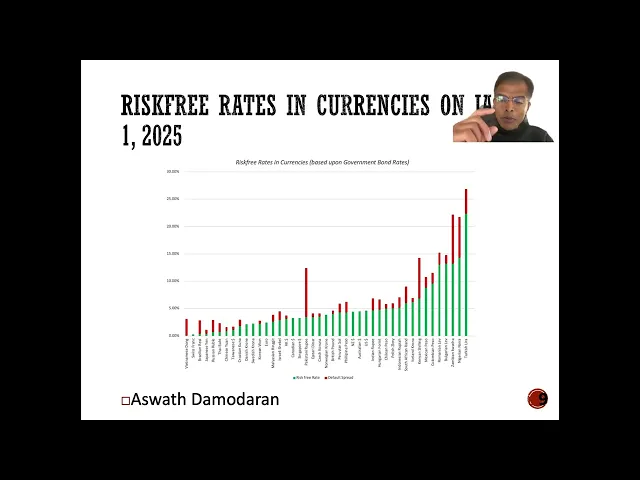

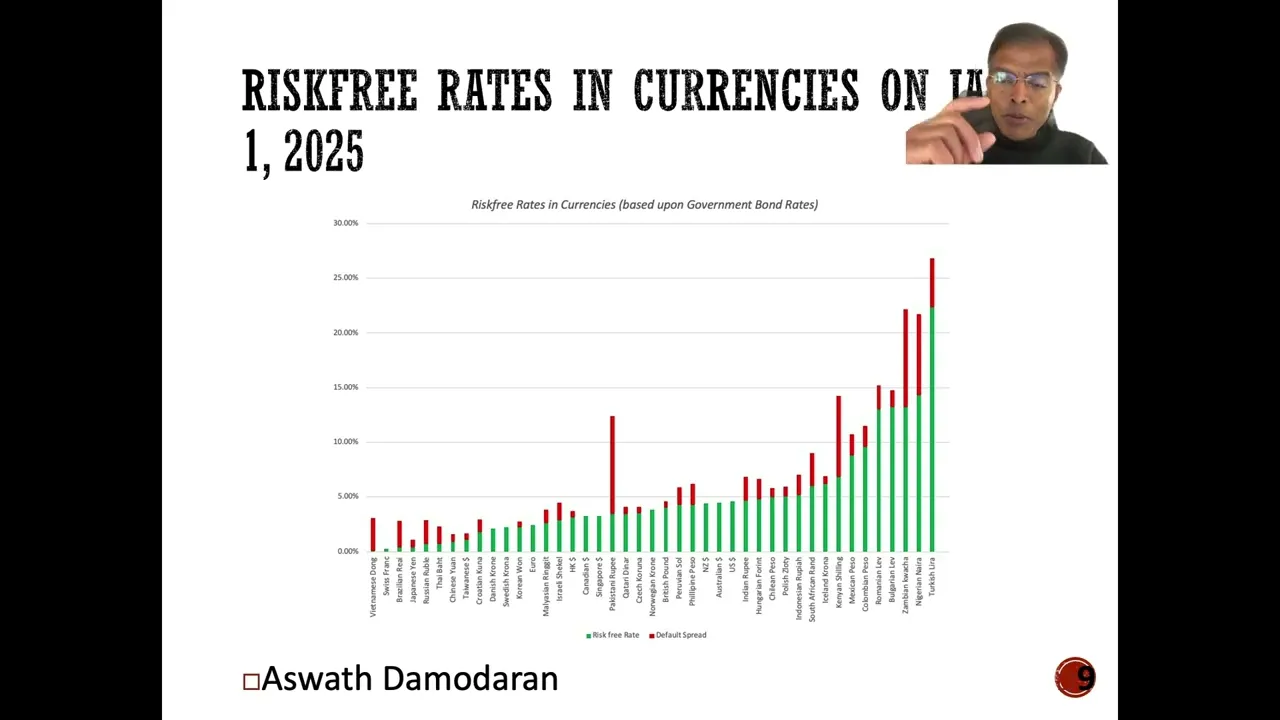

5 2% amazing impressive but it's still in nominal Pacos unless you bring inflation into the picture you cannot just look at a normal return index said that was a good return so here's what I'm going to do to get returns that are comparable across countries across region first I'm going to look at all publicly traded stocks in every market so I'm not going to pick an index I'm going to pick this is part of what I at the start of every year where I download the data in every publicly traded stock I then use market caps all converted into US dollars that way the return will be in dollars and you can compare them across markets and the way I'm going to come up with the market cap of the in each each country is I'm going to add up the market cap of every listed company in that market so if you take Poland I take every traded stock in Poland add up the market caps at the start of 2024 at the end of 202 before compute the percentage return so it's like a weighted return then because if a large company does well it's going to have a much bigger effect than if a small company does well so here's what the world looks like if you convert everything in dollar terms and I've broken down broadly into regions with a few countries thrown in the best part of the world to invest in 2024 and I think you saw this from our very first post was the United States in fact if you look at across much of the world it wasn't a great year in dollar terms you got us you got India and then everything else is single digit returns and some of negative returns for the most part 2024 was a ho home year in terms of dollar returns for much of the rest of the world outside of the US and India now actually the US outperforming its Global counterparts everybody outside the US is not something new for much of the last 15 years us stocks have outperformed investing in a global index and that's befuddled people because we were all taught that you should diversify that you should bring in foreign stocks into your portfolio that lesson got passed on the 80s and '90s we took it to heart we invested outside and for the last 15 years people invested only in US Stocks have beaten us now 15 years is not a long time in US market history so you could argue that this two shall pass but I think there's another reason why investing just in US stocks doesn't carry the consequence it did 40 years ago say you invest in US Stocks the biggest stocks are in the S&P 500 and the Very biggest of them are the MA 7 take a look at the MA 7 and look at where they get their revenues they are us companies in terms of incorporation but they get their revenues globally so maybe US Stocks you're capturing a global index and that's what you seeing here so those are the returns I did decide look at individual countries to see which were the best performing in the worst performing markets remember Argentina 172. 5 2% return in the index I cautioned you that that was before inflation well even if you factor in inflation and the exchange rate effect Argentina was the best performing Market in 2024 you got Bulgaria Kenya Pakistan Croatia I mean this is a list of countries we don't think of having invested a lot of money many of them are small markets but 2024 was a good year the worst performing Market in 2024 was Brazil down 29% in dollar terms followed by Mexico and then you got Bangladesh Egypt Etc a couple of these countries had political crisis going through so maybe that that played out that played a role so you can see the best performing and the worst performing markets so when you look at returns you look at what the what a country slm market did in 2024 now one reason the index return and the dollar return deviate is because of exchange rate effects so I decided to take a look at the US dollar in 2024 against three indices the first is an index of Emerging Market countries you're saying how do you classify them I don't I use the Federal Reserves if you don't like the classification take it up with them so the Federal Reserves data set Fred maintains these indices against emerging and developed markets and guess what the dollar was stronger against both but a little stronger against emerging markets 10. 31% than developed markets there's also a broad index against all currencies across all markets and the dollar appreciated by about 9% in 2024 now once we've opened the door to currencies might as well walk in he's saying well so what drives differences in interest rates across currencies so put differently if I'm valuing a company in Egyptian pounds or Pakistani rupees or Indonesian rupe or Brazilian R how would I come up with the risk freting so let me set up something that I think is critical if you're an investor knowing what you can make on a guaranteed investment is critical to investing sensibly a risk free rate so here are the three scenarios you might face from most from easiest to most difficult first question I'm going to ask you is does the government in the currency are interested in issue long-term bonds which are traded and if the answer is yes and there is no default risk in the country then I can use the Government Bond rate as a risk free rate so if you're interested in getting a risk free rate in Swiss ranks not a problem there's a 10e Swiss rank Government Bond rate I take that rate and that becomes my risk free rate so there's no default risk you say how would I know if there's default risk I cheat I use the Sovereign rating for a country and as you know Moody S&P Fitch all rate countries and if a country has a AAA rating I make the assumption that there's no default risk you're saying that's dangerous I agree but think of how how much work it saves just taking that shortcut so if you're looking at a currency where there is at least one entity with no default is issuing long-term bonds at currency your home free use the government bond rate same rational I use for using the German Euro bond rate is the risk-free rate in Euros he's saying what if you have a traded Government Bond in the local currency but there is at least the perception of default risk just yesterday in class our was estimating an Indian rupee risk reate there are 10e government bonds and rupees but the Indian government is not viewed as default free by any of the ratings agencies doesn't have a AAA rating and I'm talking about the local currency rating the rating that S&P and fit and Moody is attached to India when it borrows money in rupees India's rating is B3 where there is default risk here's what you need to do you need to assess what that default risk translates into a spread and take it the government bond rate because you wanted something risk fre so the Indian government bond rate is six or seven or 8% let's say it's 8% and the default spread is 2% 8 - 2 is 6% that's your risk free rate in rupees ising but what if my government does not have traded bonds remember there are 100 plus currencies where the government does not issue long-term Bonds in that currency they borrow money from a bank the World Bank you're saying what do I do that well if inflation is the reason risk free rates very across currencies and I believe it is here's what you can do start with the risk free rate in US Dollars then take the differential inflation between the local currency and the US Dollars and add that on to the risk free rate so if your T bond rate is 2% and your differential inflation is 5% 5% higher than the US your risk free rate should be 7% so started 2025 I computed risk-free rates and currencies where I could find a Government Bond as you can see it's a subset of the currencies he saying what's the red and the green the total height of each column each bar is the government bond rate the red portion is what I'm taking out for Deford risk and as you go cut across you can see that the currency with the highest risk free rate at the start of 2025 was the Turkish L at the Nigeria and nir as you walk down the list you can see currencies like the New Zealand dollar and the Australian dollar where I'm effectively taking the government bond rate because they're AAA and then you get further down you get to lower and lower risk free rates now a pause and to think about why do risk free rates very across currencies the answer is not mysterious High inflation currencies will have high risk free rates low inflation currencies will have low risk free rates and deflationary currencies could actually have negative RIS free rates so that's for governments where there is a currency out there but let's say you don't have a Government Bond a currency and saying how do I get a RIS create I'm going to use the Brazilian R to illustrate this even though there is a Government Bond in R and I can do it that way let's say I did not have it the US bond rate at the start of 20 at the start of 2025 was about 4 and a half% the expected inflation rate in the US was about 2 and a half% let's say I can estimate the expected inflation Brazil R we'll come back and talk about how best to do it and it's 7 1.

2% the shortcut and that's at the bottom of the page that I can use is take the 42% the USD bond rate take the differential inflation and have a risk-free rate in brazilan reiz there's a little that's an approximation because there's a little tweak rates inflation and real rates build on each other there a compounding effect so if you want to bring that in here's what you need to do start with 1 plus the USD bond rate 1. 04 five and multiply by 1 plus plus the inflation rate in Brazil divided by the one plus the inflation rate in the US then for remember to subtract out one what is all of these gymnastics bring you to 9. 6% now you see why you're in a hurry the approximation works you get 9.

5 so 9. 6 big deal the higher inflation G gets the more you have to worry about the approximation not working with reasonable inflation rates the approximation works so that's risk free rates in different currencies vary because of inflation a little pause you're saying you know where do you get expect inflation the US actually just look up the difference the tond rate and the dips rate it's a market given number for expect inflation that's a 2 and a half% saying what if about for Brazil I can use last year's inflation but God only knows what that number is I would like an expected inflation rate and I not a Brazil specialist I don't want to be estimating it so here's what I do I go to the IMF the World Bank web page and they have date and they have expected inflation for the next 5 or 10 years for Brazil I use it you're saying what if they're wrong it doesn't matter and here's why if you're consistent about using that inflation to come up with the risk free rate and you use the same inflation your cash flows you're going to be okay we looked at we've looked at returns we've looked at risk-free rates let's talk about risk across Curren countries at the risk of stating the obvious risk varies across countries there are risky countries and safe countries I do an entire peace on this in the middle of the year so I'm going to rush through some of the things and you can take the last country risk thing that I did in the middle of last year and look for a more detailed explanation the risk of a country is driven by political structure and it's U not a slam dunk democracies expose businesses to more continuous risk because things can change all the time as governments get elected and in and elected out of office authorita regimes often offer the the promise of predictability there's a reason companies like to be in China for much of this Century because you were offered the rules won't change for the next 40 years India can't do that but authoritarian regimes you have more discontinuous risk what's discontinuous risk think about Syria PRI Assad no Bashar Assad could have told you I can set your policy for the next 40 years as a business and he went back saying oh that's amazing I've got a promise and you wake up one day and you've had a violent overthrow and there goes the promise so political structure matters war and violence clearly plays a ro when you operate a business in a country exposed to violence War terrorism or even internal strife it's much more difficult to operate it translate to higher cost more risk that throws up in your country risk corruption is like a hidden tax it's like an extra tax paid not to the government but to the corruptor the people you pay those those those to whom those payoffs go countries in corrupt locals are riskier because that corruption is unpredictable and can vary and finally for if you're valuing a business or assessing a business legal and property rights matter you want somebody enforcing contracts so in a country where there are no a weak property rights there's more risk than when there is the those rights are enforced and it's nice to have those rights enforced in a timely way before you take issue with what I show you as numbers think about by the country you're most interested in put it through this test so as many of you know I estimate Equity risk BRS by country it's most widely downloaded data set there's no intellectual Firepower and I'm absolutely transparent about how I estimate those risk premiums remember the implied Equity risk premium I came up with for the S&P 500 the start of 2025 I think it was in data update to 4. 33% that becomes my starting point I then look at what your Sovereign rating is using Moody's S&P fit one of the ratings agencies if you're AAA rated I give you the same Equity risk premiums the US and my rationale is a very simple one if you have five mature markets with different Equity risk premiums one is 4.

33 1 is 5 1 is3 you know exactly what's going to happen right money will leave the low premium Market go to the high premium market so that rationale I'm going to give Germany Australia the Netherlands 4. 33% if your rating is not AAA my task is laid out for me I come up with a default spread either using your rating or a sovereign default spread a sovereign CDs spread and then I scale it up scale it up why because Equity Equity is riskier than a Government Bond and to get the scaling factor I look up the standard deviations and an Emerging Market Equity index maintained by S&P and an ETF of Emerging Market government bonds and that ratio is 1. 35 equities were 1.

35 times more volatile than bonds say how am I going to use it if your default spread is 2% you multiply by 1. 35 you get a 2. 7% you add that to the 4.

33% your Equity risk premium is 7. 03% I do this for every rated country so what you see on the next page is a page that if youve taken any of my classes you see at some point it's the equity risk premium by country at the start of 20125 and you can see take any part of the world Asia Latin America you can see wide variation within that region some some countries have much lower risk premiums you're saying what's the blue the red and the green the blue is your rating that's what drives the process the red is the country risk premium which is the default spread times at 1. 35 and the green is the country risk premium added on to the 4.

33% the US premium or the mature Market premium now if you're saying if you look at towards the top end there's a black box with numbers those are Frontier markets these are markets which don't have a rating Syria Sudan North Korea and for the last three years Russia since the ratings agencies have stopped rating the company there I look up a score called political risk Services it it's a estimated by political risk Services Europe based risk assessment I think it's Europe based Maybe I'm Wrong on that but they assess scores for countries and a low score suggests a high risk and a high score is a low risk so I look up the political risk scores for these countries then look for other countries with similar scores that have ratings and Equity risk premiums and I take the average I know simplistic guilty as charge but now I have an equity risk premium no matter where in the world you operate so if you're a company and you operate in four countries I can estimate an equity risk premium for you now having used this data or estimated for a long time I'm entirely aware of its weaknesses right I know right now one of the push backs I will get is why are you using the US still as a mature Market hasn't it lost lost its triaa rating it has two of three agencies I'm holding on for dear life to that Moody's rating of triaa that too could shift but let's say it does shift and becomes a doublea plus rated country next year all I have to do is get the spread for a doua rated country and subtract it from the US Equity risk PR so from the 4.