For decades, China has been the factory floor of the world. An economic miracle unlike anything in history. It went from impoverished agrarian state to industrial superpower in a single generation.

Over 800 million Chinese climbed out of extreme poverty during this boom. An achievement no other country has come close to. China now produces nearly 1/3 of the world's manufactured goods.

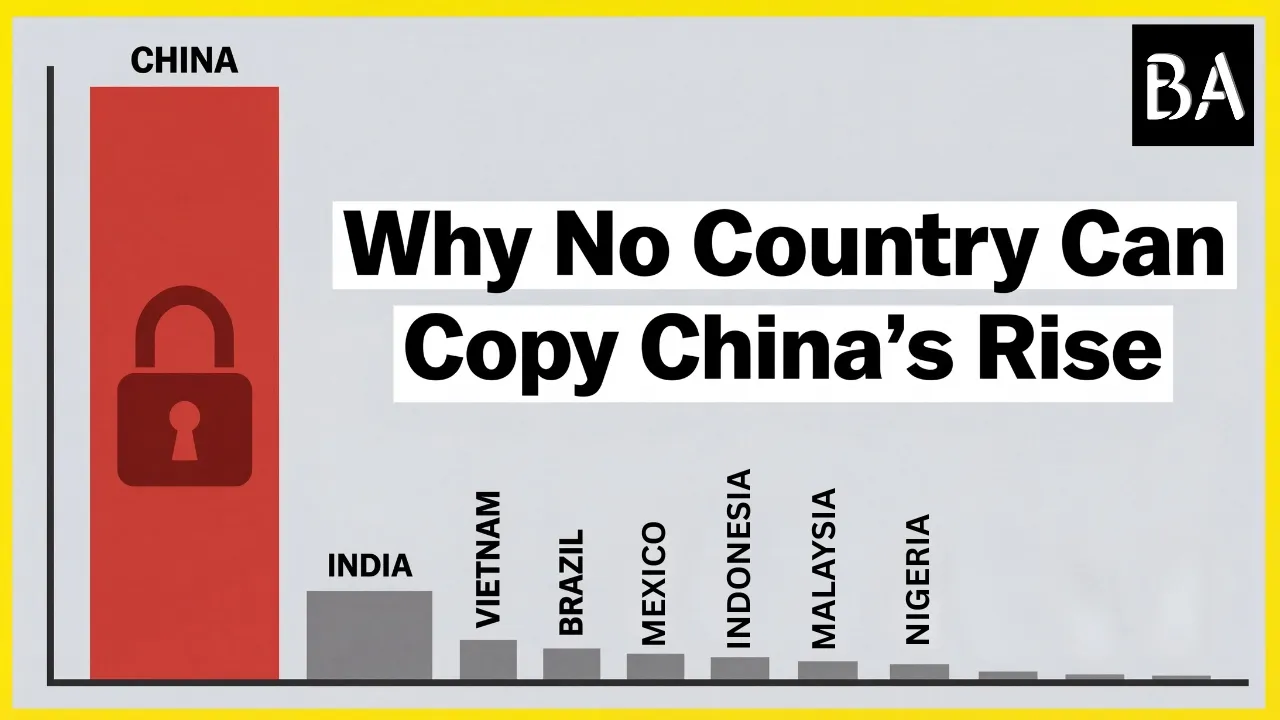

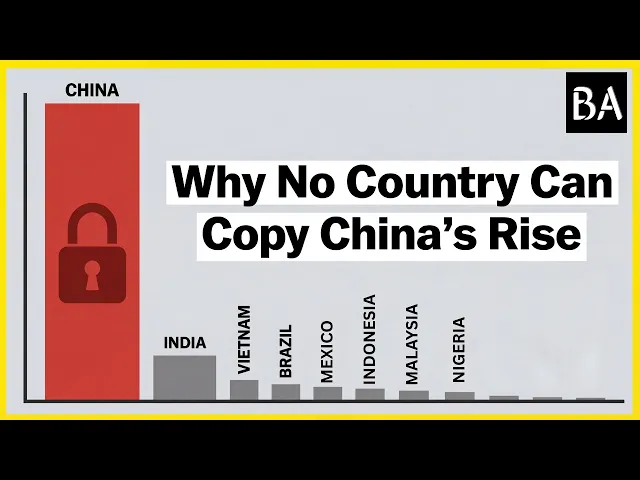

From smartphones to steel. Today, emerging nations from India to Vietnam to Nigeria all hope to copy China's success. The stakes are enormous.

Billions of people seek the same ladder out of poverty that China climbed. But what if that ladder is gone? What if China's economic miracle was a one-time event, never to be repeated?

There will never be another China. The unique formula that powered China's rise, cheap labor, hyper globalization, open western markets, and unrivaled supply chain ecosystems has broken down in the 2020s. No other country, not even giants like India or fast risers like Vietnam can replicate what China did because the world has changed too much.

Let's set the stage. In 1980, China was one of the poorest countries on Earth. Its GDP per person was under $200, a fraction of that in Latin America or Asia's tigers.

China was isolated from the global economy, still recovering from decades of turmoil. Yet by the 2010s, China had become the world's second largest economy and the workshop of the planet. Per capita income surged past $12,000, more than 60 times higher than in 1980.

Over 40 plus years, China's growth averaged nearly 10% annually. Hundreds of millions moved from farms to cities. By 2021, China alone accounted for about 15.

1% of all global exports, up from just 1. 8% in 1990. The scale of this transformation is hard to overstate.

China built worldclass infrastructure, highways, railways, ports. It joined the World Trade Organization in 2001, unleashing a flood of trade and foreign investment. In fact, China's total trade in goods jumped from about $510 billion in 2001 to $4.

1 trillion by 2017 after WTO entry. An 11-fold explosion as global companies rushed in and Chinese exports surged. This export boom turned China into the world's manufacturing superpower.

By 2023, China produced roughly 31 to 32% of all manufacturing output on the planet, more than the United States, Japan, and Germany combined. It's been said that the world's factory moved to China, and for good reason. Everything from t-shirts to smartphones started carrying the label made in China.

Crucially, this manufacturing growth lifted an unprecedented number of people out of poverty. Over 40 years, close to 800 million Chinese escaped extreme poverty, defined as living under $2. 15 a day.

That represents threearters of all the people worldwide who moved above extreme poverty during that period. In human terms, China's rise meant better jobs, higher incomes, and improved lives on a massive scale. The very outcome every developing nation craves.

Little wonder then that dozens of countries have tried to emulate China's model. From India launching its make in India campaign to African nations courting factories to Southeast Asian neighbors expanding exports, the dream has been to become the next China. The ladder China climbed export-led industrialization seemed like a proven path out of poverty into prosperity.

But here's the problem. That ladder may now be broken. To understand why, we first need to examine how the ladder was built in the first place.

What unique origins and mechanisms enabled China's meteoric rise? Only then can we see why no one else can climb it the same way? How did China do it?

It turns out China's takeoff was not due to any single magic ingredient, but a combination of historical conditions that lined up just right. Think of it like a recipe. Leave out any key ingredient, and the result might have been very different.

Let's break down the core pillars that powered China's rise. First, demographics. China entered its growth era with a workforce of staggering size.

In the 1980s and 90s, hundreds of millions of people were entering the labor force. Between 1982 and 2015, China's working age population swelled from about 600 million to 1 billion people. That is an extra 400 million workers added in just over three decades.

This army of labor, young, able-bodied, and eager, provided manpower at an unprecedented scale. With GDP per capita under $200 at the start, wages were extremely low, making China hyperco competitive. Millions of rural Chinese migrated to factory zones along the coast, filling assembly lines for very little pay.

But crucially, it wasn't just about quantity. Over time, it became about quality. High literacy rates and investments in basic education meant that this cheap labor force could learn new skills quickly.

Unlike India, which historically struggled with literacy, or Vietnam, which lacked the sheer population scale, China uniquely combined size with basic skills. This cheap, capable labor was the spark that ignited the engine. The second pillar was timing.

China's rise coincided with the era of hyper globalization. The Cold War had ended. Trade barriers were falling and multinational companies were eagerly looking to offshore production.

In this climate, Western markets flung their doors open to Chinese exports. The turning point was China's entry into the World Trade Organization in 2001. This allowed China to ship goods to rich consumer markets with minimal tariffs.

Once inside the WTO, global demand for Chinese goods exploded. From 2001 to 2006, China's exports grew at an astonishing rate of about 30% per year. Western companies shifted production to Chinese factories, and Western consumers fueled the growth by buying those products by the container load.

By flooding Walmart, Target, and global supply chains with inexpensive goods, China's factories found nearly insatiable demand. It was a perfect moment in history, a time of free trade optimism that gave China an opportunity no other country may ever get again, especially as protectionism rises today. However, cheap labor and foreign demand wouldn't have mattered if China couldn't actually produce and deliver the goods.

This leads to the third pillar, policy and infrastructure. The Chinese state built a launchpad. Starting with Deng Xiaoings reforms, the leadership made a strategic decision to become a manufacturing superpower.

They established special economic zones like Shenzhen, offering tax breaks, cheap land, and streamlined regulations to attract foreign investors. Simultaneously, the state poured investment into the physical backbone of the economy. They built power plants, highways, railroads, and mega ports at breakneck speed.

Today, six of the world's 10 busiest container ports are in China. This infrastructure meant that a product could be manufactured inland and transported to a port efficiently. While other emerging economies struggled with patchy power grids or poor roads, China offered an unbeatable package.

Endless labor plus reliable infrastructure plus pro-investment policies. The government created a stable, if rigid, environment where factories could operate at massive scale without the logistical bottlenecks found elsewhere. The final and perhaps most unique pillar is supply chain clustering.

As China's industrial base grew, it reached a critical mass where entire ecosystems were located in country. In regions like the Pearl River Delta, you could find not just the final assembly plant, but every conceivable supplier of parts and components within a short drive. This clustering dramatically lowered costs and sped up production.

If a company needs a specific screw, a custom plastic mold, or a microchip, the supplier is likely down the road rather than across the ocean. This is why an iPhone can be assembled in mere days. China now produces the vast majority of the world's smartphones and computers because it dominates these supply chains end to end.

This created a cycle of increasing returns. Success bred more success. Once China became the one-stop shop for manufacturing, it became incredibly difficult for any other location to compete.

This was the ladder. Start at low-end manufacturing, leverage global markets, build infrastructure, and climb to the high end. It seemed like the ultimate playbook.

But even as China reached its manufacturing apex, the ground began to shift. The perfect historical conditions that allowed for this miracle was starting to evaporate. To understand why the future looks different, we have to look at how these pillars are beginning to crack.

Around the mid2010s, a plot twist emerged in our story. The very factors that had turbocharged China's rise began to shift into reverse, creating a scenario where the ladder that once lifted millions started cracking under new weight. The first major shift was the end of endless cheap labor.

After decades of growth, the limitless pool of young workers dried up as the population aged and birth rates fell. China reached the Lewis turning point, a critical economic threshold where surplus labor runs out and wages sore. Between 2005 and 2016, manufacturing wages in China tripled, eventually surpassing those in Mexico and Brazil.

By the late 2010s, the average Chinese factory worker earned more than their counterparts in many Latin American countries. While this was excellent for Chinese living standards, it meant the country was no longer the default lowcost producer for basic goods. Simultaneously, globalization hit a wall.

The political winds in the west changed and the openness China once exploited began to close. The shock of China's rapid rise fueled a populist backlash in the US and Europe, leading to a dramatic shift toward protectionism. The United States launched a trade war in 2018, slapping tariffs on hundreds of billions of dollars of Chinese goods.

Overnight, exports faced steep levies, eroding their price advantage. Beyond tariffs, western governments grew wary of over reliance on China, implementing policies like the chips act to reshore production. The era of hyper globalization peaked and began unwinding.

For any country hoping to emulate China's export-led path, this is a crisis. The welcoming western import markets of the 2000s have been replaced by skepticism and trade barriers. Perhaps the most profound turn of all has been technological.

China's model relied on massive numbers of lowcost workers assembling goods. But robots and automation have fundamentally changed the equation. The cost of industrial robots has fallen while their capabilities have risen, leading to record-breaking installation numbers worldwide.

Crucially, the labor cost advantage of developing nations matters much less now. A robot arm does not care if wages are lower in Ethiopia. It can assemble widgets continuously without a paycheck.

Even in China, companies like Foxcon have replaced tens of thousands of workers with machines to offset rising costs. This creates a new reality where the rungs of the development ladder have been kicked away. You cannot employ millions of unskilled factory workers if the factories of the future only need a few technicians and a lot of machines.

As economist Danny Rodrik warns, many developing nations are now experiencing premature de-industrialization, losing manufacturing jobs without getting rich first. The main escalator for economic convergence is grinding to a halt far earlier than it did for the West or for China. By the 2020s, the game board had flipped.

China's GDP growth decelerated, global trade fractured, and technology rewrote the rules of manufacturing. It is not that other countries failed to learn from China, but rather that the environment of the 2020s is far less forgiving. The old export-led growth model is faltering, and aspiring economies are hitting walls that China never had to face.

Let's examine how the broken ladder is playing out in real time. No other country has managed to recreate China's manufacturing magic so far, and the trends we have discussed explain why. In this part, we will highlight a few key consequences of this changed landscape and compare how different countries are weathering the storm.

The first major consequence is a shift from manufacturing booms to stagnation. Despite many attempts, most developing countries have not seen industry take off the way it did in East Asia. In fact, in parts of Latin America and Africa, manufacturing is shrinking before nations ever fully industrialize.

A phenomenon economists call premature de-industrialization. Mexico, however, presents a different but equally troubling warning, the productivity paradox. Positioned next to the United States and armed with the NAFTA free trade agreement, Mexico seemed destined to become an export powerhouse.

While factories did move there, the outcome has been underwhelming. The manufacturing sector remained an enclave that didn't enrich the broader population as hoped. A McKenzie study noted that Mexico's economywide productivity barely budged because a modern manufacturing sector coexists with a much larger traditional sector that employs most people.

In Mexico, millions ended up in low-wage services or informal work despite the factories. This is the face of the broken ladder. Even with access to the US market, Mexico couldn't replicate China's broad income explosion.

India is another case often touted as the next China. It has a huge population now surpassing China's and rising wages in East Asia made India look attractive to labor intensive industries. The government launched make in India in 2014 explicitly aiming to raise manufacturing to 25% of GDP by 2022 but they missed that target significantly.

By 2022 manufacturing was still hovering around 15% of India's GDP actually slightly lower than before. Despite ambitions the sector has struggled to expand because the business environment and infrastructure remain challenging. Power outages, congested ports, and bureaucratic red tape persist.

A World Bank report noted that India hasn't yet made the necessary leap in investment and technology infusion to get manufacturing roaring. Critically, the world isn't as open as when China rose. India faces competition from robots and skepticism from trade partners.

The difference is stark. China had seamless logistics and a culture of long-term planning. Whereas India often struggles with opaque regulations and hidden costs.

This makes it incredibly difficult to follow China's playbook. Today, India's case underscores another broken rung. Development can no longer rely on endless low-skll factory jobs.

Today, India's labor cost is lower than China's, but that alone isn't drawing a tidal wave of factories. Many industries have alternatives such as automation or require reliable power and supplier networks that cheap labor cannot offset. Without the ecosystem and skills, cheap labor by itself isn't enough to spark a boom.

In the past, countries had time to develop those skills through gradual industrialization. Now, global firms don't have the patience to train an unskilled workforce from scratch when they can use machines or stick with China's established base. Even China itself is struggling to climb further.

The story isn't over, but the country is now facing the notorious middle income trap. After raising incomes dramatically, growth often slows and countries struggle to reach rich nation status. China is nearing that critical income threshold.

Yet growth has cooled and heavy industry-ledd expansion is waning. The government is trying to pivot to innovation and domestic consumption. But the new global context makes it tough.

Export growth isn't what it used to be. Geopolitical tensions are cutting off access to advanced technology like semiconductors and an aging population is straining the workforce. The World Bank has warned that more than 100 countries including China and India face serious obstacles to becoming highincome nations.

Since 1990, only 34 middle-income economies managed to make the leap, often due to special circumstances like EU integration or oil discoveries. If even China is finding the last rungs of the ladder shaky, it is easy to see how hard it is for countries still at the bottom. As Western companies respond to geopolitical pressures, supply chains are diversifying, but no one is filling China's shoes completely.

The China plus one strategy is creating winners like Vietnam, Bangladesh, and Mexico. But these nations are capturing only pieces of China's former dominance. Vietnam has become a major assembly hub for electronics and Bangladesh is a titan in garment exports but neither has the capacity to replace China outright.

Companies are scattering production among multiple loces to spread risk. There will likely never be another China because the conditions giving rise to its prowess were unique. Instead of one massive successor, we have many smaller mini China, each with partial advantages but significant limitations.

Vietnam, for example, is 1/14th the population of China and is already nearing full employment in many sectors, facing rising wages and port congestion. Mexico has seen a surge in nearshoring investment, but it faces security concerns and a skills gap. India has the workforce but lacks the infrastructure.

The bottom line is that the manufacturing leaving China is being spread thin. Perhaps the most profound consequence is that the ladder of development itself is in question. For two centuries, the playbook was to industrialize, export, and get rich.

Now, developing nations are hitting a ceiling where manufacturing peaks at a much lower share of employment than it did for earlier powers. If automation allows a giant factory to run with 200 workers instead of 2,000, building industry won't absorb labor the way it once did. The risk is a future where developing countries stagnate in agriculture or low-level services, creating a recipe for persistent global inequality.

The manufacturing first path is much narrower than before. We have painted a challenging picture. The straightforward road that China traveled does not lie open for the next in line.

So, what can the next wave of developing nations do? How can they build prosperity in the 2020s and beyond? Think of it not as a single ladder but as a maze or a rock wall where countries must find different handholds to climb.

One emerging strategy is to focus on investment, infusion and innovation. The World Bank suggests that very poor countries must first focus on basic investment in infrastructure and education. Once they reach lower middle income, they should pivot to infusing technology, adopting and absorbing existing tech from advanced countries.

Finally, by upper middle income, they must shift to innovation. This is a more nuanced playbook than simply opening factories. It means countries like Bangladesh should continue building foundations while diversifying manufacturing via foreign tech, laying the groundwork for future local R&D.

It is about climbing a broken ladder by building new rungs as you go. Another clear lesson is that cheap labor alone is insufficient. Countries need to develop labor value, a workforce that is skilled and adaptable.

This requires major investments in technical education and vocational training. China's later advantage wasn't just low wages, but a disciplined, experienced workforce of engineers. Countries like Vietnam and Malaysia are emphasizing technical education to climb the value chain, moving from shirts to smartphones.

The new mantra is to compete on productivity and quality, not just price. If automation is inevitable, being the country that can design, maintain, and integrate automation is key. Several developing nations are establishing technology parks and codingmies, recognizing that brain power might succeed where muscle power no longer can.

Developing nations must also look inward. The old model was externally driven, making goods for the rich world. The new reality suggests countries must grow by serving themselves and their neighbors.

China pivoted to rely more on domestic consumption after 2008 and others may need to follow suit. India's huge population could be a source of demand to drive growth, producing affordable goods for its own emerging middle class. Regional trade blocks like the African continental free trade area aim to create integrated markets so industries can scale up by selling to nearby countries.

The idea is to reduce reliance on temperamental western markets by developing south south trade and robust internal demand. Finally, governments may need to reconsider social policies. If the private sector won't create tens of millions of manufacturing jobs, governments might have to be more proactive.

Ideas like public works programs, universal basic incomes, or support for the informal sector are gaining traction. Developing countries must navigate an economic transformation while ensuring their populations don't lose hope. This means investing in health, education, and social protection so people are resilient enough to seize whatever new opportunities arise.

The challenges are enormous and the broken ladder means there is no simple path to prosperity. But human ingenuity is vast. Countries are experimenting and adjusting.

Vietnam's rapid development, Costa Rica's success in medical devices, and Ethiopia's early gains in light manufacturing show that climbing is still possible. The climb may be slower and require more agility, a mix of manufacturing, services, and innovation rather than one big export juggernaut. Ultimately, developing nations must play a more complex game than China did.

They need to simultaneously invest in people, attract selective industries, embrace technology, and guard against risks like climate change. It is tougher, but not impossible.

![[WKF2024] The End of China's Rise and the Future of World Order](https://img.youtube.com/vi/IL6OHMr21f8/mqdefault.jpg)