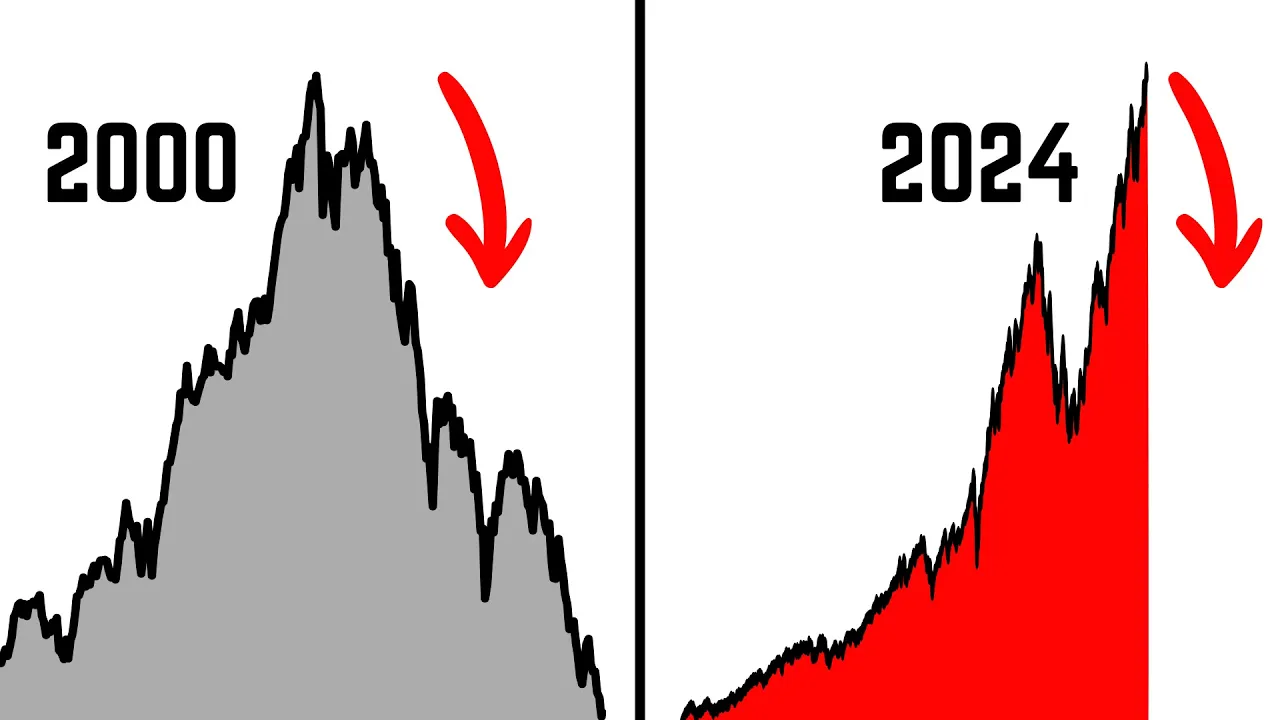

between 1995 and 1999 the NASDAQ 100 the US Technology stock market index doubled in price every 2 years now these kinds of returns might look absurd but believe it or not this is not that different from the returns that we've seen on the NASDAQ 100 more recently since its bottom in late 2022 the NASDAQ 100 has made a 100% return doubling in price in fact when we copy and paste the price action from the late 1990s onto the last 2 years worth of price action we see that they're actually quite a close match the only

difference of course being that the NASDAQ 100 sustained these gains for multiple additional years in the late 1990s but we shouldn't be dismissing the idea of the NASDAQ 100 being able to sustain another melt up like this today while the 1990s bubble was fueled by optimism around the internet today's Technology stock market melt up has been fueled by optimism around artificial intelligence a theme that is just as real and just as as revolutionary as the internet was back then so is this what's waiting for us on us technology stocks in which case we should really

be going all in on this sector well on a valuation basis the NASDAQ 100 is about as expensive today as it was in October of 1998 which was definitely much closer to the end of the Doom bubble than it was to the beginning but from that point on the NASDAQ 100 still climbed another 234 before making its final Peak and we can see that on this chart that shows us what's called the PE ratio of the NASDAQ 100 this is a way for us to gauge how expensive this index is at any given point in

time and the current PE ratio of around 30 has only really been seen during the Mania of the dotom bubble in the late 1990s and early 2000s this right here was October of 1998 in fact when we compare this to the PE ratio of the rest of the US Stock Market using the S&P 500's PE ratio we see that there is a similar Gap developing between the valuation of technology stocks and the rest of the market to what we were seeing in the late 1990s now this Gap right here is what a lot of experts

point to to justify having a negative outlook on tech stocks because not only are tech stocks expensive relative to history they're also expensive relative to the rest of the market but the truth is when you look at the late 1990s the Gap got significantly bigger than it is today this is what can happen when narratives like the internet or artificial intelligence take hold of the market there's really no telling how big this Gap can get if you know a little bit about how Market psychology works it can be dangerous when the market begins to get

too complacent like this this can lead to a situation where the pricing of the market begins to diverge away from the fundamental reality of the situation this is exactly what you call a bubble and it's very typically fueled by widespread viral narratives and right now we're definitely seeing some of that with the technology sector in the United States this chart for example shows us something called long-term earnings expectations of technology stocks now that may sound a bit complicated but it's basically showing us how high the earnings expectations of Wall Street analysts are on technology stocks

looking out 5 years so for example you can see here in the late 1990s Wall Street analysts were forecasting that the technology sector was going to grow by 30% each year over the next 5 years that would have been absolutely m massive growth over a 5-year period 30% growth is something that the market even rarely achieves within just one year let alone five then once the dot bubble blew up these expectations came back down to more reasonable levels at around 133% now today look at how much growth analysts are forecasting again they're expecting the technology

sector's earnings to grow by 25% per year over the next 5 years again this is an absurdly high amount of growth and in our opinion it's very unlikely that this actually materializes so yes we are beginning to see signs that the tech sector is disconnecting from the underlying fundamental reality but as George Soros famously said when I see a bubble forming I rush in to buy adding fuel to the fire so shouldn't this be our approach to today's AI Tech narrative if you can't fight it join it well to answer that we need to look

at this chart right here this is a chart showing us the performance of the NASDAQ 100 index against the S&P 500 index over time and as you can see from this chart since the Inception of the NASDAQ 100 index we've seen it outperform the rest of the market by a staggering 400% and just since 2002 Tech has outperformed the S&P 500 by 230% and it's done so in a very consistent manner so yes having exposure to tech stocks has been a fantastic way to outperform the stock market and could very much continue to be so

over the next few months now if we zoom in on the last couple of years worth of price action we see the performance of tech stocks hasn't been all that impressive while they did outperformed the market significantly in early 2023 right after the release of chat GPT that fueling this initial wave of optimism around AI but since June of 2023 we've had tax performance really stagnate against the rest of the market to some this can be interpreted as a topping process with technology stocks ready to collapse under their own weight and finally revert back to

reality but to others this is the tech sector setting up a base to move up higher and continue its euphoric performance and we can rewind to 1999 to give a similar example after a big run up in late 1998 early 1999 the tax sector stagnated and Consolidated for almost a full year before simply resuming its outperformance heading into 2000 and this is actually what we've communicated to our clients today while we've been mostly new neutral on the performance of Technology stock since 2023 this most recent move that we've seen on tech stocks could be suggesting

that these technology companies are once again ready to outperform look at what happens when we add key moving averages on top of this chart over the last few months they began to Cluster together very tightly and as that was happening the technology sector began to form a base if you know a little bit about technical analysis you'll know this is quite a bullish development especially if it's followed by a breakout which is exactly what we saw last week so we have flipped to bullish on technology stocks at Bravo's research which is why we're currently actively

scanning for long trades on the technology sector to add fuel to the fire and we do already have a long trade on Amazon for example that's already up over 15% now we're also closely watching this ratio because if it comes back below the moving averages that starts to look a little bit more worrying the flexibility in our Outlook is a Cornerstone of our trade in strategy at braavos we're going to be closing the year having done about 104 trades in 2024 at braavos research.com 68 wins 36 losses if you want to be on top of

markets in 2025 make sure to grab yourself a subscription to our service