[Music] [Music] [Applause] [Music] welcome students so now we are going to uh talk about the next technique of the financial statement analysis and this technique is the cash flow state by preparing the cash flow statement we uh are uh now going to understand the uh performance of the company or what is depicted by the financial statements and what is the overall cash position of the form you see that uh why there is importance for the cash management or the preparing the cash flow statement cash flow statement we prepare the cash flow statement and and why

there is a need for preparing the cash flow statement because uh when you prepare the profit and loss account we have discussed it earlier also but let's recall it again uh this time you taking sales it is sales and you're taking the closing stock and here you're taking the expenses that is raw material wages and the other direct expenses right these are the three things so we are taking here the sales and are we writing here that the sales are on cash how many shes are on cash and how many sales are how much sales

are on credit are we writing like this we are not writing like this we are writing that the sales so then the sales are sales and no distinction between the cash sales or the credit sales in that situation in that situation if for example some form is selling in the market and that to the ratio is 8020 80% of the sales are on credit and 20% sales are on cash so finally when the net profit net profit after tax we are working out here and that profit works out as here is 20 uh 5% but

again this profit you have to segregate into that in the ratio of 8020 in the ratio of 8020 so in that case also you would have to find out that my 20% of the profit is on credit and 25% profit is only on cash save whatever the ratio works out so this is a very very dangerous position for the Farms this kind of the firms or firms having this kind of the balance sheet of the profit and loss account can't sustain much longer they will have to stop their business and they will have to be

closed down because their credit sales are going to put them in the trouble because we see that when there are the credit sales there are the bad debts also and higher the amount of credit sales higher the amount of bad debts higher the amount of credit sales there is the higher the amount of the bad debts and if the larger chunk of the bad debts are there it means buy you are selling on the credit and what you are talking here as the profit for why you're talking here as the profit for means there is

no profit as such we are say misguiding the people misguiding the investors misguiding the lenders misguiding the suppliers everybody's stake is at risk everybody's stake is at risk so this is the one important question that we have to address by preparing the cash flow statement and you see the foolishness of the company's management is that when they are selling 80% on the credit and here means when the sales are growing because you sell to anybody on credit people are ready to buy it they have not to pay they have not to pay to the company

at the moment they receive the inventory or they receive the consignment they'll sell That Consignment in the market later on they'll keep their own profit with them and then they'll rebit the company's part to the company and sometimes they can say that I couldn't sell in the market or I sold to somebody F else further in the on the credit he has not paid it back to me so far so if he pays me if he pays me I'll pay it to you if he doesn't pay me I can't pay you so it means in

that case the bad debt will also further the proposition or the magnitude or the extent of the bad Debs will further uh aggravate so in this situation and another important uh say negative point of this kind of the sales and selling process is that when you are selling in the market on credit your sales are growing and cons your profit is also growing and when your profit is growing your tax obligation on the profit is also growing your tax obligation on the profit is also growing it means you are paying the tax on those sales

even which you have not collected so far those sales which you have not collected so far you are paying the tax on those sales even so it means any income which has not come to me and I'm paying the tax on that what kind of the business I'm doing so there lies the importance of the cash flow statement that yes we have to prepare the cash flow statement and we should be knowing that by preparing the cash flow statement when any amount of the profit is shown by the company and equal amount of the cash

is not there in the bank account of the company it means if a profit making company it must be a cash profit and the balances of the cash and bank balance of that year should be say comparable to the profit maybe something maybe it's can be 9010 or uh 80 20 difference can be there that 80% of the profit is Cash profit and 20% is the credit profit accepted but if it is at 2080 that 20% is cash and 80% is credit it means you can make out that if you are going to deal with

this kind of the companies then you're going to put yourself in trouble so we want to verify that if the compan uh posing as a profit making organization excellently doing organization having the largest market share in the market you tell us whether the profit you are showing in the profit and loss account is Cash profit or larger chunk of the profit is only the credit profit or it is a pseudo profit or it is a nominal profit that's the million dollar question we are going to address here so then I'm talking to you about the

cash flow statement let's talk about the some important aspects of the cash management some important aspects of the cash management because as a true financial analyst you must be knowing the background of the cash management and then the Need For Preparing the cash flow statement that the cash management as a whole is concerned with what it's concerned with the three important issues first issue is cash flow into and out of the firm cash flow within the firm and cash balances held by the firm at a point of time cash balances held by the firm at

a point of time cash flow into and out of the form so it means by preparing the cash flow statement we are going to study that from where the cash or how much cash flows into the form and how much cash flows out of the F for example we are buying raw material we are paying wages we are paying other direct and indirect expenses and we are earning some incomes also so if we are producing something and we are selling something if we are producing something cash is Flowing out because are buying so many inputs

and if most of the inputs are coming on cash so it means you have to pay the cash and compared that how much cash is flowing in by way of sales by way of indirect incomes and uh so many other things how much cash is flowing in so how much cash is Flowing out how much cash is flowing in you have to uh make out for that and by preparing the cash flow statement you can easily make out that yes what is my cash position or others who are the external stakeholders to the company they

can easily make out that what is the cash position with this form if the cash position is not there then form selling on the credit in the lust of increasing their market share pseudo market share or in the lust of making maximum sales in the market they can soon become the sick FS sick organizations and they will not be justifying with their investors with their lenders or with their suppliers this is one important component second is cash flow within the FM you see that when you talk about the liquidity in the form that is defined

in the form of cash when you talk about the liquidity in The Firm that is defined in the form of the cash and what is the true liquidity it's not the true liquidity that you have sufficient amount of the cash in the farm true liquidity is say there are the different departments in the FM different uh uh divisions and subdivisions in the firm and they all have the def def Miss they all have their own definition of liquidity they all have the definition of liquidity for example you talk about the purchase Department purchase Department in

The Firm first because first of all if you have to start the manufacturing process you have to buy the raw material and if you have to buy the raw material it means you have to purchase the raw material purchase the raw material means you have to have the funds for that so what is the liquidity for the purchase department is having sufficient amount of the cash and funds with the purchase department or being provided by the finance to the purchase is the liquidity yes that is a liquidity one part but the second part of the

liquidity is that the purchase department is having sufficient funds sufficient cash for buying the raw material and being provided by the finance also by the finance department but there is no raw material in the market there is no raw material in the market so what is the purpose of that liquidity so liquidity for the purchase department is having cash one and having sufficient material in the market to this is the liquidity similarly you talk about the and that way for the production also there's no purpose of liquidity because purchase won't be there so production won't

be there so production department is also requesting for the or asking for the cash liquidity and for the material liquidity similarly we talk about the liquidity for the say your marketing department liquidity for the marketing department when you talk about the liquidity for the marketing department maybe or sales department marketing and sales both we talk about marketing and sales department now what is the liquidity for the sales department sales liquidity for the sales department yes when they sell in the market and if they sell a maximum part of their production in the market on cash

they are generating sufficient liquidity for the firm but if there is a demand for the firm's product in the market marketing and sales people are getting the frequent requests from the different say channels of distributions in the market but the company has no uh say uh output and no inventory company has no inventory what the marketing and sales people will sell in the market you have funds but you have no inventory there's no production it means the liquidity for the sales people is useless so because it's is getting affected it's having a circular process when

the purchase Department couldn't purchase because there was no raw material in the market production Department couldn't produce because they didn't get any production material from the purchase and then marketing people not have anything in the G down to sell in the warehouse to sell because there is no output there is no inventory nothing so it means what is the purpose of that liquidity so we have to ensure the liquidity from both the angles that there is a cash also and there is a material also so if there is a possibility that in the future course

of action you might face the shortage of a particular kind of a material in the market so you have to buy in the current period you have to buy the maximum and when you buy maximum you need Maximum cash today not tomorrow so you need more liquidity today and all the times all the years all the days all the months we don't need the same amount of cash but still we have to be careful that how the cash is Flowing within the firm and if the cash is Flowing properly from the one Department to the

other and other department to the other then there is no issue there's no problem and easily the situation can be managed then cash balance is held by the firm at a point of time as I told you that holding of the current assets and cash is also the one important current assets so you have to keep Optimum amount of the cash in the farm it means by looking at the cash balance with the form at a point of time you can easily make out if the balance held by the farm is very high in that

case you can say that in that case you can say that the f is a poor manager of cash they don't realize but that keeping high amount of the cash has a cost and if the cash balance is low then always the farm is in a vulnerable position because there is a possibility of form facing that Tech insolvency any time any payment becoming due to be made any current liabilities becoming due to be paid and the firm doesn't have the cash so we have to maintain Optimum amount of the cash and Optimum amount of the

cash we have to decide depending upon the operations of the firm depending upon the production process sales and other requirements we have to decide that what is the optimum amount of the cash so you have to look it at while preparing the cash flow statement you have not to look only the existence of the cash how much cash is there there one and we have to see that if the form cash is Flowing me efficiently within the different Departments of the firm in that case you are sure that because all the the your your your

production is sufficient your sales are sufficient your uh sales revenue is sufficient your profitability is sufficient and your cash is sufficient so one thing cash is affecting everything cash is basically called as the life blood of the company so if the say for example in the human human body if the life blood is me the blood in the human body is more it's not good if it is less we are anemic similarly in the company so we have to have Optimum amount of the blood in the human body similarly in the company if there is

more cash it means we are over capitalized we are over liquid form extra liquid form and that is not good because it will increase the cost it will not earn anything for you similarly if we are under cash then in the that case again it's affecting form will be anemic form will be technically prone to become technically insolvent and form will become uh almost uh sometime a bad performer so we have to maintain the required amount of the blood required amount of the cash in the F all the times we have to keep it so

these are the three important issues we are going to know with the help of cash flow statement or by preparing the cash flow statement now the next thing is that why the firms keep the cash why the cash is required there are the three motives like inventory if you have gone through the inventory process like inventory the cash is required for three purposes one is for the transactions so we call it as the transactions making the payment receiving the payments receiving the receipt making the payments you need the cash precautionary balance we always maintain a

minimum level of the cash we never allow the balance of cash go below that particular level if that goes below that level it means form can at any time become technical insolvent any payment becoming due to be made Farm doesn't have the sufficient liquidity sufficient cash so for that reason precautionary balance is required and third is the speculative balance sometimes you get the opportunity in the market that you have a special type of material is easily available in the market which is otherwise not so it's better if you be buy that material and store it

today because it's easily available one and it is available at the acceptable price so it means in that case for the or it can be possible that you buy this material today in bulk at the very cheap prices and then you sell it tomorrow at the very high prices so it means in that case also for that is called as a speculation because you buy today store it and you are expecting demand for that material will increase tomorrow but if it doesn't increase then speculation goes wrong so for the speculative purposes we keep cash we

use cash and sometime if our speculations go right we earn best return by investing that cash on the speculative purposes now here are the very other important very useful other important Concepts they are like cash versus profit cash flow and cash stock and cash flow project presentation cash versus profit you are going to be now after this good financial analyst because you are studying this subject that is the financial statement analysis and Reporting so do you feel that having profit by the FMS is sufficient is it only requirement of the firm that they should be

earning the profits or something more than that we have already discussed here at length by preparing looking me looking at this profit and loss account and when we prepare this profit and loss account I have told you sometimes in the past also back also that when you prepare the cash is profit and loss account and you calculate that profit maybe the gross profit or the net profit finally it will be the result is two net profit from where which account you're getting the N profit profit and loss account profit and loss statement and what is

the profit and loss statement it has incomes and gains on the credit side and it has the expenses and losses on the debit side and where this rule applies on which type of accounts nominal accounts so profit is nominal which is given to you by the nominal statement it means the profit is nominal and the cash is real so we have to be careful here that you have cash profits or you have only profits if the cash profits are there then you can boast off that yes my profit is the cash profit and that's a

real profit because cash is real cash is the asset and asset is a real account so cash is real profit is nominal so having earning profit only is not sufficient you should have the cash profits this is one important thing if you ear only profits and feel satisfied that my profit will come tomorrow you have sold on credit you are illusioned that you will be able to collect all the sales because part of the sales will become the bad debts and that profit will never come to us we've already discussed at length second thing is

cash flow and cash stock cash flow and cash stock you have sufficient cash but if it is lying as a stock and it's not flowing well pick up the balance sheet of any public sector company who is a profit making company I tell you pick up the balance sheet of BHL or any other public sector company you will find huge amount of the cash lying in the balance sheet of that company and nobody's concerned about the use of that cash they have huge cash huge Collections and entire amount of the cash after paying all their

obligations salaries administrative expenses selling advertising all kind of expenses still huge amount of the cash is lying in the balance sheet of psus because they don't know and they are not concerned with the real management of cash so true manager Financial Manager or the Chief Financial Officer of the company he should be knowing it that keeping high amount of the cash is not good so you have to make out by preparing the cash flow statement that you have the cash stock or you have the cash flow cash is flowing in the form from the one

Department to other other to other and if there is a surplus cash then it is Flowing out of the form and being invested in the marketable Securities short-term Securities that's a good strategy and if the cash is kept as a stock means it's flowing but but it is kept so much in quantity in Quantum in the in the in the amount that this much cash is not required in the farm it means why are you keeping so much of the cash don't you know that keeping cash is a costly Affair it doesn't earn anything for

you but it has a cost so it means keeping cash in the form of the cash stock is not good for us cash must be flowing and we should not keep the stock of the cash we are going to find out with the help of the the cash flow statement that what is a Quantum of cash cash is Flowing or the cash is static third important thing is the cash flow presentation cash flow presentation or preparing the cash flow statement earlier when we were preparing the cash flow statement we were starting with we were starting

with the we were preparing a simple cash flow statement that we were starting with that total profits of the firm net profit or profit after tax and then we were adding back certain non-cash expenses and then we were subtracting the cash outflows so we were adding the cash inflows and the non-cash items and we were subtracting the cash outflows and we were finding out that this is my closing cash balance and that was easily table with the balance given in the balance sheet that was there that was the process but now the process has changed

from 1st January 1994 internationally there was a development with regard to the cash flow statement and International Accounting standard committee iasc on 1st January 1994 changed the process of preparing the cash flow statement change the process of preparing the cash flow statement and Ias said that now the cash flow statement means there were the two developments one that cash flow statement will be the statutory statement now required along with the income statement and the balance sheet it will be the third statutory statement required and to be provided to all the stakeholders it will be me

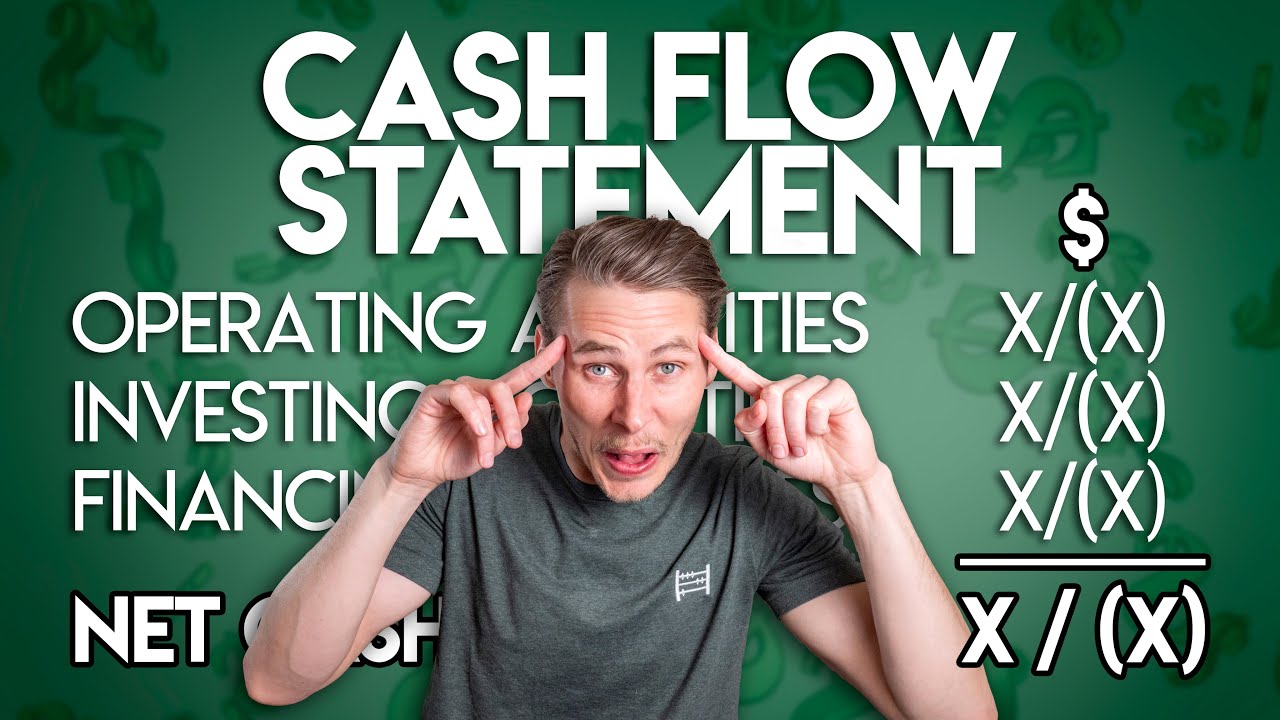

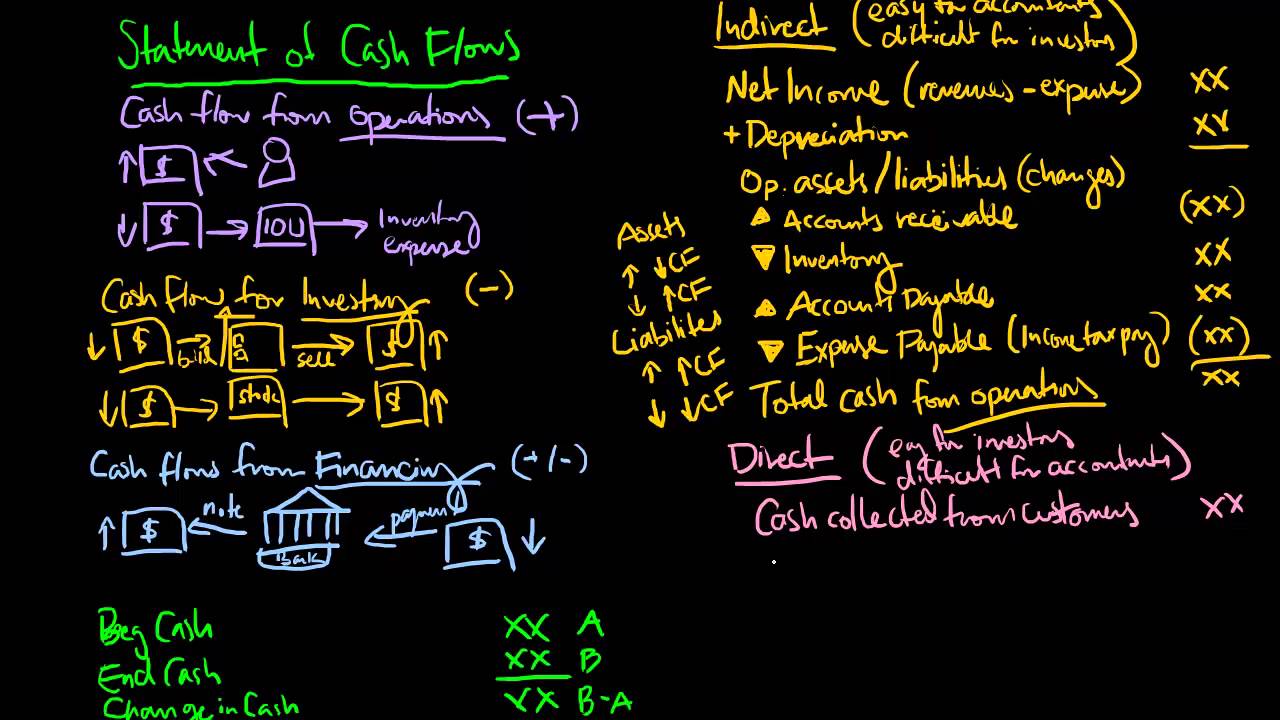

it will be the part of the balance sheet and every form has to prepare who is following the International Accounting Standards they will have to prepare compulsorily the income statement that is a profit and loss account balance sheet and the cash flow statement that was the one development and the second development was that now the cash flow statement will not be a simple composite cash flow statement but this has to be prepared in a different Manner and cash flow has to be shown under these three activities operating cash flow cash inflow and cash outflow on

account of the operating activities cash inflow and outflow on account of the investing activities and cash inflow and outflow on account of the financing activities these three activities we will have to show the cash flow so that we can easily make out why me cash flow from operating activities investing activities and financing activities I discussed at length with you sometime in the previous lectures that as I told you we I gave you the example of of the videoon and I have told you that when you calculate the gross profit of the company you will get

that's not a gross profit rather a gross loss so if you talk about the operations of the videoon and Onida they are very poor but at the end of the profit and loss statement if it is a gross loss here then it should be a net loss here but it is not the N Net loss but it is the net profit because larger chunk of the cash is flowing in videoon and Onida not from operations but from the investing activities or from the financing activities is videoon a Investment Company is videoon a financing company if

the videoon is a manufacturing organization major chunk of the cash must be flowing in from the operations second thing is yes there can be the inflow of the cash from investing activities and there can be cash from the financing activities but the magnitude of that cash must be the minimum must be after the operations first it should be the major contribution should be from operations and then from the investing activities and then from the financing activities so now today when we prepare the cash flow statement we prepare under this format that we divide the total

inflow into the cash flow from operating activities investing activities and financing activities in India though IAS accepted this standard in 1994 1st January 1994 but in India this standard was this change was adopted and made effective from 1997 in 1997 Institute of chared accountants of India they introduced new standard which is called as as3 under as3 now in India also the preparation of the cash flow statement is a mandatory requirement is now statutory requirement so along with the income statement and the balance sheet now in India also the third statement required is the cash flow

statement and the cash flow statement has to be prepared under this process cash flow from operations cash flow from investing activities cash flow from in financing activities and it has to be prepared in this fashion in this manner and in this style so in India now from 1997 also it has become mandatory it has become compulsory and it has to be prepared in that manner and in that way that it is cash flow is shown under the three activity so that any stakeholder maybe he's an investor he's a lender he's a supplier he can easily

make out what is the future of this company if the major is a manufacturing firm and he a maor major outcome of the cashes from the operations fine then it can be from investing also it can be from financing also but if it is more from investing and financing less from operations you can make out that the operating structure of the FM is poor financial structure is good so very soon the poor operating structure would eat away the strong financial structure also and soon this company may be a sick firm so my investment my supplies

my payment are not safe and secured in this company so I should not deal with this company I should not do the business so for the reporting purpose in India reporting of the financial statements now this statement has also become compulsory and in India also under say as3 now the cash flow statement has to be prepared under the three activities operating investing and financing and that composite statement is now of not that any requirement but when we are preparing the cash flow statement we are starting with the composite cash flow statement we are preparing a

basic cash flow statement then we are doing some analysis and after that we are preparing the final cash flow statement and that final cash flow statement is again based upon this so you have to confirm that the balance of the cash given in the balance sheet is true number one you will be confirming by preparing both the statements basic cash flow statement and the final cash flow statement and at the same time you will get the second answer that whatever the cash flow we are showing in the balance sheet and proven by the Prof this

cash flow statement how much it is coming from the operations how much from the investing activities and how much from the financing activities so what are the operating activities considered under as3 and the ic's standards and investing and financing activities first we will learn that what are the operating activities what are the investing activities what are the financing activities after that we will start we will we will learn how to prepare the cash flow statement under this new standard ES3 and then how to analyze that statement that discussion I'll do with you in my next

part of discussion in the next lecture till then thank you very much [Applause] [Music]