[Music] Hey guys, welcome back to the show! Thanks for tuning in. My name is Mike, this is my whiteboard, and today we're going to be talking about three adjustments for the short call.

If you missed yesterday's segment, we actually talked about the short call trade entry checklist and what we look for when we're getting into that trade. So, if you missed that, you can just click on "Find Shows" at the top, hold down to Mike's Whiteboard, and it'll be the last one there. But today, we're going to be talking about adjustments.

So, what happens when my short call is tested, or maybe if implied volatility changes? Well, I'm going to walk through a few different examples, and we're going to talk through why the changes and adjustments are beneficial and what to keep an eye on throughout those trades. So, let's start off with just a review of the very first trade in the short call.

When we're looking at a short call, it is a bearish assumption, so we want the underlying to go down in price. When we're looking at a short call, we're looking to just sell a naked call. Let's say we're looking at the 45 days until expiration window, which is optimal for selling premium.

Let's say we can get 10 points out of the money, or 10 points above the current stock price, and collect one dollar for this short call here. So, when we're selling premium, the first thing we need to remember is that the max profit is just the amount of credit that we receive. With a short call, if I'm collecting one dollar and that controls, theoretically, 100 shares of short stock, then my max profit is 100.

I would just multiply this value by 100 to get my true value in dollar form. So, my max profit is 100, which means that my break-even is going to move to 71. Whenever we're selling premium, we move our break-even in a beneficial manner.

So, this one would be to the upside. If I was selling a put, it would move my break-even to the downside, but since I'm selling a call and it is acting as a theoretical short position, my break-even is going to be improved to the upside here. Because the worst-case scenario is that the stock price actually moves up.

With short calls, it's a little bit different than with short puts when we talk about max loss, because our max loss is truly undefined. With a short put, which is just the opposite strategy (where I would want the underlying to go up), a short put is different because it does have undefined risk, as we don't know where the stock price will go. But we do know that a stock price cannot go below zero, so our risk is capped if the stock price goes to zero, which would be our max loss if we were to sell a short put.

However, with a short call, our loss is when the stock price goes up, and as we know, there is no cap to the upside when we're talking about stock price movement. This stock price could go from 60 to 100 overnight, or maybe from 60 to a thousand over the next few years; there really is no cap, so the max loss is truly undefined. Now that we've got the opening trade down, let's talk about a few adjustments that I might make if the stock price moves a certain way.

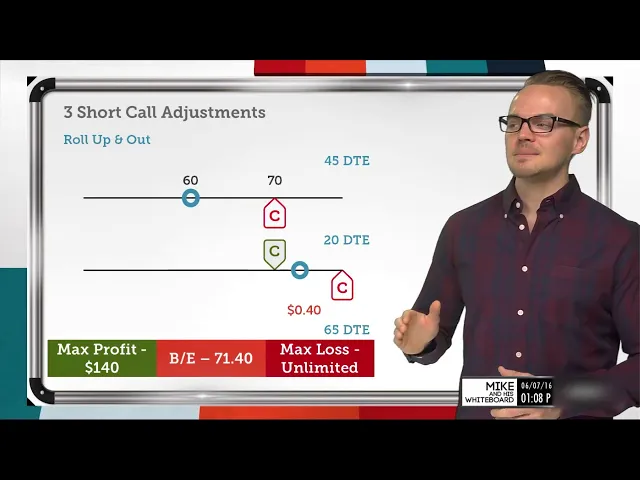

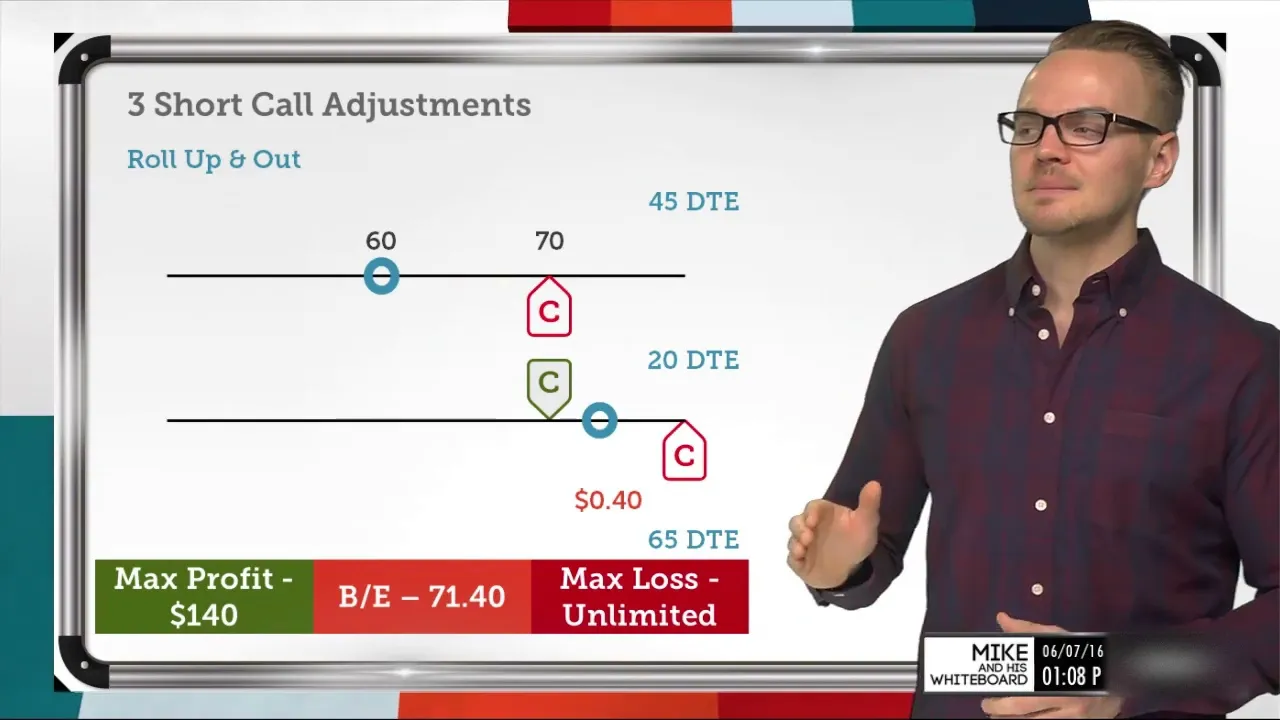

So, on the next side, we're going to talk about what happens when the stock price goes up, and we're going to highlight just simply rolling the option out in time. So, this top line is the exact same trade we just covered, and the bottom line is the adjustment I would consider making if the stock price was testing the short call. One thing that we know, and one thing that's beneficial with short options and naked options, is that we can always roll out in time for a credit if we keep that same strike in place.

So, here we've got that exemplified, and we're going to be looking at potentially closing our current expiration and opening up a new one in the next expiration cycle. Let’s say I open the trade at 45 days and 25 days went by, and the stock price rose above 70. Well, I'm going to have to buy back my short call here, which is this call listed here, and I'm going to sell a new call option, which is going to be rolling.

Whenever we're rolling, we're basically just buying back our current position and selling out or opening up a new one. When we're talking about rolling a position, so here I’m closing out the same expiration; there are only 20 days left on this one, and I'm looking to sell it out in time. So, I'm selling a new expiration cycle with 40 days to go, and let's assume that I can route this for a 50 cent net credit.

Since I can collect an additional 50 cents, it actually benefits my break-even and increases my max profit if this option actually expires out of the money. One cool thing about rolling naked options is that we can usually roll it for a credit when we're rolling it out in time, and that's because we have the same intrinsic value in both of these options. So, let’s say the stock price is at 72.

Our options are two points in the money, so my long call, or the long call that I'm buying back, is going to be trading for at least two dollars, and this option that I'm selling out is also going. . .

To be trading for at least two dollars because it has the same intrinsic value. Even though both of these are in different expiration cycles, it doesn't matter because intrinsic value is really just the difference between the in-the-money option and the current stock price. So if the stock price is at 72, both of these options have two dollars of intrinsic value if we keep it on the same 70 strike.

So what does this mean for the position? Well, there's still 20 days to go, so let's say I'm buying back my short option for three dollars. So I've got two dollars of intrinsic value and one dollar of extrinsic value.

But what I can do is, instead of just buying that back for a loss, I can sell out a new one with 40 days to go, and I can collect a net credit of 50 cents. So what does this mean? That means that this option is worth three dollars and fifty cents.

If I have to buy back this option for three dollars, and I can sell this option for three dollars and fifty cents, that's where I get this net credit of 50 cents. And that's why I can use that net credit to increase my max profit eventually and move my break-even just a bit. So instead of my break-even being at 71, now it's at 71.

50 because I collected a net credit and improved my max profit to 150, even though I have a loss on my old position. If this option expires out of the money, since it's really worth three dollars and fifty cents, even though we're getting a net credit of 50 cents, it's worth three dollars and fifty cents. So the loss on this position is actually embedded in this option here.

If the stock price comes back down, and let's say it goes to 68 by expiration, this option that's worth three dollars and fifty cents would be expiring worthless, which would knock out my loss on my old position and let me realize the max profit of 150 on my new position, including the roll that we just did. So that's how you can think about rolling, and that's why when we're dealing with naked options, we can always roll out that same strike out in time because there's always going to be more extrinsic value when there's more time until expiration. We're allowing the other side of that party to hold the option for a longer time.

Since extrinsic value is always going to be more with further-dated options, we can always roll it out in time for a credit. If we have the assumption that the underlying is eventually going to go down, we can do that easily and benefit from our breakeven, increasing our max profit. Although we would be at a lower probability of success since we're basically selling an in-the-money option, we would need the stock price to now move below that to reach our profitability.

But all in all, if we want to roll it out indefinitely and hopefully eventually this option would expire out of the money, we can do so easily with naked options. And of course, my max loss is still unlimited because I'm buying back this option, but I'm selling out a new one. So I'm still holding the theoretical short shares or short 100 shares of risk with this short call here.

So let's go into the next slide, and we'll talk about another thing we can do with that same exact situation. If we're not, if we don't want to keep that in-the-money option and we actually want to move out of the money again, what we can consider doing is rolling up and out. So what we would do is look at the same thing.

Of course, we'd have to buy back our losing short option here. So let's say we're buying back the option, but instead of going to an expiration on the same strike with 40 days to go, maybe I can go out in time to 65 days and move my call out of the money. Since we know there's going to be more extrinsic value associated with this, we can actually move our strike out of the money.

We probably have to add a lot more days to do so, but we can certainly do so for a credit. So if I'm getting a net credit of 40 cents, and let's say we had the same scenario where the stock price was at 72, I'm buying back this option for three dollars. If I can collect a net credit of 40 cents, that means that this short call is worth three dollars and forty cents.

Now, of course, out-of-the-money options are made up of entirely extrinsic value, so we probably had to go far out in time to 65 days to make sure that we were collecting more than that three dollars. So with this option specifically, we were able to go out of the money and collect three dollars and forty cents total for this option, which brings me to a net total since I'm buying back this option for three dollars and forty cents. So now my new max profit would improve as well, and my break-even would improve as well.

So my max profit here would be 140, which is really just my original credit of 100 that I received, and then we add on the net credit of 40 cents. My break-even would improve to the upside as well, so my breakeven would move from 71 to 71. 40, and my max loss is still unlimited.

I bought back the option, and I opened up a new one, so I'm still holding one contract of this. Give me that unlimited loss potential if the underlying continues to go up, as there's no cap to the upside. But I also want to talk about what we can do if we're presented with an opportunity.

Some might see this as a marked loss on the next slide, but we're going to talk about implied volatility and how we can scale into it. So, let's say we had a nice implied volatility level when we originally had the trade on. We sold this call for a dollar, and we had a nice volatility level.

But over the course of three days, let's say implied volatility expanded drastically. So maybe the stock price dropped a tiny bit, but implied volatility expanded drastically, and it allowed us to sell another call on the exact same strike for a dollar twenty, as opposed to just one dollar. This is an opportunity that we can take into account.

We're looking for opportunities with implied volatility. So, with implied volatility, we know that it's a reflection of the option prices. When IV is high, option prices are going to be inflated, and when IV is low, option prices are going to be deflated.

So if we have an opportunity to actually sell another option for twenty dollars more than we did originally, and only three days went by, maybe we'd look into scaling into that. Let's say my normal contract size is five contracts. This is why we usually trade smaller than that, because even though I could have just laid out five contracts right here, if I only lay out one or maybe two, and implied volatility increases, now I actually have an opportunity to get into the same position but at a better price.

So that's why, when we're looking at our contract size, we actually usually go into a trade smaller than that, so we can leg into more opportunities here. So let's say I was able to do that. I sold another call on the seventy strike in the same exact expiration, and now I basically have two contracts on the seventy strike, and I've collected a total of two hundred twenty dollars if we just add these together, which means that if these options expire out of the money, my max profit would be two hundred twenty dollars.

Now, what's interesting is that the break-even doesn't change too much, and that's because of the fact that we're doubling down on the contracts. So when these options move in the money, our rate of loss is going to double as well. What we have to do to calculate our break-even, since we have two contracts here, is basically calculate our total value of two hundred twenty dollars that we collected and divide that in half because every point that the underlying moves against us, we're actually going to lose two hundred dollars now as opposed to one hundred.

So our break-even isn't improved too much; it's improved by ten cents. But really, the opportunity here is the max profitability, and what we really need to focus on is the unlimited loss. What we basically just did is we multiplied that by two.

So now we have unlimited loss to the upside, and we have to consider the fact that we now have two contracts as opposed to one. This is an opportunity for us because we can increase our max profit, but we also want to be aware of the unlimited loss that we're putting ourselves at with the short call. So let's wrap all this together with some takeaways.

The very first takeaway is that trading small allows us to scale into these opportunities. So if we have a normal contract size of maybe five contracts, maybe I'll look at going into the first option trade as two contracts or maybe one, so that I can see what happens with that underlying. If it gives me a better opportunity to scale into more, I can do so, and if we're uncomfortable with in-the-money options, we can actually roll up and out.

Now, of course, if we want to roll up and out, we're going to have to probably add a lot more time since we need to make sure that the value of the new option we're selling exceeds the value of the option that we're buying back. That's how we create a net credit for a roll. So to do so with an out-of-the-money option, we probably have to add a lot more time to get that value, as you saw.

And definitely be aware of the unlimited risk to the upside with naked calls. Now, of course, we do have a lot of opportunities, but when we're looking at the opportunity for failure with naked calls, it is truly undefined. So be aware of that when trading naked calls.

Thanks so much for tuning in! My name is Mike. If you've got any questions or feedback, shoot me an email here, or you can follow me at @dotradermike on Twitter.

Stay tuned, though; we've got Jim Schultz coming up next.