From Wall Street to rural America. Today's AI is the economy and markets have priced it like a miracle that can't fail. Investors are really banking on incredible growth, Microsoft meta alphabet.

They are just committing billions and billions of dollars to capital expenditures and expected to continue to, you know, raise those numbers over time. The AI boom is more than just software. It's construction.

So that's building out the data centers, that's securing the energy that's needed, the water that's needed. But in this burgeoning industry, what goes around doesn't necessarily come around. A precarious investment strategy is emerging Multi-billion dollar circular deals.

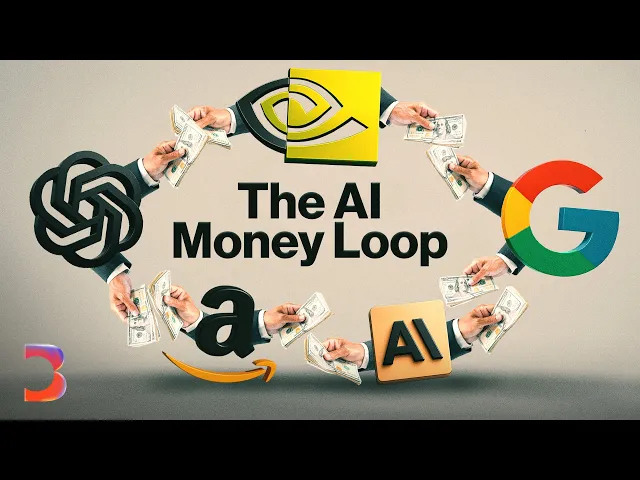

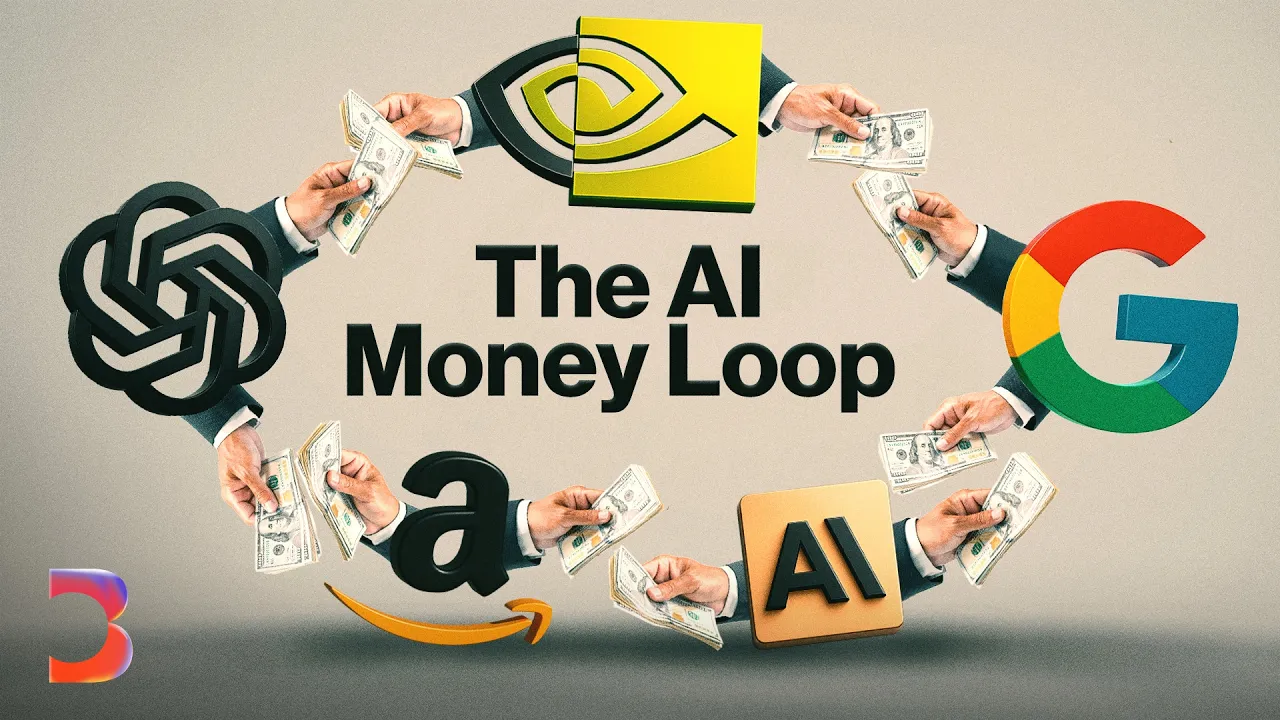

Nvidia will invest as much as $100 billion in open ai. The merry-go-round of money continues. Huge, huge sums of money are just being passed between these enormous companies that are, are pouring hundreds of billions of dollars into the promise of ai.

And the promise is huge. About 80% of US businesses use ai. So this is a structural shift, electricity or the internet, but AI with all its potential remains largely unproven for profitability.

Probably the biggest question in San Francisco right now is, are we in an AI bubble? And if we are, then well, how big is this bubble? And how bad would it be if and when it does burst?

So is this the dawn of a new age of AI powered growth, or the biggest bubble ever? A circular deal is when companies are basically blowing money ,product services, in between two of them, Nvidia has said it's going to invest up to a hundred billion dollars in OpenAI. At the same time, OpenAI is a major customer of NVIDIA's services of their chips.

To make it even more complicated, there are also sort of other middlemen. One example is Oracle. OpenAI sometimes will lease compute from Oracle.

And so you have Oracle being a customer of Nvidia. So you can see how there can be more sort of arrows back and forth between these companies. But Nvidia, OpenAI and Oracle are just part of the web.

The full picture entails a who's who of the AI landscape. This money is kinda spinning around the same companies, and that's why people are worried. I don't think there's anything inappropriate about that in principle.

Now, if you start stacking these where they get to huge amounts of money, then yeah, you can. You can, you can, you can overextend yourself, of course. It becomes kind of symbiotic.

And I think that's sort of the concern that's cropping up now is that if one of those companies stumbles or doesn't do well, does the whole thing fall apart? A lot of this investment is going straight to the build-out of data centers across the nation. We're really in an infrastructure build out arms race.

Have a look at construction spending in 2025. It's down in most sectors, but not data centers or power stations. We're seeing a lot of companies that are sort of the picks and shovels of the AI industry.

They're out there. Actually, you know, digging into the ground. One recent estimate from Morgan Stanley predicts that companies will spend $3 trillion on AI data centers.

That is obviously a major bit. If you're in the business of selling picks and shovels, you are living it up. You are getting all the money you need, and there's more demand than you can meet.

We're currently in a facility that was once upon a time, a textile facility, one of the largest ones on the eastern seaboard, about 1 million square foot. We realized we could actually repurpose it as a data center. There is an insatiable demand for building data centers, for making sure that we have the power to build the data centers, the megawatts, the infrastructure and the expertise.

We don't see any slowdown in that for a long while. It comes to artificial intelligence. Time is not your friend.

So if you can get up and running in six months using a retrofit format versus a greenfield format, which is starting from scratch, which takes up to two years, that's a much better proposition. All these data centers need power. The growth in utility costs is outpacing inflation.

Utility companies have done really well, especially ones that are providing energy to data centers. Construction stocks have done well, But building fast isn't always built to last. You don't just build a data center, switch it on, forget about it, and make money.

You have to keep on investing to keep that technology working, otherwise it'll quickly become useless to the people you want to sell it to. And so far, all major AI projects are operating at a loss. The problem is, every time someone uses chat, GPT open AI likely loses money.

Those Open AI's and Anthropics of the world are not yet profitable. Sam Altman says Open AI should be able to break even around 2029, 2030, given the amount of cash that company's burning through right now, and the amount it still needs to spend to build the data centers and pay for the computing power to do what it wants to do. That feels like a tall order to me.

There's some concern about whether the AI startups are actually able to pay their bills when they're racking up these huge commitments to spending on data center infrastructure. And these AI data center companies, they are the kind of canary in the coal mine. They are the ones where we perhaps see on their balance sheet any first sign of companies pulling back from needing as much AI data center capacity Right now, all the companies, they're all saying that the demand for AI products is really, really high.

If that were to change, if demand were to suddenly weaken, that would become an issue. To understand the stakes of today's ai boom, you don't need a crystal ball. Just a quick trip down memory lane, you've got mail in 2000, the dot com's promised a brave new world.

Instead, we got wiped out savings, empty office parks, and $5 trillion in vanished value. The worst hit shares around the world have been the technology stocks, including the. com companies.

Even the strongest companies in that era took years to recover. Amazon, one of the big, great famous survivors, its share price, didn't recover for another eight years after the. com crash happened.

Cisco, one of the picks and shovel companies, it took them 25 years before their stock price recovered. There are definitely some similarities. One is that there is circular deal making.

In both instances, the question is, is this bubble gonna get to a level that goes beyond just kind of the normal ups and downs of tech booms, but actually has major consequences for the economy? The dotcom boom was devastating for the economy, but I don't think it will compare to the far reaching effects of the AI boom collapsing. The money pouring in has been a huge contributor of growth to GDP helping boost a US economy otherwise hampered by tariffs and inflation.

Everyday Americans are exposed to this risk via 4 0 1 Ks and other investment accounts that hold stakes in many of the big tech companies participating in the spending spree. So does that mean the AI bubble is too big to pop? There's definitely this question about are these companies becoming too big to fail?

If they were to go down, that could have not just economic consequences. There is a suggestion that this might be like the global financial crisis where huge financial institutions needed money to survive to prevent a wider collapse of the economy, then that's obviously a far greater problem for the US economy. But despite these stakes, many remain bullish on AI because of the evolving nature of the technology itself.

In the dotcom boom, there were companies that were laying fiber optic cable, like subsidiaries of a company were basically all spending in a circle, you know? And it did contribute to the. com bubble popping.

But after a while, that became the backbone of internet broadband. And that unused part of all the fiber optics that were built in the nineties actually ended up being extremely important for the internet. And so we think with respect to data centers, if there is potential excess capacity that's being built, those data centers will eventually be used.

There's a scenario here where AI takes longer than we think, and therefore the strongest companies, sure they'll survive, but in the meantime, there might be a huge hit to their valuations. Ultimately, this technology is not going to burst. There are certain companies that will not make it, but AI itself is not a bubble.

There are real products. It's clearly the biggest gamble that Wall Street has ever made. And this is a street known for its gambling.

This is the wager to end them all.