Dear participant, dear delegate, dear colleagues, welcome to this webinar on the 2025 update to the model tax convention, the OECD model tax convention. My name is Jessica Di Maria. I'm a member of the tax stratey team at the OECD and I will be your master of ceremony for today's webinar.

All the plan for today is to walk you through the main change included in the 2025 update to the model tax convention and those are basically the changes made to the commentary on article 5 on permanent establishment. uh the changes made to the commentary on article 9 on transfer pricing and the changes made to article 25 in its commentary on dispute resolution. We have over 3,500 participant uh to the webinar coming from over 150 countries.

So thank you very much for being here with us and I will now invite our director Manal Corin to open the webinar. Thank you very much. Thank you very much uh Jessica and let me add my uh very warm greetings to participants uh delegates and colleagues um and uh it's wonderful to have so many people joining in for this uh for this webinar.

Uh I'm pleased to be here with you today for this uh dedicated webinar on the release of the 2025 update to the OECD model convention. a release that has been much anticipated by all stakeholders and um in which there's a lot of interest as we can see by today's uh very large participation. In a couple of minutes um my team uh who have worked very very hard to support securing this update will provide an overview of the the main changes made to the OECD model.

Uh before that however I just wanted to take a few minutes to step back and to reflect on the significance of this update. Um the update to the model which was informed by consultations and discussions with all of you, our stakeholders, reinforces the the continued importance of multilateral cooperation in tax matters and demonstrates that governments when working together can deliver greater certainty and stability in a an evolving and increasingly complex international tax environment. Tax treaties are a bedrock of the international tax system.

They form the foundation upon which countries manage crossborder taxation and on which taxpayers rely to avoid double taxation. Um today there are an estimated there are estimated to be more than 3,500 such agreements in force worldwide. Um this sheer number reflects how essential uh they are to global economic cooperation.

These treaties play a critical role in facilitating crossber trade and investment. In their absence, businesses and individuals operating internationally would face significant tax barriers um with double taxation being one of the most common. Um in addition, governments would face information asymmetries that interfere with enforcement and threatened tax bases.

So by reducing these barriers, addressing abuses and reinforcing transparency, treaties create an environment where economic activity can flourish across borders. They also have proved quite durable um thereby providing businesses with certainty that in recent times has been somewhat elusive. Um so the OBC model tax convention has been the foundation for bilateral treaties since it was first released in 1963 providing a standardized approach to the negotiation of bilateral income tax treaties which ensures consistency and fairness across all jurisdictions.

In addition and very importantly, the detailed commentaries to the model which also are developed and adopted by consensus um serve as key interpretive aids um that are absolutely critical to maintaining consistency. These model commentaries by setting out the agreed understanding of the meaning and application of the provisions provide additional stability and certainty and are c are extensively referenced and relied upon by businesses and tax administrations when navigating complex international tax rules. Since 1963, the model has been regularly updated to reflect changes in global commerce and tax policy while maintaining its core purpose of providing a uniform basis for resolving issues of double taxation and providing a more certain international tax landscape.

This update, the first since 2017, is no different. Um the changes that are included in the update ensure that the model has is is been adapted to the way business is being conducted in 2025. The update responds to issues raised by businesses and governments alike with a view to providing further tax certainty for all those that make use of the model.

So let me just briefly highlight just a few of the more significant changes in the model. The first relates to remote working uh across borders. Crossber teleawworking existed before the uh co 19 pandemic but its scale and significance increased significantly um both during and after the pandemic and the trend continues uh today.

stakeholders um including many of you joining us today had noted that the existing guidance was insufficient as it related to teleawworking uh arrangements and thus needed an urgent update. Responding to stakeholder concerns, members have expanded uh the commentary to article five of the model to provide clarity on the relevant considerations associated with these arrangements um which I think is is quite welcome. A second change in the model involves the taxation of activities related to the exploration and exploitation of finite natural resources.

Um specifically the commentary to article 5 now includes an alternative and optional provision that allows countries to agree bilaterally to a lower threshold for taxation by the state where the resources are located. Um this alternative provision comes with extensive explanatory commentary bringing uniformity and clarity where the provision is used. Um the alternative provision will be of particular help to resource endowed countries many of which are developing countries.

Next, um the interaction between domestic law rules and uh domestic law rules on interest deductibility and tax treaties and particularly the transfer pricing provision in article 9 has also been clarified. Some of you may remember um the public consultation that was held on this topic and hopefully will welcome uh the additional certainty provided in the update. My team will also inform you about further work that's that has already begun on the topic of domestic law deductibility rules and tax treaties when we get into some of the details.

Finally, um I want to highlight a new paragraph inserted into the model that clarifies the interaction between tax treaties and uh trade agreements. As with the other updates that I've mentioned, the key objective here of this update um or this provision is to provide additional certainty as to how these agreements interact. So, I'm sure you're eager to hear more details on each of these provisions and we will also offer the opportunity to ask questions um at the end.

Um so, let me end where I began which is to emphasize the wider significance of this update. Um tax treaties are not just technical instruments. They seek to eliminate double taxation and reduce barriers to trade and economic growth.

They are enable enablers of global commerce, promoting certainty and stability while fostering trust and predictability in an interconnected and an increasingly uncertain world. Much like the update of the model in 2017 um when the beeps related changes were included a number of the changes included in the 2025 update were also discussed by the inclusive framework which currently has 147 members. The policies underlying the update to the model therefore represent multilateral views and demonstrate the continued importance of governments working together to achieve their shared goals.

Of course, our work will not stop here. Um, delegates to Working Party One, the subsidiary body that is responsible for developing uh the content of the OECD model, will meet regularly in 2026 and 2027 to address technical questions identified in relation to the model, as well as continuing to monitor and discuss recent developments in the sphere of tax treaties. These activities show that the model, its influence and the benefit it brings in maintaining stability and certainty remain at the heart of government priorities.

In parallel, um the inclusive framework will also continue to work on some of the topics that are reflected in this update. For example, the inclusive framework is undertaking work on the global mobility of individuals under an evidence-based phased approach. This will sit alongside the wider range of topics being addressed by the inclusive framework which continue to work together to achieve uh tangible results.

So in closing, I want to reiterate how pleased I am to be with you today to mark this very significant and achievement and I wish to thank you all for being here with us. And now let me hand it over um to back to Jessica as well as uh to the team um to provide you with more detail on the changes included in this update. Thank you very much Jessica.

>> Thank you Manad. And we will now turn to our first presentation today presentation of the changes made to the commentary on article five and we will start with the changes associated with what we will refer to as home office permanent establishment. And for that presentation I am pleased to introduce to you Eve and Rousel and John Stoke two members of the treaty team that supported the work of working party one in this area.

So Eve over to you. >> Thank you Jessica and hello to everyone online. So John and I will now provide you with a high level overview of the updates to the commentary on paragraph one of article 5.

That's the paragraph that contains the definition of a fixed place of business permanent establishment. And the commentary on that paragraph was updated to provide more guidance on its application to certain crossber working arrangement arrangements notably those involving the use of a home office. I will start with presenting you the context that informed those changes as well as a bit the objective of the work and the form of the changes.

After that John will take us through the core of the changes and some examples. We will have a look at what the context is that informed the revised and expanded commentary. And for that, as Manal has mentioned, we have to recall the the disruption that the COVID 19 pandemic caused in general, but also more specifically that it caused to people's working arrangements.

Workplaces were closed, travel was restricted, and many businesses needed to rely on remote ways of working in order to carry on their activities. Now during the pandemic as some of you might recall the OECD issued two sets of temporary guidance which clarified the application of the model tax treaty provisions where individuals got stuck abroad due to the pandemic. This was guidance issued in response to questions from business on applying the rules in those unique circumstances.

Then the pandemic ended and what we saw is that many remote working arrangements continue. If we look back, it appears that the pandemic accelerated and embedded a gradually emerging trend towards increased levels of remote working. And this is often at the preference of the worker as individuals saw that it was perfectly possible to carry out their work from a home and that that brought certain advantages with it.

Now employers want to respond to this phenomenon and the but the emergency context of the pandemic past and that temporary guidance naturally ceased to apply at some point. So business stakeholders continued to tell us that the existing guidance on crossber working from a home was insufficient and outdated. It was giving rise to more and more uncertainty.

The substantive guidance was also only one and a half paragraphs long and even included a statement that crossber teleworking was rarely a real issue. So clearly it was in need of updating and doing that was exactly the priority identified by both business and governments. So moving on to the next slide.

Thank you very much Ria. We can we will now have a short look at the objective that was set for this work. Well, basically that objective was to modernize and expand the guidance to elaborate how the existing principles apply to modern working arrangements and thereby to increase tax certainty for taxpayers and tax authorities relying on this guidance.

The key question that working party one sought to clarify the answer to is when in which circumstances does the use of a home office result in a fixed place of business permanent establishment for the non-resident enterprise. Now with that objective in mind we uh can now consider the nature of the changes that were developed. First, it's important to note that the text of paragraph one of article 5 has not been modified.

That paragraph gives us the key ingredients of the definition which are a place that is fixed and that is a place of business through which the business of an enterprise is carried on. All the changes that were made consists of updates to the commentary on paragraph one. And those changes are first of all the deletion of the pre-existing paragraphs 18 and 19 while retaining uh the principles reflected in in that paragraph which are also reflected in the new material and more importantly the inclusion of a new section in the commentary specifically on crossber working from a home or another relevant place.

And this section consists of 21 new paragraphs including five new examples. One important highlight as I've mentioned is that there have been no changes to article 5 of the model itself. The changes are only made to the commentary elaborating how existing principles apply to this more modern working context.

This means that the new guidance can be applied immediately to existing tax treaties that that are based on the OECD model. There is no need to change the text of a tax treaty in order to apply this agreed interpretation of uh paragraph one of article 5. This new guidance, as I've mentioned, builds upon the existing principles that are found in article 5 and that were also already reflected in paragraphs 18 and 19.

And one of those is that any assessment as to whether a home will be a fixed place of business permanent establishment will always uh be determined by looking at the specific facts and circumstances of an individual case. What also remains is that other elements of article 5 continue to apply or continue to be relevant. Those include first of all the notion of fixed.

So in order for a place to be a fixed place, it needs to have a certain degree of permanency. There is already extensive guidance on this and that guidance continues to be relevant in a working from home context. This guidance, for example, also notes that a permanent establishment will generally not be considered to exist if a place is used for less than six months.

Second, the application of paragraph 4 of article 5 also continues to be relevant. So even where a home would be considered a fixed place of business, it will not be a permanent establishment if the activities that are carried out at that place are of a preparatory or auxiliary nature. And finally, paragraph five on dependent agent permanent establishment needs to be considered separately that continues to be the case.

So let's now proceed with discussing what the updated commentary this new section on crossber working tells us. So the opening paragraphs of the new section set out the evolved context that we discussed um earlier. First of all the commentary now recognizes that it is increasing increasingly possible for individuals to work from a place located in a state that is different from the state of which the enterprise is a resident.

and that such a working arrangement can be initiated by an individual by a worker for personal reasons. So it's not always businesses that request this arrangement. The commentary also recognizes that an individual can work from a range of places that are not the premises of the enterprise or of a connected enterprise.

Commentary in this case specifically mentions the individual's home, a second home, a holiday rental or the home of a friend or a relative. And this type of places have have some unique features as you will. They are generally not accessible to other individuals working for the same enterprise and the individual has a certain level of control over and a connection to those type of of places.

So this is the context in which the updated commentary is uh relevant. And after those paragraphs on the context, there are a couple of new paragraphs that refer us to other bits of the uh guidance such as the guidance on fixed that I mentioned um earlier. Uh now we're not going to discuss those today.

No, instead I'll hand over to John who will take us through the core of the new material. Over to you John. Thank you very much Eve and hello everybody.

Yes. So now we will come on to consider what the commentary tells us about whether a home or other relevant place when a home or other relevant place may constitute a place of business of the enterprise. And as Eve just told us, these are probably the most substantive of the changes relating to use of a home office or other relevant place.

And they certainly contribute the most number of paragraphs to the new commentary. And so we'll spend or most of our time thinking about these changes to the commentary on article 5, focusing on when a home or other relevant place results in a place of business for an enterprise. So what does the commentary tell us?

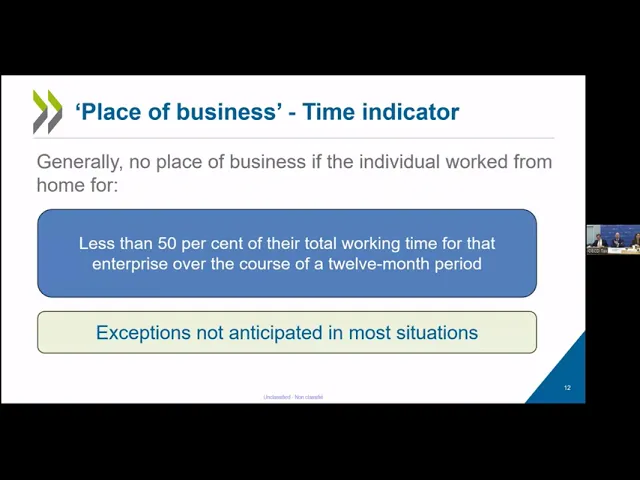

Well, importantly, it tells us or it gives us what is labeled here on this slide as the timebased indicator. And that timebased indicator tells us that if a home office or other relevant place is used for less than 50% of the total working time of that individual for the enterprise over the period of 12 months beginning or ending in the fiscal year concerned then that place will not be a place of business of the enterprise. The commentary also tells us exceptions to this approach are not anticipated in most situations given the context in which this commentary is written and is described.

Paragraph 44. 1 of the commentary and which Eve described to us on the previous slide. What does all this mean?

Well, this is a very significant update to the commentary. It tells us that if an individual spends less than 50% of their working time from their home or other relevant place, then that place will not be a place of business of the enterprise, which means that home or other relevant place will not be a fixed place of business, permanent establishment of the enterprise. And this approach responds to many of the questions, concerns, issues that you, our stakeholders, raised with us in the process that was was described by Eve just a moment ago.

It's intended as a first step, a relatively simple first step that deals with the most commonly observed situations. If there an individual works from their home for less than 50% of their working time, that is the end of the story. Generally speaking, no further analysis is needed.

There will be no fixed place of business permanent establishment. And in including such an approach in the commentary, members of the OECD were seeking to provide additional tax certainty for all of us for taxpayers and for tax administrators when we seek to anal analyze whether a home or other relevant place results in a fixed place business permanent establishment for an enterprise. Having thought about situations where an individual spends less than 50% of their working time from a home or other relevant place, we must then go on to think about the alternative situation where an individual spends 50% or more of their working time from a home or other relevant place.

Importantly, that first time indicator acts as a filter. An individual who works for less than 50% of their time from place no further work said as I as I mentioned but it is not the end of the story if they spend 50% or more of their working time from that place that does not automatically mean that that home or other relevant place is a fixed place of business permanent establishment it's not necessarily a place of business we just need to understand the facts a little bit better Now, as with all determinations of a permanent establishment, as Eve said, this is a facts and circumstances type approach. However, what the commentary goes on to tell us is that a prominent consideration is whether there is a commercial reason for the use of that home or other relevant place for the carrying on of the business of the enterprise.

Now that leads us to consider well what is a commercial reason in this context and essentially we're required to answer the question as to whether the physical presence of the individual in the state where the home or other relevant places located facilitate the carrying on of the business of the enterprise. The commentary helps us to address that question and it says that a commercial reason will be present where the individual directly engages with customers, suppliers, associated enterprise or other persons on behalf of the enterprise and that engagement is facilitated by the individual being located in that state in the state where the home office or other place is located. Helpfully, the commentary gives us eight illustrative examples of where there will be a commercial reason.

It tells us what these kind of arrangements might look like. And it includes an individual who directly meets with customers, suppliers or or wherever else it might be in that state. Um it might be that the individual performs services at the premises of a customer who is located in that state.

So maybe some training um services or or maybe some repair type services. But you have eight examples listed there. One of those particular examples um is is worth just pausing on because because we've had some some questions addressing that particular circumstance and it's it's where the use of a home or other relevant place enables real time or near realtime interaction with customers or suppliers in different time zones.

So just to just to explain this a little bit further, we'll we'll maybe use an illustrative example. So consider that we have an enterprise that wishes to provide 247 medical services to its customers and let's assume that this business is located in Oceanana. Now if it is to provide those services around the clock to its customers who are in Oceanana, it would need to require its employees to work through the night.

Some of those employees would have to work during the nighttime to provide those services to to customers in Oceanana. To avoid that, the enterprise says, "Aha, I know what I can do. I can use employees located in Europe to provide those services from their home in Europe remotely.

And when they provide those services, it will be daytime for those individuals. we won't require anybody to be up at 3:00 in the morning in order to provide our services to customers. And so what that enterprise does is it moves to a model whereby services provided by employees located in their homes in Europe.

That gives us an example of an enterprise that is making use of differing time zones between where customers are located and where the home office is located in order to facilitate the delivering of its business activities. The commentary tells us that kind of arrangement would result in a commercial reason for the use of a home or other relevant place. Okay.

So having considered when there is a commercial reason, the commentary also tells us when the opposite is true, when there will not be a commercial reason. Those three reasons are listed on this slide. The first of which is if engagement is intermittent or incidental.

This is a a concept that you will find elsewhere in the existing commentary that discusses place of business. And so again, as Eve described, we're just following through those principles into our discussion of place of business in this context. Likewise, if an individual is permitted to work from home solely to retain the services of that individual, there is no link between the home and the the geography in which that home is located.

There will be no commercial reason for allowing that activity for the for that activity being undertaken from a home. And finally, an individual permitted to work from home solely to reduce costs will not result in a place of business. So let's say that a business moves to a home only model just to reduce costs on office space.

That would not result in the home being a place of business. Now with all of that said, it could be that there are a number of reasons for the use of a home or other relevant place. If one of those reasons is a commercial reason, then that would be sufficient for that home or other relevant place to be considered a place of business of the enterprise.

Now hopefully to assist you all, we have a number of ex illustrative examples included in the commentary. They cover a number of different concepts that we've been discussing in our time today. And each of those contain a justified conclusion.

And we'll just spend some sign considering two of those examples which hopefully illustrate the context concepts that we've been talking about in our time so far. The first of those is example B. Now, example B tells us about an employee of Aco, which is a resident of state R, who works from her home in state S for one or two days per week, and she does so over the course of a long period of time, over the course of a year, for example.

Here, the home would be considered fixed because it is used for the purpose of those activities over a extended period of time. it has a sufficient degree of permanence because it's used for let's say 12 months or whatever it might be. We then must consider whether this place is a place of business of the enterprise and following the time indicator that I described.

We know that this individual spends less than 50% of her time working from her home. That's the end of the analysis. This place is not a place of business of the enterprise.

the use of her home does not result in a fixed place of business permanent establishment. Finally, we'll consider example D. And example D, we have an employer, Aco, a resident of state R, who has an employee in state S, who spends 60% of his working time working from his home in state S.

Now this employee delivers a range of services remotely to customers of ARCO that are situated in state R that are situated in state S and they're situated in third states. This individual does however visit the premises of one of the customers of ARCO in state s for one day per quarter just to review how the contract between Arco and that client is being operated, how it's being implemented and so on. What's the analysis here?

Well, first of all, just like the prior example, this is a fixed place because it's maintained for a year for an extended period of time. It has a sufficient degree of permanence. The question is then whether it is a place of business.

This individual spends 50% or more of his working time from his own home office. The time indicator is satisfied. We must then go on to consider whether there is a commercial reason for his presence in state S.

Here we know that this individual does go to the premises of a customer. However, he does so only one day per quarter. That would be considered an intermittent or incidental uh kind of approach for this purpose.

He's only there very rarely and not for not a very long period of time. As such, there would be no commercial reason for this individual to work from his home office. There would be no place of business.

There would be no fixed place business permanent establishment. And with that example, that concludes our comments on the updates, the commentary on article 5 that relate to home office permanent establishment. Um, and so I will pass back to to Jessica to move us along to the next section of the presentation.

>> Many thanks John and E. Thank you very much. We will now move to the second presentation of the day.

We stay in the commentary on article five on permanent establishment, but we we're going to focus now on this new optional provision, the new alternative provision on extractive. And to walk us through that provision, I'm pleased to introduce to you Sarah Shurmer, a member of the treaty team that has supported working party one's work on the provision. Sara, over to you.

Thank you. >> Thank you, Jessica, and hello to all. I'll now present the changes made to the commentary on article five regarding the taxation of activities related to the exploration and exploitation of finite natural resources or extractive activities for short.

So in terms of context, the the broad policy consideration behind this update is that countries endowed with finite extractable natural resources such as oil, gas, and minerals will often seek to secure an adequate share of the value bound up in those resources. Now, there are a variety of methods and instruments that can be used to achieve this goal. And the focus here is on introducing a lower permanent establishment threshold for this specific purpose.

If we look at the ordinary definition of a permanent establishment in article five of the OECD model, a lot of activities and in particular services relating to the extractive sector may not meet the relevant criteria. For example, these activities could be of a very short duration or they could be highly mobile such that such that they would not constitute a fixed place of bi of business within the meaning of paragraph 1 of article 5. But these same activities may be of a high value and countries where the resources are located may want to seek to preserve their taxing rights at source on the profits of non-resident enterprises from those activities by providing a lower permanent establishment threshold in this context.

A number of existing treaties already contain a provision of this kind. However, it was recognized that greater consistency in terms of approach and interpretation was needed in this area building on existing experience. The objective of this update is to offer a standardized template provision that could be used by states that have agreed bilaterally to follow this approach.

In other words, the starting point of this new section of the commentary is that states have already agreed to include in their treaty a lower threshold for source taxing rights over the profits of non-resident enterprises carrying on extractive activities. The aim of this update is to support greater consistency and certainty of interpretation of these provisions. So what are the changes exactly?

This update introduces in the commentary on article 5 a new alternative optional provision with detailed related commentary setting a lower permanent establishment threshold in the extractives context. Specifically under this alternative provision a non-resident enterprise would be deemed to have a permanent establishment where it carries on relevant activities in a state for more than a bilaterally agreed period of time. Which activities are covered by the alternative provision?

Broadly speaking, the provision covers activities connected with the exploration or exploitation of non-renewable or finite natural resources. The provision comes in two forms, one that covers offshore activities only and another that covers both onshore and offshore activities. The offshore only version covers activities carried on offshore in connection with the exploration or exploitation of the seabed, its subs soil and their natural resources.

This is subject to a specific exclusion for the operation of certain vessels which we'll get to in a moment. The onshore and offshore version is broader. Firstly, it covers all activities in connection with the offshore exploration and exploitation activities regardless of whether these connected activities are themselves carried on on or offshore.

Second, it extends to the exploration and exploitation of onshore finite natural resources together with connected specialized activities. Now here the term specialized ensures that the provision won't extend to standard or generic activities that may simply happen to take place at a site of extraction on shore. Instead, it is targeted to the activities uh involving a degree of expertise or the use of specialized equipment in a way that is tailored to the onshore extractive activity.

Now a variety of examples are provided in the commentary which we won't go into here but of course I invite you to consult them uh in in the commentary. Now the same exclusion for the operation of certain vessels applies to both versions of the provision. This exclusion covers the operation of ships or aircraft used for the primary purpose of transporting supplies uh or personnel or of towing or anchor handling or the operation of other vessels whose function is auxiliary to offshore extractive activities.

We note that article 8 will continue to apply in respect of international traffic and any other activities that may be excluded from the scope of this alternative provision would continue to be subject to the ordinary rules in articles five and seven. One final note here you'll see that both versions of the provisions refer to activities carried on in connection with exploration and exploitation. This covers certain related services and importantly it should also be understood in the temporal sense.

So connected activities would be covered at every stage of the extraction process from exploration through to development, production and decommissioning. Now moving on uh let's look at the core operative rule of the alternative provision which is set out in its paragraph three. This rule provides that where an enterprise of one contracting state carries on relevant activities in the other contracting state being the state of source for more than a minimum period of time.

Those relevant activities will be deemed to be carried on through a permanent establishment of the enterprise in that state of source. For purposes of applying this threshold, only the relevant activities carried on by the enterprise in the other contracting state are taken into account. This is the case regardless of whether the activities relate to one or more customers, projects or other factors.

However, activities carried on anywhere else outside the state of source will not count towards this threshold. The duration of the time threshold is left to be bilaterally agreed by the parties and we observe a range of different thresholds used in the existing treaty provisions of a similar nature. Where a permanent establishment is deemed to exist under this provision, then the state of source may tax the non-resident enterprises profits that are attributable to that deemed permanent establishment in accordance with the usual rules on business profits and profit attribution set out in article 7.

Finally, I I'll quickly mention some other aspects of the alternative provision, starting with its fourth and final paragraph that deals with capital gains. This paragraph confirms the source state's primary right to tax gains from the disposal of certain extractive related assets. It brings together the rules governing the treatment of capital gains in this context and largely matches what is already found in article 13 on capital gains as it relates to immovable property and movable property of a permanent establishment.

The provision also provides a potential expansion um of source taxing rights in respect of gains from the disposal of shares or comparable interests that derive more than 50% of their value from underlying extractive related assets. The commentary accompanying this alternative provision also sets out a number of possible additions or variations on uh that provision. For example, it includes a tailored anti-contract splitting rule that could be used and examples of provisions that would expand source taxing rights on employment income connected to relevant extracted activities.

With that, I'll now hand back to our master of ceremony, Jessica. >> Thank you very much, Sarah, for your presentation. We will now move to our last presentation of the day.

a presentation that will cover both the changes made to the commentary on article 9 on transfer pricing and the changes made to article 25 and its commentaries on dispute resolution. For that presentation, I'm pleased to introduce to you Edward Barrett, a member of the treaty team that has supported working party one on both of these work stream. So Ed, the floor is is yours.

Thank you very much. Thank you very much Jessica and hello to all of the participants who are welcoming us with us uh online today. Going to start the presentation of the changes to the commentary on article 9 by putting these changes in their context.

The work on these commentary changes had its origin in related work on the transferpricing aspects of intergroup financial transactions. This other work was carried out by working party 6 and resulted in chapter 10 of the transfer pricing guidelines. In the work on chapter 10, a number of questions were raised about the interactions between article 9 and certain domestic law rules designed to prevent beeps.

These questions also concerned interactions between the existing commentary reflecting the 1986 report on thin capitalization and the conclusions that would be set out in chapter 10. The new commentary addresses these different questions. Like other parts of the 2025 update, these commentary changes were finalized taking into account input from a public consultation.

in this case a March 2021 public consultation. Looking at these changes, what they do is provide guidance and increased certainty concerning the application of article 9 of the OECD model and domestic law rules for the determination of taxable income like domestic law rules on the deductible deductibility of interest. In particular, these changes align the commentary discussion of approaches to characterize and p price intgroup loan transactions with the conclusions that are set out in chapter 10 of the transfer pricing guidelines.

These changes also clarify that article 9 does not deal with the issue of whether expenses are deductible once profits have been allocated in accordance with the arms link principle. The changes to the commentary in article 9 are accompanied by related changes to the commentary on article 7 and to the commentary on article 24. In connection with these commentary changes, it's important to note here the concerns that were raised by stakeholders in the context of the public consultation.

In particular, stakeholders raised the issue of domestic law provisions that may operate in a way similar to article 9 and related issues of access to the mutual agreement procedure to resolve possible economic double taxation. In response to these concerns, we are considering different examples of such domestic law provisions and the issues they present. The goal is to reach a common understanding of the contours of these issues and how to address them including by identifying circumstances in which access to the mutual agreement procedure is appropriate.

We'll move now uh concluding this overview of the content of the 2025 update with a look at the changes to article 25 and its commentary. New paragraph 6 of article 25 elevates a modified version of an alternative provision until now included in the commentary in article 25. This new paragraph reflects the circumstance that while tax treaties and trade and investment agreements generally work well together to promote crossber trade and investment, their shared objectives can sometimes lead to overlaps and uncertainty.

Such issues result in particular with the general agreement on trade and services or GATS in connection with certain non-discrimination disciplines and dispute resolution mechanisms. New paragraph 6 of article 25 addresses two long-standing issues with how the GATS national treatment obligation applies to tax measures. These issues can in turn create uncertainty regarding the legitimate distinctions made in domestic tax laws for sound tax policy reasons.

How does the new commentary uh how does the new provision address these different issues? Well, first new paragraph 6 ensures that tax competent authorities will decide whether a measure falls within the scope of a tax treaty for all treaties regardless of when those treaties entered into force. Under the GATS, how this issue is resolved in the absence of this provision can differ depending on when a tax treaty entered into force.

in particular whether that tax treaty existed at the time the GATS entered into force in 1995. The second issue addressed by new paragraph 6 concerns what it means for a measure to be within the scope of a tax treaty for purposes of the GATS. Paragraph 6 provides an express definition thereby eliminating potential uncertainty as to the meaning of this concept.

Before closing this presentation of the content of the 2025 update, we wanted to note certain other changes to the commentary on article 25 connected with amount B of pillar one. This new commentary signs posts specific language in the report on amount B relating to tax certainty and the elimination of double taxation. This commentary provides relevant cross references to the report on amount B and is intended to ensure that optionality is preserved in all dispute resolution mechanisms for non-adopting jurisdictions.

With that, I thank you for your attention and I will pass the floor back to our master of ceremonies. Thank you. >> Thank you very much, Ed, and thank you very much to all our speaker for today's webinar.

We have only a few minutes ahead of us and we will need to close this webinar. So we won't have the time to go through all of the questions that you've submitted. We want to stress that the questions you've submitted are all interested in relevant and we want to thank you have submitted those question.

They will inform most probably our future work and they they might also inform future material that we will be producing. So thank you very much for those question. I might take one or two just very quickly looking at the time here.

We got um a question from several of you asking us that guidance on home office fee the guidance developed and incorporated in the commentary on article 5 do do country needs to update or change the bilateral tax for that guidance to apply or can I rely upon that guidance immediately so that's a question that we receive and here the very short answer is that you could you can rely upon that guidance immediately and that bilateral textually do not need to be changed or modify in order for that guidance to kick in if you want. So that's the short answer. Um another question that we've received as well on the commentary on the changes made to the commentary on article nine, we had a very interesting question um from a person asking you've changed paragraph three of the commentary on article 9 that was there for a very very long time.

What's the intention behind that? So for those who remember paragraph three of the commentary on article 9 reflected the conclusion of the 1986 report on tin capitalization. So it's not a paragraph that was very new.

That paragraph was updated and it's only and purely to reflect the updated conclusion um on tin capitalization that were that were reaching that you could see on chapter 10 of the transfer pricing guidelines. So that this is this is this is it. This it's it's only that we we unfortunately don't have much time for question.

We will close this webinar. But before we do so, we just wanted to thank you all for being with us uh today at the webinar. We also wanted to thank a lot of you for the work that you have conducted conducted on the changes that we've made on the model because uh as you may know the changes the update to the model convention is a collective effort.

So we wish to thank and we know that there are several of you on the line. We wish to take thank all the delegates of working party one for their hard work on this. We also wish to thank all of these stakeholder all of you stakeholders that have provided inputs throughout the years on the changes we were making.

So you you you remember public consultation on extractive on article 9. We we've discussed with several of you as well the changes that we made to the commentary on article five on on this whole month. So many thanks uh to you all.

This is truly a collective effort. And finally as well many thanks to the team here. Uh the entire treaty team is in this room.

So many thanks to the speakers but many thanks as well to other members of the team uh who made this webinar happen. So thank you very much and the work will continue. So we will be in touch very soon.

Thank you.