[Music] what's up everyone thanks for tuning in welcome back to the show my name is mike and today we're going to be talking about some adjustments for the poor man's covered put a few days ago we talked about three adjustments we might consider with a poor man's covered call and you're actually going to see a lot of some of the same similarities with that strategy and the adjustments we might make in this strategy but there are a few key differences mainly being the directional assumption which is opposite for the poor man's covered put and some

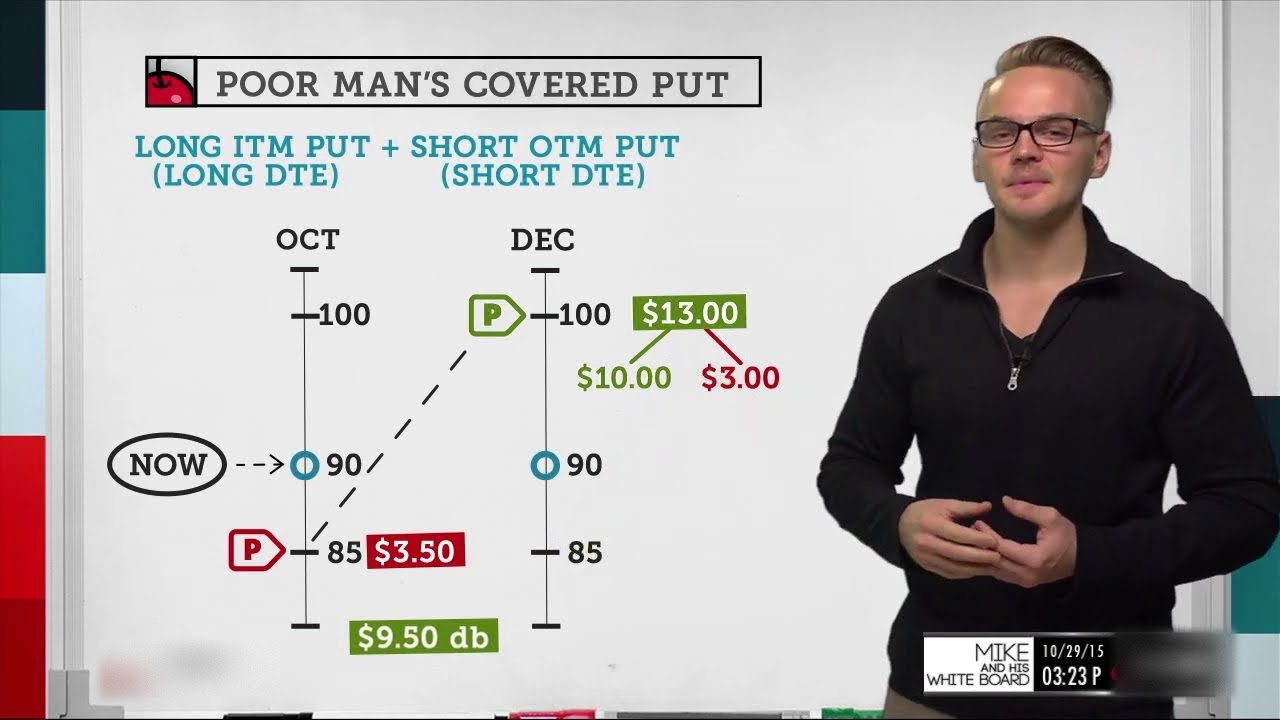

of the greeks that play into the poor man's covered put more than they would for the poor man's covered call so let's break it down in the very beginning here and we'll start off with the opening trade and we'll talk about a few things to consider when we're creating this spread so the very first thing to consider is that when we're creating a poor man's covered put it's basically a synthetic strategy that aims to replicate short stock so short 100 shares of stock while selling a put against those synthetic shares so instead of selling short

shares here we're actually looking to purchase an in the money put so when we're looking at puts in the money would be above the current stock price so we're looking to purchase an in the money put in a further out expiration than the put that we would be selling against it to reduce our cost basis so one of the main differences here that i wanted to point out is that when we're looking at this specific example we're actually jumping ahead a month so we're looking at june instead of may in the poor man's covered call

example we looked at may and april but today we're going to be looking at moving that long put a little bit further out in time and you're going to see a few differences there so the very first difference is that we're going to be paying a little bit more than the intrinsic value of our option so again just to calculate intrinsic value all we need to do is look at the in the money put and calculate the difference between our strike and where the stock is trading right now so in this scenario the the 95

long put in june has five points or five dollars or 500 of intrinsic value and that will be ringing true at expiration but we're paying 620 and we're going to be okay with this because of the fact that i know that i've got multiple months i'm pushing this way out so even if this april option expires worthless i can actually deploy another option in may and my aim or my goal for that would just be to reduce that basis a little bit further hopefully collect more than a dollar 20 on my next position in may

which would reduce my cost basis to lower then intrinsic value on that long put so just like when we're looking at the poor man's covered call we don't really know what our max profit's going to be or where our break even will be because of the fact that we're dealing with multiple expirations if we were dealing with the same expiration it would just be a standard vertical spread and we could easily calculate our max profit and break even but since we're dealing with multiple expirations specifically the long option in june it's going to have a

different implied volatility and changes in implied volatility are going to affect these options very differently so an increase in implied volatility will actually affect the june option more it'll change the price of the june option more than that of the april option and that's just because there's more time to the june option expiration and it's got a lot more vega exposure but we do know that our max loss is simply the debit paid for the strategy so if i'm paying six dollars and 20 cents in real terms that's 620 dollars and i can't lose more

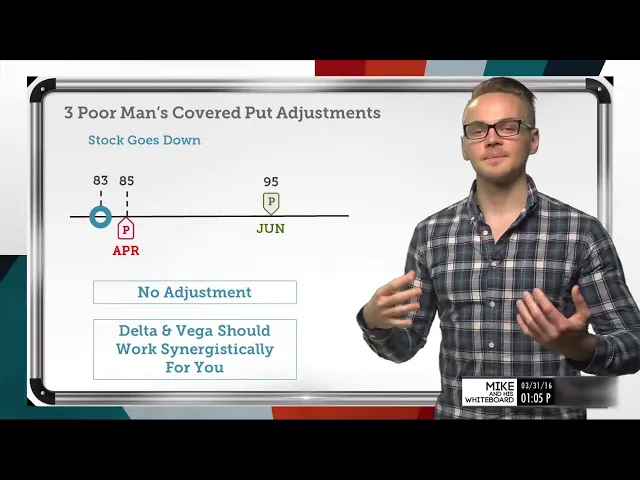

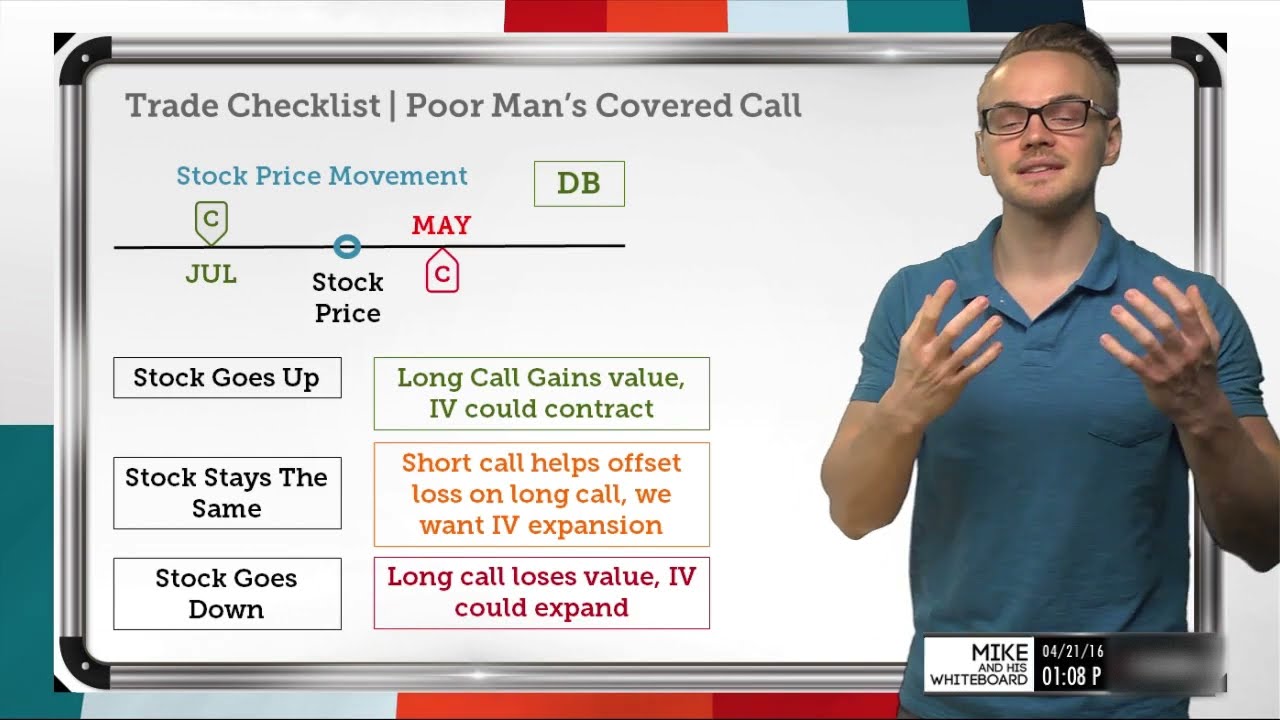

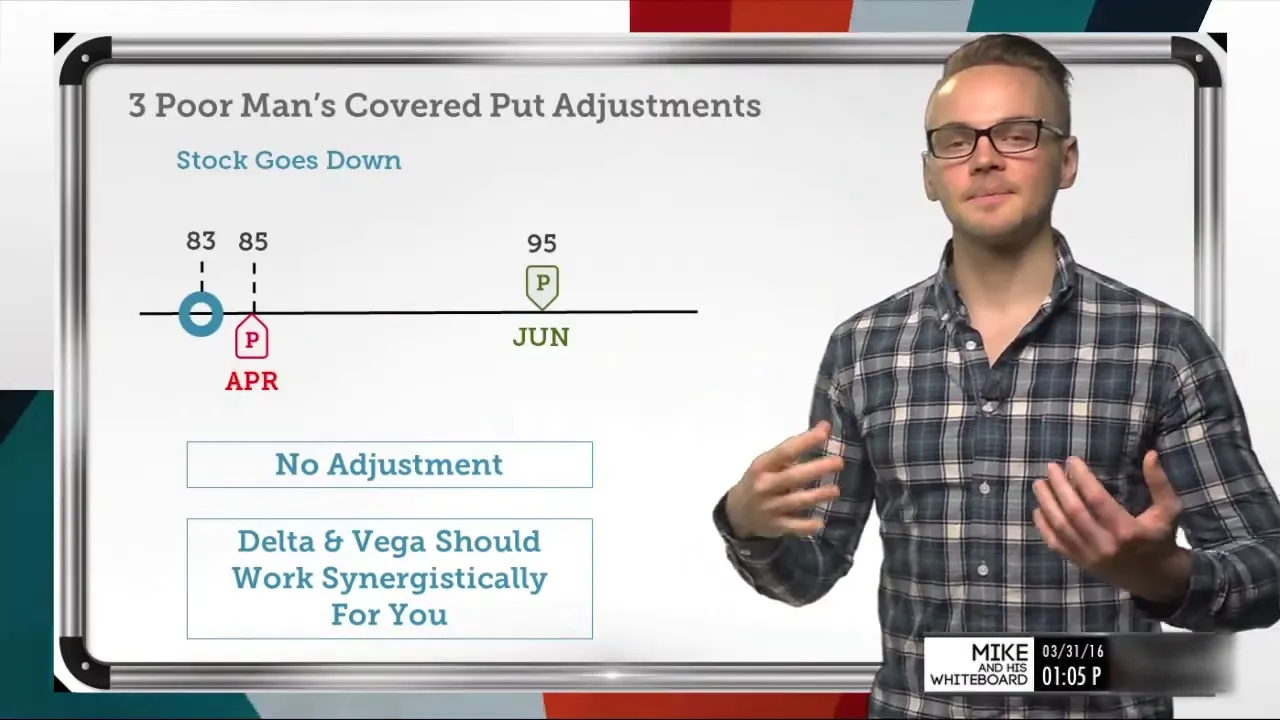

than that because i'm really just long this long put in june and i'm selling this april option against it to reduce my basis in no situation can i lose more than that max loss of 620 because of the fact that i'm really long that june option so what are some things to consider when the stock price starts to move either for or against us well let's break that down on the next slide here we'll talk about what we're looking at in terms of when the stock goes down so if the stock goes down this is

actually going to be good for us just like in a poor man's covered call scenario where the stock is going up that's exactly what we want because if we think about what we're actually doing here this is a synthetic short stock strategy and we're just selling a put against that short stock to reduce our cost basis so since we're replacing our short stock with a long put we want the stock to go down anytime we're shorting stock outright we want the stock to go down so if that happens here then we're not going to make

an adjustment in fact we'll probably end up closing this trade for a pretty sizable profit because when we're looking at a poor man's covered put specifically delta and vega are going to work synergistically for us if the stock price goes down so let's talk about that a little bit if we know that delta is the directional assumption and also the rate of change of our options price and this would definitely have a negative delta or a bearish assumption when the stock goes down that's going to be good for us my put is going to be

the put that i'm long in june is going to gain value because it's going to move further and further in the money and my short put is actually going to increase in value as well which is bad for my position but since we know that generally when a stock price goes down especially when it goes down seven points in a short period of time we would tend to see an increase in implied volatility and if we know that implied volatility is just a reflection of the options prices delta and vega is going to work synergistically

for us and again vega is just the rate of change of our options price given a one percent change of implied volatility so when we when we pair a negative delta trade like this one here with a positive vega trade which this is also then we get that accelerated profit potential so when we look at when a stock goes down when the stock goes down and especially when the stock goes down and there's an increase in implied volatility both of these greeks delta and vega are going to be working for us when this trade goes

our way so here we're not going to make any adjustments we're probably again we're probably going to be able to close this trade for a pretty nice profit our long put would be 12 points in the money and at expiration our short put would be the april expiration our short put would be worth about two dollars as it's two dollars in the money now but because of that implied volatility factor even when this april option expires we would still be long that june put so if implied volatility had increased we know that this is 12

points in the money so it's going to be trading for at least 12 dollars but probably much more if implied volatility does increase so here no adjustment this is a great scenario and we're probably going to see a very nice profit but what happens when the stock goes against us so on the next side we're going to be talking about what happens when the stock goes up which is going to be bad for our poor man's covered put situation so if the stock goes up the one thing that we can do and the one thing

that we'll consider is moving that short option just like the poor man's covered call example the short option is going to be our mobile option we don't really have a reason to move our long put option because when we're adjusting trades our key is to reduce our cost basis and the only way we can do that is to move our short put specifically up which is going to get us that extra credit hopefully and we can move it just to where that stock price was trading it's really important to remember what we paid for the

trade originally so i probably wouldn't want to move this short strike anywhere further up than let's say 90 because i know that even if the stock price has come up if i move my strike to 90 and let's say the stock turns back down and goes goes starts going my way if my short strike is now at 90 then i'm basically capping my profits to the downside at 90. if i move it too far up for example if i move it to 92 or 91 of course i'm going to be able to collect a lot

more credit but if the stock actually moves for me i have to remember that i paid six dollars and 20 cents for this trade if i move it to 92 even at this expiration of april my trade is probably going to be capped at around let's say three dollars if i close the entire trade together and i don't consider leaving that put option there in june so if i know that i open my trade for about six dollars and 20 cents and i move my short strike too far up i can put myself in a

situation where it's really hard to make money unless implied volatility has just exploded through the roof and in which case i might be able to close this trade for more than what i paid for it so the consideration here is to roll the put up and one thing to be aware of is that just like when delta and vega are working for us when this specific strategy and the stock price goes down if the stock price goes up delta and vega are going to work against us so when we're looking at the acceleration of profit

we're also looking at the acceleration of loss so if the stock price goes up and we know that when a market slowly drifts up we tend to see implied volatility decrease since i purchased this spread it's going to hurt the value of my spread overall specifically this long option in june because as we know the long option is going to be more susceptible to implied volatility changes and when the stock price is going up my put value is going to decrease because it's moving from being a pretty deep in the money option to being almost

an at the money option and the further we go down the line or the further the stock price moves up this is going to move further and further closer to at the money or even out of the money and the further out of the money we go as we know is going to reduce the price of that option so even though this situation would really work against us with delta and vega it's really important to realize that these two greeks are going to accelerate the loss and also potentially accelerate the profit when we're looking at

two different scenarios but let's look at the final example where we have a good situation it's not perfect obviously the perfect situation is when the stock price goes down but when we look at the next slide here we'll be able to see what will happen and what we can do when the stock price stays within our range so obviously we had that that poor man's covered put scenario where we had the long 95 put and the short 85 put and what we can consider doing is let's say the stock price is at 87 and it's

at april expiration so my 85 put in april has expired worthless well now i know that i still have my june option because i had a two month wide spread in terms of calendar expirations i can then go ahead and deploy another option in the next cycle so now we're at april expiration maybe i'll look to deploy the same exact strike in may and let's say that since we saw a small decrease from 90 to 87 let's assume that implied volatility has increased a little bit so instead of collecting two dollars and 30 cents like

i did in the april option i can now collect 2.50 in the may option so what this does is it continues to help me reduce my cost basis if i know that my original trade was placed for six dollars and twenty cents and i can collect another two dollars and fifty cents and if we remember our target was really just to get our cost basis down to about five dollars because that's where intrinsic value was at when we originally placed the trade if i collect two dollars and fifty cents i would be exceeding my target

by one dollar and thirty cents so now even if the stock price comes back up here and let's say i can deploy even another option in june if it stays within this range and then eventually i would create a vertical spread because if this option expires and i can sell another option in june then i would just have a long put in june with a short put in june as well it would be a typical vertical spread but i would have collected so much value by completely selling those uh out of the money puts here

so again we would have that out of the money put in may we collected money for out of the money put in april that we collected money for and then we could sell a final one in june so we can collect all this value which basically reduces my overall cost basis at which point even if the stock price was back at 90. my cost basis would be so low that i would be able to sell this put for the intrinsic value or close out that long put for intrinsic value there and even if it's back

at 90 and i can close this put for five dollars i would have collected much more than that by continually selling those puts which would bring me to a profit potential zone so really we would look to just redeploy our new short put in may and then if we stay in the same range we would do the exact same thing in june depending on where implied volatility is if it's increased maybe i can move this strike even further out of the way or if it's decreased maybe i'll have to tighten it up a little bit

to collect some extra credit but the whole key is to continue to reduce our basis so that at our june option expiration if we want to hold this trade that long we're going to be able to sell out of this long put for whatever intrinsic value it hopefully has but because of the collections we've made on these short puts we're going to be in a profit so let's wrap all this together with some takeaways the very first takeaway is that the poor man's covered put unlike the poor man's covered call we're going to see a

lot more of that delta and vega speed and we're going to see that speed and acceleration affect our profit potential if the stock moves down but also our loss potential if the stock moves up again these two takeaways are exactly the same as our poor man's covered call the key to adjusting is always going to be reducing our cost basis so if you've watched any of these other adjustment strategies i've covered some other ones such as covered calls short puts iron condors jade lizards the whole key is always to make an adjustment that reduces our

cost basis because at the end of the day we know what our cost basis is but we don't know where the stock will move so if we focus on controlling the variable that we do know which is cost basis we're going to be able to put ourselves in a key position to be successful in the long run and again especially with this strategy and the poor man's covered call the short option is the mobile one we don't really see a reason to move our long option unless our assumption has changed in which case we'll usually

just take off the trade so thanks so much for tuning in hopefully you've enjoyed this segment my name is mike if you've got any questions or feedback shoot it to these emails here or you can shoot me a tweet at doe trader mike stay tuned though we've got jim schultz coming up next hey everyone thanks for watching our video if you liked this video give it a thumbs up or share it with a friend click below to watch more videos subscribe to our channel or go to our website [Music]