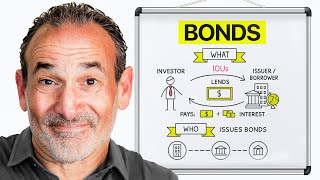

Stocks, bonds, currency. When you buy them, you own something real. But derivatives?

You're not buying anything. You're betting on a deal. A contract that can pay big or really burn you.

Let's see how they work. Imagine you're considering a concert ticket but aren't sure you can go. What if you could pay a small amount now to reserve it and only buy the ticket if you decide to actually go?

That's what options are in finance. They give you the right, not the obligation, to buy or sell something at a fixed price in the future. That price is called the strike price.

And derivative? It's not calculus. It just means the option's value comes from another asset, like a stock or commodity.

If that asset's price shifts, the option's value does too. Options come in two types, calls and puts. A call option lets you buy an asset at a set price.

Before the expiration date, there's no pressure to do it. A put option lets you sell at the strike price. Same deal.

That's why they're called options. You've got the choice to act or not. It's optional.

Options also come in two flavors, American and European. With American options you can exercise or use them any time before the expiration date, buy or sell when you want. With European options you can only exercise them on the expiration date, no sooner.

Most stock options are American style, so you get that flexibility. There are other types, binary, Asian and so on, but American and European are the ones you'll see most. Let's recap the terms we've seen so far.

American options you can exercise any time before the expiration date. European options only on expiration day. Calls let you buy and puts let you sell at the strike price.

All options are tied to an underlying asset like a stock. Master this jargon and you'll start saying things like "I bought a three-month call for Microsoft with a $450 strike. " Let's say you're a wheat farmer.

Harvest is three months away, and you're worried wheat prices might drop. A big fall in price could really cost you. So, you buy a put option on wheat.

It lets you sell at a fixed strike price. If prices fall below the strike price, it makes sense for you to exercise your option. You sell at the strike price, avoiding a big loss.

If prices climb, you skip the option and take the higher market rate. Make insurance, you pay a small cost up front, the premium, for protection. It's there if you need it, ignored if you don't.

Futures are all about commitment. Unlike options, where you can choose to buy or sell, a futures contract means you must buy or sell the asset at a set price when it expires. That price is called the futures price, not the strike price as with options.

With futures, the trade happens on the expiration date, no backing out. Let's go back to our wheat farmer situation. Instead of a put option, suppose you buy a futures contract on wheat.

This locks in a selling price for your harvest. When the contract expires, you must sell at that futures price and it doesn't matter where the market's at. If prices fall below that, you're protected.

The catch? If prices rise, you still sell at the futures price and miss out on bigger profits. Futures aren't just for wheat, they work in stock markets too.

Take the S&P 500 E-mini futures contract. It tracks the S&P 500 index without you buying all those stocks. Each contract is worth 50 times the index value.

If the index is at 4,000, that's $200,000. You control that much without putting up the full amount. The original S&P 500 futures contract was much larger, each one worth 250 times the index value.

At 4,000 points that's 1 million dollars. The E-mini at 50 times the index is 1 fifth the size. That smaller size made futures trading accessible for more investors, not just the big players.

Here's one more important detail. Mark to market (MTM) accounting. Unlike options, where you settle everything when the option is exercised, futures are adjusted daily.

If prices drop, you lose money that same day. If they rise, you get paid that day. You don't wait until expiration.

Your gains and losses are settled in real time. Every trading day, that means you need cash on hand in what's called a margin account to cover those swings. Do you want to learn more about quantitative finance?

At Socratica. com, we have everything from the basics to the nitty gritty. There's a course too.

With deeper math and tools you can use, you are cordially invited to visit. Options and futures trade on exchanges, but some derivatives don't. They go through the over-the-counter market, OTC for short, where two parties deal directly with no exchange involved.

That lets you customize derivatives in ways you can't on exchanges. The catch? You depend on your counterparty, the other party to follow through.

If they don't, you're stuck. A forward contract is one example. It's the OTC version of a futures contract.

You agree to buy or sell an asset at a set price on a future date. Another OTC derivative is the swap. As the name suggests, you and your counterparty swap something.

But what exactly? That depends on the type of swap. Let's look at the interest rate swap as an example.

Let's say company A has a $100 million loan with a fixed 4. 5% interest rate. Company B has a $100 million loan too, but theirs is floating.

SOFR plus 10 basis points. New terms. SOFR is the secured overnight financing rate, what banks charge each other overnight, and it's the base for floating loans.

One basis point is short for 0. 01%, so 10 basis points is 0. 1%.

Here's the issue. Company A wants a floating rate because they think rates will drop below 4. 5%.

Company B wants a fixed rate for steady costs with no surprises, so they swap interest payments. Company A pays company B, SOFR plus 0. 1%, company B pays company A 4.

5%. They're not swapping the $100 million loans, just the interest. Every payment date, company A sends the current SOFR rate plus 10 basis points to company B, and company B sends 4.

5% to company A. Instead of exchanging the full amounts, they just settle the difference. What happens when rates change?

If SOFR jumps to say 4. 8%, then company A pays 4. 9%, more than the 4.

5% they receive. A loses, and B wins, since B receives more than they pay. If SOFR falls to 3.

7%, company A pays 3. 8%, less than the 4. 5% coming in.

A now wins, and B is stuck paying more than market rates. This is how interest rate swaps work. One company trades fixed rate certainty for floating rate risk, the other does the reverse.

Big players, corporations, banks, hedge funds use swaps to tweak their rate exposure. Sometimes the swap is direct like here, but often banks step in as middlemen, taking a fee of course. There's no free lunch on Wall Street.

Options, futures, forwards, swaps. Four popular derivatives in finance. But there's no limit to what you can build.

Exchanges give you plenty of options and futures, but big banks and hedge funds use the OTC market for forwards and swaps. And if you ever need something truly bespoke, well if you're wealthy enough, there's always someone willing to make a deal. Follow link to Socratica.