Welcome students. So, in the process of discussing the accounting principles, till last part of discussion, we talked about the accounting concepts, we discussed 10 accounting concepts and now we will be moving forward and talking about discussing the accounting conventions. So, apart from the 10 concepts of accounting we have the 4 conventions of accounting.

. And these 4 conventions are given here that is convention of consistency, convention of disclosure, convention of conservatism that is prudence and convention of materiality these are the 4 conventions which are also to be taken along with the accounting concepts. So, these 4 conventions which we call as the traditions also traditions of accounting, we follow; we observe these traditions while recording the business transactions in the books of business or the books of accounts.

So, the first convention; first tradition is that is the convention of consistency. When we talk about the convention of consistency or consistency in maintaining the business records, we normally say remain consistent in every respect and we do not change the processes of the business or may be the methods of recording the business transactions and if we are following one method of recording the business transactions into the or the transaction of the business into the books of accounts, we will continue following the same method and we do not change it. So, when we talk about the consistency, we will be talking here about say certain important things that how we maintain the consistency in the business or in the business processes or recording of the business transactions and then drawing the profit or loss and say knowing about the financial position of the business.

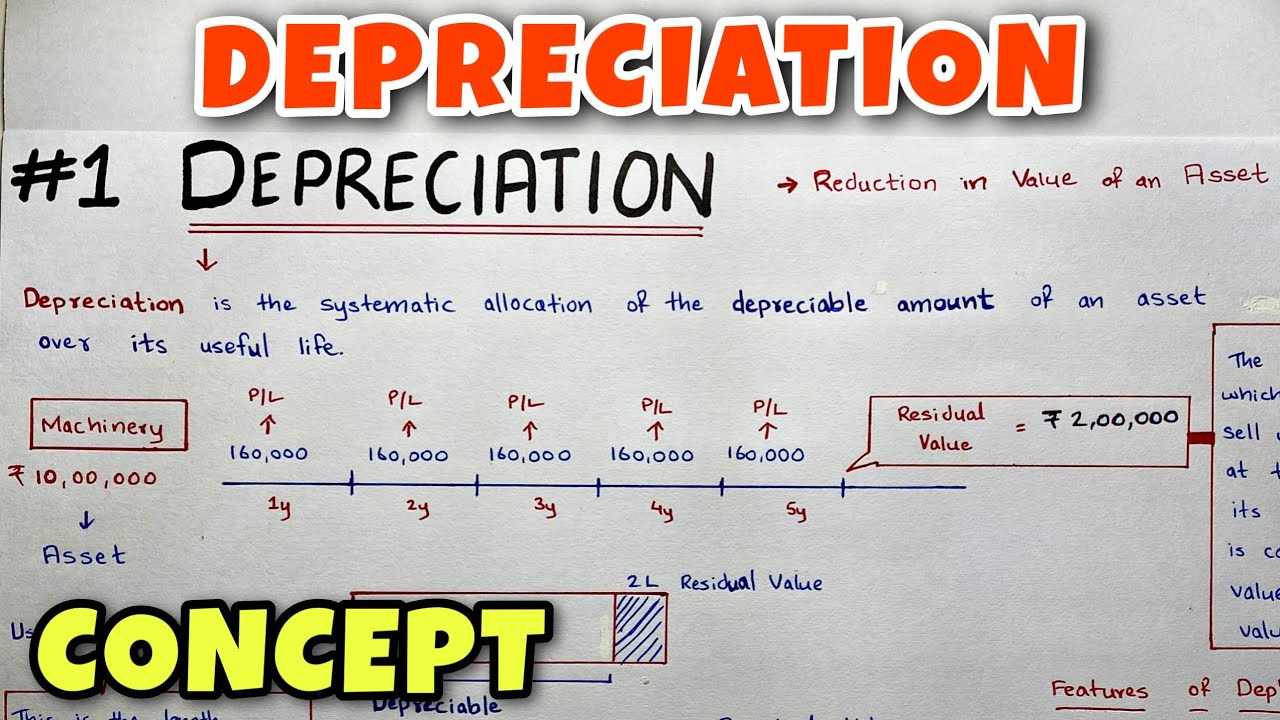

. In that case, say when you talk about the consistency, if you take here the example of one process that is called as depreciation. Depreciation is as I think you must be knowing about that it is basically the reduction in the value of any asset because of the wear and tear or may be because of the use of that asset.

So, when you say use any asset we have to record the depreciation in the books of accounts of the business, we have number of methods for that and normally there are 10 methods of recording or calculating the depreciation and then recording that depreciation in the books of accounts and charging against a particular asset. But in the now a practice we used 2 methods that is one method is that is the fixed installment method or you call it as the straight line method; fixed installment or the straight line method which we normally use and we call it as SLM and second method is the diminishing balance method DBM. So, these are the 2 important methods which are normally in vogue or which are normally used in the say businesses for recording the depreciation or maybe say charging the depreciation and then working out the amount of the depreciation.

So, as per the convention of consistency, what is required that if we are following one method of calculating the depreciation, for any asset or any anything means which is being used in the business on the long term basis. So, in that case, if we are following the; we have started in the first year of the business, we have started following or charging depreciation as per the straight line method of calculating depreciation. We will continue following the same method over the number of years in future also and we will not change the method all of sudden or without any reason.

Because say if in one year we charge the depreciation as per the straight line method and in the second year we charge the depreciation under the diminishing balance method or may be the another name of the diminishing balance method is that is the written down value method also. So, if we written down value method also WDV method. So, which we charge the depreciation in the first year under the straight line method and in the second year, we convert that change the method and we start charging it under the written down value method, it means we are not maintaining the convention of consistency.

So, what will happen? Normally the value of depreciation will be same at the end of the say life of the asset, we will be calculating the same amount of depreciation and the residual of value of the asset will also be same, but over the years the value of the depreciation will be changing and if we are frequently changing the methods of charging depreciation then in that case, we are not maintaining the consistency and in that case means the profit and loss of the business cannot be calculated correctly over the years may be at the end of the say life of a one particular asset the profit and loss will not be affected, but annually it will be affected because amount of the depreciation will change. So, you will have to maintain the consistency not in depreciation, but in all the methods of a say recording the transactions in the books of accounts, posting them into the ledger, then say preparing the trial balance and then preparing the profit and loss account and balance sheet.

So, whatever the process we are following, whatever the method we are following, we will have to observe that we will have to continue observing that and we should not change it because if we are changing it we are not say observing or following the convention or the tradition of the consistency. So, this is the convention of consistency means we will continue to follow the one method of accounting or maybe the one method of say charging any particular income or expenditure or may be recording asset or liability in the books of accounts and we will not change the method, this is the convention of consistency. Second convention is the convention of disclosure under the first convention that is under the convention of consistency as I told you that normally, we will not change the method of depreciation say for example, we are talking about depreciation, but because of certain reasons if we are required to change the method of charging depreciation then we can do that, but if we are doing it in any special year or in any particular year in that case we will have to disclose that.

Means when you are preparing the profit and loss account and where you are showing the profit and loss account related information and there in the profit and loss account we are showing the amount of depreciation then we will have to. . Say for example, this is your profit and loss account and we are showing somewhere here that say for example, to depreciation we are showing here to depreciation and this amount of the depreciation is different as compared to the previous year, it means if anybody who does not know that there is a change of the method in the depreciation he will not be able to understand why there is a change in the value of the depreciation being shown in the profit and loss account of this year.

So, what we have to do is that we have to put a line here and then at the end of that statement, we will have to give a note and in this note, we will have to disclose that in this particular year because of the change of the method of depreciation because of this reason the amount of the depreciation worked out and shown in the profit and loss account debit side is little different as compared to the amount of depreciation in the previous year. So, because of the change in the method of depreciation the amount is different and the reason why the method of depreciation has been changed from the previous years to this year that has to be given. If you are not disclosing it means if any third person who is not aware about this particular change, he will not be able to understand that why this value of the depreciation is coming up because when we talk about the straight line method of charging the depreciation.

Under this method of depreciation, the value of or the amount of the depreciation remains the same all through the years for example, there is 10,000 rupees and the life of the asset is 10. So, it means in all the ten years we will be showing the amount of depreciation as 10,000 rupees it will remain straight it will not be changing. So, it means in one year if it is 10,000 and next year we change the method from the straight line method to the written down value method and the amount of depreciation has changed.

So, we will have to disclose it that why there is a change and that has to be disclosed on the same page by drawing a line here on the bottom of the page and we will have to mention that there is a change in the method of depreciation because of that there is a change in the value of depreciation and why the method of depreciation has been changed. So, that is a convention of disclosure. Then we talk about the convention of conservatism or prudence, when we talk about the convention of conservatism or prudence means we would like to be conservative in the in recording the affairs of the business.

What do we mean by the conservatism here? That conservatism may be defined in terms of the profit or loss to the business if we talk about the profit and we are sure that in the given period of time or at the end of a given period of time the business is going to earn the profit or because of any special transaction or a particular transaction if the business is going to earn the profits, but that profit is not yet earned by yes and we are not sure, but we can say that yes 99. 9 percent we will be say earning the profit at the end of this transaction, but we will not claim that until and unless the profit is earned.

But if the reverse is going to happen that we are going to incur a loss. So, maybe loss has also not happened now and it is expected to happen in future, but about that loss, we will be more sure about we will say that this loss is going to happen to the business and if this loss happens to the business, what would be the end result and how this loss will be affecting the business. So, it means ignoring the potential profits, but seriously taking into account the potential losses that is called as the convention of conservatism or the prudence we would like to remain prudent, we would like to remain conservative about the affairs of the business that any potential profit we will not recognize until and unless that profit has really been earned.

But if any expected loss if it is going to happen or expected to happen in future we would expect that this loss will happen to the business and if this loss happens what would be the effect of this particular loss to the business. So, that is called as the convention of conservatism that not recognizing any potential profits not recognizing the potential losses and would remain conservative. We would remain all through the business transactions recording and preparing the financial statements prudent.

So, that if the profit happens then business is going to gain out of it, but if that, but we are not recognized that the profit will happen and we have not taken the note of that profit anywhere in any part or any books of accounts, but if the loss is not recognized and if the loss happens in future then it is very difficult for the business to manage that loss. So, what we have to do is always expect and recognize that if any potential loss is there recognize it, but if any potential profit is expected do not recognize it. And then the last convention 4th convention is the convention of materiality convention of materiality says or the tradition of materiality says that we will not record any transaction maybe it has a monetary value, but the monetary value should be a value of a size a value of a material.

Means for example, now we take talk about one thing say we talk about stationery and when you buy stationery we have number of things to be categorized under stationery. . So, one fine morning we can buy some pens for the business, then we can buy some pencils, then we can buy a paper or we can buy some other stationery items.

So, in this case, when we are incurring the expenditure on account, the pen pencil, paper or paperweight or anything any kind of things, we will not be recording them means as the individual transaction that we brought the pens for say 100 rupees and we are recording the transaction in the business that is not normally advised. Similarly, pencils, papers so what we do is to convert these small expenses, petty expenses into the material expense, we will call this expense and they will they will count all these expenses under one single head and that head will be called as stationery. So, stationery will be the item which is of the material used to us and the material recognition to us and not the individual items.

So, it means whatever is going to be recorded in the books of accounts that must be of the material value of a significant value material value means that should be of a significant value and that is done with the objective of minimizing the transactions to be recorded in the books of accounts. If you record all the transactions pertaining to pen, pencil, paper everything it means that with the number of transactions will be. So, much that ultimately means it will be very difficult for the business to control these transactions record and then to work out the actual effect of that.

Whereas if you convert them into the material transactions in that case it will come down to some sizeable number of transactions; they can be easily recorded in the books of accounts and can be taken to the respective places and the effect on the profit and loss can be seen. So, these are the 4 conventions these are the 4 traditions of accounting which we normally follow when we prepare the books of accounts and we record the transactions in the books of accounts. We follow 10 concepts of accounting and 4 conventions or traditions of accounting and we are following these concepts and conventions, we means are in the process of following GAAP generally accepted accounting principles these concepts and conventions are called as accounting principles and we are following these concepts and conventions we make these accounts or the books of accounts or financial statements easily understandable commonly readable by all maybe the internal stakeholders or external stakeholders everybody reads the books of accounts.

In the same sense, in the same meaning, in the same manner because it follows a GAAP that is generally accepted accounting principles the meaning of which means these accounting principles concepts and conventions they remain conveyed to all in the same sense. So, there is no problem in communicating with the external stakeholders also by the internal stakeholders or with the external stakeholders that kind of the say communication is not difficult. So, this is in a way you can call it as the accounting language also.

Accounting principles are the accounting language also. So, that everybody understands this language in the same spirit, in the same motive, in the same way, in the same manner. Up to now these conventions of 4 conventions of accounting; we will be moving forward with the next part.

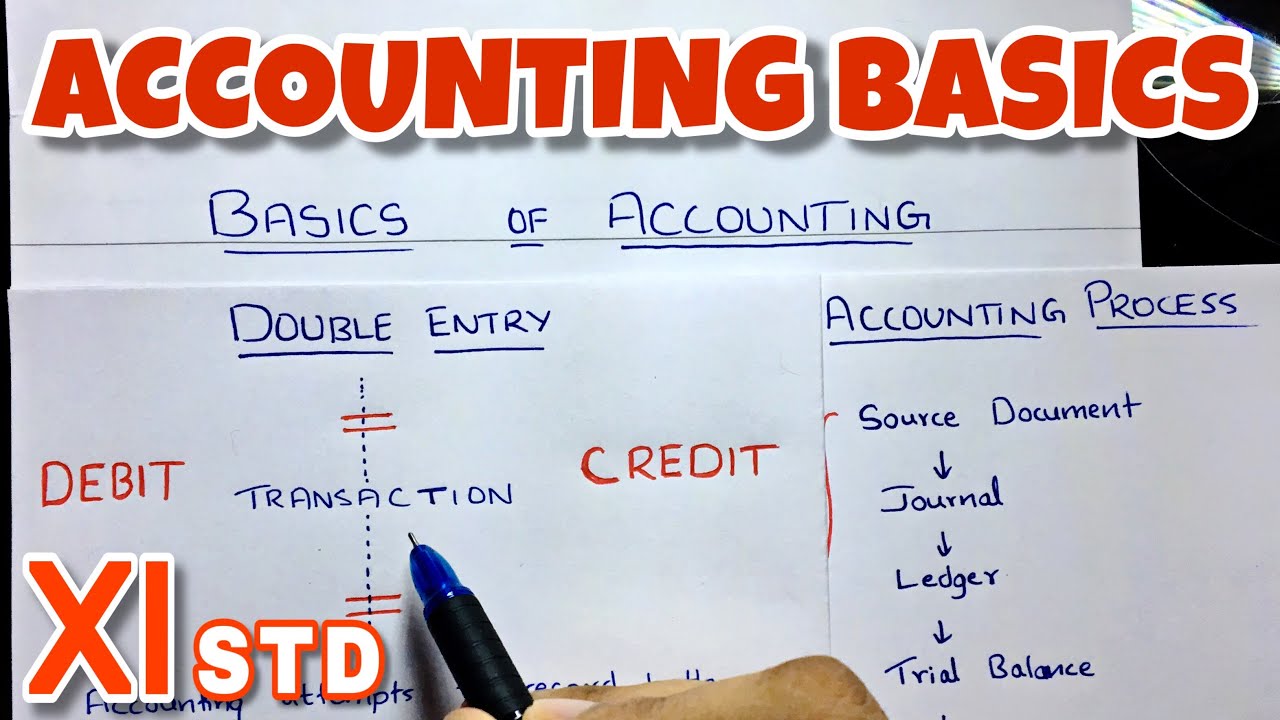

. And now we will be talking clearly about the accounting process. So, after the principles of accounting, next thing in the GAAP is that is the accounting process and when we talk about the accounting process here we have certain steps to follow to complete the accounting process.

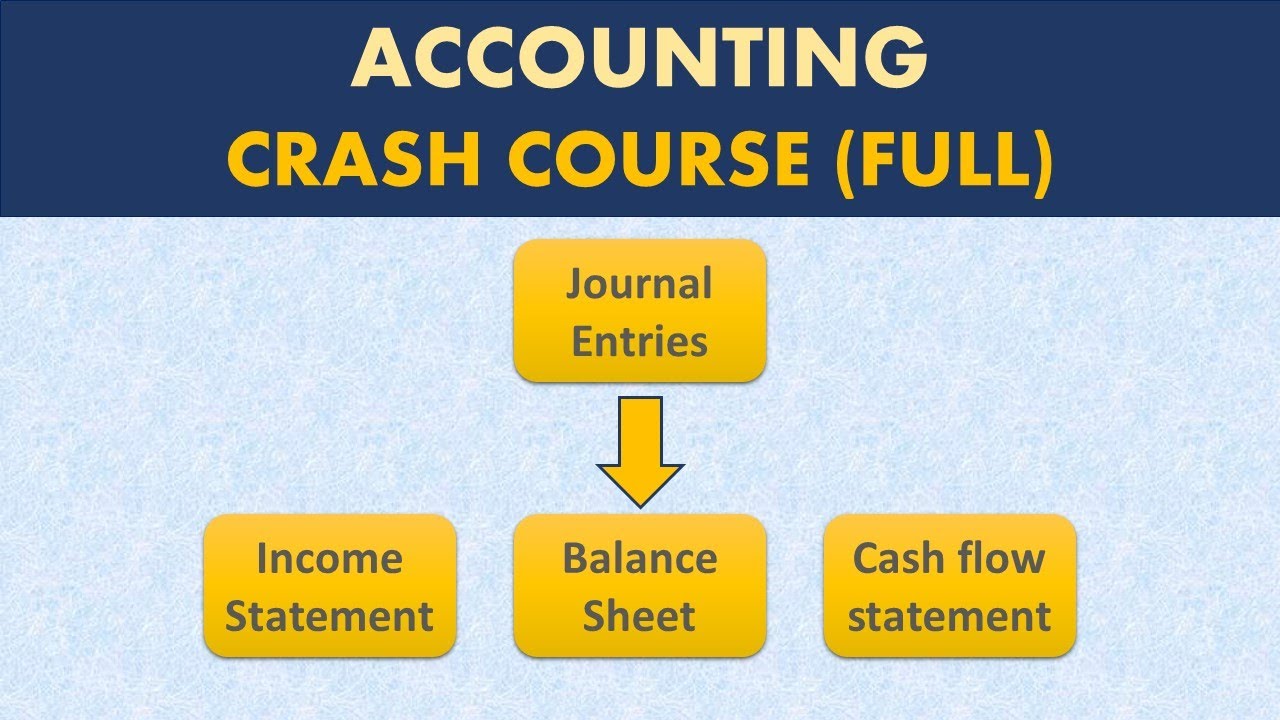

If we look at these all the steps given here we have first step in the accounting process is that we have the transaction here, then second step is the journal third is the ledger, 4th is the trial balance, then preparing the first statement that is called as income statement that is the profit or profit and loss account and then the balance sheet. So, this means the accounting process starts with transaction and ends up with the balance sheet. So, these are the different steps 6 steps we have to complete while completing the accounting process.

And apart from the profit and loss account and balance sheet, there is a third statement also that is called as the cash flow statement which is now mandatory statement; important statement. So, first we will be learning about preparing the balance sheet, income statement and balance sheet and then we will be talking about the third statement that is a cash flow statement. So, now, let us discuss before we move into practically preparing the balance sheet and profit and loss account let us try to understand theoretically here that what are the steps involved in the accounting process.

Here we say that the first step in the accounting process is the transaction means when any business starts its operations any business starts its operations, what happens? Transactions start taking place and those transactions because of which funds are moving in or going out means which have the monetary value those transactions are of use to us as far as the accounting process is concerned. So, any transaction business is making for example, business purchased raw material and because of raw material for 1000 rupees.

So, it means in that case 1000 rupees is spent and the raw material is purchased now that raw material is an expense will have a far reaching effect of all the profitability of the business because it is an expense will be taken to the profit and loss account. So, that is a transaction. After that we paid wages to the workers working on the plant maybe in the evening same day we are paying the wages.

So, in the evening we means did one transaction payment of the wages to the people working in the plant that is again a transaction. So, all these transactions means ultimately the business is what it is a bunch of transactions and all these transactions having a monetary value the impact upon the profit and loss position of the business as well as the financial position of the business. So, it means first thing in the accounting is that we have to recognize we have to identify all the transactions which are happening and those transactions will be identified and process of the accounting will begin with the recognition of those transactions.

Once these transactions are with us then the next step; second step is recording these transactions in the first of the original book of accounting which is called as journal first or original book of accounting is called as journal. . So, we will have to record these transactions in the journal this is called as the first book of accounting or the original book of accounting.

So, these transactions are first recorded and then from the journal these transaction move to the next book of accounting which is called as ledger. Now, what is the difference between the journal and ledger? If we are recording the transactions in the first book of account that is journal then why we are shifting these transactions from the journal to the ledger.

The basic difference between these 2 books of accounts is that in journal all the transactions are recorded in the chronological order. Chronological order means in the order of happening the transactions and when the transactions are happening in the business, they do not happen in the similar form or the similar type of the transactions taking place in one series, different types of the transactions. In the morning, you are purchasing a raw material, you are making the payment for that we are making the payment for wages, we are buying some lubricants, we are buying stationery, we are paying for electricity bills, we are say writing cheques for may be some other kind of selling and distribution expenses.

So, different kind of transactions are taking place and all these transactions in the order of happening that is called as the chronological order, they are recorded in the journal, but we are not able to find out that what is the balance in one particular or how much what is the balance of funds under one particular transaction or one type of the transaction or the series of the transactions. Now, for example, the purchase of material, we are buying material every now and then today we purchased one truck load of material that is consumed in 2 days, after 2 days we again purchased another truck load of material and in between that lot of other transactions have happened in this process in one month we have purchased the raw material means any number of times, you can say 10 number of times or may be for the 12 times or 15 times a month, but they are not in the series means first when we purchased material after that many other transactions happened then we again had the transaction about buying the material then many transaction then material. So, it means at the end of the month, if you want to know what is the balance in the material account how much material we purchased, how much material was supplied for the production process and how much is the balance left with us if we have not prepared the second book of accounts, then what we have to do?

We will have to count it that say we purchase one truck load of the material maybe the 100 units of the material we purchased and out of that we consumed 80 units and 20 were left in the stock then we purchased another 100 units after that 40 units were used and the 60 were left in the stock it means we have to count it and counting will take the time. So, what will happen? While preparing the ledger, we post the transactions recorded in the journal in the ledger and in the ledger we open different types of the accounts and similar transactions are put at a common place under a common account and these accounts are periodically balanced.

So, that we are able to know it what is the balance of one particular account as I told you there are number of accounts 3 they are broadly divided into 3 categories personal account, real account and nominal accounts. But real accounts can be any say for example, cash is a real account buildings are real account material is real account any asset which can be touched observed or seen that is a real account. Now, it is a balance in the cash account to find out that balance we will have to prepare a cash account in the ledger and then to balance that account.

So, that if you have properly prepared the cash account in the ledger and balanced it properly regularly it means we can at any point of time we want to know about the cash balance we can open the ledger account and we can know about it. So, it means we have a T form of account when you talk about the journal the format I am I will be preparing it later on also, but here I will be talking about the format of the journal is something like this we prepare here and here we record the transactions then we here put the LF ledger folio and then we put here the amount then we have a 2 columns of putting the amount here debit and credit. So, this is a rough summarized format of preparing the journal.

So, once all these transactions are recorded in the journal they are posted in the ledger for the proper classification the objective of preparing the ledger is the proper classification of the accounts or the different accounts which are there in the journal similar transactions belonging to similar type of accounts having to be taken to the next book of account that is the second book of accounts that is called as the ledger. And in the ledger we have the T format kind of a thing, we divide this into two equal halves and here we put here that this is the format of the ledger here we put the particulars then we put here the journal folio then we put here the amount and this is the debit side here again the particulars then it is the journal folio and then it is the amount and this is called as the credit side of the ledger account. In detail I will be discussing with you when we will practically prepare the journal and ledger we will be talking about these all formats and everything again, but just for the reference purpose I am sharing with you that first all the transactions in the order of happening in the chronological order they are recorded in the journal that is the first book of accounts and journal is also called as the original book of accounts.

And after that for the classification of the similar transactions at a common place under a common account we prepare the second book of accounts and that is called as ledger and under ledger the similar transaction for example, cash all the transaction relating to cash they will be put in under the one account, all the transaction relating to purchase of machines they will be put under the one account, all the transactions relating to a person X, they will be put under one account, all the transactions relating to person Y they will be put under one account and that will be periodically balanced may be regularly everyday daily balanced. So, that we come to know in the evening of any particular day what is the balance of cash account what is the balance of X account, what is the balance of Y account, what is the balance of machinery account, what is the balance of any other account. So, classification of the transactions recorded in the journal is done in the ledger.

Then after that we have the next statement in the accounting process after transaction journal and ledger the next thing is that is called as the trial balance. Now what is a trial balance and what is the purpose of preparing the trial balance. If you talk about the trial balance trial balance is basically an intervening statement between the important financial statements that is profit and loss account or the income statement and the balance sheet this statement is the intervening statement trial balance.

Trial balance is taking into account or recording the means this statement is prepared with the purpose of verifying that whatever the transactions are recorded in journal and whatever the transactions are posted in the ledger, they are recorded and posted in the correct manner correct manner means that numerically they are correct. What are the values recorded under different transactions, what are the values posted in the different accounts there is no mathematical error in that and if there is any mathematical error. .

Then that error will be caught by preparing this account this particular not account, but a statement which is called as trial balance which will be called as trial balance. Trial balance means that we balance the ledger accounts and balance is only balances which are of the 2 category, one are the debit balances other are the credit balances. So, we prepare the trial balance is prepared this way and here we put the, this is the say format of preparing the trial balance here we write as head of account this is head of account and here we put the balances here we put the balances and these balances are debit balance and the credit balance.

These balances are debit balance and credit balance, because we follow the double entry accounting system and I told you many times under double entry accounting system that any particular transaction it has 2 accounts. So, we are means one effect of that transaction means that is the debit effect and the second effect of the transaction is the credit effect. So, if any particular account means we are debiting with the same amount we are crediting the corresponding effect of that account for example, we have a transaction here that raw material purchased raw material purchased on cash for 100 rupees it means in this case we have to record these transactions in the books of accounts very simple we will be recording that it has 2 aspects one is the raw material and second is the cash.

So, it means what is happening raw material is coming into the business and cash is going out of the business accounts. So, it means it has a double effect and finally, your raw material amount will increase by 100 rupees and this cash account will go down by the 100 rupees. So, it has a same effect.

So, the balance of the raw material will be debit balance and the cash is going out. So, it will be having a cash account will be having a credit balance. So, it means if you write here raw material account.

So, we will be writing 100 here and if you write here if there is no other transaction it is 100 here as cash. So, if you total it up the total of both the sides is equal. So, it means trial balance is tallying.

So, it means if all the balances are means all the transactions are rightly recorded in the journal they are righty posted in the ledger and rightly the all the balances are rightly calculated then these balance when we will put into the trial balance then total of the debit balance will be equal to the total of the credit balance. So, by tallying the trial balance both the sides being equal in the trial balance we can be sure that at least there is no arithmetical mistake in recording and posting of the business transactions in the journal and in the ledger. There can be number of other kind of errors say for example, there is a error of omission there is a error of commission there is a error of principle different types of the errors are there, but arithmetically these transactions are accurately recorded in the journal they are accurately posted in the ledger, and there is no problem as far as this process is concerned that has been rightly taken care of and there is no arithmetical mistake.

For example if you write here that raw material account is debited with 100, but wrongfully we have we have forgot to put one more 0 here and we wrongfully put here as a rupees 10. So, what will happen here this side will be 100 rupees this side will be 10 rupees. So, what will happen?

A balance of 90 rupees will come here and this trial balance will not tally. So, by preparing this trial balance we means from the ledger, we can directly prepare the profit and loss account in a balance sheet, but we prepare this statement that when we prepare the trial balance, we can be sure that at least there is no arithmetical mistake in recording the transactions of the business and posting them into ledger and from this trial balance, whatever the profit and loss account you prepare or the balance sheet you prepare there that will be these 2 statements will be depicting the right and the clear view of the business and financially or if we talk about the arithmetical values or may be numerically whatever the figures are taken to profit and loss account and balance sheet they will be correct. So, this is a intervening statement and statutorily this is a very very important statement, without preparing the trial balance we cannot move forward to prepare the income statement and balance sheet right from the ledger you cannot prepare the profit and loss account and balance sheet we will have to prepare the trial balance and we have to make sure that yes all the transactions are arithmetically correct and all the values have been rightly been debited and credited.

So, that debit and credit balances are equal and on the basis of that whatever the profit or loss we work out that is going to depict the true and fair view of the business and the right and the proper financial position of the business. So, this is something we talk about the accounting process the first 4 steps of the transaction journal, ledger and trial balance and after this we will be talking about the profit and loss account and the balance sheet and some other statements and that we will be talking in the next part of discussion. Thank you very much.