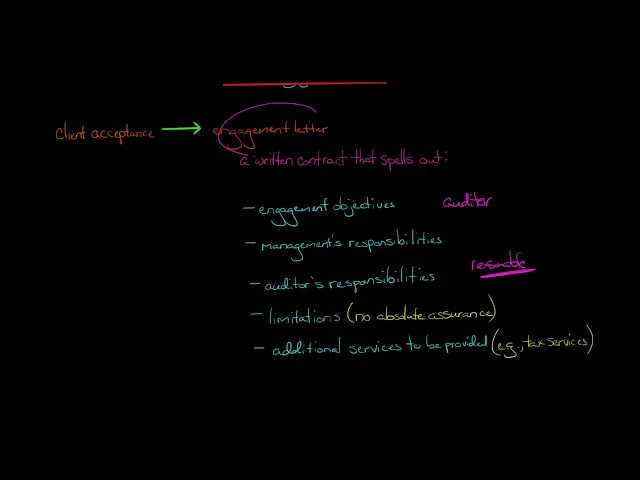

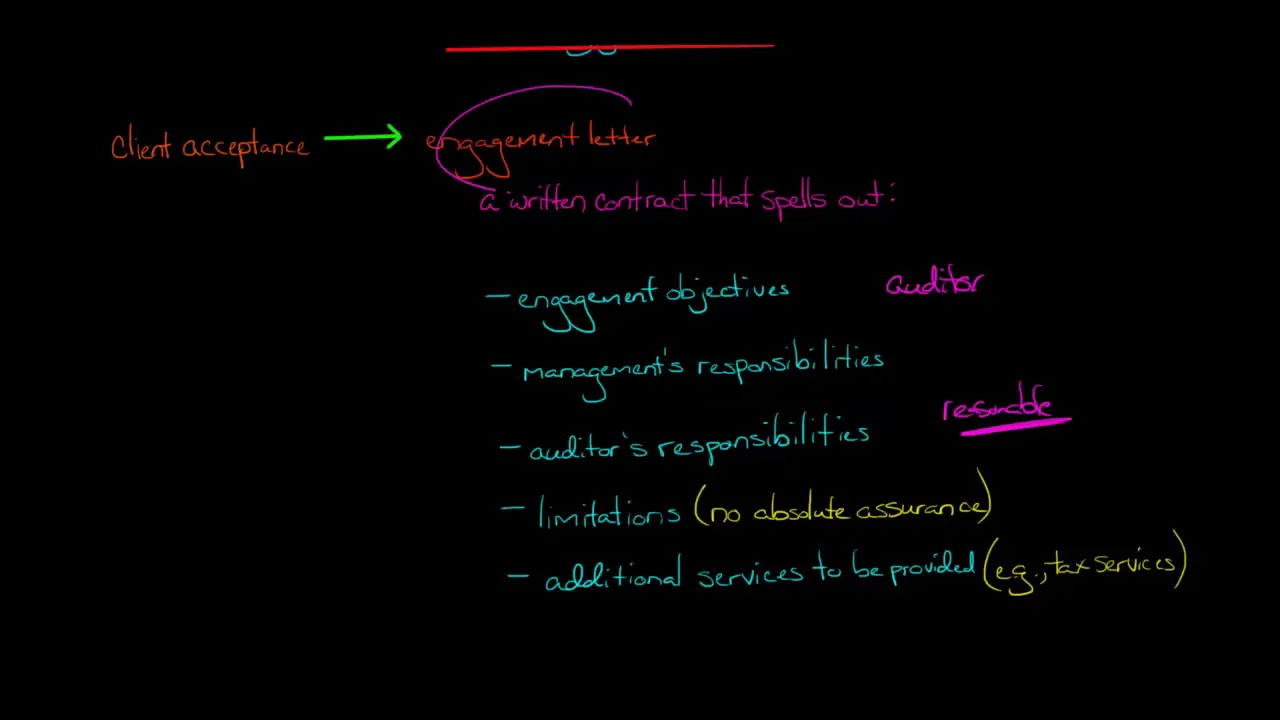

after an auditor is decided to accept a new client or continue with an existing client the auditor needs to formalize that relation through something called an engagement letter the engagement letter is gonna spell out exactly what are the responsibilities of the auditor and what our management's responsibilities as well for example we talk about the engagement objectives which is to perform an audit that's what the auditors doing but management would take responsibility and it would say management's responsibility is the financial statements it's not the auditors responsibility the auditor is going to conduct tests in an attempt

to determine with reasonable level of assurance whether the financial statements are free from material misstatement whether due to error due to fraud so that's what the auditor is gonna do but ultimately the financial statements are management's responsibility and that's gonna be spelled out in the engagement letter then also the engagement letter is going to talk about any limitations for example as I said we are not guaranteeing as the auditor let's say where the auditor of General Electric we are not guaranteeing we're not providing absolute assurance that general electric's financial statements are fine and don't have

material misstatements we acknowledge the possibility that even though we're doing we're sampling different transactions and we're attempting to do these tests to get an ascertain whether management is being truthful about the financial statements and whether it's material misstatements we are not guaranteeing we're saying look upfront we are not providing any absolute assurance we're providing reasonable level of assurance and then if the auditor so let's say we're the auditor and we're gonna provide some additional services to General Electric like for example some tax services or something like that then we would also spell that out in

the engagement letter and say okay this is what we plan to do